Key takeaways

-

L.E.K. Consulting’s proprietary Launch Monitor provides a comprehensive look at the sales performance of U.S. biopharmaceutical launches going back to 2004.

-

Leveraging these data and analytics, we support biopharma companies launching new products, enabling greater value for patients, providers, payers and shareholders by applying key learnings from previous market launches.

-

Early launch planning, effective stakeholder engagement, better forecasting and highly disciplined execution can help address barriers and better manage the Street’s expectations.

-

This Executive Insights reveals findings from the Launch Monitor and provides key perspectives based on our experience working across a wide variety of launches.

The cost of drug development continues to rise and the probability of creating new blockbuster therapies is not getting any easier. As a result, most biopharma companies focus primarily on how to efficiently develop product candidates with high commercial potential. However, a Food and Drug Administration approval is no guarantee of success; it is just the beginning. To drive real value, it is critical that biopharma companies execute the launch process flawlessly. As history shows, many companies fail in this process, due to a combination of factors such as limited market access, poor understanding of market needs or misjudgment of competitive threats.

L.E.K. Consulting’s proprietary Launch Monitor provides a comprehensive look at the sales performance of U.S. biopharmaceutical launches going back to 2004. This includes more than 450 launches of new molecular entities. This tool enables analysis of launch trends over time as well as in-depth analysis of how performance, both absolute and relative to Street consensus expectations, varies across different therapeutic areas, company types, product profiles, competitive dynamics and pricing bands.

Leveraging these data and analytics, L.E.K. supports biopharma companies launching new products, enabling greater value for patients, providers, payers and shareholders by applying key learnings from previous market launches.

Key findings from L.E.K.'s Launch Monitor

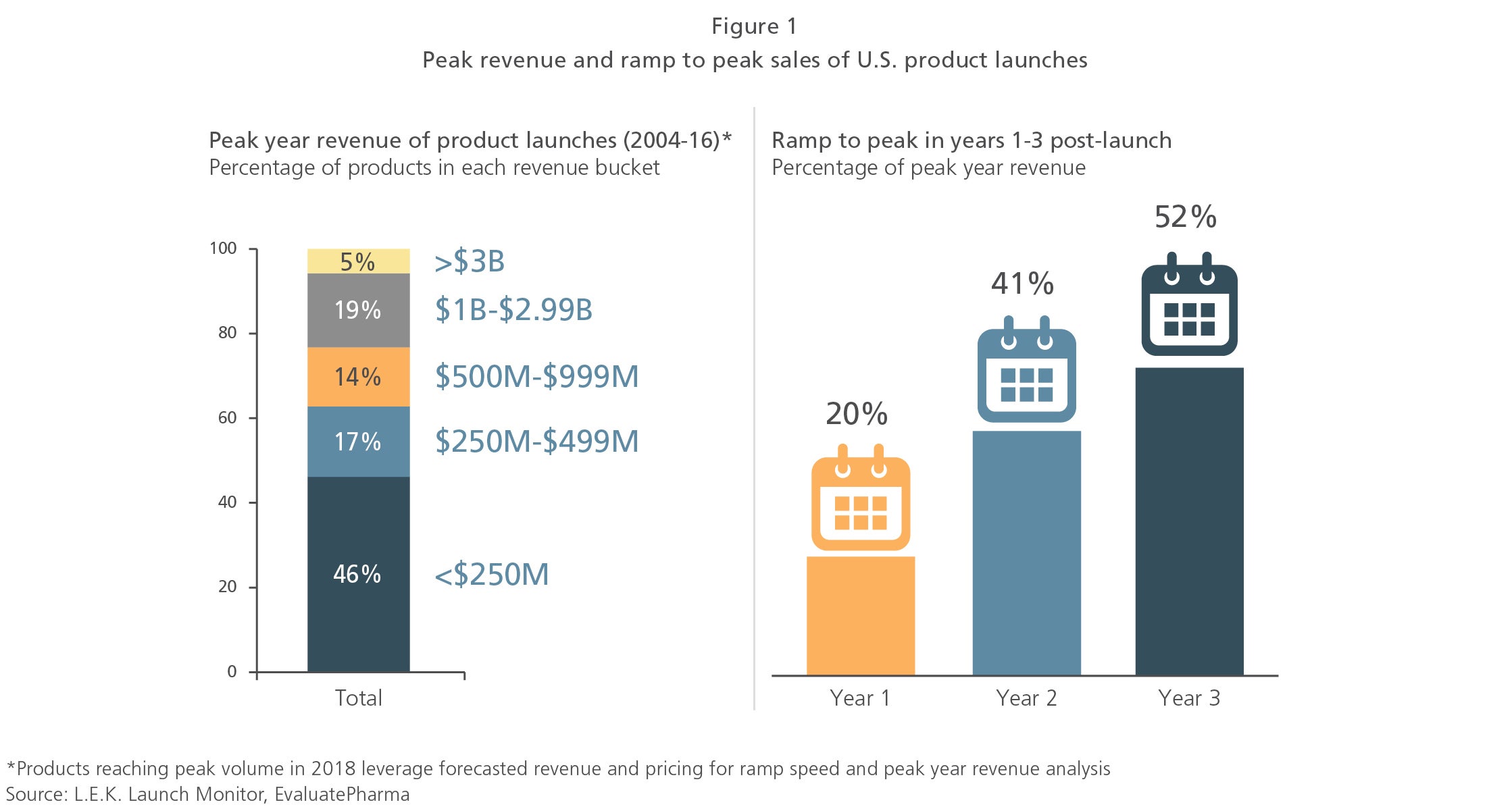

- The average peak U.S. revenue of products launched over the past 15 years is about $800M, with only one in five reaching U.S. sales of $1B, and over half failing to reach peak U.S. sales of $250M

- On average, products reach ~50% of peak sales by year three, and these early-year sales are strongly predictive of ultimate peak sales

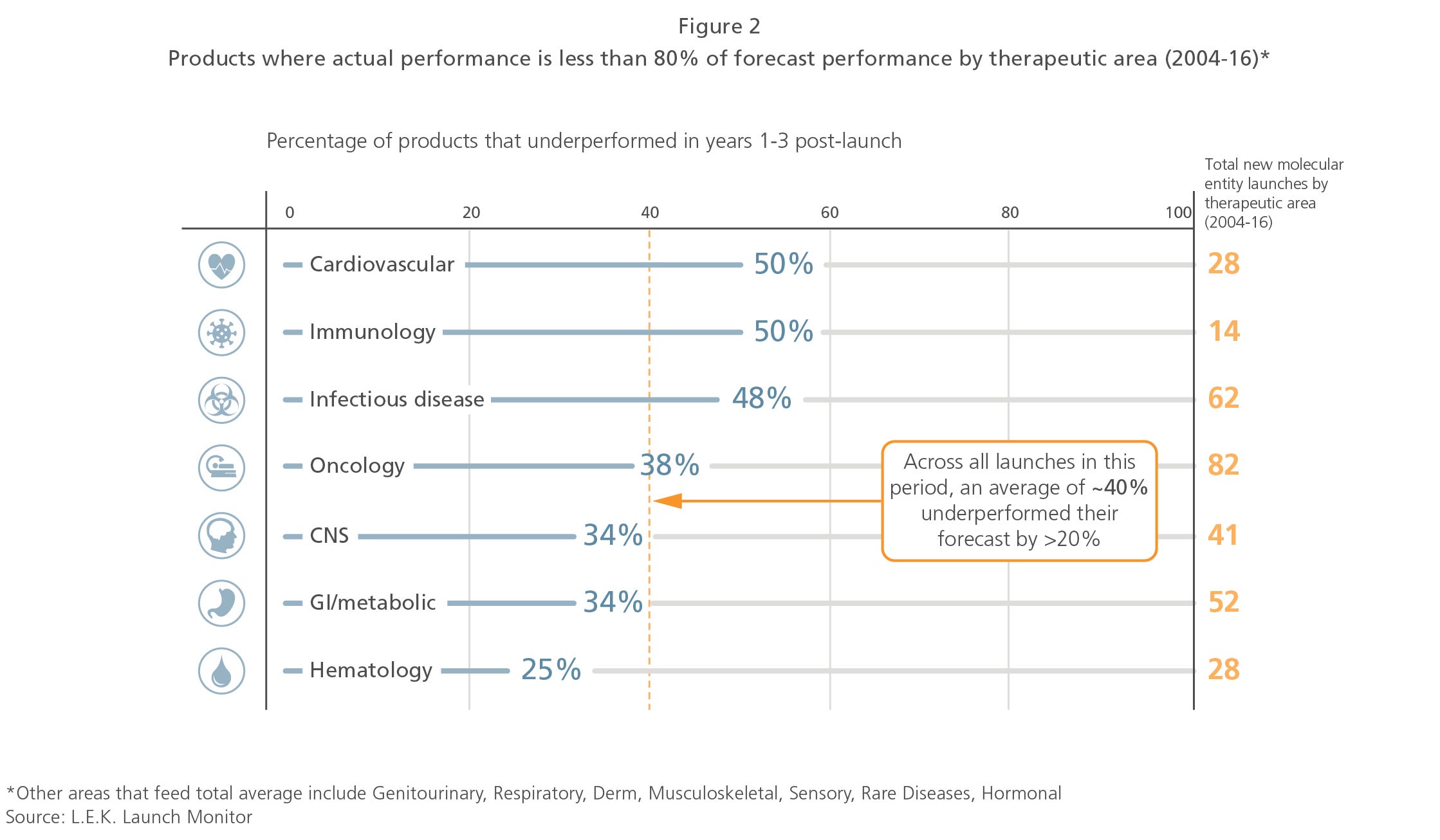

- About half of all products launched over the past 15 years have underperformed pre-launch consensus forecasts by more than 20%

- While performance issues cut across all therapeutic areas, infectious disease, immunology and cardiovascular diseases are the therapeutic areas where the most products underperform Street expectations

- On average, large pharma companies’ product launches have average peak revenues 50% higher than those of smaller players

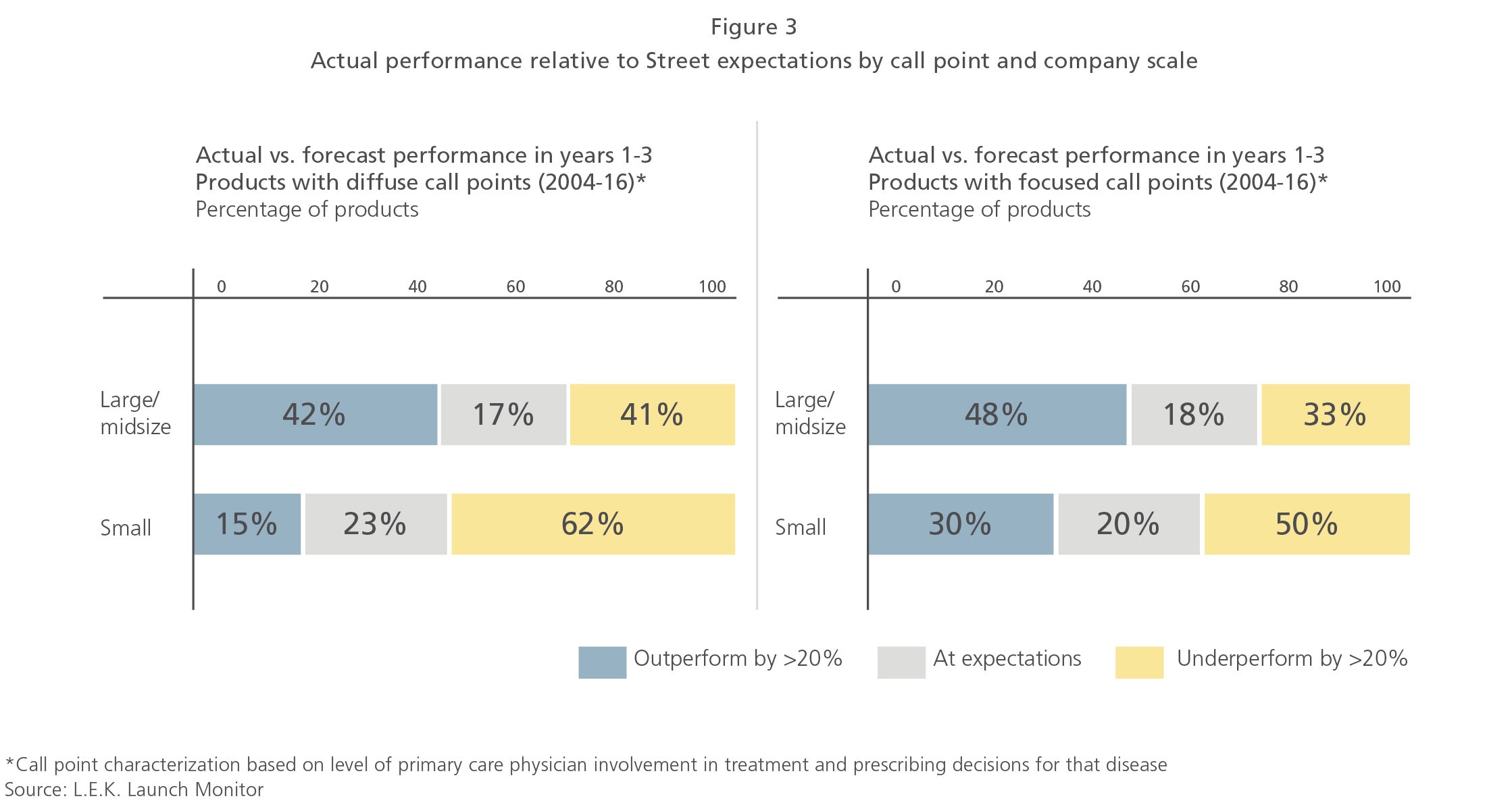

- Small companies were also more likely to underperform expectations than larger companies, and this difference in revenue performance is magnified in diseases driven by primary care channels

- Early launch planning, effective stakeholder engagement, better forecasting and highly disciplined execution can help address barriers and better manage the Street’s expectations

A strong launch is critical to achieving maximum commercial potential

Looking back over the past 15 years, it is apparent that blockbuster products are rare. While the average peak U.S. revenue of products launched over that time is just over $800M, only one in five of these products reached U.S. sales of $1B, and this does not factor in the long list of candidates that failed in the clinic. More surprising, approximately 50% of all products launched over the past 15 years failed to reach peak U.S. sales of $250M (see Figure 1).

Stumbling out of the gate on a product launch can be challenging to overcome, especially as competition continues to intensify across most disease areas. On average, products will reach 50% of their peak sales by year three, and these early-year sales are strongly predictive of ultimate peak sales (see Figure 1). Some areas like oncology ramp even faster, reaching 50% of peak sales by the end of year two, further underscoring the importance of early launch performance.

Only half of all product launches meet or exceed the Street’s expectations

Even after a product gets through the clinic, one thing that becomes clear is that achieving the Street’s expectations is a significant challenge. Most market observers agree that the accuracy of analyst forecasts is spotty, especially when products are still in development and clinical profiles are more uncertain. As a result, any gap between Street expectations and actual performance is likely driven in part by the lack of precision in these analyst forecasts. However, even when looking at consensus forecasts just prior to launch — forecasts that are heavily informed by expected product labels and management expectations — 40% of products underperform Street forecasts by more than 20% (see Figure 2).

This is especially true in the first few years after launch, when meeting unrealistic Street expectations can be challenging. Analysis of the past 15 years shows that more than 90% of products have U.S. revenue less than $250M in year one and more than 70% have revenue less than $250M in year two. Since the negative impact of missing a forecast can be severe, particularly for a small biotech launching a first product, companies must be cautious when providing revenue guidance and managing expectations from the Street.

While performance issues affect all therapeutic areas, they are worse in areas like infectious disease, immunology and cardiovascular disease, where about 50% of products underperform launch expectations by more than 20%. Whether it is underestimating the challenge of educating and changing the prescribing behavior of a large and disparate group of physicians, or misjudging some of the logistical and/or economic barriers that may be more prevalent in these areas, it appears that products targeting larger, more diffuse call points are more likely to underperform than those targeting focused, specialty call points.

Size matters for commercialization

Shifting the lens from disease area to company scale reveals some similarly interesting insights. L.E.K.’s experience has shown that small biopharmas are better equipped than their larger brethren to innovate and develop first- or best-in-class products, originating more than 50% of innovative products. However, where size, scale and institutional knowledge can be a barrier to innovative R&D, they become key enablers when it comes to the commercialization and life cycle management of a new pharmaceutical product.

Given big pharma’s propensity to disproportionately acquire assets with the greatest revenue potential, it might not be a surprise that average peak revenue for products launched by big pharma is 50% higher than the average peak for products launched by smaller players. What is more insightful is that even after normalizing for product expectations, small companies were more likely to underperform expectations than their larger counterparts. This delta in performance versus expectations is magnified in disease areas with larger, less well-defined call points (see Figure 3).

This analysis is aligned with prior L.E.K. research showing that only a small percentage of emerging biopharma companies launching their first product exceeded analyst sales expectations, highlighting how challenging commercial execution can be for smaller companies embarking on their first launch.

Early launch planning can help overcome adoption barriers and manage analysts’ expectations

So what does all this mean for biopharma companies preparing for an upcoming commercial launch? From our experience working across a wide variety of launches, L.E.K. has distilled a few key launch perspectives:

- Plan the launch early and monitor: Even for companies with great products, a lack of launch preparation can lead to performance challenges. We recommend that biopharma companies start thinking about launch planning up to 36 months prior to first market authorization. It is also critical to ensure that a cross-functional team is in place to support and track the myriad things that are important for a successful launch. Additional L.E.K. perspectives on essential factors for a successful launch can be found here.

-

Be realistic about the launch challenges: As a part of the process, biopharma executives need to think critically about the barriers to uptake, especially within some of the larger primary care or hospital-focused indications. Pricing and reimbursement pressures, access to key stakeholders, and competitive pressures vary widely across indications and therapeutic areas and can significantly impact the scope and pace of adoption.

-

Carefully consider partnership: Smaller companies have been less successful than large companies when launching pharmaceutical products, given their limited resources and capabilities. It is important for biopharma executives to think strategically about commercialization choices and carefully evaluate partnership opportunities. Additional L.E.K. perspectives on partnership decisions can be found here.

-

Manage investor expectations: Biopharma companies should thoroughly examine forecast assumptions and solicit external expert opinions where relevant to manage investor expectations toward realistic and achievable goals. Small overstatement of the addressable patient population, misjudgment of market access levels or mischaracterization of emerging competitive dynamics can throw off a forecast considerably and misalign market expectations as well as launch planning efforts.

For more insights on biopharma launch performance or to hear more about how you can optimize your upcoming launch, please reach out to us and we would be pleased to arrange a meeting.

02022021170205