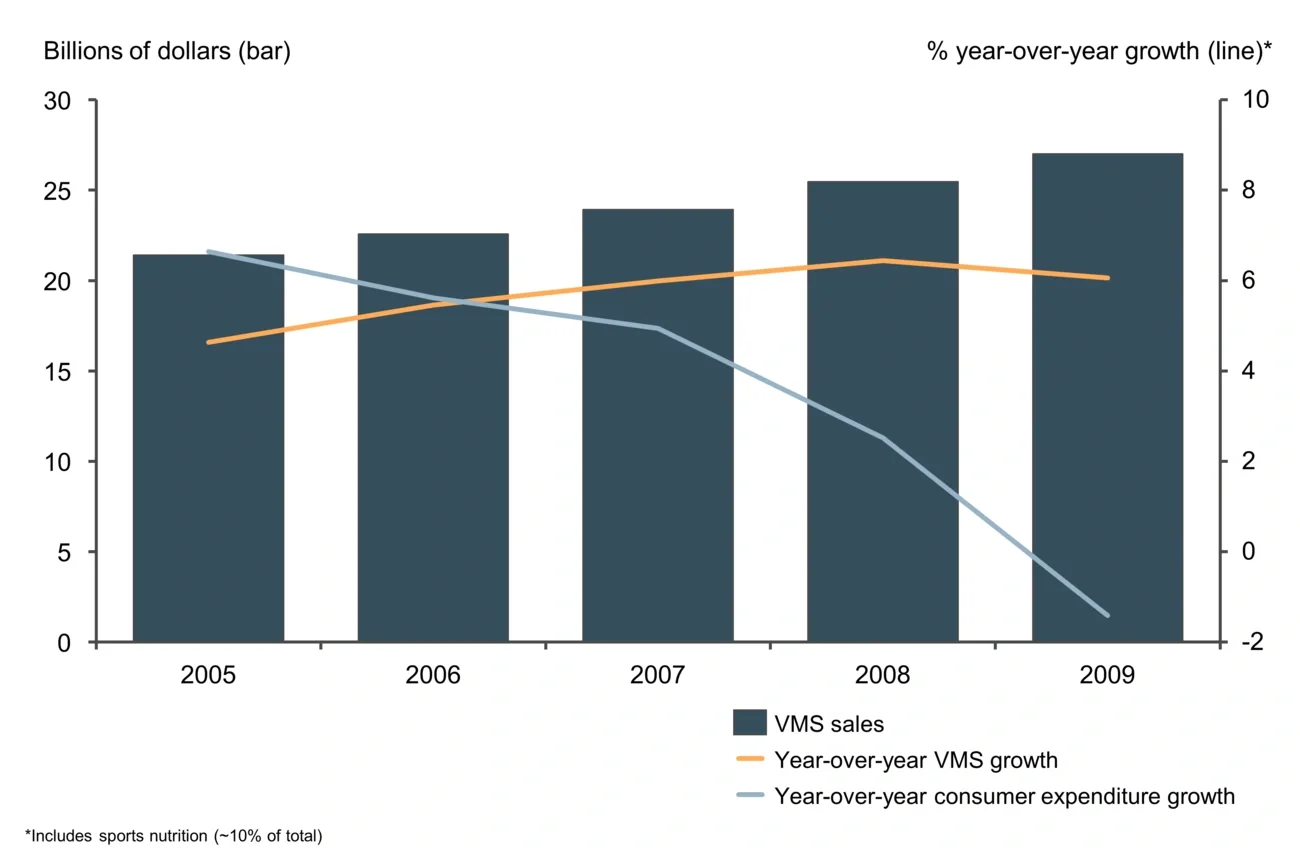

The consistent growth in 2008-09 reflects two key underlying elements of consumer behavior with VMS that suggest VMS demand in 2020 will form a new, higher base of sales from which the category can grow.

First, health and wellness spend, like VMS spend in particular, has historically been prioritized by consumers in times of recession and is one of the last discretionary spend categories to be impacted. For many, VMS consumption may actually increase, as it represents a cost-effective, preventive measure to mitigate the need for more costly physician or hospital visits, particularly when disposable income declines and/or health insurance coverage is reduced.

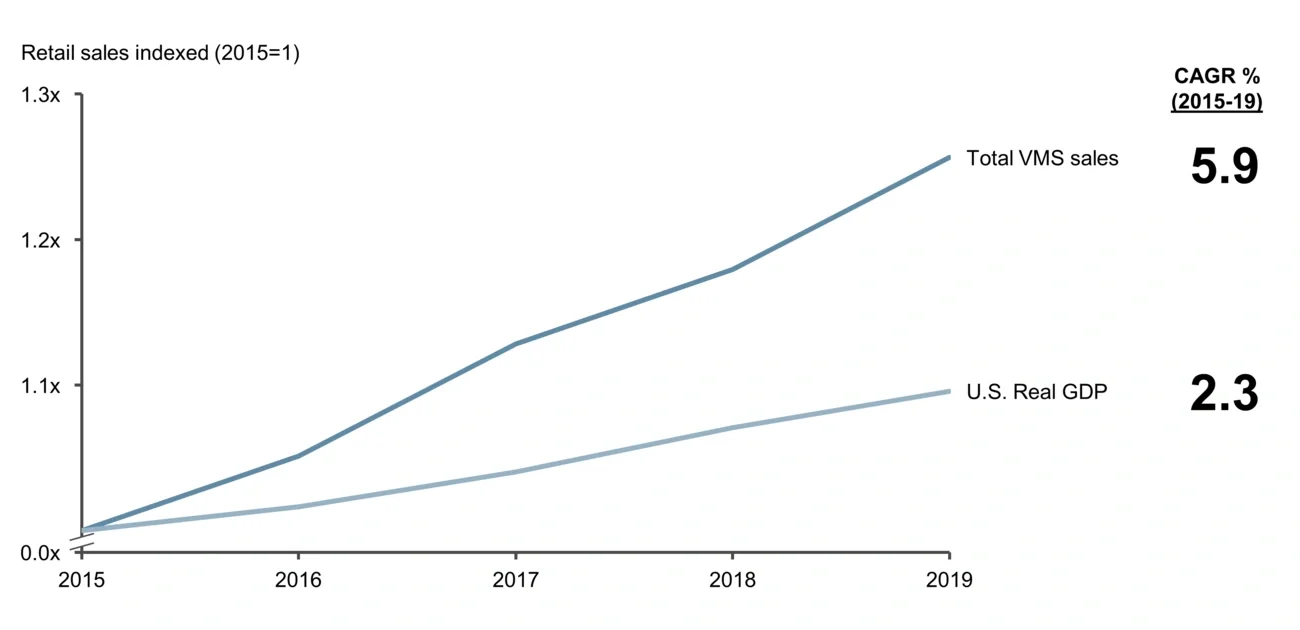

Second, the VMS category sustained its growth during and after the recession, averaging 5% per year growth through 2019. Notably, product trials during the recession brought new consumers into the market who were converted into consistent purchasers, establishing a higher base of consumers for category growth. This behavior is particularly pertinent given the significant increase in consumer interest in health and wellness that is occurring today.

Implications for VMS players today

Within the VMS market, a multitude of players should be considering how to prepare for the long-term increase in sales that is expected in the category. These include ingredient suppliers, contract manufacturers, consumer brands and retailers. For each of these participants across the value chain, beginning to prepare now can optimize value creation over time.

Based on our experience with consumer behaviors in the category, there are five key commercial implications that we think are critical for industry participants to consider now:

- Secure your supply chain and operations

- Refine and optimize your portfolio of offerings to tailor to consumer needs

- Establish a robust omnichannel capability now and in the future

- Develop a strategy for the expected increase in private-label demand

- Consider synergistic, personalized nutrition partnership opportunities

Secure your supply chain and operations

Despite elevated levels of demand for VMS products, retailers can provide only as much product as they can source. Both online and brick-and-mortar retailers are reporting shortages as new consumers enter the market and existing users stock up. Manufacturers are also experiencing raised prices and potential shortages of raw ingredients to keep up with consumer demand.

In the immediate term, securing your supply chain to fill as much of the near-term demand as possible is essential, in particular so that you do not lose potential new consumers who may be trialing the category. In the long run, the COVID-19 pandemic should also bring sourcing practices under the magnifying glass to guard against future developments. Reducing reliance on single sources (by supplier or geography, especially China) is a key next step to reducing operational risk and potential consumer concerns about product quality.

Refine and optimize your portfolio of offerings to tailor to consumer needs

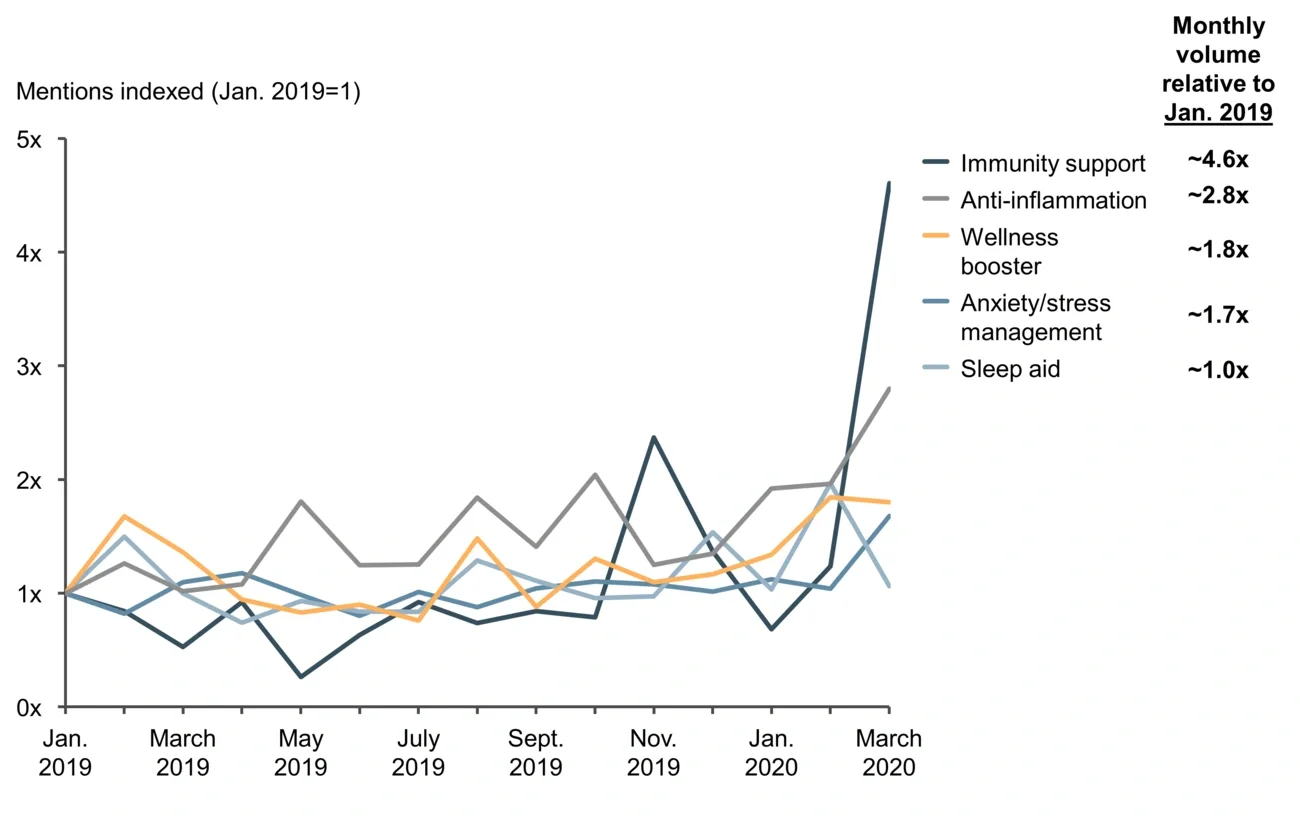

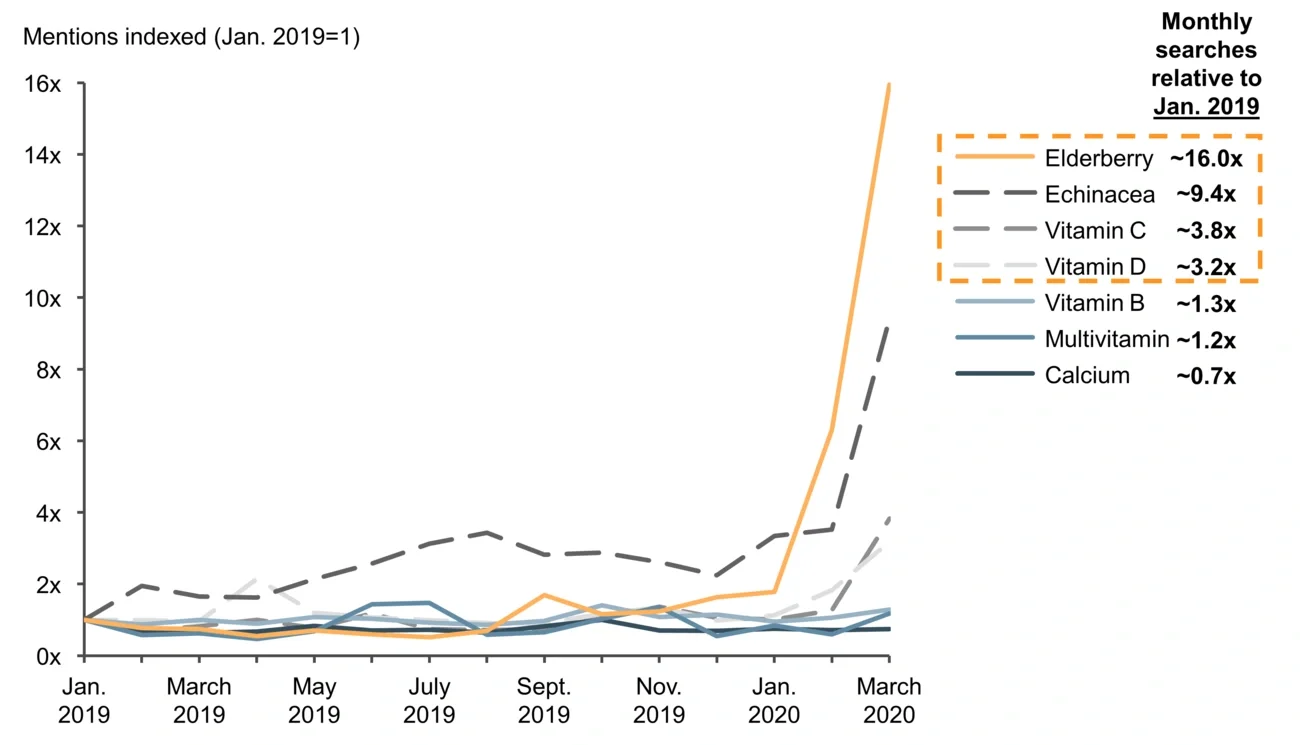

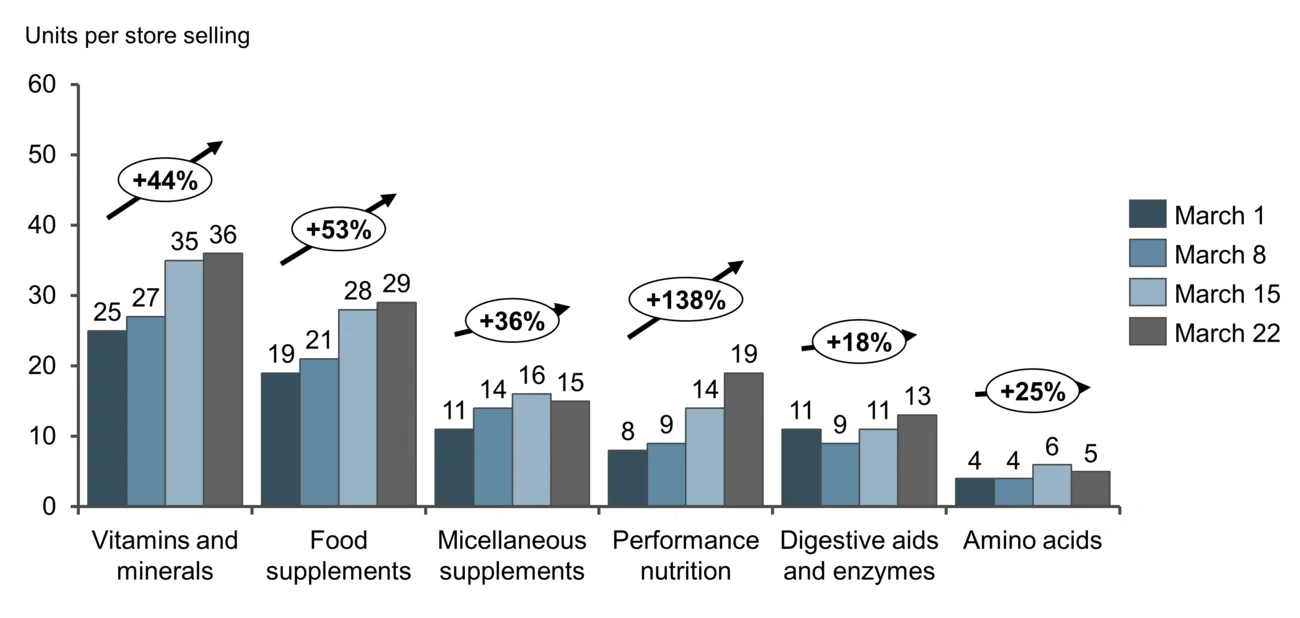

Although sales for almost all VMS sub-segments have risen, you can expect demand growth going forward to be asymmetric. While NBJ is projecting year-on-year sales growth of all supplements to reach approximately 5%-8% or more in 2020, sales of supplements addressing cold, flu and immunity are projected to exceed 25% year-on-year growth in 2020.2 In a related matter, demand for certain products that are typically more modest is likely to spike significantly; on social media, for example, the volume of consumer chatter about elderberry has risen by 16x, surpassing the volume of discussion about vitamin C and vitamin D combined (see Figure 3).

For retailers and manufacturers, right-sizing assortments and production resources to meet the changing balance of consumer needs in real time will be a challenge, but this is essential to maximize capture of consumer value and optimize in-stock levels in the future.

Establish a robust omnichannel capability now and in the future

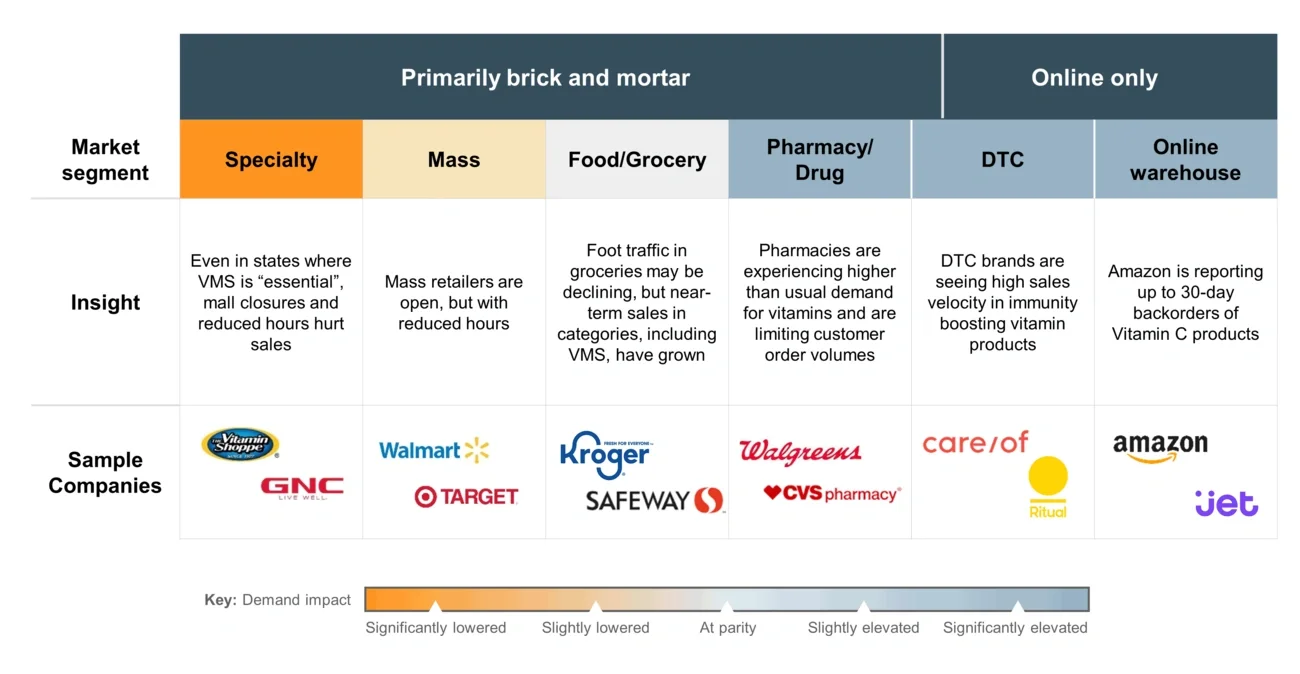

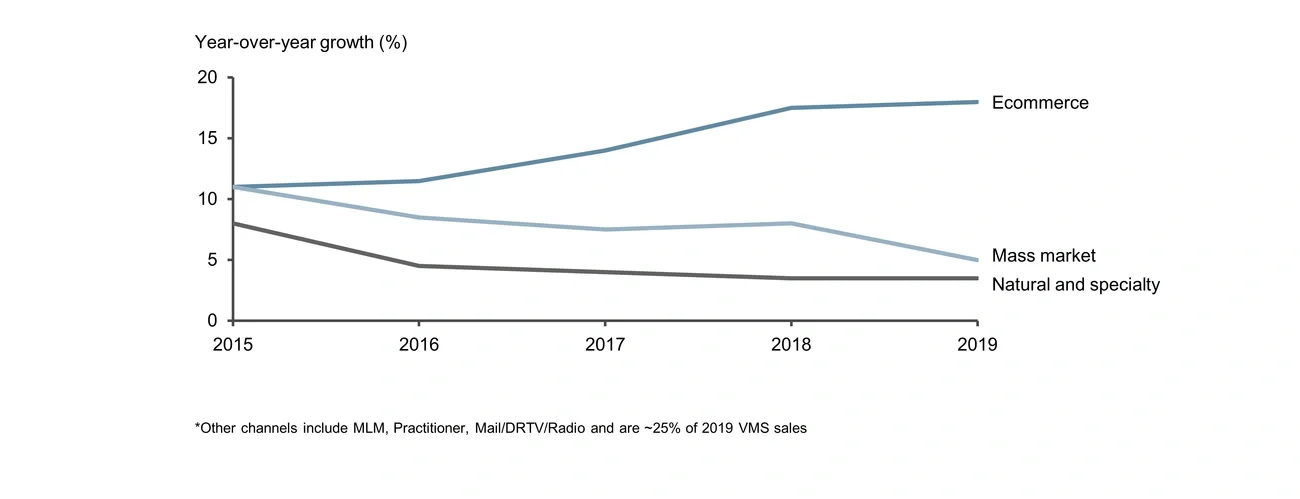

A key impact highlighted by the COVID-19 pandemic and the resulting shelter-in-place directives is the increased importance of an omnichannel capability and strategy for brands and retailers. In the immediate term, market participants invested in online and/or direct-to-consumer (DTC) access are disproportionately benefiting from consumer demand (see Figure 7).