Awareness of health and self-care among the general population has risen steadily since 2019, increasing demand for consumer health products. COVID-19 restrictions accelerated an existing shift from brick-and-mortar stores to ecommerce channels. Now that we have adapted to a ‘new normal’, how are these trends expected to shape the consumer health category?

Loading transcript...

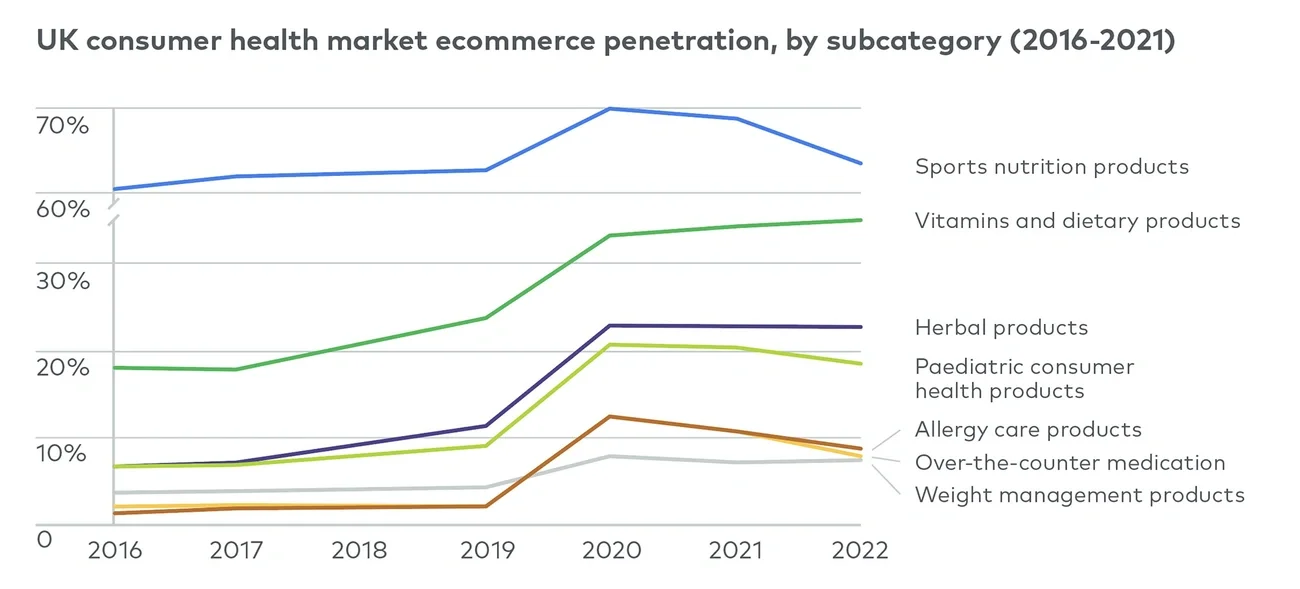

Reassessing consumer shopping trends post-Covid

Government lockdowns imposed during the pandemic and an increased focus on immunity spurred a significant uplift in online consumer health penetration, particularly for vitamins, minerals, and supplements (VMS) and ‘natural’ products. Existing pre-pandemic consumers shifted towards online channels, while new consumers discovered and purchased the category online for the first time. The speed, cost, and convenience of home delivery, particularly for heavy or bulky products (e.g., protein powder), plus the rise of subscriptions/repeat purchase options (e.g., Amazon automatic re-order) have created new purchase habits among consumers, which further accelerated growth of online purchases through 2022, with most sales occurring in the UK and Germany.

While demand for overall consumer health products has grown, the shift to online purchases has lowered the barrier to entry and significantly increased competition between brands and suppliers. Changes in pricing for marketing services from retail giants like Amazon and Google, have put additional competitive pressure on brands and retailers vying for customers online. Social media also led to the rise of digital new entrants and ‘Instagram brands’, which helped increase awareness in the category, while strong campaigns and ‘micro influencers’ promoting healthy routines and collaborating with brands converted ‘views and likes’ to purchases. However, despite the number of new entrants in the market, very few have secured a significant share in the current fragmented market.

Despite store closures, brick-and-mortar retail is slowly rebounding, driven by ‘point of need’ purchases (e.g., cold and flu remedies), particularly in Western Europe (e.g., France, Italy, Spain), where long-time consumer behaviours and pharmaceutical regulations encourage in-store rather than online purchases. To best serve all customers, most suppliers are looking for omnichannel solutions that combine their online and offline presence. As they seek to expand their footprint and differentiate in an increasingly competitive market, clear brand messaging, positioning and identity across both retail (e.g., in-store merchandising, packaging) and online (e.g., digital marketing, online ‘community building’) channels have become essential to building and maintaining brand engagement and a recurring customer base.

Many companies, including D2C or digitally native retailers, still rely on having at least one physical touchpoint, whether it is a show room or ‘pop-up’ within another existing store. Beyond being a point of sale, these can enhance the consumer’s shopping experience, and educate the consumer through sales representatives and samples, and provide opportunities for consumers to engage with products. It can also provide a more functional role, such as refilling their bulk or ‘package free’ health supplies (e.g., protein powder, tonics).

Omnichannel retail strategies have been well-received by consumers who enjoy the option to discover, browse, and interact with new products and brands in-store, the convenience of ordering products online and receiving it at home, and will likely be the primary strategy adopted by brands moving forward.

“Being only online is often not enough; even originally ‘digital native’ brands are seeing the clear benefits of being omnichannel – in terms of reach, visibility, ROI.”

— Mark Boyd-Boland, London, Partner

Image

Redefining what health and wellbeing means

In addition to changing ‘how’ consumers purchase, the pandemic has altered ‘what’ consumers buy. Whilst traditionally consumer health was focused on physical ailments, the pandemic raised awareness of mental health and holistic wellbeing, causing a surge in demand for a broader spectrum of self-care products.

Sleep quality has been a longstanding problem. However, upended routines, heightened stress levels, increased alcohol consumption, and less separation between work and personal life during the pandemic exacerbated this, encouraging many adults to seek treatment often in the form of sleep aids (e.g., sales of Melatonin rose 42% in 2020). There is similar growth for other common, and often overlooked, issues such as dehydration, poor digestive function, stress management, and depressed mood/mood support. Consumers are looking for remedies beyond pills and powers in the form of readily accessible digital therapy (e.g., BetterHelp, Talkspace), meditation apps (e.g., Calm, Headspace), and holistic routine tracking apps (e.g., MyFitnessPal, Skincare Routine, Lifesum). These digital tools enable brands to increase consumer awareness and education, cross-sell to other target consumers, and gather data to provide consumers with better/more-tailored product recommendations.

Natural remedies

Consumers are seeking to improve their wellbeing with ‘natural’ and ‘clean’ remedies made from recognizable ingredients. Some ingredients, including CBD, have been re-branded by suppliers as natural alternatives with long-term benefits and fewer side-effects than chemical counterparts. While ‘functional’ ingredients (e.g., maca root, sea moss, rhodiola rosea, yeast) have defined a new category of superfoods, aiming to promote overall well-being, reduce stress levels, improve sleep, increase immunity and solve digestive issues. Recently, they have been sold as individual ingredients (e.g., sea buckthorn powder, collagen drops) or pre-crafted blends (e.g., Bloom Nutrition) that can be mixed into food or drinks that are part of consumers’ routines.

The concoction of these ingredients requires consumers to be informed of each ingredient, however they tend to use them at their own discretion. While the US first embraced this trend of creating personalized supplement mixes, Western Europe follows closely behind with an estimated 52% of European consumers who take supplements for overall health. However, the variety of ingredients consumed is more limited – essential oils, medicinal plants, ginger, turmeric and seaweeds are among the most popular natural remedies in Europe.

Innovative delivery methods

Brands are leveraging innovative delivery formats to help customers overcome ‘pill fatigue’, stand out from competing products, improve compliance and enhance the supplement consumption experience. As of 2021, non-pill products comprised 34% of the supplement market. These innovative delivery formats include jelly/gels (e.g., Bulk), gummies (e.g., HUM nutrition), inhalers/vaporizers (e.g., Luvv Labs), ‘orodispersables’ (e.g., Vista-B12 Active) and powders (e.g., AG1, Liquid IV).

These new formats enable the category to develop new F&B segments and allow brands to shift into ‘lifestyle’ brands. For example, superfoods and supplement ingredients like matcha, chaga and collagen can now be blended into a drink, sprinkled on foods or eaten on the go. While it increases the occasions for consumption, these format changes affect the brand’s supply chain, manufacturing and packaging. Experiential health is an emerging trend that can be considered a delivery method; while still somewhat niche, consumers are turning to quick-fix clinics to top up on vitamins (e.g., B12 administered through IV drips) or boost recovery from dehydration, lack of sleep, etc.

Personalization of products

Consumers seek to support their investment in personal health with products that align with their unique lifestyles.

The pandemic sparked demand and ‘willingness to pay’ for customised, data-driven health solutions amongst consumers, particularly those aged 30-44, where the data is collected from fitness tracking wearables, apps and consumer quizzes.

In recent years, the cost of wearable tech has decreased, making devices like fitness trackers more mainstream. It has also become more accessible and ‘normal’ to monitor and measure one’s statistics (e.g., heartrate, BMI, hours spent in REM). The volume of data collected means that health brands have broadened the use cases they support, including menstruation, pregnancy, menopause, weight management and management of underlying health conditions (e.g., diabetes).

Through purchased data or online quizzes (e.g., Care/of), brands can personalise both the purchase journey and the recommended products to consumers based on their typology. They may also offer additional elements of customisation in the form of personalized packaging, bundles and budget. Traditionally, these ‘customized’ products have been offered by online-only brands, but large health brands (e.g., Nurish by Nature Made) have entered the space, leveraging existing supply chains and repackaging products into ‘custom’ products at lower price points. However, further innovation is required to provide true personalization on an individual basis (e.g., bespoke formulations). Many companies are actively building innovation pipelines to develop and delivery these solutions at scale.

“Personalisation is the new premium, and companies who offer tailored solutions may build stronger recurring customer bases then those who do not.”

— Adrienne Rivlin, London, Partner

Sustainability

Sustainability has become an increasingly key topic for all sectors, and for consumer health, that means consumers have an interest in eco-friendly, natural products. In response, many brands have prioritized R&D for products made from natural, cruelty-free and/or vegan ingredients or eliminated single-serve packaging. To reduce their carbon footprint, some companies have sought to manufacture products ‘close to home’ or used locally sourced ingredients, which has increased in-house and local contract manufacturing in Western Europe. Brands stand out with clear messaging, clean and recyclable or compostable packaging with natural ingredients.

Beyond changes to the products themselves, customers are looking for brands, and their owners, to embrace a holistic environmental, social and corporate governance (ESG) approach. Consumers are increasingly factoring the actions brands have taken to address sustainability shortfalls in their own operations and supply chain, communication of environmentally friendly initiatives and social policies, and overall transparency into their decisions of where to spend money.

The outlook for 2023 and beyond

In the wake of the pandemic, consumers have taken a more holistic view of health, expanding their needs beyond remedies for physical ailments to a more holistic approach rightly encompassing mental health. Consumer focus on holistic health and demand for products that broadly address existing (e.g., anxiety reduction) and new (e.g., improvements to poor sleep quality) well-being needs and accompanying solutions from consumer health brands are expected to see continued growth in 2023 and beyond.

Consumer demand is changing. Choosing ‘clean’, customised, and convenient products is increasingly common. Although the ongoing ‘cost of living’ crisis adds pressure on the market, health brands must be more innovative in how they differentiate, win new consumers and retain a loyal customer base. There are many areas in which they can innovate – ingredients, distribution, marketing, formats, packaging and pricing – however, they should ensure that they have a clear message and product that can be integral to their customers’ daily routines and rituals.

Why L.E.K.?

Our focus is on helping clients track and anticipate consumer trends, refine their value proposition, and create business strategies that deliver long-term sustainable growth.

Related insights

You might also be interested in these insights.

English