Key takeaways

- Fitness-minded consumers are turning to at-home fitness to maintain a healthy and active lifestyle during the COVID-19 pandemic.

- Consumer investment in digital fitness has increased by 30%-35% relative to pre-COVID-19 levels, positioning the sector for faster growth in the future.

- The complementarity between digital fitness and traditional fitness centers is expected to grow post-COVID-19, with ~30% of consumers expected to continue spending above their pre-outbreak levels.

- In this Executive Insights, we discuss the key considerations for digital fitness companies and their investors as they make strategic decisions.

The COVID-19 pandemic will have many unanticipated impacts. While the near term promises to be extremely challenging for all of us — both individuals and businesses — as we adapt and try to protect ourselves, the digital fitness market is expected to experience long-term consumer engagement. The initial returns from L.E.K. Consulting’s ongoing COVID-19 Consumer Insights for Business series suggest that digital fitness — connected exercise equipment and streaming fitness content — is one of these opportunities.

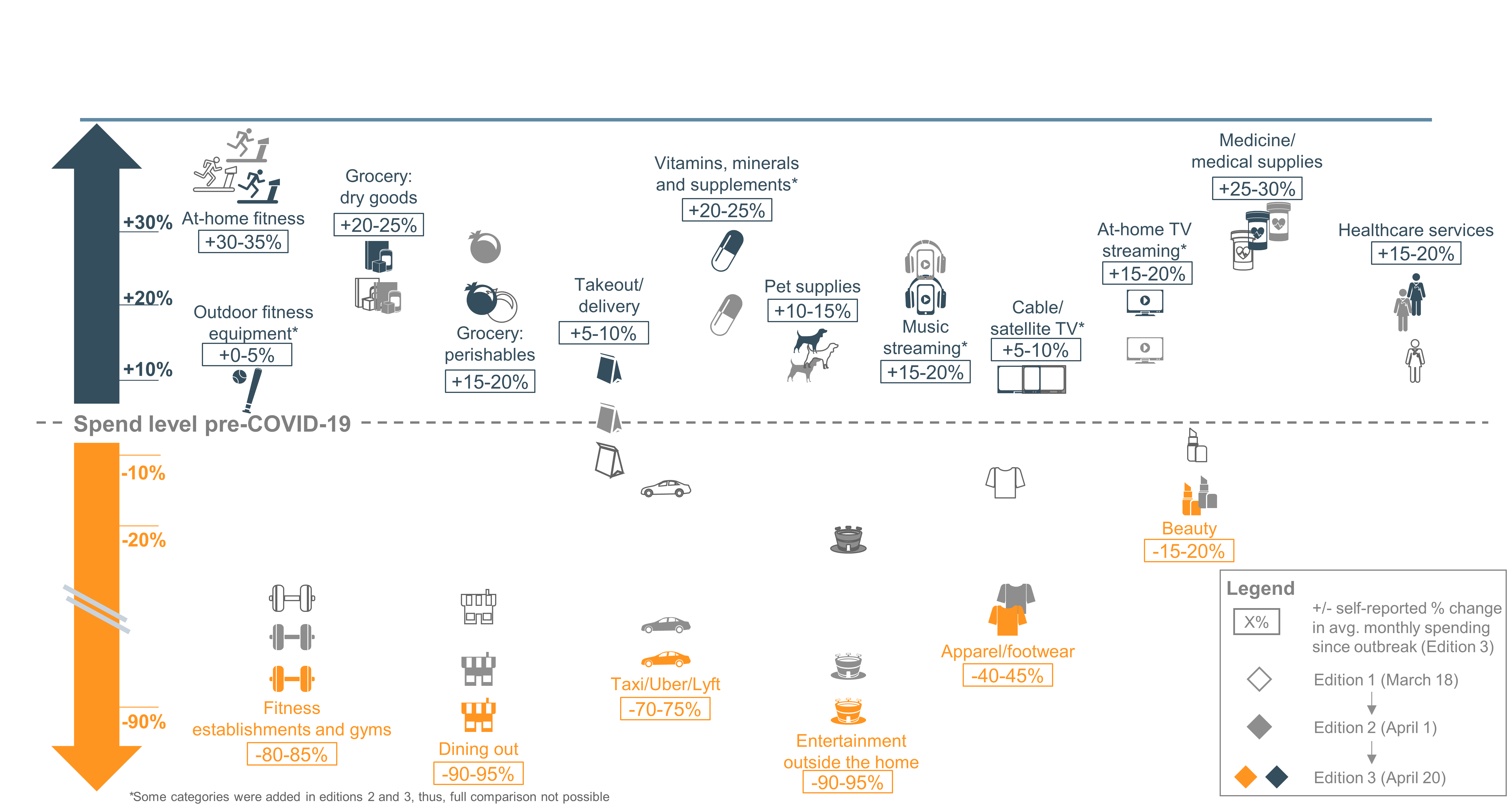

As gyms, fitness centers and boutique studios have closed and “shelter in place” has become the new normal, fitness-minded consumers are turning to at-home fitness to maintain a healthy and active lifestyle, increasing their spending on digital fitness by 30%-35% relative to pre-COVID-19 levels (see Figure 1). Digital fitness was already poised for strong growth for the foreseeable future, but the COVID-19 crisis will likely accelerate the use of digital fitness and create long-term changes in how consumers manage their health.

Figure 1

U.S. consumers: Reported change in average monthly spend since COVID-19 outbreak began

(Existing and new category buyers; N=2,403)

A quick primer on digital fitness

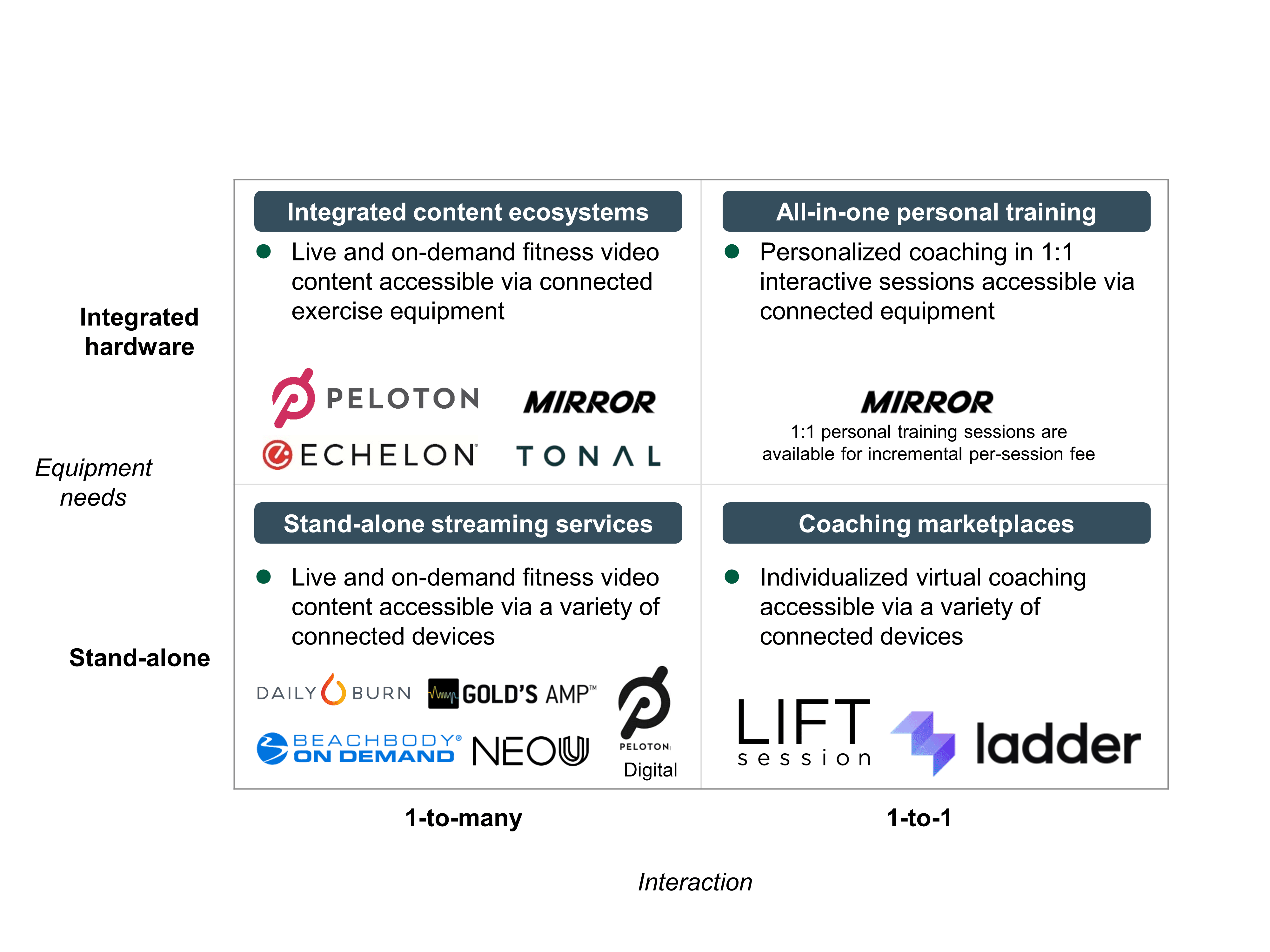

Before getting into the recent impact of COVID-19, let’s take a step back and examine the evolution of the digital fitness landscape. Broadly speaking, digital fitness services can be characterized across two dimensions — equipment needs (integrated hardware and content vs. stand-alone content) and type of interaction (one-to-many, such as group exercise classes, vs. one-to-one, such as personal training sessions) (see Figure 2).

Although digital fitness services existed prior to Peloton’s 2014 launch, Peloton was the first to effectively commercialize the opportunity at scale by launching an integrated hardware and content product. By owning the entire end-to-end customer experience and investing heavily in high-quality content production, Peloton was able to deliver a cycling workout comparable (or perhaps even superior) to leading commercial gyms and boutique cycling studios. Peloton’s success inspired investment in other integrated hardware and content products across multiple exercise modalities, including group exercise classes (e.g., Mirror), rowing (e.g., Hydrow) and strength training (e.g., Tonal).

Additionally, there has been a proliferation of hardware-agnostic, stand-alone digital fitness services that need only a smart TV, a tablet or another connected device to access content and deliver an effective workout. While these services do not offer the same end-to-end experience as an integrated product, the entry point — typically ~$10-$20/month — is much more accessible for the broader population.

Large opportunity with strong macro tailwinds boosted by COVID-19

Though only a ~$1 billion market in the U.S. today, digital fitness has a substantial growth runway remaining, as the total U.S. opportunity is estimated to be ~$10 billion to $15 billion, indicating only ~7%-10% penetration so far. Even prior to the COVID-19 crisis, digital fitness was well positioned to deliver material growth due to growing interest among nonsubscribers and broader alignment with consumer megatrends, including the growth in holistic wellness, the rise of the quantified self and the ongoing shift toward an increasingly mobile lifestyle.

As a result of COVID-19, consumer demand for digital fitness has surged. With traditional gyms and boutique studios closed for the time being, digital fitness has emerged as the next best alternative to maintaining a healthy, active lifestyle, creating a step change in consumer awareness, interest and usage of digital fitness services.

Additionally, the incremental digital fitness growth due to COVID-19 is not temporary; once COVID-19 is contained and traditional gyms and boutique studios are reopened, ~30% of consumers expect to continue spending on digital fitness above their pre-outbreak levels. This is likely due to the high level of complementarity between digital fitness and traditional fitness centers, as nearly ~60% of digital fitness subscribers who are commercial gym members reported an increase in the time spent at the gym as a result of digital fitness.

Digital fitness investment options and considerations

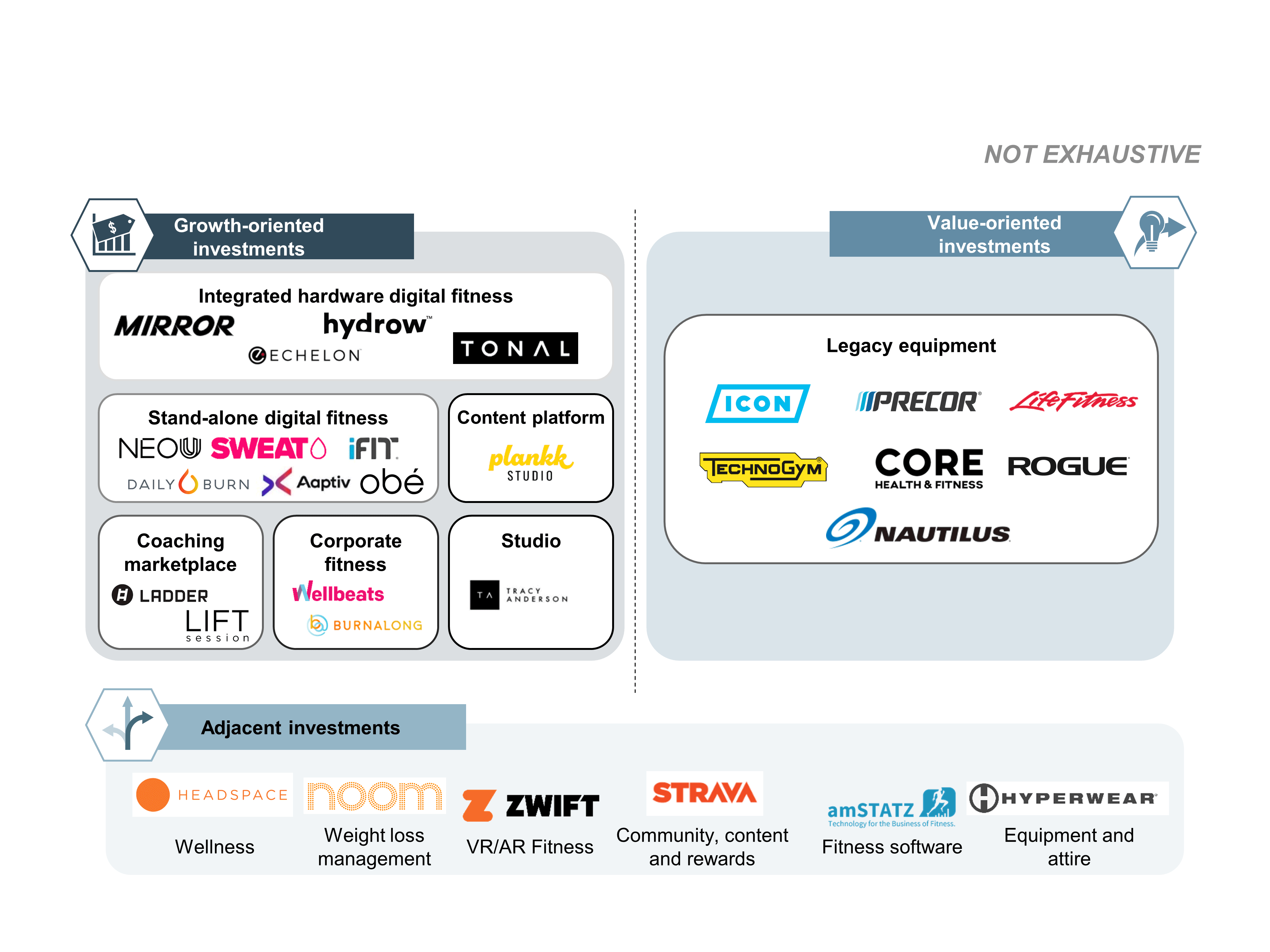

Even in today’s uncertain economic environment, innovative digital fitness companies are highly valued due to their strong growth potential. While investing in early-stage digital fitness companies and providing growth capital in hopes of a large future payoff (in the manner of Peloton), it is not the only route investors can pursue to gain exposure to digital fitness. Other approaches include:

- Growth-oriented digital fitness investments: Startups and emerging businesses represent attractive, potentially high ROI opportunities if provided the appropriate financial and strategic support to enable successful, rapid expansion.

- Value-oriented digital fitness investments: Alternatively, investors can revisit “legacy” fitness equipment businesses that are losing share to Peloton and other digital-native services. Capitalizing on depressed valuations and navigating an effective strategy pivot toward digital fitness could generate compelling investment returns.

- Digital fitness adjacent investments: Investment in an adjacent services business (e.g., weight management, wellness services) may represent a viable entry point to build out a robust, integrated digital platform across multiple health- and wellness-related businesses.

Within each of these investment approaches, there are multiple potential acquisition targets to consider (see Figure 3).

While the strong growth profile of digital fitness can potentially reward investors in the future, the market remains highly fragmented, with limited brand recognition outside of Peloton. Regardless of the investment pathway, digital fitness companies and their investors need to make the right strategic decisions to realize the coming returns, including:

- How can we differentiate our service offering from the rest of the competitive set?

- What is our content strategy, including the role of live content?

- What is our trainer/talent development strategy?

- How can international expansion amortize content and technology investments to drive accretive growth?

- What strategic partnerships can enhance brand awareness, customer acquisition and customer retention to accelerate value creation?

- How do gym operators participate in digital fitness in a post-COVID-19 world where digital fitness is more prevalent? What are the build vs. buy vs. partner trade-offs and implications for future growth?

06142021130600