L.E.K. Look Forward Into 2024

Welcome to Look Forward, L.E.K. Consulting’s annual analysis of the challenges and opportunities in the year ahead. In this paper, partners Adrienne Rivlin and Mark Boyd-Boland look back at a slow year for M&A in consumer health but find reasons to be optimistic for some segments in 2024.

Look Forward to M&A opportunities for segments focused on consumer health and well-being

Pent-up demand from the pandemic, strong capital markets and an increase in the consumer trend for self-care made 2021 a strong year for M&A. However, transactions fell significantly in 2022 and slowed further in 2023, largely due to a combination of the unfavourable macroeconomic environment, rising inflation and interest rates and sluggish sales in some segments due to cost-of-living pressures. Looking ahead, we anticipate more subdued M&A activity to continue into 2024, given the prevailing economic headwinds and cost-of-living challenges. Investors are more likely to hold off for improved market conditions and clarity on future product trends that will drive growth within the sector. Certain segments, however, such as vitamins, minerals and supplements (VMS), organic/ alternative products and digital solutions, are poised to sustain continued interest given the heightened consumer focus on overall well-being (both physical and mental). How will 2024 unfold? We have five key predictions for the year ahead.

Prediction 1 — Portfolio rationalisation of large consumer health players likely to resume

A recent major trend has been spin-outs/demergers of the consumer health businesses from large pharma players, most notably Haleon (GSK) and Kenvue (J&J). Adding to this is Sanofi’s planned 2024 separation. These restructurings have shifted priorities and reshaped the M&A landscape.

These newly independent consumer health businesses are expected to return to historical portfolio optimisation strategies, mirroring the M&A approach of their parent companies in the 2010s. They are also likely to maintain their category focus by divesting non-core brands.

This has been seen in the recent sale by Haleon of Lamisil to Karo Healthcare and also in Haleon’s exploration of divestment opportunities for the Nicotinell brand (as of July 2023).

Countries such as the UK have also committed to reducing barriers for pharmaceutical over-the-counter (OTC) switches, offering a potential avenue for further M&A among consumer health businesses with an OTC focus in particular.

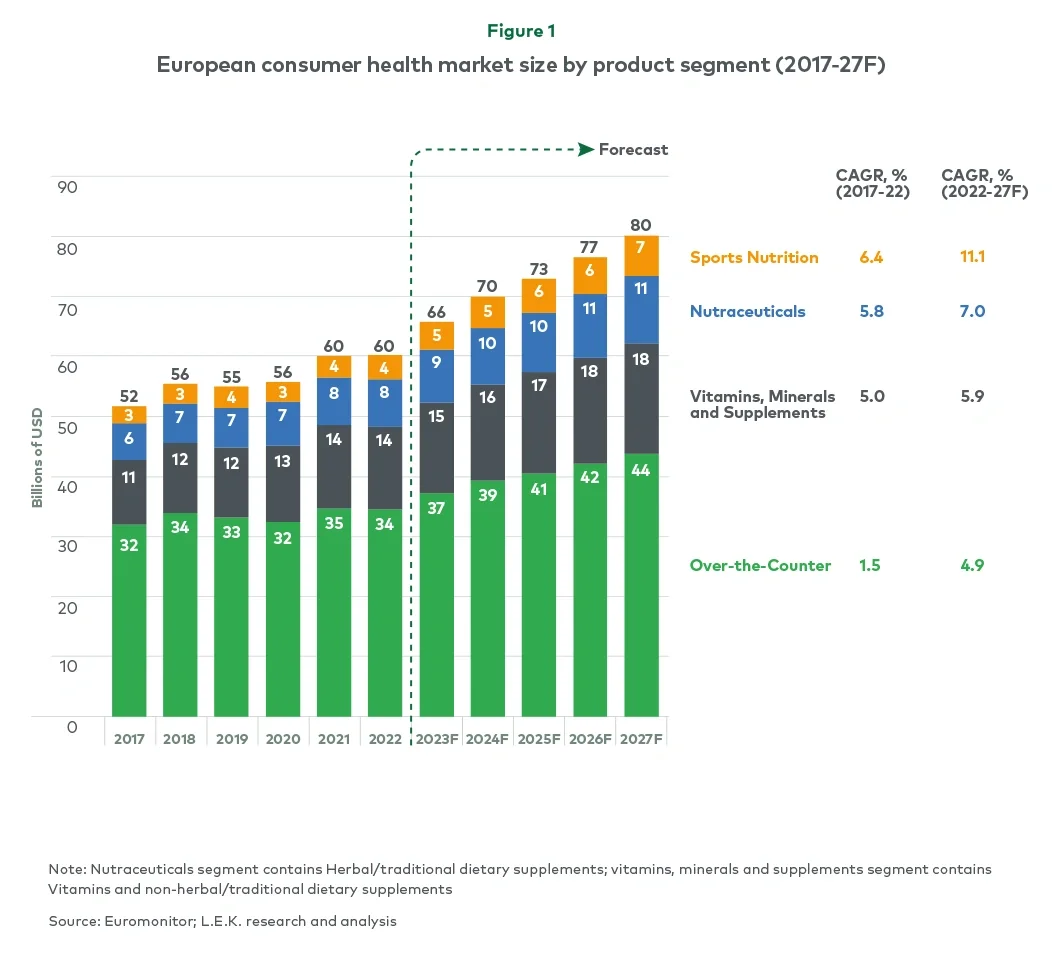

Prediction 2 — VMS, nutraceuticals and sports nutrition likely to remain robust despite recent revenue downturn

VMS and nutraceutical companies have consistently commanded strong valuations in recent years and are likely to continue to be attractive despite recent, more restrained market growth. We expect that Covid-19-linked greater consumer focus on personal health and well-being will continue to sustain product sales, particularly as consumer confidence returns fuelled by easing inflation and cost-of-living pressures.

For VMS and nutraceuticals, M&A trends are expected to mirror current consumer preferences, with an emphasis on holistic ‘wellness’ and a growing focus on ethical sustainability. Brands that have built an identity based around sustainable, organic, natural and ethical sourcing of ingredients and business practices will make particularly attractive acquisition targets.

The sports nutrition space has been the highest-growth consumer health segment of the past five years and continues to have a favourable outlook (see Figure 1).