The benefits of scale

Scale brings myriad benefits to commercial landscaping, namely the capacity to better weather labor and material shortages, the ability to leverage the potential of technology, the growth of “expertise”-driven services, and finally, consolidation up the value chain, which encourages partnerships with larger installation businesses.

In the face of material shortages, larger commercial landscaping players are able to obtain the supplies and equipment needed more quickly than smaller ones can. Supported by a strong value proposition, larger players may also be able to offer improved career paths to employees — and, potentially, higher wages.

They also have more resources to navigate the complex H-2B visa program and take better advantage of its benefits. The H-2B program can be an “all or nothing” proposition. For example, a landscaping company that requests an allocation of temporary workers will only receive that allocation if it accepts it within a specific local market. So whereas a single-branch operation has one shot to get its allocation of workers, a company with 10 branches will have multiple shots at getting at least some of its allocations for some of its branches.

Larger players are also better positioned when it comes to meeting the rise in demand for outdoor living solutions and related landscaping services, as customers are placing a greater value on speed and responsiveness. In a survey L.E.K. conducted in 2021, for example, we found that on-time delivery was the top selection criterion for installers when selecting distributors, ahead of pricing.

The management of larger commercial landscaping players is more professional than it is at smaller companies. These managers can drive efficiency by planning and scheduling crews and by redeploying resources across their geographic footprint as demand spikes in one area over others. The scale of larger players also increases efficiency, such as by creating more density within particular locations, optimizing truck routes and lowering transportation costs.

The growth of expertise-driven services also favors scale players. For example, irrigation requires technical capabilities that larger players are better able to deliver. Indeed, technology offers larger players multiple opportunities to differentiate themselves from the competition, close sales and retain customers. Examples of technology include the following:

-

BrightView Connect allows customers — who increasingly appreciate solutions that allow them to make requests, see live updates and aggregate data — to submit and track service requests, among other functions. For instance, a facilities manager could walk a property and submit service requests (e.g., for a damaged tree) in real time. Technology such as this is harder for smaller players to deploy.

-

Yellowstone Landscape is investing in robotic lawn mowers for hard-to-reach areas like really steep slopes. While such technology may only be applicable to specialized (e.g., institutional) needs, it provides a point of differentiation.

-

TruGreen uses Microsoft virtual bots to enhance customer service.

-

Bartlett has developed a solution for taking inventory of and managing services related to trees using GPS.

-

Davey leverages drones to inspect and map properties.

-

Juniper Landscaping also utilizes drones for the inspection and mapping of properties. It claims that doing so helps save labor costs and allows estimators to measure the property through annotations in an easier and more efficient way.

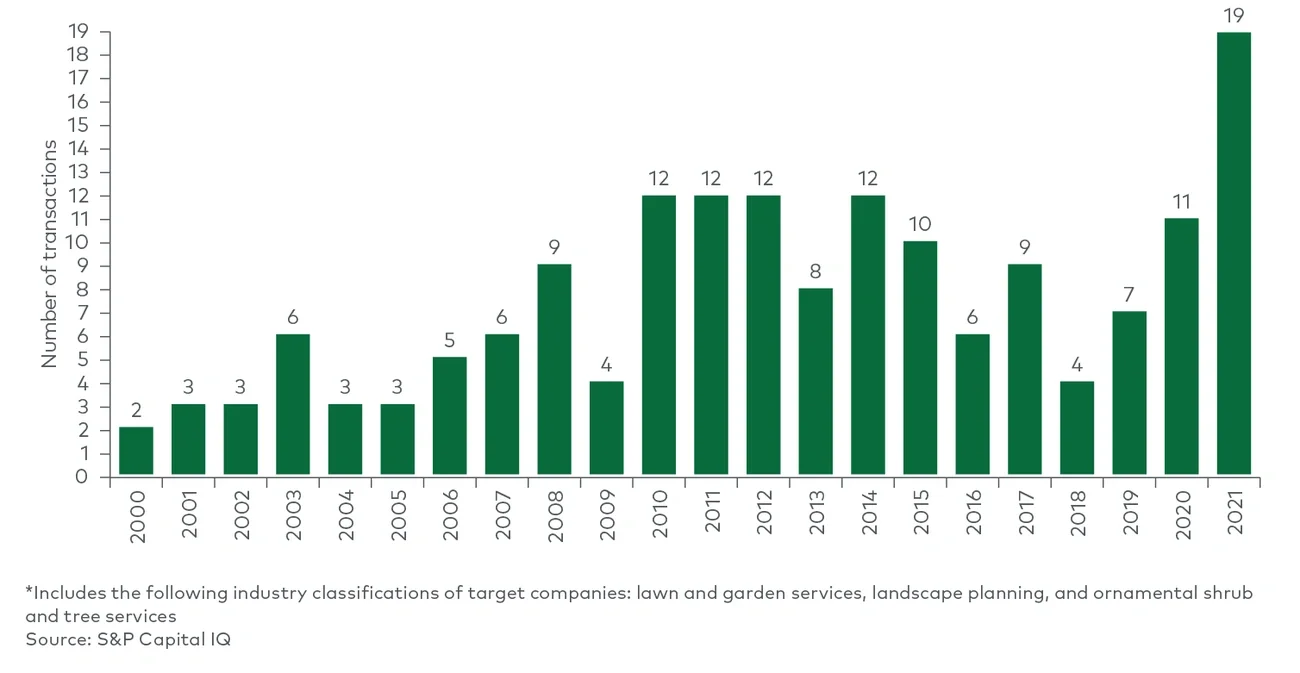

Meanwhile, consolidation is occurring up the value chain. The pace of consolidation has also increased across hardscape and softscape distribution, led by some key players (see Figure 8).