We have witnessed the most profound example in history of airline capacity responding to demand as a result of the COVID-19 crisis. Governments around the world have closed their international borders and discouraged all but essential domestic travel. Airlines in Australia have responded by grounding international fleets and withdrawing almost all domestic capacity.

The key question confronting the aviation industry is therefore not how far will demand fall, but rather, when will the recovery commence and how quickly will demand grow?

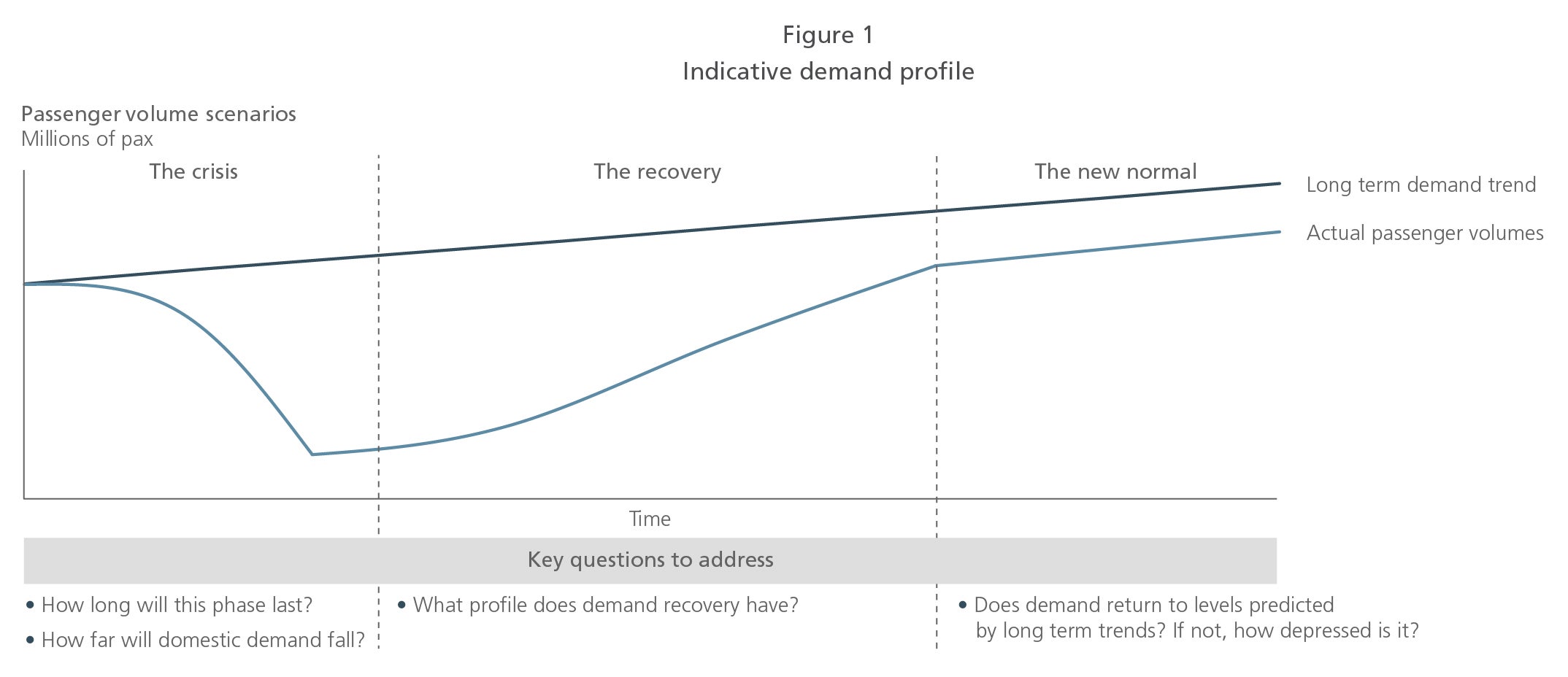

The figure below characterises the three stages of the recovery:

- Stage 1 — The crisis

- Stage 2 — The recovery

- Stage 3 — The new normal

The crisis

The timing of the recovery’s commencement is impossible to predict at this point. The Australian government has progressively taken steps to limit travel with a view to ‘flattening the curve’. The demand for air travel will return only when the following two conditions are met. First, the government declares that it is now safe to resume domestic and international travel and second, the travelling public regain the confidence to do so.

The recovery

The initial driver of the recovery will be business travel. Some of this demand will precede an observable recovery in conventional measures of economic activity (e.g. GDP growth), so it will be necessary to take a view on those sectors of the economy that will lead the recovery of business-related travel and their relative size.

There is an emerging hypothesis that remote working (i.e. “working from home”) and video-conferencing will drive a significant and permanent shift in ways of working which will flow through to business-related travel. The same suggestion was made during the 1989 Australian domestic pilots’ dispute, which saw monthly domestic traffic fall by as much as 75% year-on-year and only limited business travel undertaken. In this case business-related travel quickly recovered at the end of the dispute. The clear difference here is that the business world has evolved significantly since the late-1980s from a technology perspective. The longer the COVID-19 crisis restricts domestic and international business-related travel, the greater the scale of the likely behavioural shift away from face-to-face meetings requiring intestate and international travel as new ways of working are locked in.

In our view, there are a number of demand- and supply-related reasons why non-business travel will significantly lag the recovery of business-related travel.

From a demand perspective, there is the obvious impact of the crisis on household incomes and wealth and the flow-through impact on discretionary expenditure in 2021, including for visiting friends and relatives (VFR) and holiday trip purposes. The level of household debt as a proportion of net disposable incomes in Australia is extremely high — much higher than is seen in the United States and the United Kingdom for example — and many households will either seek to, or be mandated to by financial institutions, reduce debt levels after the crisis.

However, a further constraint on both domestic and outbound international travel will be that leave balances for those who retain employment will be depleted and this will be a significant constraint on discretionary travel during 2021. This will be particularly so for holiday travel, with many likely to prioritise domestic and international VFR travel as a means of re-engaging with their personal networks.

The demand for inbound travel will need to be carefully assessed on a market-by-market basis. A low Australian dollar will improve Australia’s attractiveness as a holiday destination compared to other countries, but the same considerations set out above for Australians will apply to potential international visitors (i.e. the impact on household income and wealth and diminished leave balances for those who retain employment). This latter point is particularly pertinent for long-haul international travel given the minimum viable time required to visit Australia.

The supply side also has a number of dimensions.

First is the approach of the airlines to the recovery phase. What will initial networks look like and how fast will capacity and route coverage increase?

The expectation that business-related travel will lead the recovery suggests an early ramp-up of domestic services on the Golden Triangle (i.e. Melbourne-Sydney-Brisbane) and capital city links more generally. Airports with the largest exposure to non-business domestic traffic can expect to wait longer for the re-establishment of services and probably at diminished levels of capacity for some time. This could mean that airlines look to rebuild yields relatively quickly, but this will inevitably depend not only on the market segments driving the recovery of air travel but also on airline industry structural considerations (i.e. how our two primary carriers emerge from the crisis).

The re-establishment of international services is more difficult to predict — it will inevitably be a reflection of the financial health of the world’s airlines and their own plans for re-booting operations. However, in some cases, other factors will play out. For example, prior to the COVID-19 crisis, China capacity was already being reduced as incentives available to Chinese carriers expired.

A further overlay here will be the potential (early) retirement of ageing fleet which will remove potential capacity from airline schedules.

It is also possible that some governments around the world may actively discourage international travel for a period of time to support the recovery of domestic tourism and the economy more generally.

The availability of tourism infrastructure and services will also impact on the attractiveness of domestic and inbound international travel. The Australian tourism industry was already confronting the impact of the catastrophic bushfires across late 2019 and early 2020. While many of Australia’s leading tourism regions (e.g. Queensland, west coast of Western Australia and the Northern Territory) were unaffected by the fires, all regions now face the prospect of little to no trading activity over the coming months, and it is likely that smaller operators will struggle to survive. The impact will manifest itself across the entire tourism supply chain — accommodation, food and beverage, and attractions.

The new normal

The new normal represents the period when the traditional drivers of the demand for aviation services can once again be relied upon to forecast activity levels in the medium to long term.

In the case of domestic and outbound travel by Australians, that means primarily Australian economic performance and the level of real air fares. Additionally, real exchange rates will impact the balance of domestic and outbound travel by Australians.

For inbound international travel by foreign visitors, it will again be possible to reliably forecast traffic volumes with reference to economic performance in the source countries, air fares and exchange rate movements.

However, these drivers will be acting on a relatively low base, and the relationships between these fundamental drivers and demand may well be different from that applied historically.

During previous shocks to the industry, such as SARS, 9/11 and the global financial crisis, there was a degree of confidence that demand would revert to the long-term trend and hence there would be no sustained impact on observed demand.

This crisis could break that trend. The scale of the crisis is unprecedented and the impact on both demand and supply fundamentals for the industry will be profound and long lasting.

Conclusion

The COVID-19 crisis requires a new approach to airport demand forecasting across the short, medium and long term. It needs to be bespoke to reflect the national, regional and local context and the expected timing and scale of recovery of the airlines serving the Australian domestic and international markets.

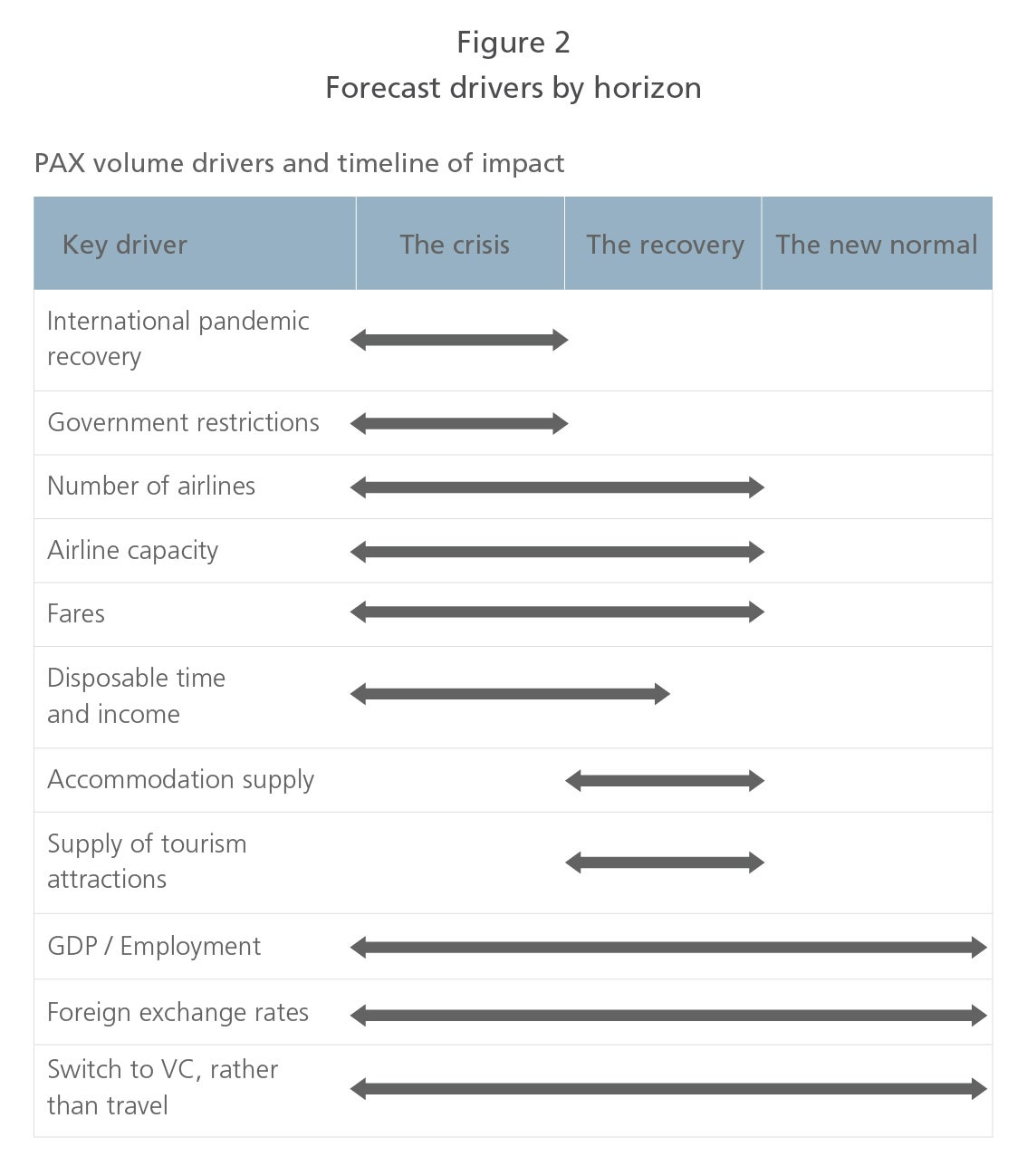

Figure 2 summarises the 11 factors that L.E.K. Consulting has identified that will drive the demand for air passenger services across the three forecasting horizons — the crisis, the recovery and the new normal.

01262022140145