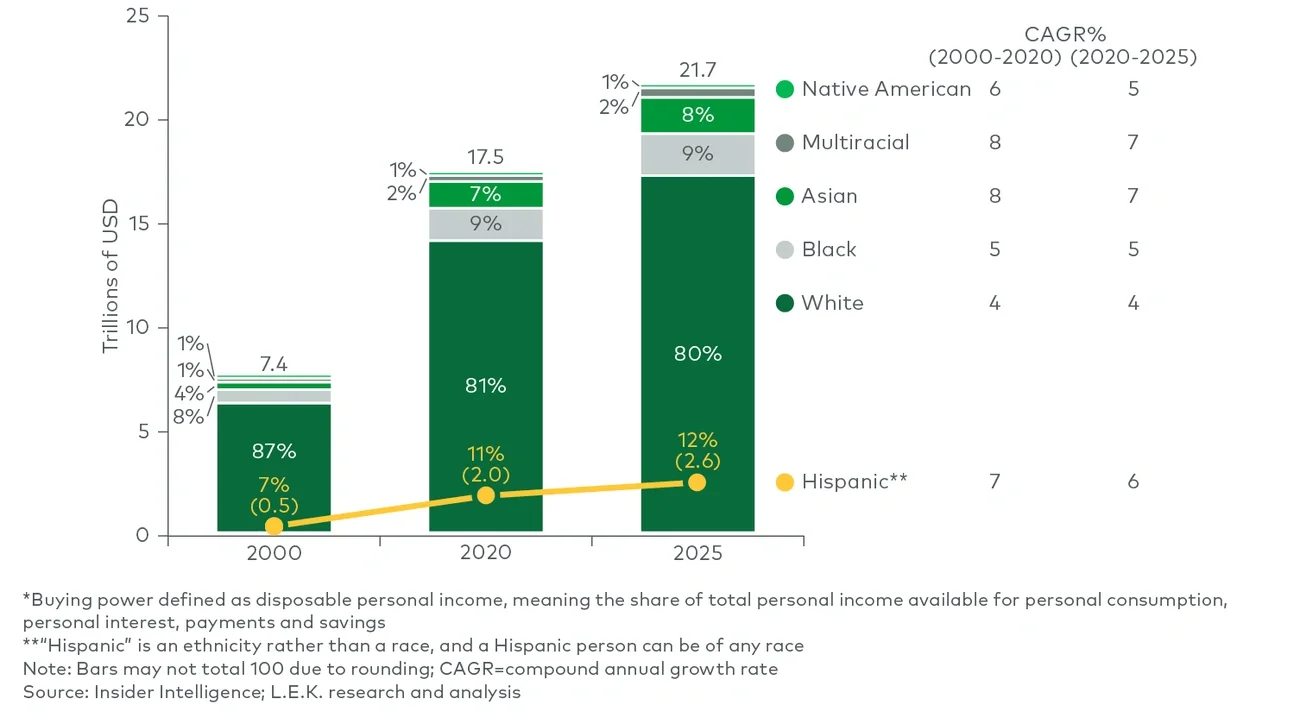

As the number of Hispanics in the U.S. continues to grow — by 2028, they are expected to account for 22% of the U.S. population, according to the data-based marketing firm Claritas — so does the opportunity for grocery retailers and food and beverage brands and manufacturers, as well as their respective investors.

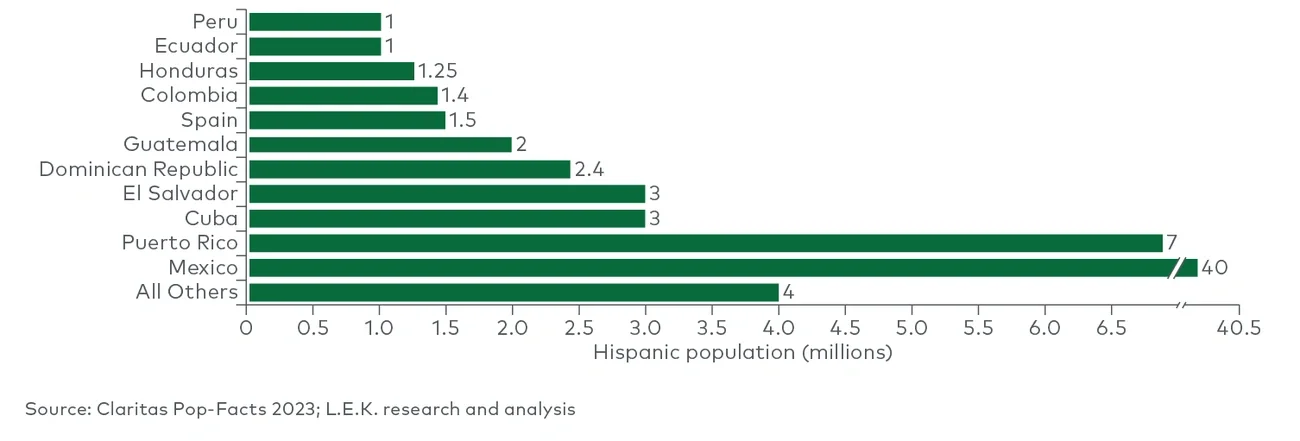

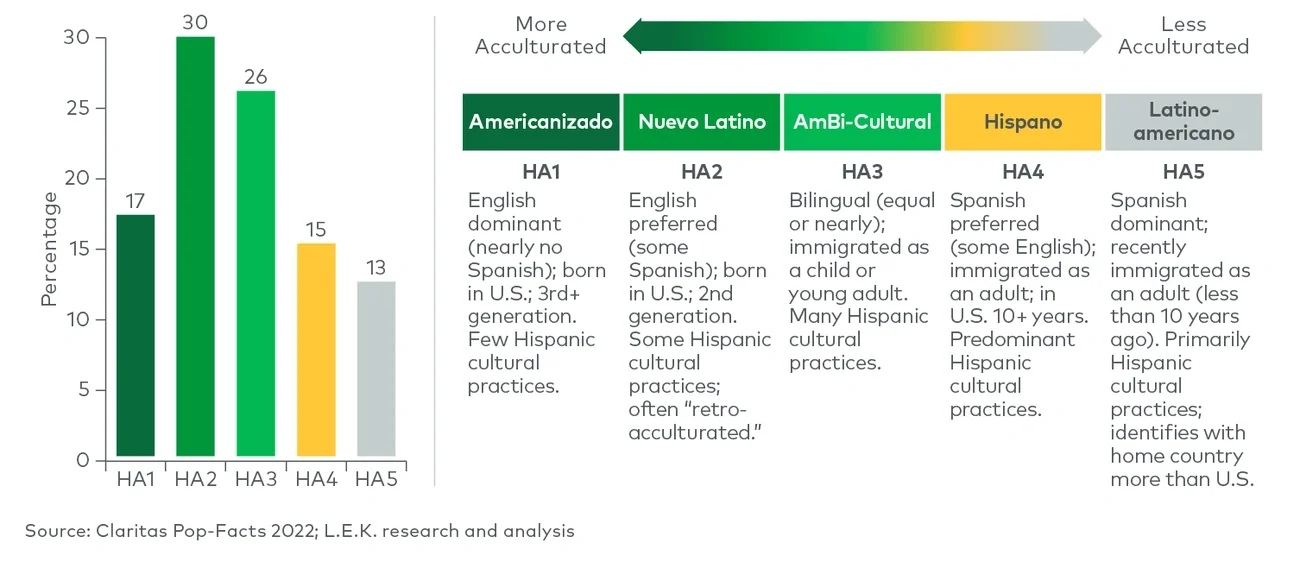

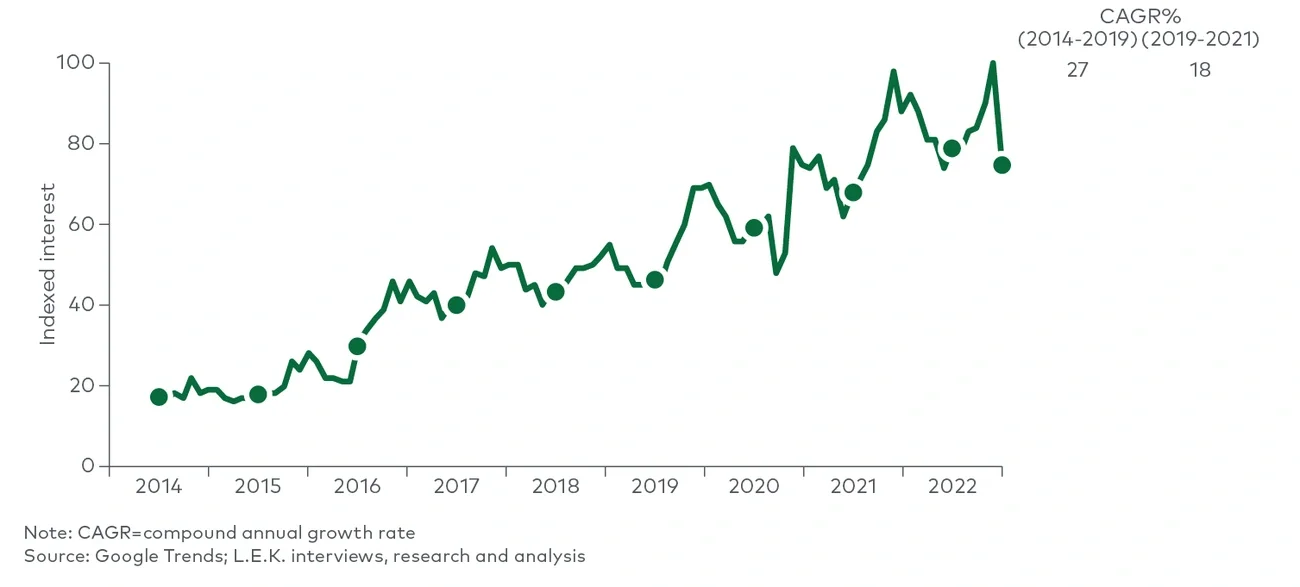

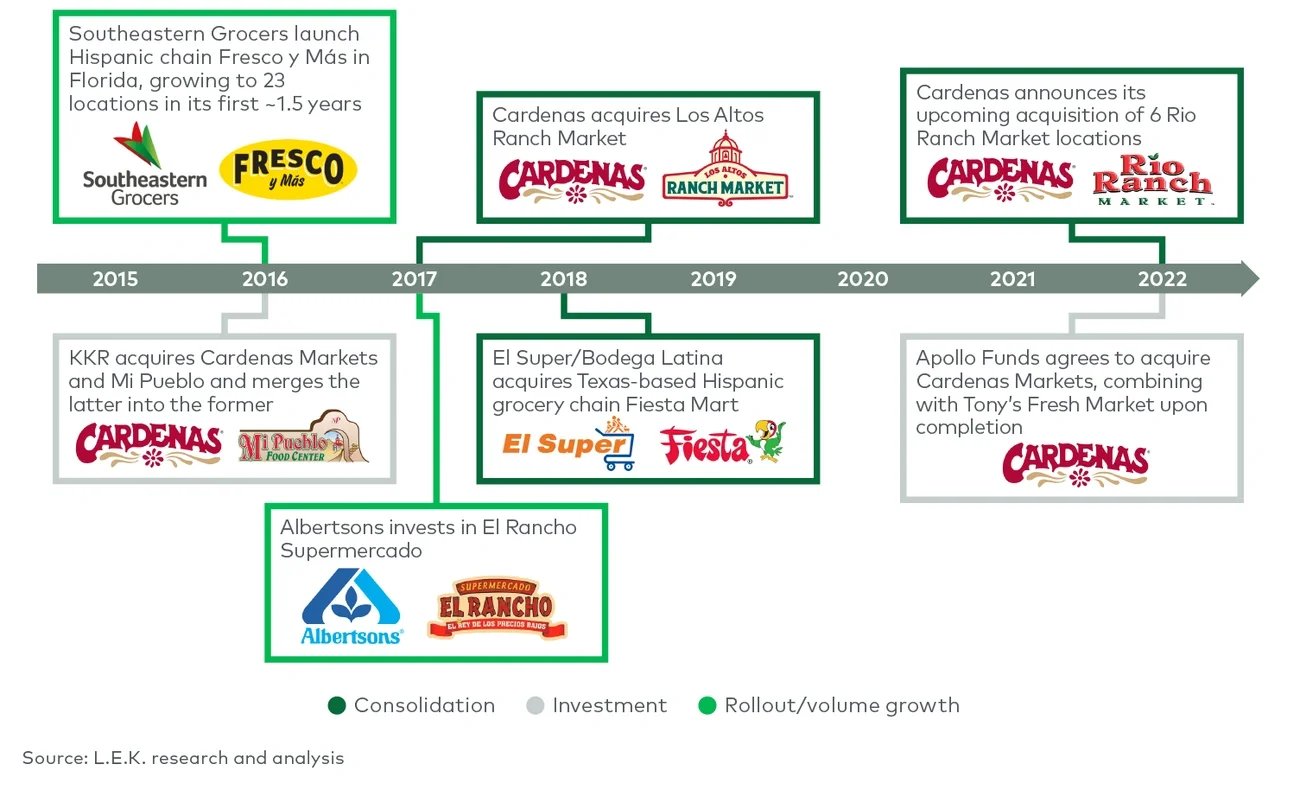

But while certain core characteristics can be applied to Hispanic food and the shopping preferences of the Hispanic population, they are a notably heterogenous ethnic group, with preferences that vary depending on their families’ countries of origin and level of acculturation and where in the U.S. they live. There is also a notable amount of expansion, consolidation and investment taking place in the Hispanic-specific grocery space — all against a backdrop of Hispanic food’s rising popularity among non-Hispanic American consumers. In this L.E.K. Consulting Executive Insights, we take a look at how, taken together, these factors present a unique opportunity for grocery retailers, food and beverage brands/manufacturers, and investors to tap into a new customer base while expanding their existing ones.

The changing face of the US population

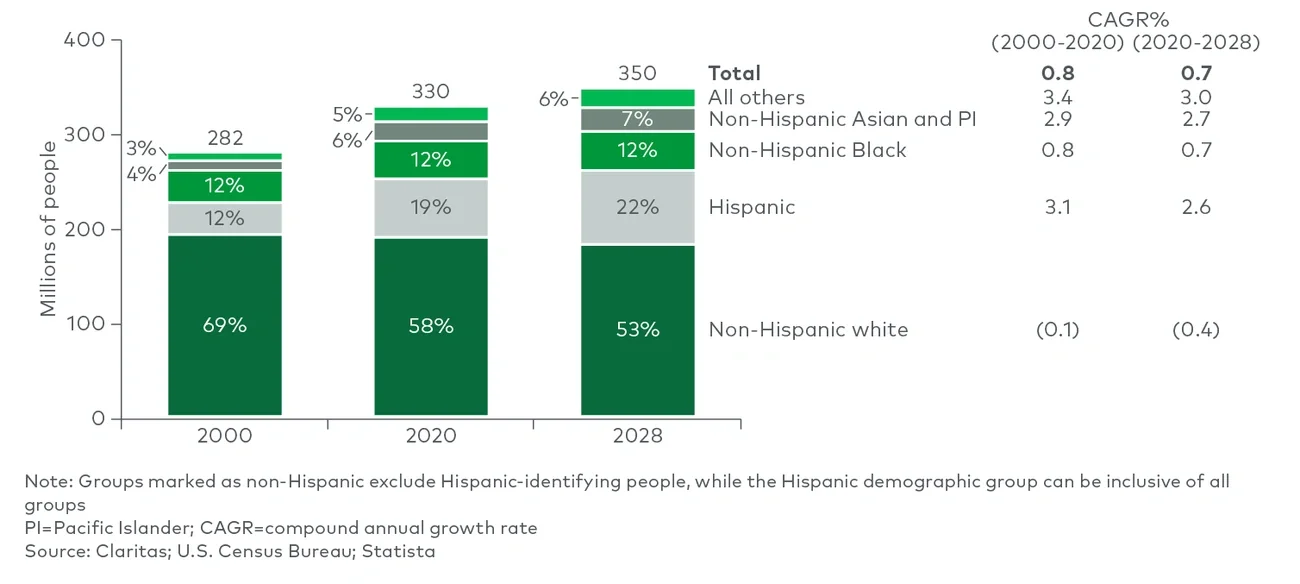

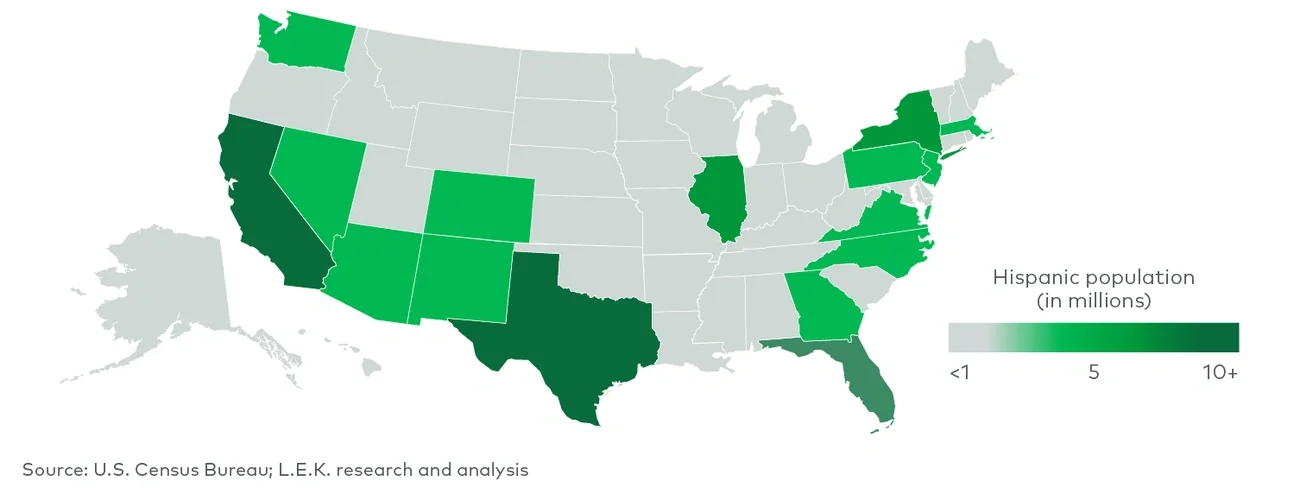

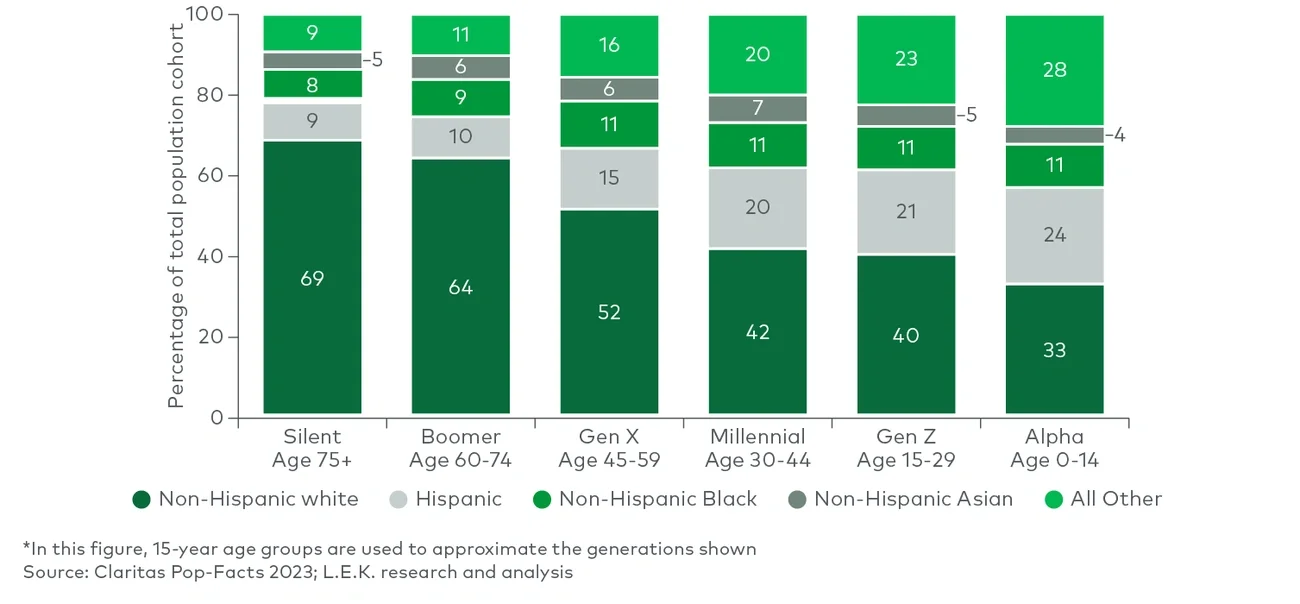

The face of the U.S. is changing — and changing quickly. Hispanics, who comprised 19% of the population during the 2020 census, up from 12% in 2000, are expected to account for 22% of the population by 2028, an annual growth rate of approximately 3%. Meanwhile, the number of non-Hispanic white Americans, who have historically comprised the majority of the U.S. population, is forecast to be flat or to decline by as much as 1% (see Figure 1).