Key takeaways

-

Two years after the first CAR-T cells were approved by the European Medicines Agency, CAR-Ts have begun to gain momentum in Europe.

-

Update is relatively low, but momentum is gaining as a result of positive reimbursement decisions, emerging infrastructure and referral networks, growing clinical experience and advocacy, mitigation of safety concerns and a growing European manufacturing base.

-

Further progress is required to address underdeveloped payment mechanisms, concerns about manufacturing timescales and reliability, the effectiveness of referral networks and institutional capacity constraints.

-

Investment and outcomes could also be improved in Europe through consensus on patient selection, CAR-T’s position within treatment paradigms and whether CAR-Ts are substitutes or bridging therapies for allograft.

-

Despite these challenges, enthusiasm in Europe remains high and CAR-Ts are gaining momentum. Pharmas, healthcare providers and payers should focus on four areas to accelerate adoption: logistics and manufacturing, evidence and experience, treatment ecosystems, and reimbursement.

In August 2018, CAR-Ts reached a major milestone in Europe when the European Medicines Agency (EMA) approved the first two CAR-T cells, Novartis’ KYMRIAH and Kite-Gilead’s YESCARTA.

Nearly two years on, CAR-Ts have begun to gain momentum in Europe but uptake remains relatively low, reflecting limited clinical trial experience, complex manufacturing and administration processes, high costs, and unresolved logistical issues.

In this Executive Insights, L.E.K. Consulting reviews progress to date, outlines barriers to uptake and identifies potential catalysts for accelerating European CAR-T adoption.

Encouraging signs of momentum

Key opinion leaders interviewed by L.E.K. reveal the excitement of the European medical community in the potential benefits of CAR-Ts. As one leading U.K. haemato-oncologist commented, “Four to five years ago, having commercially available CAR-Ts was unthinkable. I thought it would be far too much of an investment in time, energy and resources, but in fact, all parties have been very engaged and willing to make this a reality.”

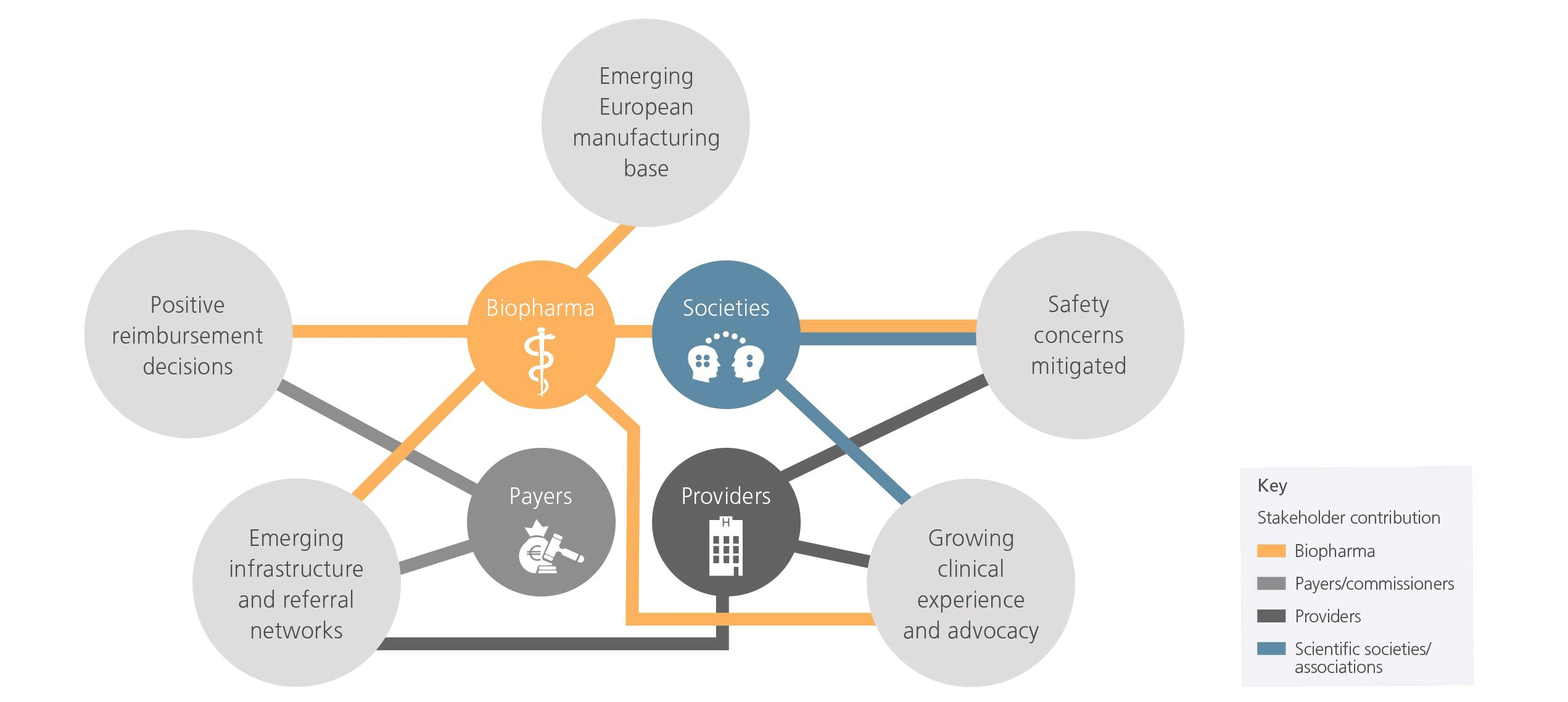

As CAR-Ts approached launch, there was consensus around key challenges such as reimbursement and safety concerns, but five drivers of momentum have begun to address these barriers (see Figure 1).

1. Positive reimbursement decisions. Pharma and payers have demonstrated preparedness, cooperation and innovation in overcoming anticipated reimbursement challenges. For instance, the U.K.’s National Health Service (NHS) approved funding for KYMRIAH just one month after EMA approval (among the fastest in U.K. history) and negotiated a confidential discount for YESCARTA soon thereafter. Italy developed a novel ‘payment for results’ reimbursement approach, whereby payments are made in three instalments based on patient response to treatment. German and Spanish payers approved reimbursement through managed entry agreements, while France approved reimbursement contingent on annual re-evaluations using real-world data. Across all these examples, pharma has been flexible in its approach to working with payers.

2. Emerging infrastructure and referral networks. There are promising signs of providers building infrastructure to enable referrals and geographically equitable access. The European footprint of CAR-T delivery centres (institutions authorised to administer commercial CAR-Ts) is growing fast, expanding from ~30 to ~85 centres between February and September 2019 alone. Progress is most notable in the U.K., where NHS England worked closely with pharma and JACIE1 to select and prepare nine geographically distributed centres for CAR-T delivery by the time of approval. The NHS also established national CAR-T clinical panels to coordinate referrals, triage patients and determine eligibility.

3. Growing clinical experience and advocacy. Early adopters are establishing themselves as European centres of excellence, whilst European haematological societies2 have emerged as key drivers of CAR-T adoption, publishing Europe’s first implementation and clinical guidelines in 2019. Meanwhile, the development of a pan-European CAR-T patient registry is increasing the availability of real-world data.

4. Safety concerns mitigated. Providers, pharma and scientific societies have been successful in overcoming safety concerns. Acute adverse events associated with CAR-Ts are becoming increasingly manageable as routine practices are established. This is enabled by the growing adoption of JACIE standards across CAR-T centres and pharma’s proactivity in driving education on safety management.

5. Emerging European manufacturing base. Pharma has invested in European manufacturing sites to increase capacity and reduce historically long turnaround times. Novartis built a new facility in Switzerland, established a partnership with Germany’s Fraunhofer Institute, and acquired CellforCure, a French contract manufacturer. Kite-Gilead is building a CAR-T manufacturing facility in Amsterdam.

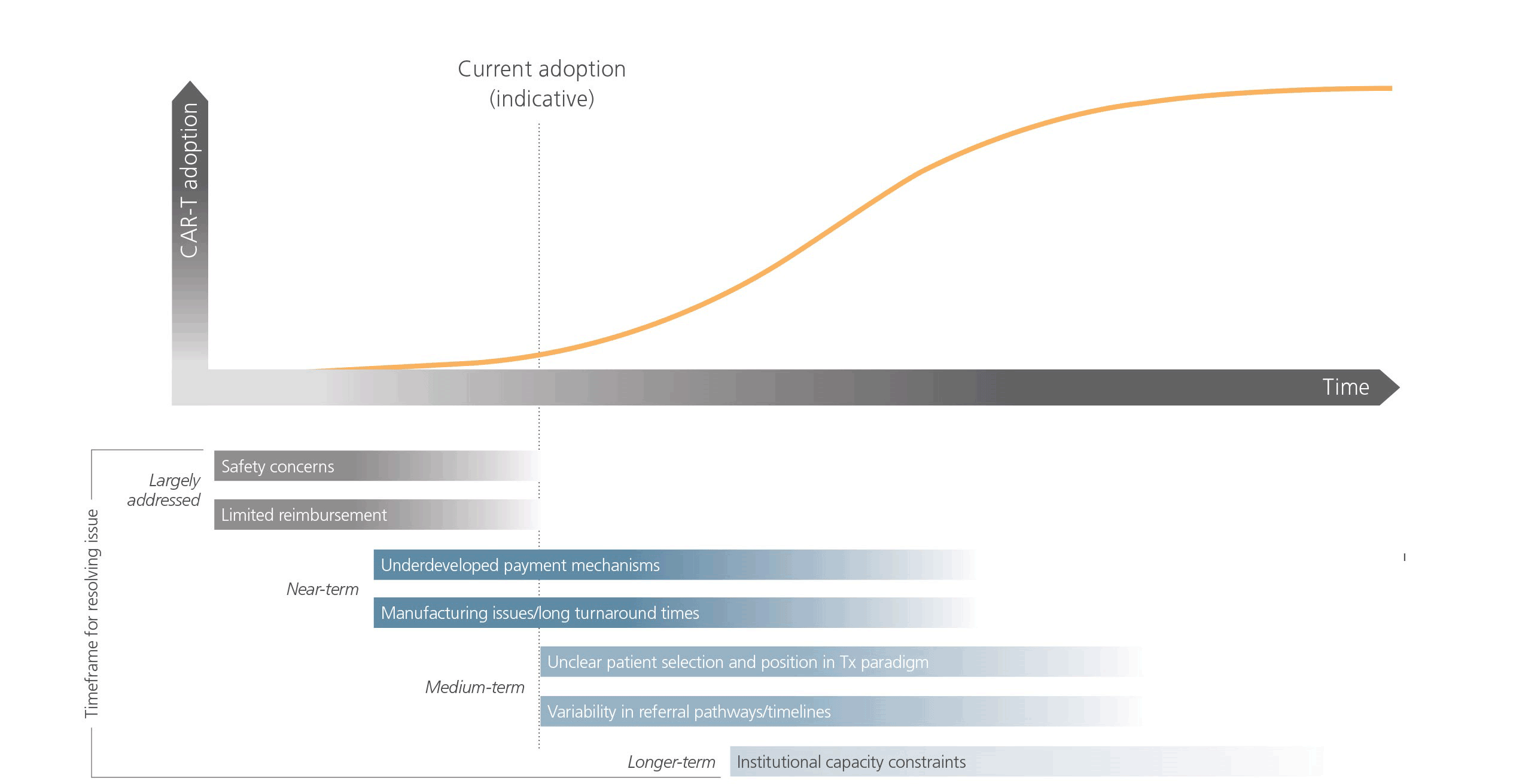

Inefficiencies and uncertainties hold back adoption

Despite encouraging signs, pharma and other stakeholders have been conservative in introducing CAR-T into Europe, focusing on building expertise and early positive experiences in a small number of highly specialised centres. While early barriers have been overcome, the nature of issues faced by CAR-T is evolving as it reaches the next stage of adoption. Several remaining barriers need to be resolved in the near, medium and long-term (see Figure 2).

Underdeveloped payment mechanisms, most notably in Germany and Italy, represent near-term barriers to adoption. In Germany, CAR-T reimbursement currently occurs outside the Diagnosis Resource Group (DRG) system, requiring centres to negotiate approval from insurers annually to receive payment. Italy’s current DRG system covers the cost of CAR-T cells but not all ancillary costs, leading to financial risk for centres investing in CAR-T.

CAR-T manufacturing is also seen as too time-consuming and at times unreliable. U.S.-based manufacturing leads to longer turnaround times in Europe and the three-to-four-week turnaround time limits patient populations to those without progressive disease. Real-world data from an Italian centre suggests that nearly a third of eligible patients died of progressive disease while waiting for CAR-T cells. Industry leaders report that production delays have, at times, led to suboptimal experiences.

In the medium-term, further work is needed to determine markers that predict patient suitability, as Europe remains divided regarding patient selection and CAR-T’s position within treatment paradigms. There is also a lack of consensus on whether CAR-Ts are substitutes or bridging therapies for allograft. This is leading to suboptimal outcomes and the reluctance of some oncology centres to invest in CAR-Ts. One leading U.K. haemato-oncologist commented, “I’ve been slightly disappointed by recent data from the American Society of Hematology showing poorer outcomes in the U.K. relative to the U.S. We need to answer questions around patient selection to improve outcomes here in the U.K.” Furthermore, the anticipated entry of monoclonal antibodies for B-cell cancers (e.g., Roche’s mosunetuzumab and Morphosys’ tafasitamab) could complicate the clinical landscape.

Referral networks are still emerging across much of Europe. Centres have mixed track records in early identification and referral of CAR-T candidates — considered key for successful treatment. There is a need to educate physicians outside CAR-T delivery centres on referral protocols and the benefits of CAR-T, particularly in countries such as Germany, where many patients are treated by community-based physicians.

Institutional capacity constraints represent a long-term barrier to adoption. Logistical complexity and safety requirements limit CAR-T administration to a small number of specialised delivery centres, leading to geographic inequalities due to the concentration of these centres in urban regions. Authorising centres to administer CAR-Ts still requires a major investment in resources, time and training. Compared with U.S. centres, which have benefitted from more clinical trial experience, European centres must develop more experience to scale up operations.

Catalysing adoption

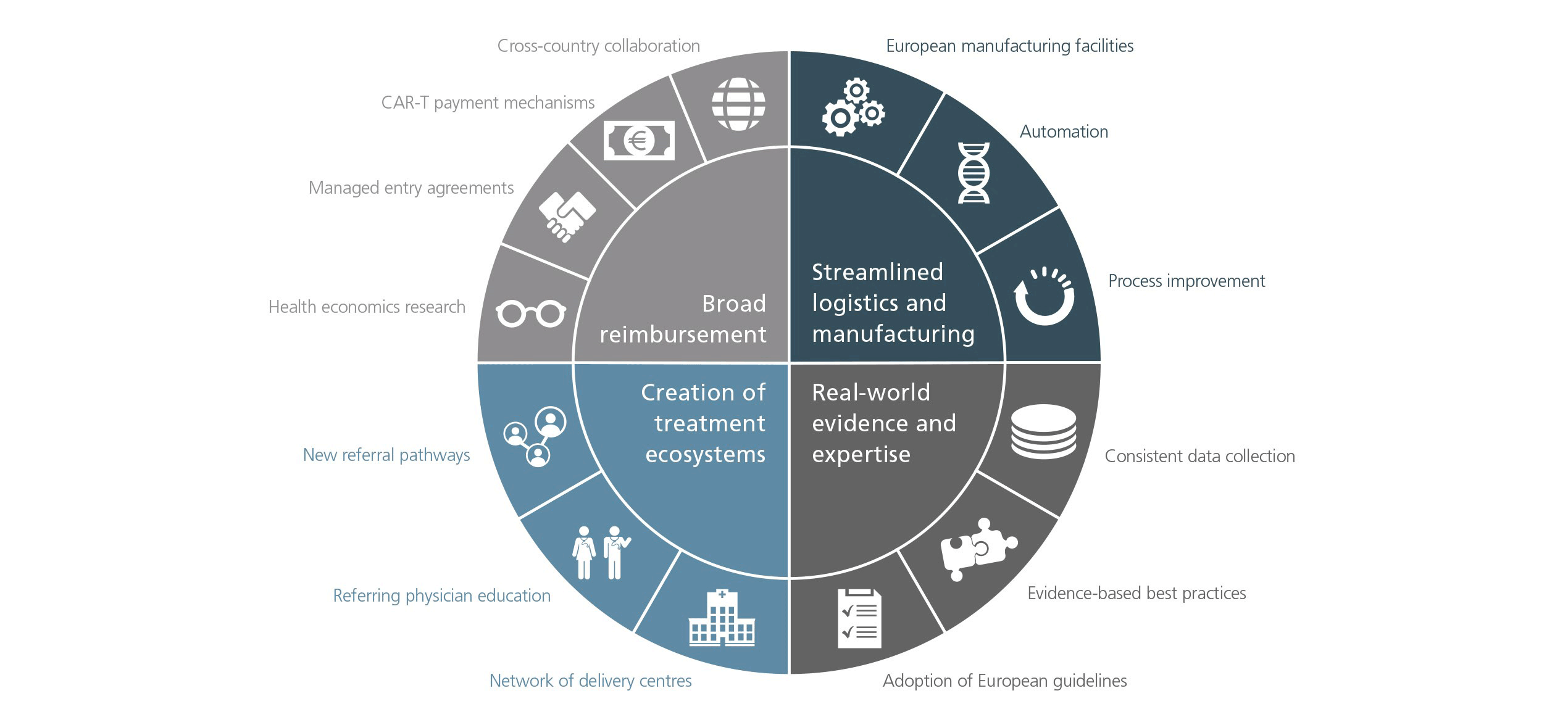

Despite these challenges, enthusiasm across the continent remains high and CAR-Ts are gaining momentum. We have identified four areas on which pharma, healthcare providers and payers should focus in order to accelerate adoption: logistics and manufacturing, evidence and experience, treatment ecosystems, and reimbursement (see Figure 3).

Streamlined logistics and manufacturing. Reduction in turnaround times should improve the CAR-T customer experience and inspire physician confidence. In addition to investment in European manufacturing facilities, increased automation has the potential to improve efficiency. Continued improvements in processes for coordinating therapy should also ease bottlenecks in the CAR-T patient journey.

Real-world evidence and clinical experience. If correctly harnessed, this has the potential to establish confidence in CAR-T’s effectiveness and cement its position in treatment paradigms. With consistent data collection, real-world evidence can be used to define best practices, optimise patient selection and improve outcomes. Collaboration between local key opinion leaders and European scientific societies will be critical in reshaping and ensuring broad adoption of guidelines as best practices emerge.

Creation of treatment ecosystems composed of an established footprint of delivery centres supported by well-established referral networks. Pharma can build on momentum by qualifying the next wave of delivery centres and by educating referring physicians. In parallel, institutions and health authorities can optimise referral pathways to reduce geographic inequalities and ensure timely referral.

Acceptance of broad reimbursement across Europe. For payers and pharma, continued investment in health economics and outcomes research, careful monitoring of managed entry agreements, and maintaining adaptability will be vital to securing future reimbursement. This will become increasingly important as indication expansions increase the burden on healthcare budgets. The implementation of appropriate payment mechanisms (e.g., DRG codes for CAR-Ts and ancillary costs) should minimise the administrative and financial burdens on institutions. Meanwhile, increased cross-country collaboration on health technology assessments, including efforts to introduce a pan-European framework, should mitigate challenges associated with assessing CAR-T’s value.

The future of CAR-T in Europe

To catalyse CAR-T adoption, the four areas identified above need to be tackled holistically through a multi-pronged strategy. Key considerations for biopharma seeking to succeed within the space include:

- Developing innovative ways to partner with providers, payers and the scientific community

- Identifying the right partners to bolster manufacturing and logistical capabilities

- Evaluating the use of digital technologies to streamline the treatment process

- Defining how best to utilise emerging real-world evidence

- Optimising pricing and design of managed entry agreements to minimise barriers to access

Pharma, payers and healthcare providers have already demonstrated enthusiasm and agility in introducing CAR-T to Europe, with many initial challenges overcome and a continued commitment to realising the promise of this therapy.

1 Joint Accreditation Committee of the International Society of Cellular Therapy and the European Society for Blood and Marrow Transplantation.

2 European Haematological Association and the European Society for Blood and Marrow Transplantation.

11032020121107