The integration of energy and information was first introduced as a concept nearly 10 years ago, and since then it has become desired for its cleaner and more efficient use of energy. Recent developments in China on smart grid development just might make this a reality. In this Executive Insights, L.E.K. Consulting sheds light on recent advancements in the energy internet and its potential for growth in China’s energy industry.

The energy internet — an open platform

The concept of the energy internet was first introduced by Jeremy Rifkin in his book “The Third Industrial Revolution,” published in 2012. The author outlined four main features in the energy internet:

- Leveraging renewable energy as a primary energy source

- Allowing large-scale distributed power generation and energy storage

- Enabling wide-area energy sharing and an energy prosumer (producer and consumer) to emerge

- “Electrification” of the transport system

The energy internet could bring about a new model inside the energy industry. This model, through the close integration of energy and information, would ensure a cleaner and more efficient use of energy. It could enable a two-way exchange of both energy and information by leveraging advanced information technology, intelligent terminals, and systems that can upgrade traditional power grids into new intelligent platforms.

Recent development of the energy internet in China

In China, the State Grid Corporation of China has proposed the concept of a “Global Energy Internet.” It is based on having a smart grid connected to an ultrahigh-voltage power grid that could potentially deliver clean energy worldwide.

However, most experimentation in this field has been carried out by distributed energy and micro-grid integration. For example, GCL’s distributed micro-energy network and ENN’s pan-energy network have both been able to establish regional smart-energy networks capable of balancing energy needs within the network, achieved by companies trying to extend their reach within their industrial value chain.

Drivers of the energy internet

Energy internet advancements can be attributed to the increased emphasis on sustainable development, the continuous breakthroughs in energy technology, the gradual opening up of the power market, and continued regional economic and energy integration.

Sustainable development: China raised its own emission reduction targets in the Paris Agreement under the United Nations Framework Convention on Climate Change, with a goal of reducing greenhouse gas emissions by 40%–45% from 2005 levels and raising the proportion of nonfossil energy consumption to approximately 15%. We expect China’s renewable energy capacity to grow at a compound annual growth rate of 7.6%, reaching a 2,300 GW capacity by 2035. The installed capacity of renewable resources will account for 65% of total capacity.

Breakthroughs in energy technology: Photovoltaic (PV) and wind power efficiency levels have continually been raised. The current average domestic cost of PV is at Chinese yuan renminbi 0.7 kWh and is expected to decline by 10%-20% per annum. It is expected that PV and wind in most regions of China will achieve grid parity by 2020.

Gradual opening up of the power market: Power industry reform has allowed for the separation of distribution and retail. It has pushed innovative business development and encouraged cross-sector companies to introduce new technologies and ways of thinking to further accelerate energy internet development.

Continued regional economic and energy integration: Globalization and regional integration have become driving factors in the irreversible development of the energy internet. Harnessing energy and electricity for cross-regional connectivity is an achievable goal when you consider the interconnection between large power grids and international resource allocation in Europe. China’s Belt and Road initiative will help strengthen the energy link between China and neighboring countries, and promote regional integration development through energy infrastructure, commercial finance and investment cooperation.

Opportunities in developing the energy internet

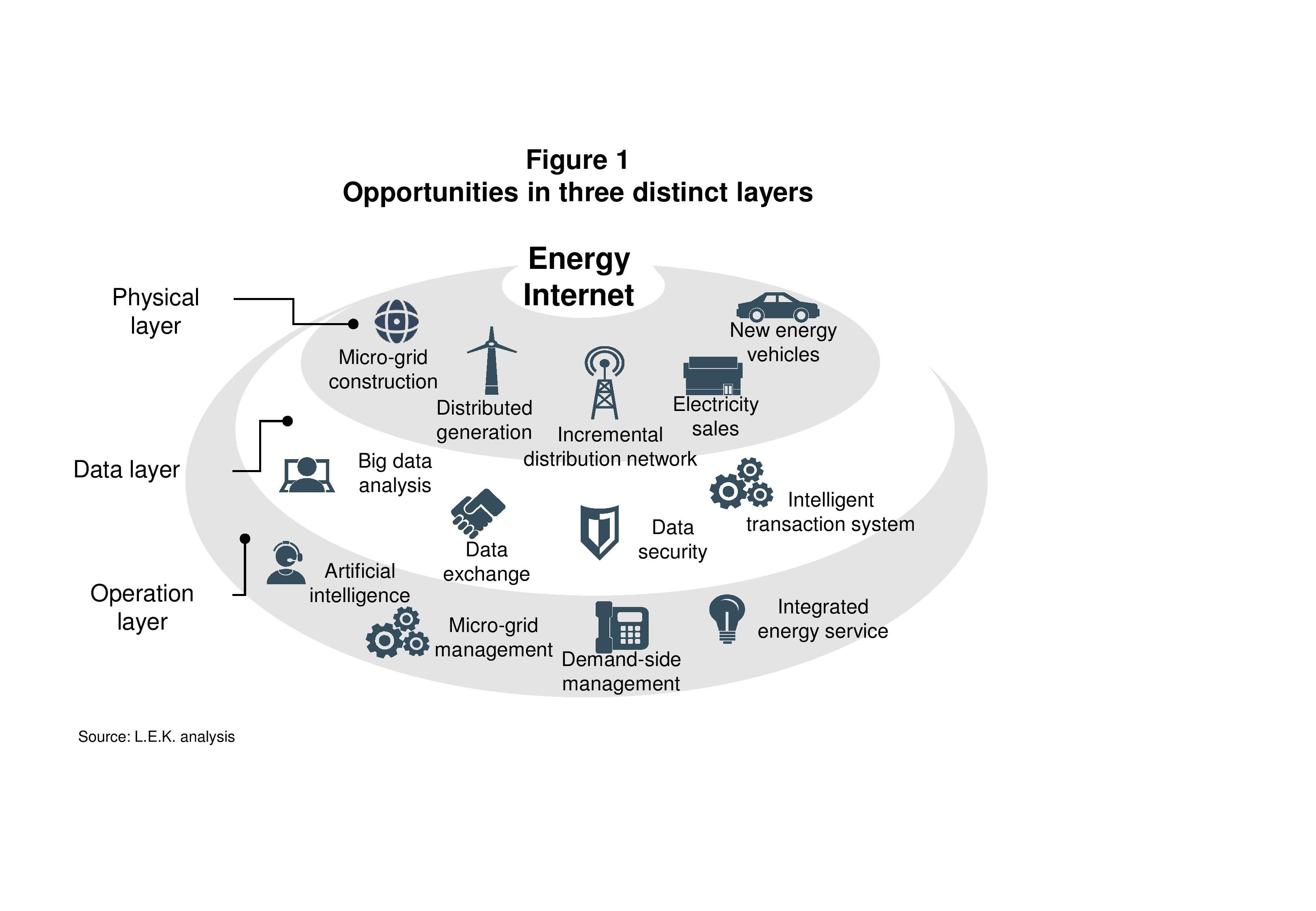

The energy internet will create opportunities in three distinct layers: the physical layer, data layer and operation layer (see Figure 1).

At the physical layer, integrated energy networks (including power, gas and heating) provide business opportunities in distributed energy development, micro-grid construction, new smart distribution grid, electricity retail, electrical vehicle charging infrastructure, etc.

At the data layer, accelerated technological development forms the foundation of the entire energy data value chain. Business opportunities lie in energy data collection, data exchange, data analysis, data security and intelligent transaction systems (carbon trading, power trading).

At the operation layer, market players need to be user-centric and be able to leverage a “connected network” to realize business value for end customers. This is a great opportunity to provide value-added services and solutions, including those in maintenance and operations, demand-side management, and integrated services.

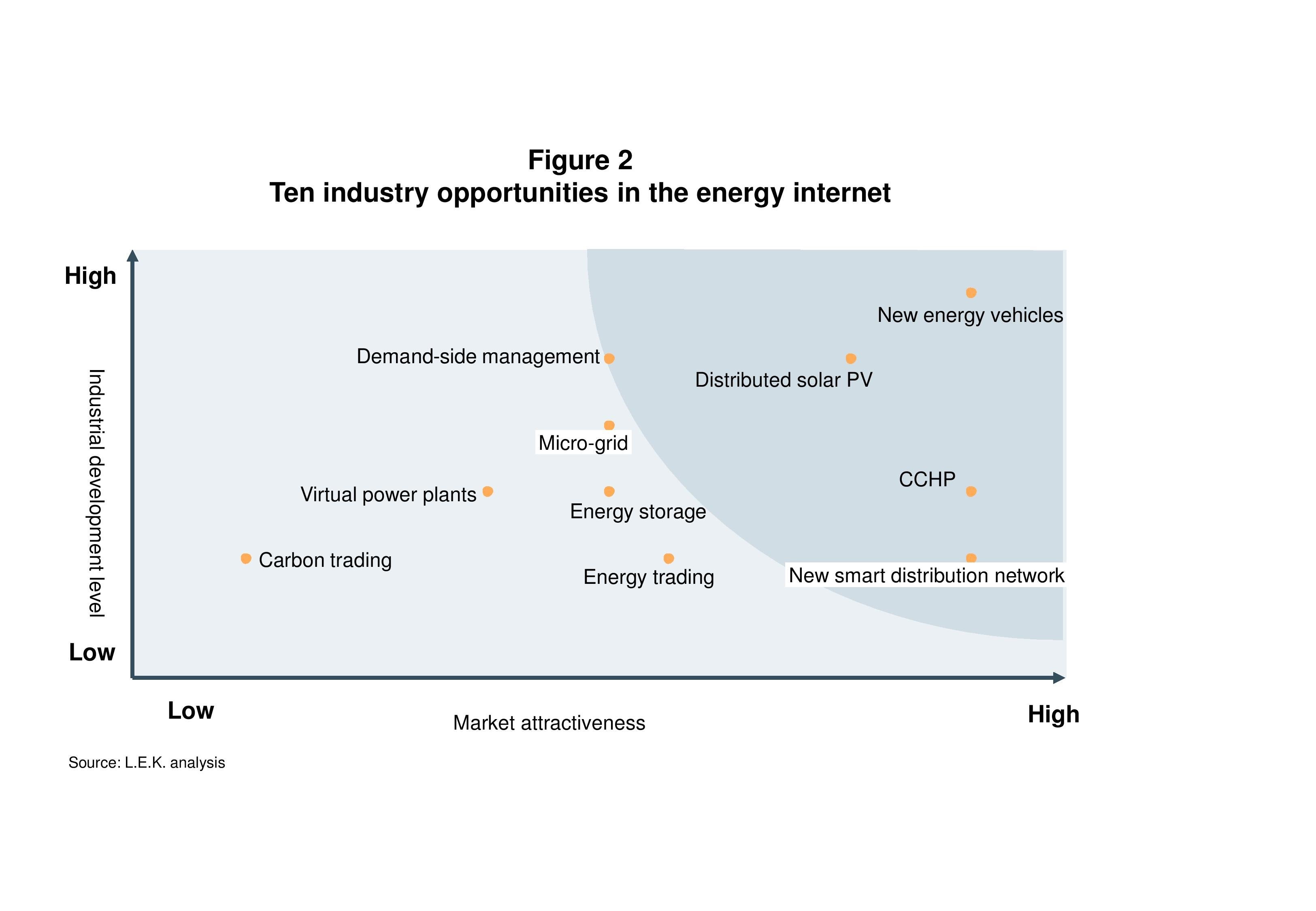

Based on the current stage of development and market attractiveness, we have identified 10 future market opportunities that could arise in the near future (see Figure 2).

Sectors such as combined cooling, heating and power (CCHP), distributed solar PV, a new smart distribution grid, electric vehicle charging infrastructure, and demand-side management are increasing.

- CCHP-installed capacity will continue to grow at an annual rate of 17.5%, reaching 250 GW in 2035. Therefore, power companies, oil and gas companies, and professional and technical services companies will all have various opportunities to position themselves.

- China’s PV market currently accounts for 20%-30% of the global increase in capacity. It is expected that by 2035, distributed PV installed capacity will reach 300 GW, of which large and medium-size projects (≥1 MW) will account for 60% of it.

- Power sector deregulation will allow new smart distribution grids to open to competition, especially those at new industrial parks, existing infrastructure expansions, and new commercial centers that were previously monopolized by grid companies. By around 2035, new smart distribution grids will produce approximately 555 GW in China.

- The electric vehicle sector has become one of the fastest-growing industries. We expect there will be more than 30 million electric vehicles in use, with annual sales topping 5 million by 2025.

- Demand-side management refers to energy management activities that aim to minimize costs through effective measures that guide end-users to optimize power usage, improve consumer efficiency and optimize resource allocation. For example, in East China, the commercial adjustable load accounts for 16% while the residential adjustable load accounts for 13%.

In addition to the previously listed opportunities, energy storage, micro grids, energy trading, virtual power plants and carbon trading are also trending in the right direction within the power industry and should warrant some level of exploration.

How to capture these opportunities

For traditional grid companies, the energy internet brings about real challenges, as new distribution grids continue to open up for competition. Therefore, it is necessary for traditional power grid companies to retool their business model and engage in active innovation. Traditional grid companies have to actively manage this transition and improve in the face of fierce market competition.

For power-generating companies and others, as they move away from a “back office” role to having increasingly direct contact with clients, there is a need to develop a more diversified business model to cater to different client needs. Their focus should be placed on clean energy, demand response and distributed energy segments.

For new energy companies, the energy internet could bring about increased economic benefits that reward first-movers. This provides a window of opportunity for new energy companies to leverage inherent operation flexibility developed through years of fierce market competition, and to actively launch groundbreaking projects and set industry standards. Such initiatives would ensure they are in a good position to compete with traditional energy giants.

For equipment companies, the energy internet has raised the bar on offerings to be more intelligent and interoperable just as stipulated in the Made in China 2025 initiative. The first priority should be to better integrate the energy sector with the internet by collaborating with other companies and codeveloping intelligent solutions.

For internet and IT companies, the focus should be on how to collect and extract value from big energy data. There is a need for internet and IT companies to explore data integration possibilities with other industries to realize the potential of this sector.

Conclusion

Facing such great challenges and opportunities, the energy industry must embrace the “change” mind-set. Companies that are able to adapt and take advantage of the new opportunities will be rewarded with exponential growth in this burgeoning new market.

06042021090627