It’s essential to understand the specifics of each value chain application — the cost and carbon impact of production, the logistics of hydrogen delivery, the timeline for the introduction and full realization of each hydrogen use case, and the local government’s plan to facilitate its development. Only then may hydrogen be fit into a company’s investment strategy, operations or integrated resource plan.

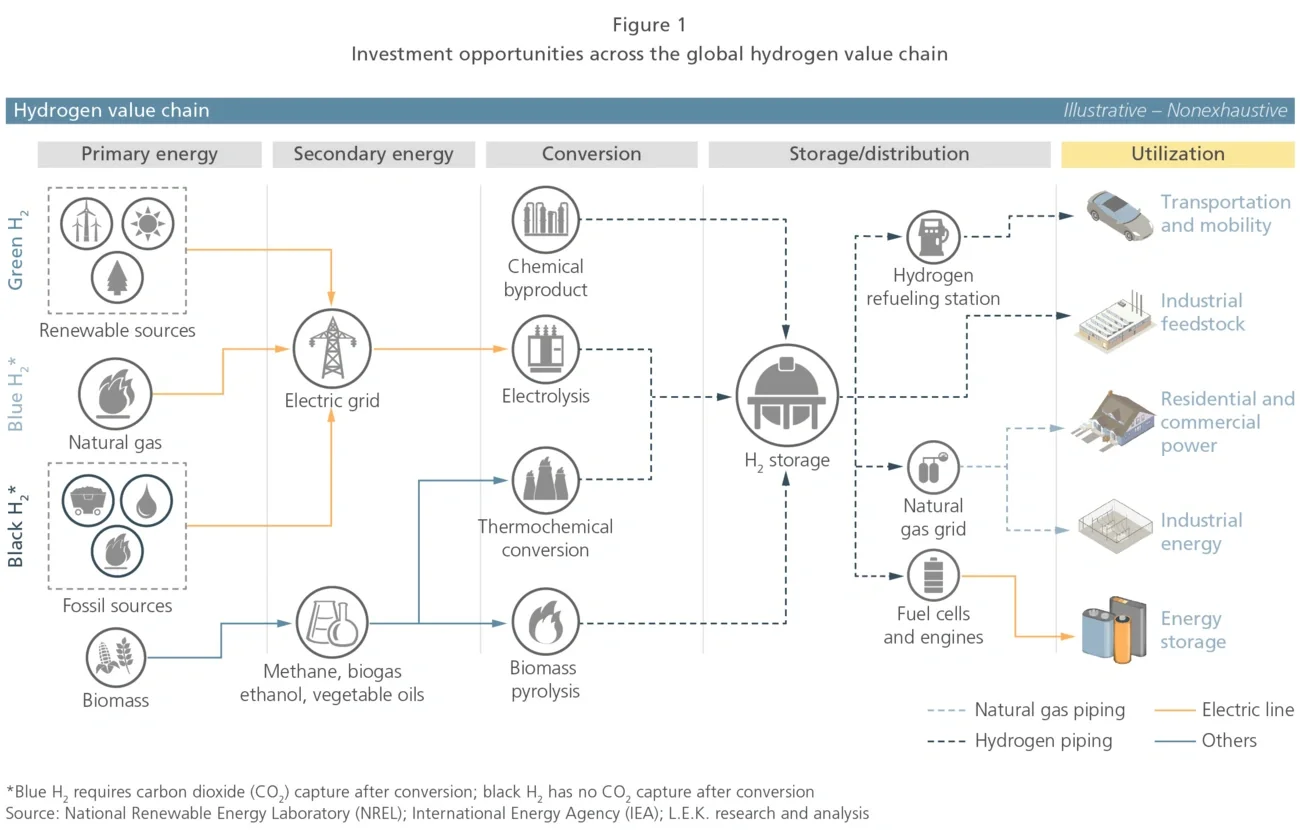

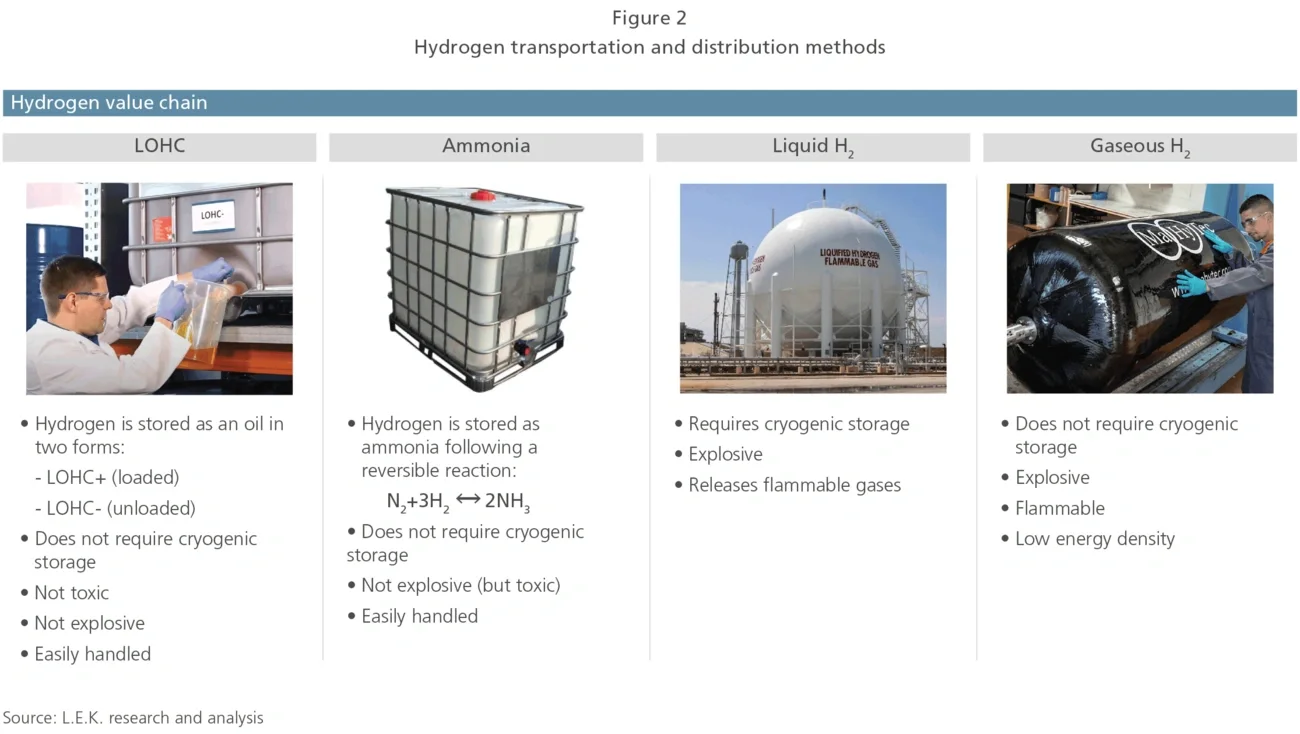

- It’s critical to know the value chain. There are many relevant, strategic and attractive investment entry points across the hydrogen value chain. In hydrogen production, hydrolysis technology (particularly alkaline, polymer electrolyte membrane and high temperature electrolysis) is attracting most investment interest given its relevance to the realization of the green path. It presents challenges related to cost-effectiveness and energy efficiency. For storage, the cost and energy density drawback limitations are driving more research in solid state or LOHC storage.

- Be mindful of production costs and regional competitive advantages. Fuel input cost and capital expenditures are the two most important categories driving hydrogen production economics. For black (gray) hydrogen from natural gas, fuel — the largest cost component — accounts for between 45% and 75% of production costs. Low gas prices in the Middle East, Russia and North America give rise to some of the lowest hydrogen production costs. Gas importers like Japan, Korea and India have to contend with higher gas import prices, which makes for higher hydrogen production costs from steam methane reforming and partial oxidation processes. On the green hydrogen front, dynamics are similar, but in contrast will favor regions with a large installed base of onshore solar and wind resources. In this case, gas importers with high solar penetration, such as Japan, may see green hydrogen as the only economic pathway, while countries targeting a balanced energy mix, such as the U.S., must consider the black vs. green tradeoffs.

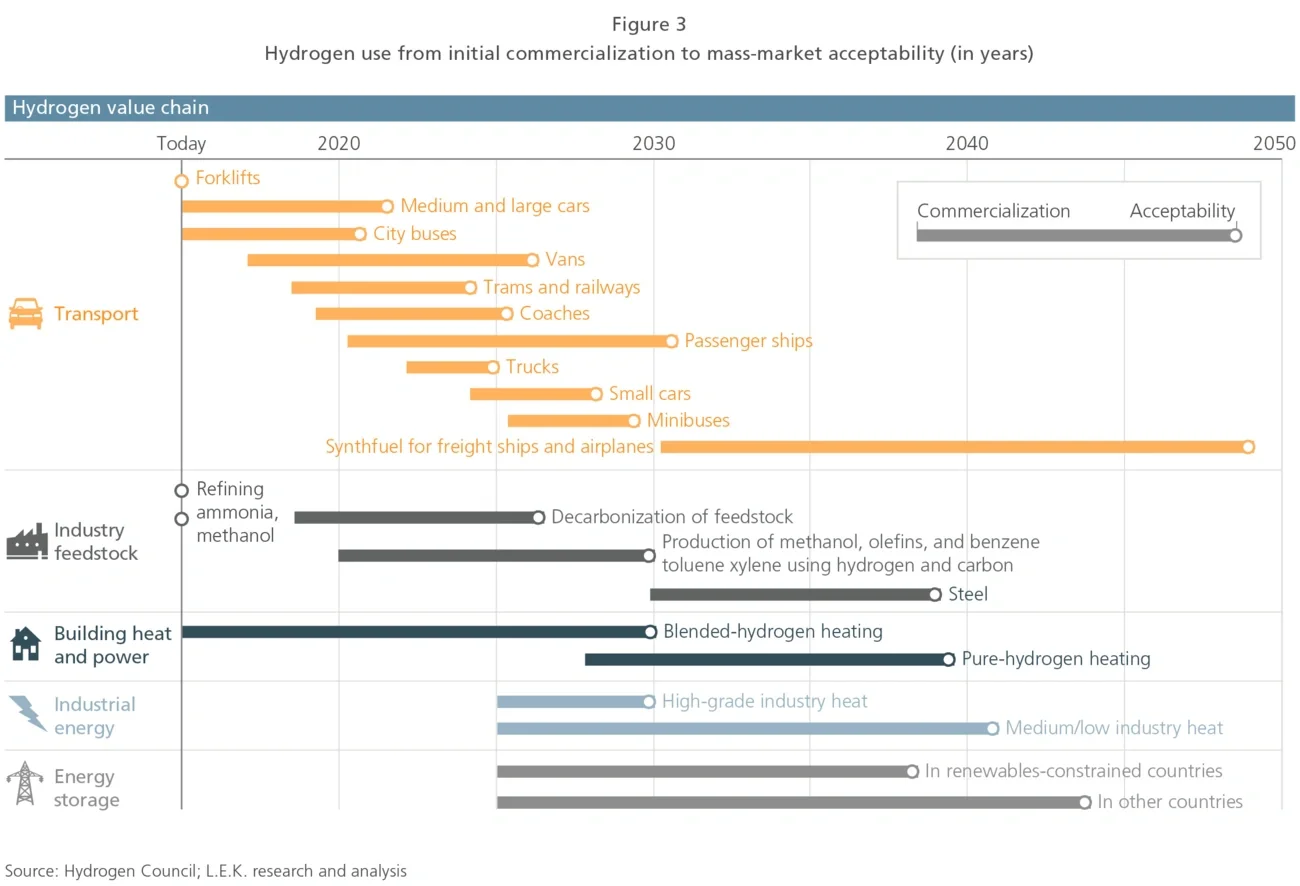

- End-use applications will mature over time — but large-scale adoption will take longer and for some applications will be measured in decades rather than years. Some hydrogen applications will arrive within the next few years. Hydrogen-powered forklifts are already a reality, and cars and urban buses will reach full maturity by mid-decade. Others applications will take longer. Building heat and power partly based on hydrogen will be mature in 2030, but pure hydrogen heating will take another 10 years for widespread adoption. The timeline for industrial energy is similar. Hydrogen for industrial production of feedstock, methanol, benzyne and steel will appear in stages over the next 20 years. Hydrogen-based synthfuel for cargo ships and large airplanes will not begin to arrive until 2030 and won’t reach full maturity until closer to 2050.

- Government policies will drive demand. Increasing demand for hydrogen is in part promoted by government legislation in several countries, allowing for faster adoption of hydrogen in the power/fueling system. According to recent research conducted by the International Energy Agency (IEA), the number of countries with policies that directly support investment in hydrogen technologies is increasing, along with the number of sectors they target. However, most government dollars today are allocated to transportation solutions, as battery solutions for long-haul commercial vehicles remain limited.

Examples of these policies include Australia’s Clean Energy Finance Corp. (CEFC) announcement that it will provide incentives for transportation end-use investments, as well as the “Hydrogen Global” initiative promoted by the World Energy Council and backed by multiple countries, corporations and institutions in order to support energy decarbonization programs. In addition to Australia, other relevant countries/regions promoting a higher use of hydrogen include Europe (led by France, Germany and Norway), China, Japan, Russia and the Middle East (led by the United Arab Emirates).

In developing your own strategy for hydrogen participation, and in considering specific investments, ask these questions:

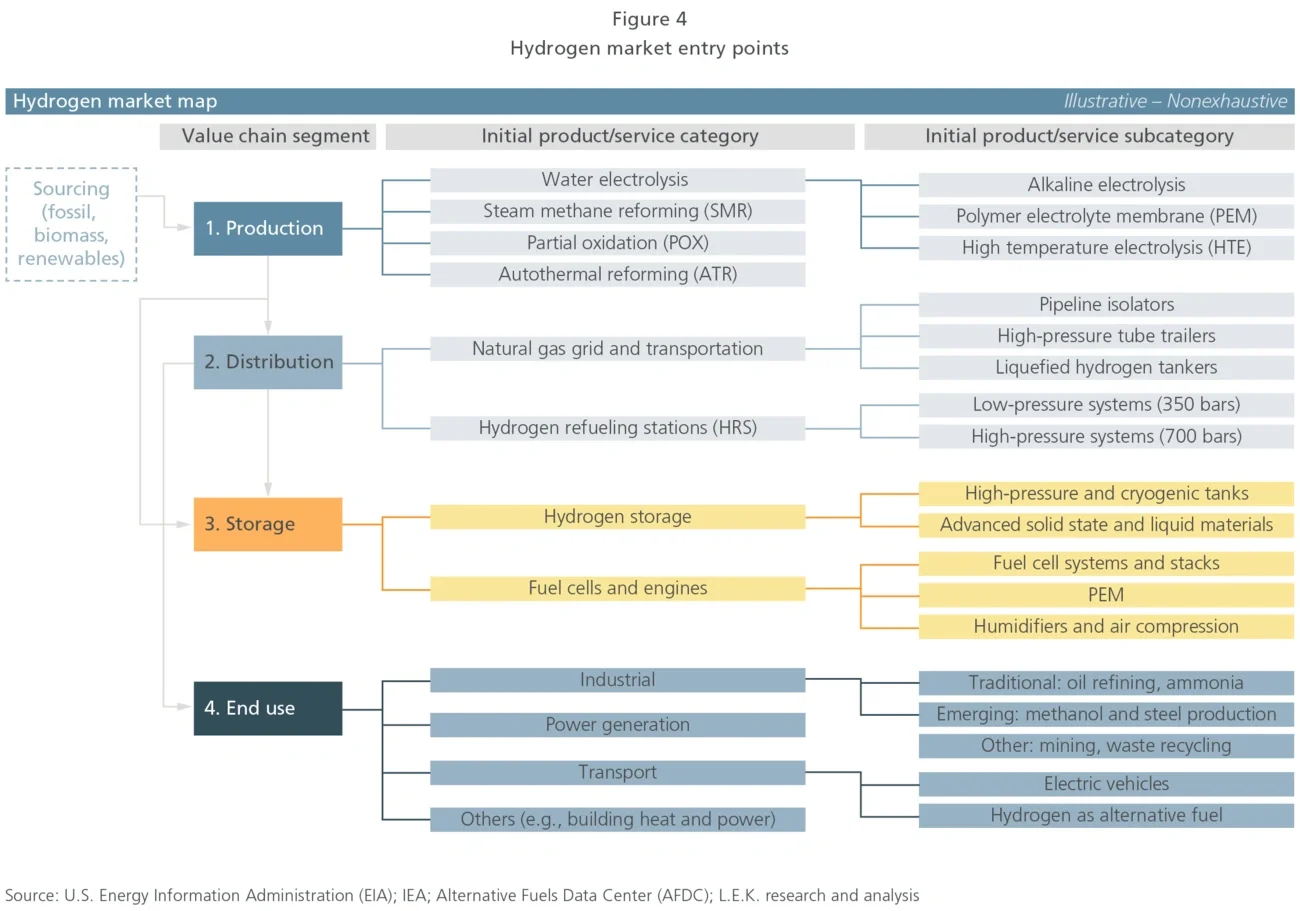

1. What are the emerging hydrogen technologies and initiatives currently in development? In the search for attractive investment opportunities in the hydrogen sector, investors must first understand the technology landscape of current and emerging solutions in development along the hydrogen value chain, including production and conversion (e.g., green hydrogen, electrolysis, biomass conversion), storage and transportation/distribution (e.g., stations, networks), and end-use applications (e.g., transport and mobility, industrial feedstock).

2. What are the key enablers to commerciality, and over what period of time will they be realized? The wide gap between hydrogen technologies in a conceptual phase and actual solutions currently being implemented in the field makes the question of commerciality highly sensitive for investors. While looking at the options, investors must develop a deep understanding of the technology maturity life cycle, the commercial viability (e.g., upfront investment, operating costs, scalability) in current versus future adoption conditions, the technical viability (e.g., technology readiness, appropriateness in addressing stakeholder needs and innovativeness) and the strategic advantages of hydrogen technologies versus alternative solutions (e.g., efficiency, density, footprint, maintenance, life span).

3. Which companies are positioned to benefit from those technologies? How does the investment scenario and timeline for technologies impact individual companies? What are the implications for feasibility, cost and time to market? Which companies are in the lead today, and which are building a capabilities system enabling a sustainable competitive advantage?

4. How should investors and companies think about portfolio fit and synergies? Finally, players must look into their own portfolios and carefully assess the potential fit of hydrogen technologies and companies in their mix, considering not only financial and commercial elements but also the feasibility of leveraging current capabilities and relationships that can potentially drive opportunities and risks for their respective integrated businesses.

With those answers in hand, investors and strategic participants can proceed to develop fully informed strategies for the emerging hydrogen economy. Make no mistake — hydrogen is an extremely promising and remarkably versatile energy source. It has the potential to be truly transformative and to open the door to a greener future. But as we’ve only described briefly, there are many complexities, and the risks and barriers can easily trap the impulsive or ill-informed. Knowing the issues and the pitfalls is an essential step toward investments and ventures that will ultimately deliver on the hydrogen promise.