Sustainability1 is more important than ever. In just the past few months, we’ve seen growing political commitments to net zero, stricter developments in corporate sustainability reporting and a general acceleration of businesses’ sustainability plans.

Investing has exploded. Capital inflows to sustainable funds, the number of financial institutions committing to low-carbon investment and the value of sustainability funds launched are all at record levels. In part, this is due to a long-term evolution in investor attitudes and behaviours. ESG is also more important to society at large, particularly climate-conscious younger generations, and women — who are twice as likely as men to say it is ‘extremely important’ that their investment portfolio considers ESG factors. On top of this long-term trend, the coronavirus pandemic has further accelerated awareness of ESG in investing.

But there is still no clear definition of what ‘sustainable investing’ means, and the market has attracted a lot of negativity. We’ve seen greater scrutiny of what sustainable funds invest in, growing scepticism about those with potentially harmful products like tobacco and sugary drinks, increasing controversy over the definition of ‘net zero’ and ‘creative carbon accounting’ (such as a high-profile debate over Mark Carney’s Brookfield claims), and even a US Securities and Exchange Commission (SEC) warning over ‘misleading’ claims by ESG fund managers.

There has been particular confusion in the private markets. While 63% of UK private equity (PE) firms now take ESG principles into account in their investments, lower reporting requirements and accountability compared to the public markets has meant a wider variety of sustainability strategies and higher scepticism about their impact. As one report sums up, most PE ESG approaches are “nascent and superficial”.

Our experience resonates with these issues. Since the pandemic struck, we have spoken to over 100 corporates, investors and experts on sustainability. We’ve learnt that there is a lack of consistency in how sustainability is defined, measured and reported, and many organisations are unsure how to pursue a strategy that maximises value for investors, investees and society at large — and takes far greater responsibility for the planet.

In this article, we aim to help PE investors as they approach ESG. We explain key elements of the sustainable investment landscape, share our core observations on future developments and highlight recommendations for a way forward.

Types of sustainable investing

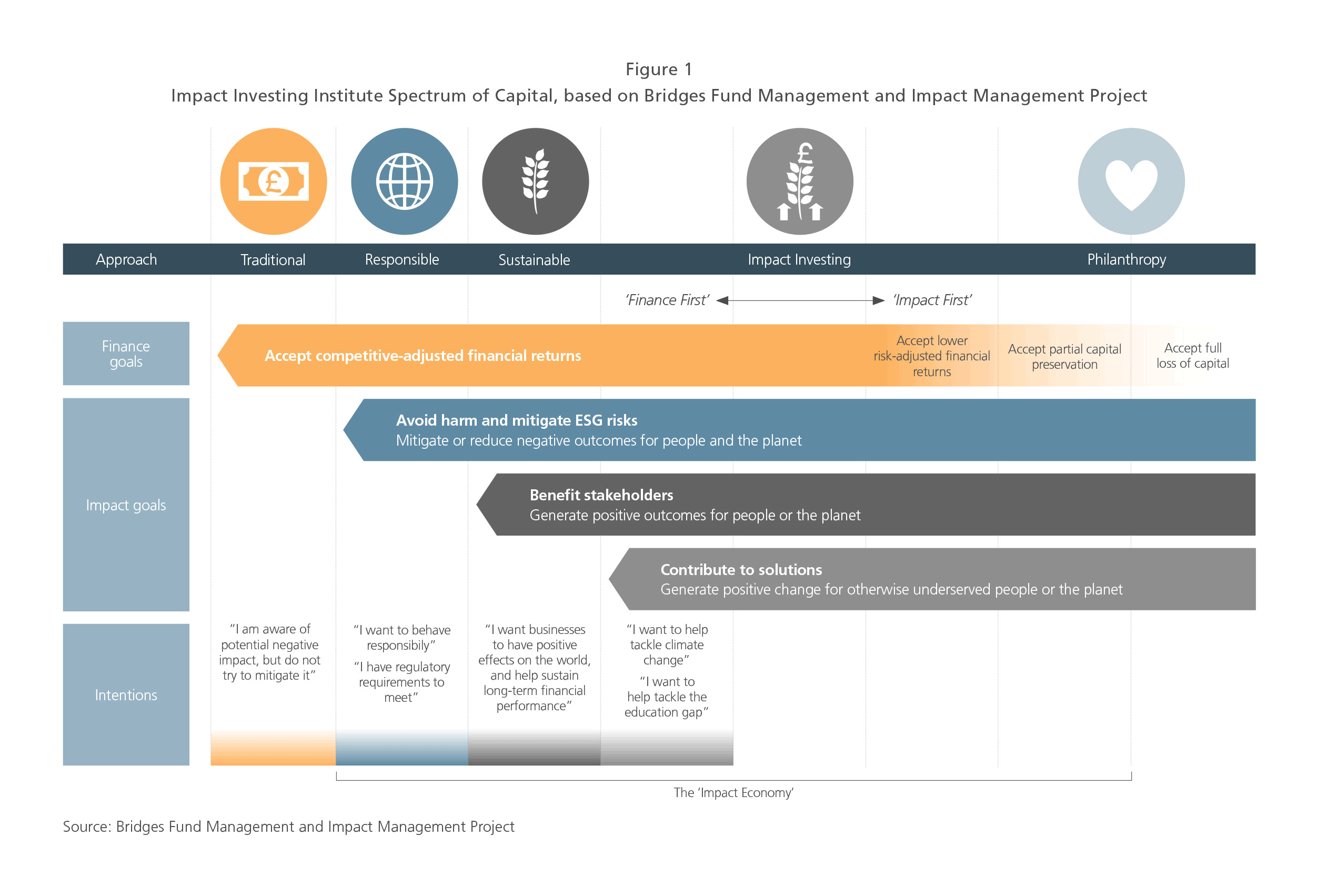

One tool often used to understand the diverse sustainability investing landscape is the Spectrum of Capital (Figure 1, below). This maps different styles of investing based on their purpose or intended outcome. ‘Traditional’ funds focus on risk-adjusted financial returns; ‘responsible’ funds seek to reduce harm; ‘sustainable’ funds aim to benefit people and the planet; and ‘impact’ funds try to create positive impact, particularly for underserved people or the planet. Other definitions describe sustainable investing as focusing on the ‘how’ of a business’s operations, while impact investing focuses on the ‘what’ of a business’s products and services.

There is still a wide diversity of fund types within these categories, and new types of funds are emerging that do not always fit neatly within these labels. Therefore, as well as segmenting by these purpose labels, we suggest also analysing funds by investment approach: how do they actually make investment decisions based on sustainability? We have developed the following framework to lay out these different investment strategies.

Sustainability investment strategy framework

Exclusionary criteria

These are funds that use negative screening to avoid ‘objectionable’ sectors, such as ‘sin stocks’ (e.g. tobacco, alcohol, gambling) or questionable labour practices. This is the most common type of sustainable investing strategy allocated by institutional investors and probably represents the majority of PE firms today. The rationale for ESG integration is often viewed from a risk-management perspective: potentially damaging products or practices may face growing pressure from regulators and customers, limiting the company’s growth potential.

Thematic investing

Thematic investing selects sectors that are actively making a positive social and/or environmental impact. Examples could be renewable energy funds, emerging markets PE funds, or other types of impact funds that focus on one or more of the EU’s 15 Sustainable Development Goals (SDGs). These funds follow a ‘profit with purpose’ or ‘lockstep’ approach, in which the company’s products and services are inherently sustainable or impactful — therefore, increasing positive impact goes hand in hand with growing the company and increasing profits.

Company-specific assessment criteria

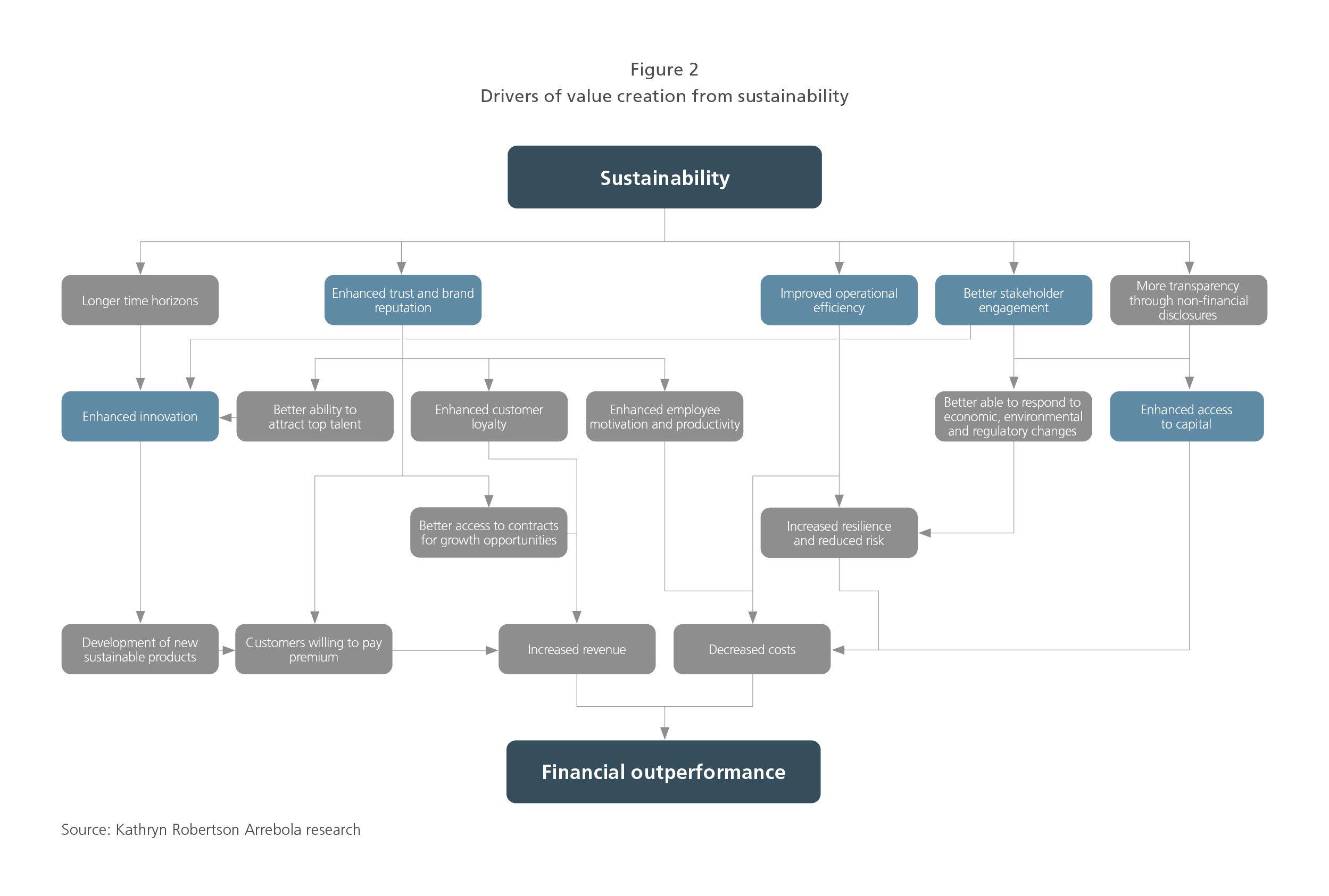

These are funds that use positive screening to seek out companies that have best-in-class sustainability credentials but are not necessarily in purely sustainable sectors. The rationale for this approach is a growing body of evidence that associates good sustainability performance with strong financial returns. The business case for sustainability has been made in detail elsewhere, but we summarise the main value drivers in Figure 2, below. Some PE firms have created a competitive advantage around strong sustainability selection criteria and management, including firms such as EQT, Palatine and Permira.

Improvement potential

Finally, we are seeing the emergence of funds focused on the sustainability improvement potential of investments. PE companies have long been involved in helping to improve sustainability performance through ESG engagement and stewardship, and traditional impact investors have frequently focused on ‘additionality’: producing or helping to produce positive social or environmental outcomes that would not have otherwise occurred or would have been smaller without the investment.

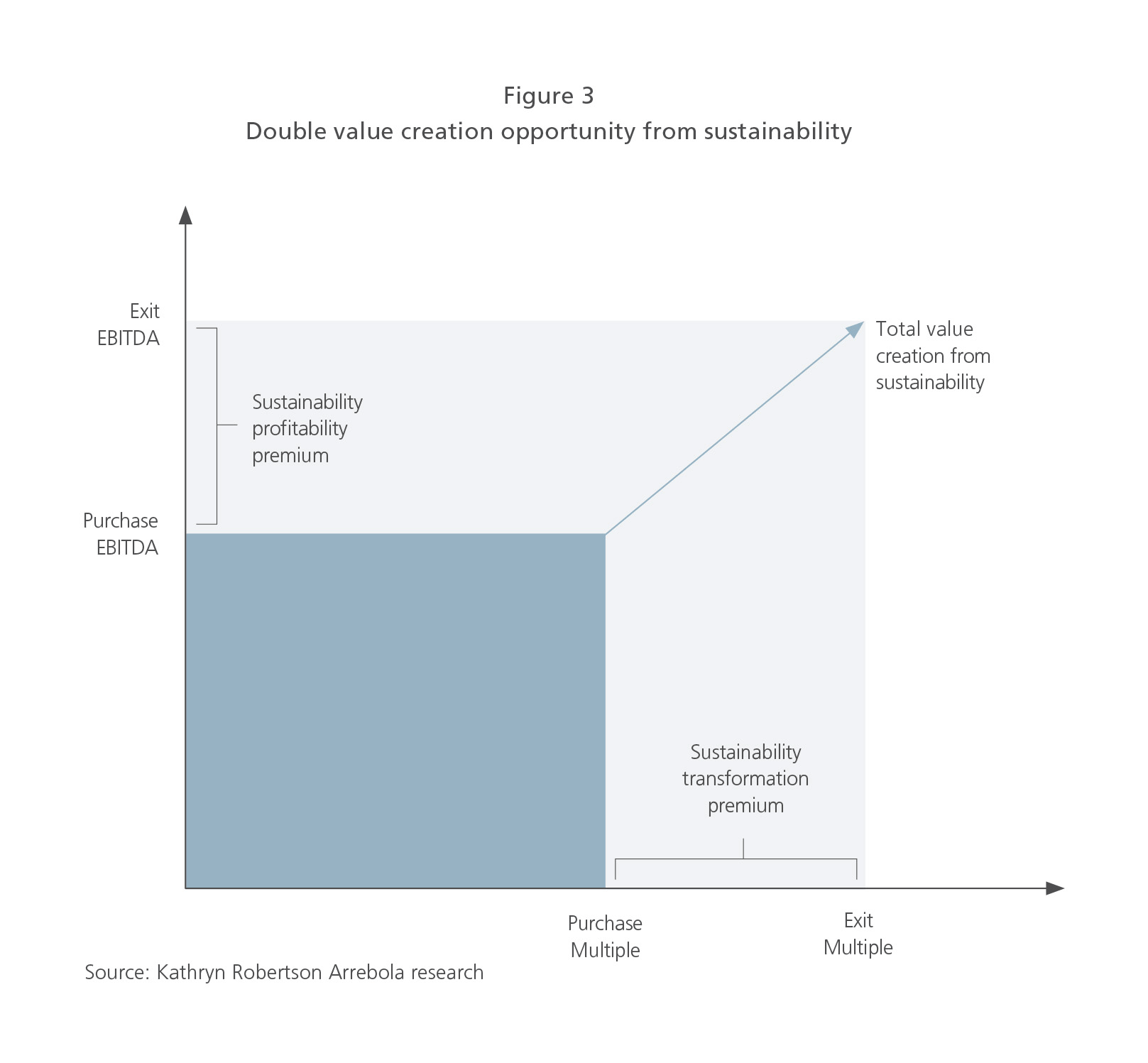

However, we are now seeing improvement potential (or additionality) become increasingly central to the core strategy of PE funds. One example is Brookfield’s Global Transition Fund, which targets investments that will “accelerate the world’s transition to a net-zero carbon economy”. The business case for these ‘sustainability transformation’ funds is compelling: improving a company’s sustainability could not only improve financial returns, as shown in Figure 2, above, but also enhance the transaction multiple at exit, given an ‘ESG premium’ — particularly if the purchase multiple is lower given an initially ‘unattractive’ carbon-intensive business. Figure 3 sketches this double opportunity for value creation from sustainability transformation.

Future developments

As the sustainability investing landscape grows and new types of funds emerge, we expect several trends to shape the industry going forward.

- Sustainable investing could become the norm. Given increasing investor demand for sustainable funds, it could be difficult for new funds to raise money without regard for ESG considerations. In addition, funds with more rigorous sustainability approaches (for example, positive screening or improvement potential compared to basic exclusionary criteria) could have a competitive advantage.

- Impact funds could replace sustainability. There is growing investor attention on the ‘what’ of a business’s products and services as well as the ‘how’ of its operations. Similarly, industry-leading funds are getting better at defining and communicating their own impact in terms of the environmental and social value created or increased specifically by their investment.

- Reporting requirements will become stricter. We have already seen the entrance of the EU’s Sustainable Finance Disclosure Regulation (SFDR) defining different categories of ESG investing, each with different disclosure requirements. Article 8 refers to funds that promote environmental and/or social characteristics and good governance, while Article 9 funds focus on economic activities that have a central sustainable investment objective. Although there will still be a wide variety of the types of funds captured by these categories, it is clear that more transparency and reporting will be required to back up sustainability claims.

- Measurement systems could become more rigorous and financially integrated. We are seeing the emergence of new types of ESG and impact measurement and reporting systems, with some pioneering initiatives aiming to create holistic, financially integrated metrics. An example is Harvard’s Impact-Weighted Accounts project, which helps companies understand the financial costs of environmental and social damage. Tools like this could help fund managers better evaluate the sustainability performance of portfolio companies, and communicate results to limited partnerships.

What to do

As investors review their approach to ESG, at a minimum they should be considering the following questions to help frame a robust strategy:

- What is your company’s level of ambition? Do you want to be a sustainability leader or take a compliance approach?

- If there is a need or desire to incorporate sustainability more effectively into your investment approach, what strategies are available to you?

- How do these different approaches align with your overall investment strategy, and therefore, what is the most suitable approach to take?

- How will you embed sustainability into your organisation? What additional capabilities do you need?

- Should you consider new opportunities, e.g. new sustainability transformation funds?

Importantly, an understanding of these approaches isn’t just needed for investors. For corporates responding to investor pressure (amongst other stakeholder demands), it is important to consider the strategies of key investors and implications for positioning to align with the different strategies we observe.

Endnotes

1In this article, we will refer to ‘sustainability’ and ‘ESG’ (environmental, social and governance) interchangeably.

01272022090113