Rapid and unabating growth for new solar installations suggests an attractive profit pool for players up the value chain, including manufacturers; engineering, procurement and construction (EPC) companies; and installers. And in the near term it is difficult to argue against the trend, especially with a Biden administration climate agenda. While 2020 saw the broader industrials production index fall (7%), global energy demand decline (5%) and oil prices drop (31%), solar capacity across all segments in contrast grew 23% over the same period and even outpaced its 20% growth rates in 2019 and 2018. However, a myopic view of the outlook may miss the longer-term profit pool trend ― that value is shifting downstream to asset management and performance optimization through software and software-enabled field services.

Rational exuberance

Total solar capacity grew 23% in 2020, the utility scale segment’s capacity grew 28%, and annual utility scale gigawatts of new solar added reached a high-water mark exceeding 12 GW last year. As a result, companies across the value chain benefited, especially those leveraged to new installations. The public solar universe confirms this assertion with notable public companies such as Array ― a tracker manufacturer and newly public company as of October 2020 that offers a sign of market optimism in its own right ― citing ~60% year-over-year growth through the first three quarters of 2020. Beyond the public company set, private companies and investor clients of L.E.K. Consulting voice similar financial health coming out of 2020 and continued optimism for both the 2021 installation outlook and the view over the next five years.

The optimism is buoyed by the blue wave that eventually carried through all branches of government. Following the top ticket results, momentum picked up and a solar investment tax credit (ITC) extension ― set to step down from 26% to 22% in 2021 and then down to 10% in 2022 ― appeared inevitable. Although this policy mechanism that occurred through budget approval in late December is a bit surprising, it is a welcome one and is expected to support market growth. Given the safe harbor policies in place that help lock in ITC benefits for the years that follow the expiration, the ITC extension is expected to benefit 2024 and 2025 installations substantially more than immediate-term growth for 2021 or 2022, which may already have ITC-secured orders.

With full congressional support and a Biden clean energy agenda already taking shape, there is no lack of optimism at the moment. The result is likely to be a boon for development and the associated value chain that supports it. However, the solar asset installed base ― for utility scale in particular ― is maturing, and new installations will increasingly account for just a fraction of total installed capacity, suggesting some of the value is shifting downstream.

An overlooked presentation of the growth story

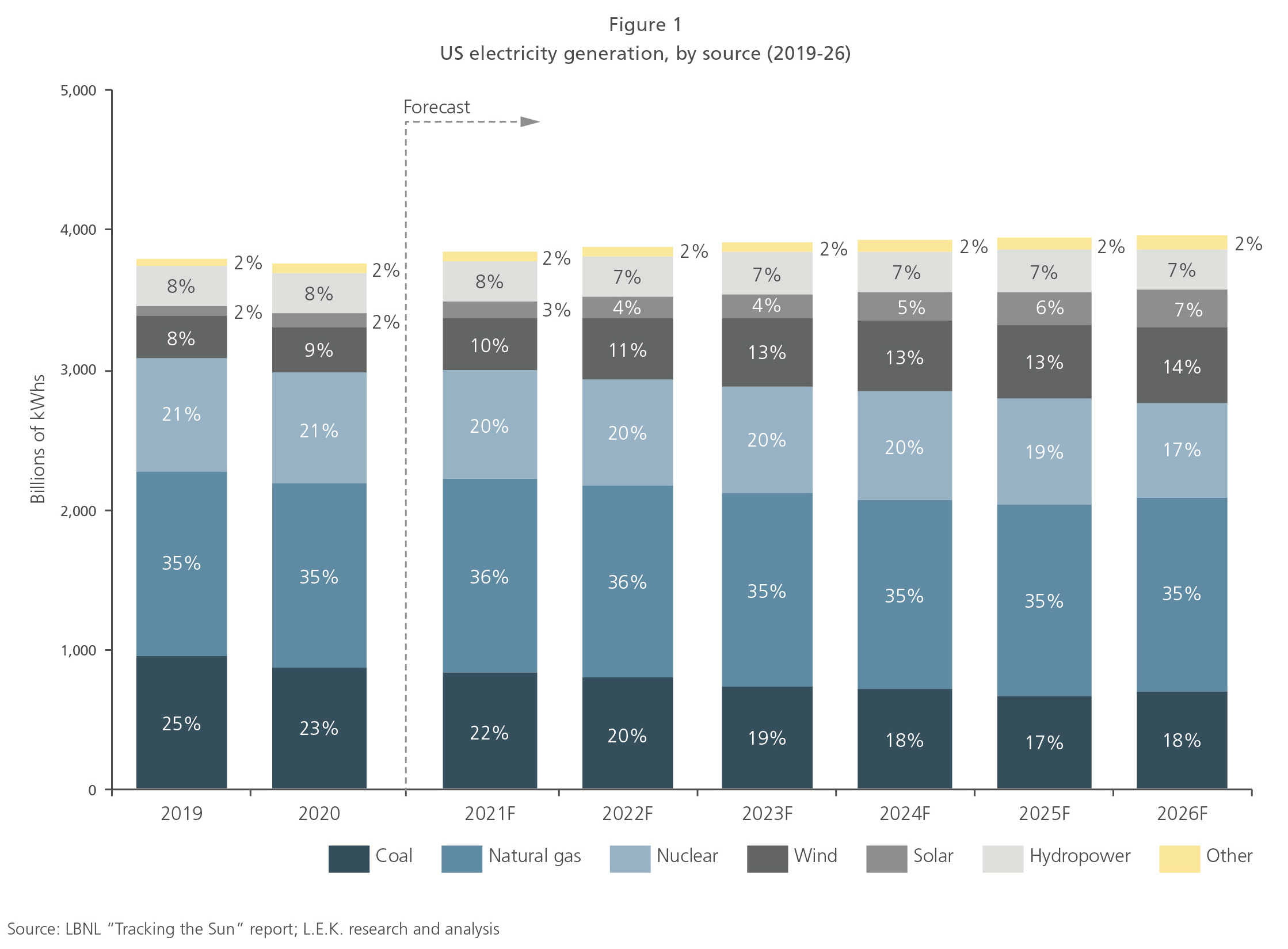

Myopia in this case is easy to understand within the context that the most-cited market research typically focuses on one or two charts. The first is generation (see Figure 1), which is used to highlight and articulate the narrative that solar, and renewables more broadly, continue to take share from coal, and to a lesser extent nuclear. This is a common way to frame the energy transition’s progress in the power sector.

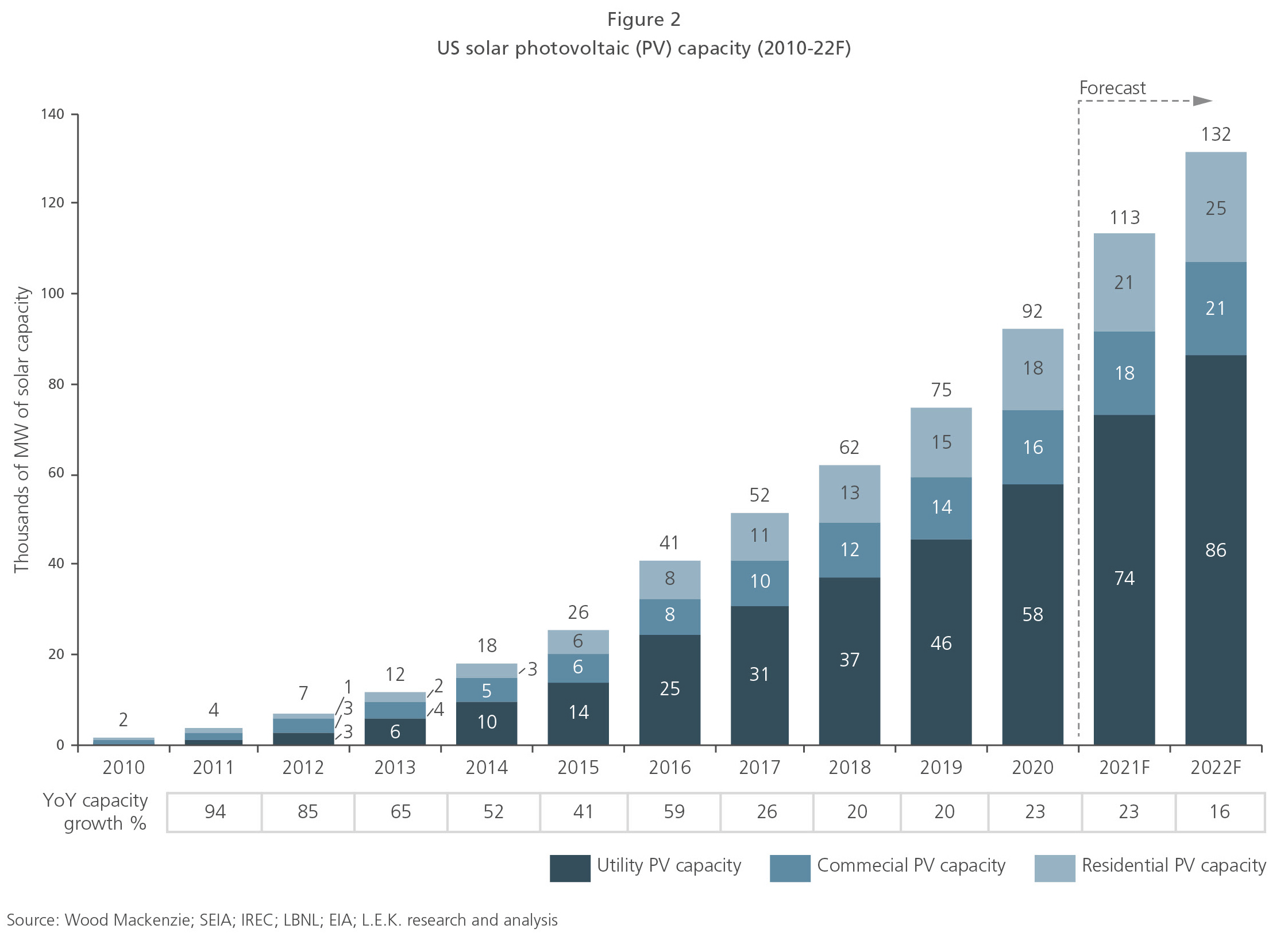

The second chart (see Figure 2) typically highlights new installed capacity either on an annual or cumulative basis. This is also understandable as new installations remain the fundamental driver for spend across the solar value chain from panels, inverters, trackers and balance of plant equipment to EPC, installation, and other subcontracted mechanical and electrical services.

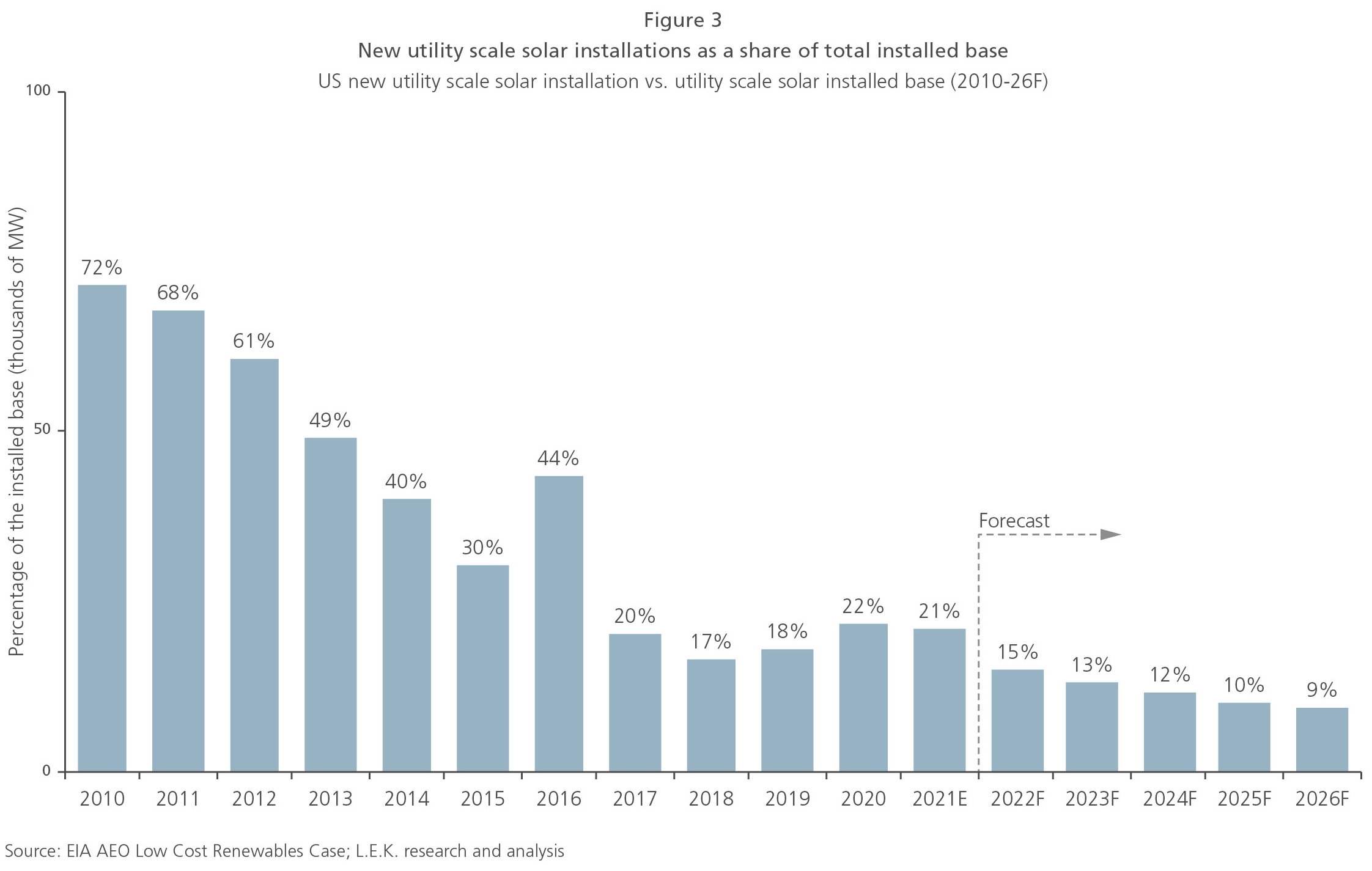

But there is another analysis often overlooked ― the new installation volume’s share of the total gigawatts installed base. Transforming this data highlights the maturation in the market, and by 2026, new installations are currently expected to account for less than 10% of the installed base, even when considering the boon from the Biden administration and further policy support (see Figure 3).

Implications for the value chain

Over the next five years, steady robust growth in utility-scale solar installations will undoubtedly drive spending for equipment and services leveraged to new installations. We expect inverters, energy storage systems, tracker systems and electrical balance of system suppliers to benefit most on the equipment side, and leading EPCs and installers to benefit on the service side. We are only just starting to see that the power of storage-paired solar and grid flexibility benefits ― load balancing, dispatchable capacity and other ancillary services ― may drive even further upside for the sector beyond what is referenced in this note.

However, growth at this pace is finite, and as the utility-scale market matures, the focus on optimizing asset performance and maximizing the return on assets will become paramount. More specifically, we expect operations and management services and asset management software segments, though relatively smaller in market size today, to increasingly capture more of the market’s profit pool.

Given this context, as a manufacturer or service provider leveraged to new installations or an investor looking at opportunities to play across the solar value chain, there are a number of strategic considerations for how to play the downstream value shift:

- Position to capture near-term installation growth, which has upside from solar plus storage, but remain aware of the slowing growth profile toward the middle of the decade

- EPCs and installers may seek to build or buy operations and maintenance (O&M) service capabilities

- Although high single-digit and low double-digit margins may not appear attractive, there are value creation opportunities in field services today from remote management solutions and more efficient dispatching

- Asset management software adoption is underway, and there are opportunities to play on the technical and performance side as well as through nontechnical solutions addressing contracts, work orders and centralized financial management

- Other utility market software competitive structures suggest this market will not remain as fragmented as it is and the potential winners are already emerging

The solar market continues its growth phase, but investments to capture growth today must also consider the longer-term maturation of the market and ensure corporate and investment portfolios will be positioned to capture value as the market migrates across the value chain.

01272022090134