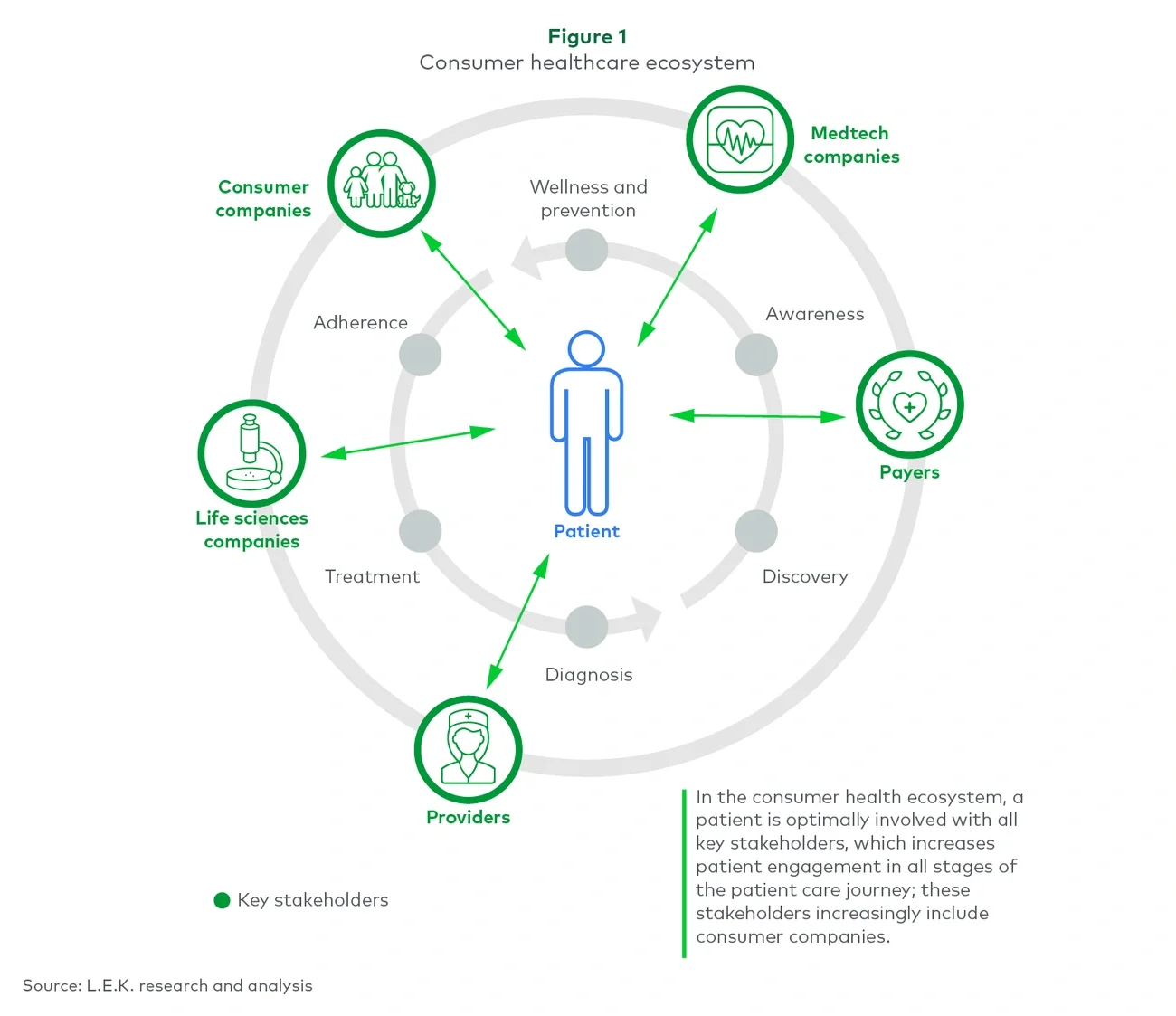

In 2021-22, consumer-focused companies became increasingly interested in diversifying into the approximately $4.3 trillion U.S. healthcare market, particularly in outpatient and other healthcare services. New entrants in the healthcare industry have been largely focused on providing services for which they can leverage their existing infrastructure — for example, clinics/outpatient services leverage established brick-and-mortar locations, and over-the-counter (OTC) remedies and supplement offerings leverage existing shelf space and supply chain infrastructure.

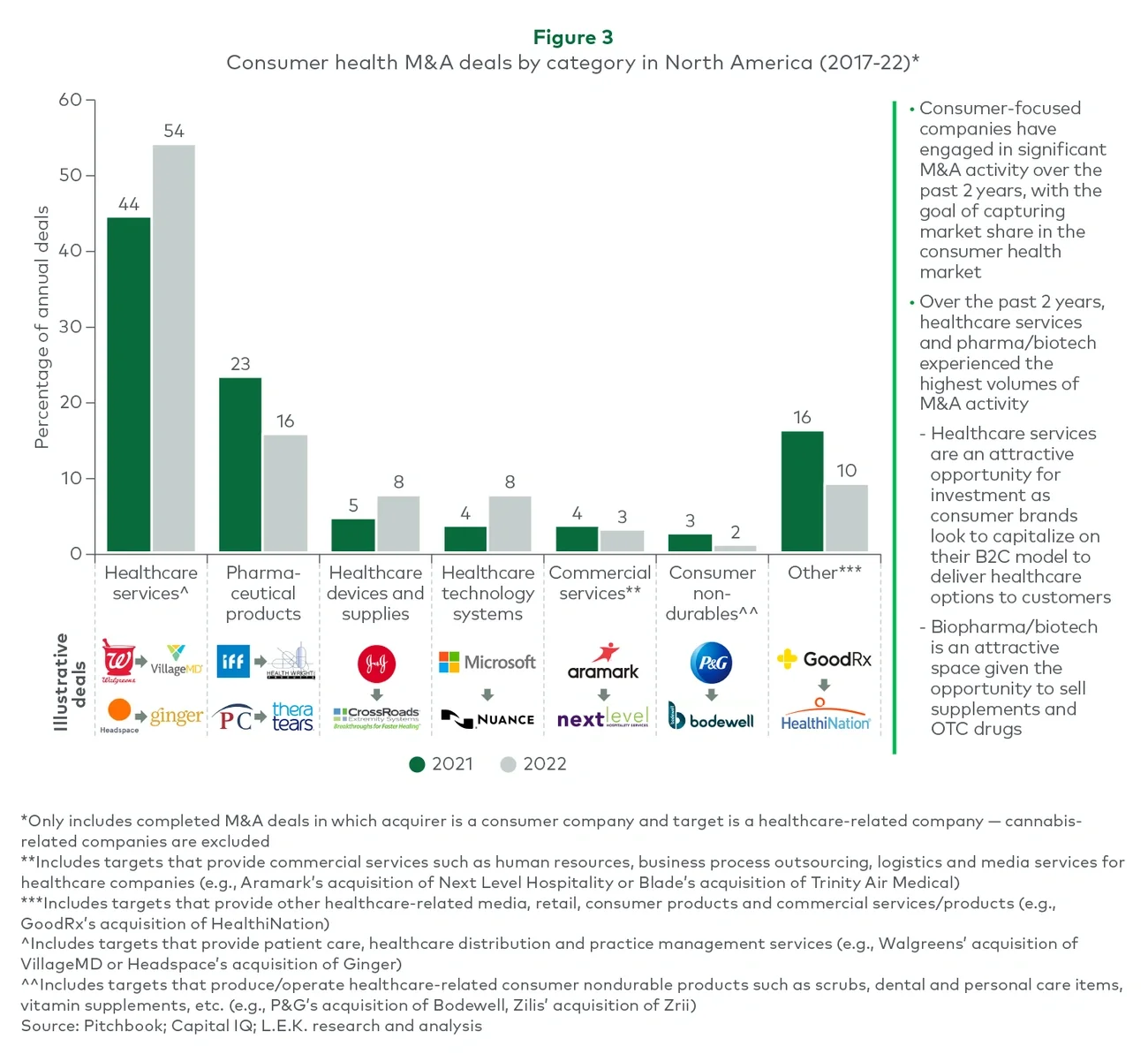

The amount of M&A activity in the consumer health space, measured by number of deals in 2021-22, was highest in healthcare services. This includes clinics and outpatient services, telehealth, at-home services (e.g., home diagnostics), and elder and disabled care.

The area of pharmaceutical products was the next most active, encompassing vitamins, minerals and supplements; OTC remedies; and animal health products. In the area of healthcare devices and supplies, the majority of companies entering this sector have existing manufacturing capabilities to make medical hardware such as diagnostic tools and devices.

Companies entering the healthcare technology space typically have prior healthcare experience and capabilities and use acquisitions to further their presence in healthcare. Healthcare technology includes health platforms or applications (e.g., well-being apps), medical artificial intelligence and online pharmacies.

The human factor clearly plays a role in consumer healthcare. Commercial services companies provide such human capital services as nurses for hire; other companies provide consulting and marketing services to promote business growth. Consumer nondurables provide ongoing opportunities for growth in the area of personal products and food products.

Retailers enter the healthcare space

Of the many high-value consumer health acquisitions in 2022, most were made by retailers looking to enter or expand their presence in the healthcare services space. Many prominent retailers are focusing on gaining expertise in clinics and outpatient services:

-

Amazon acquired primary care provider One Medical for approximately $4 billion

-

Walmart is expanding its health clinic footprint and capabilities with a 10-year partnership with UnitedHealth Group to sell Medicare Advantage policies in Georgia and leveraging Optum’s data analytical tools in approximately 15 Walmart health clinics in Florida and Georgia

-

CVS won the bidding war for Signify, a home health tech player, for about $8 billion, and it has entered into an agreement to acquire Oak Street Health

-

Best Buy acquired Current Health, a care-at-home tech platform, to supplement earlier aging-in-place acquisitions of GreatCall, Lively and Critical Signals Technologies

-

Rite Aid has partnered with Homeward, a primary and specialty care startup, to provide on-site services for approximately 700 rural Rite Aid locations

-

Walgreens has completed a series of acquisitions to gain access across the continuum of medical care: brick-and-mortar primary care players VillageMD (approximately $5 billion) and Summit Health-CityMD (approximately $9 billion), plus home health tech provider CareCentrix (approximately $1 billion) and hospital pharmacy vendor Shield Health Solutions (approximately $2 billion)

-

Nestlé acquired Bountiful for approximately $6 billion; traditional consumer packaged goods companies have shown an increased focus on healthcare through acquisitions, primarily in the pharmaceutical and biotechnology spaces

M&A trends

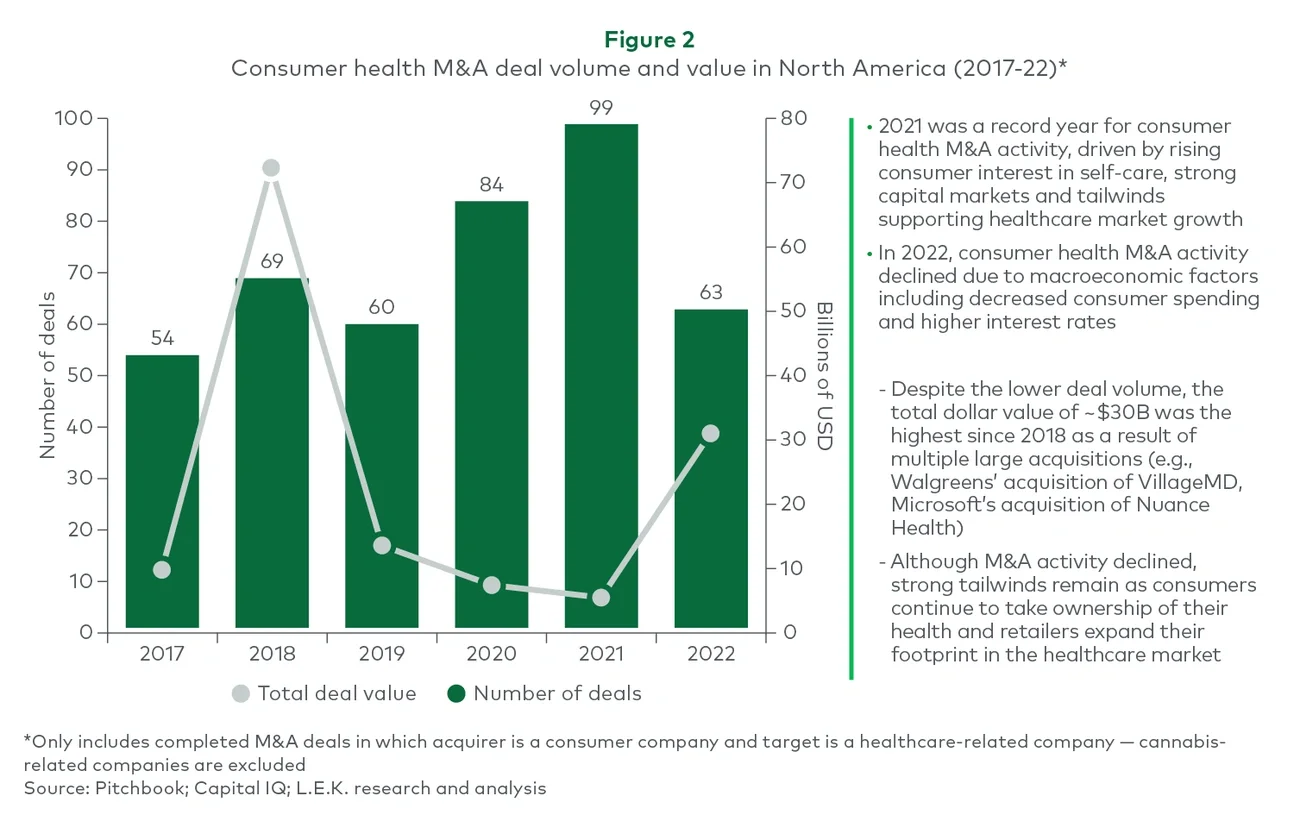

M&A values are growing. While M&A activity in the consumer health space peaked in 2021, 2022 saw fewer deals — but the deal values were higher than in the previous three years. 2021 was a record year for consumer health M&A activity, driven by rising consumer interest in self-care, strong capital markets and tailwinds supporting healthcare market growth.

In 2022, consumer health M&A activity declined due to macroeconomic factors including decreased consumer spending and higher interest rates. Despite the lower deal volume, the total dollar value of approximately $30 billion was the highest it’s been since 2018. This is a result of multiple large acquisitions such as Walgreen’s acquisition of VillageMD and Microsoft’s acquisition of Nuance Health. Although M&A activity declined, strong tailwinds remain as consumers continue to take greater ownership of their health and retailers look to expand their footprint in the healthcare market (see Figure 2).