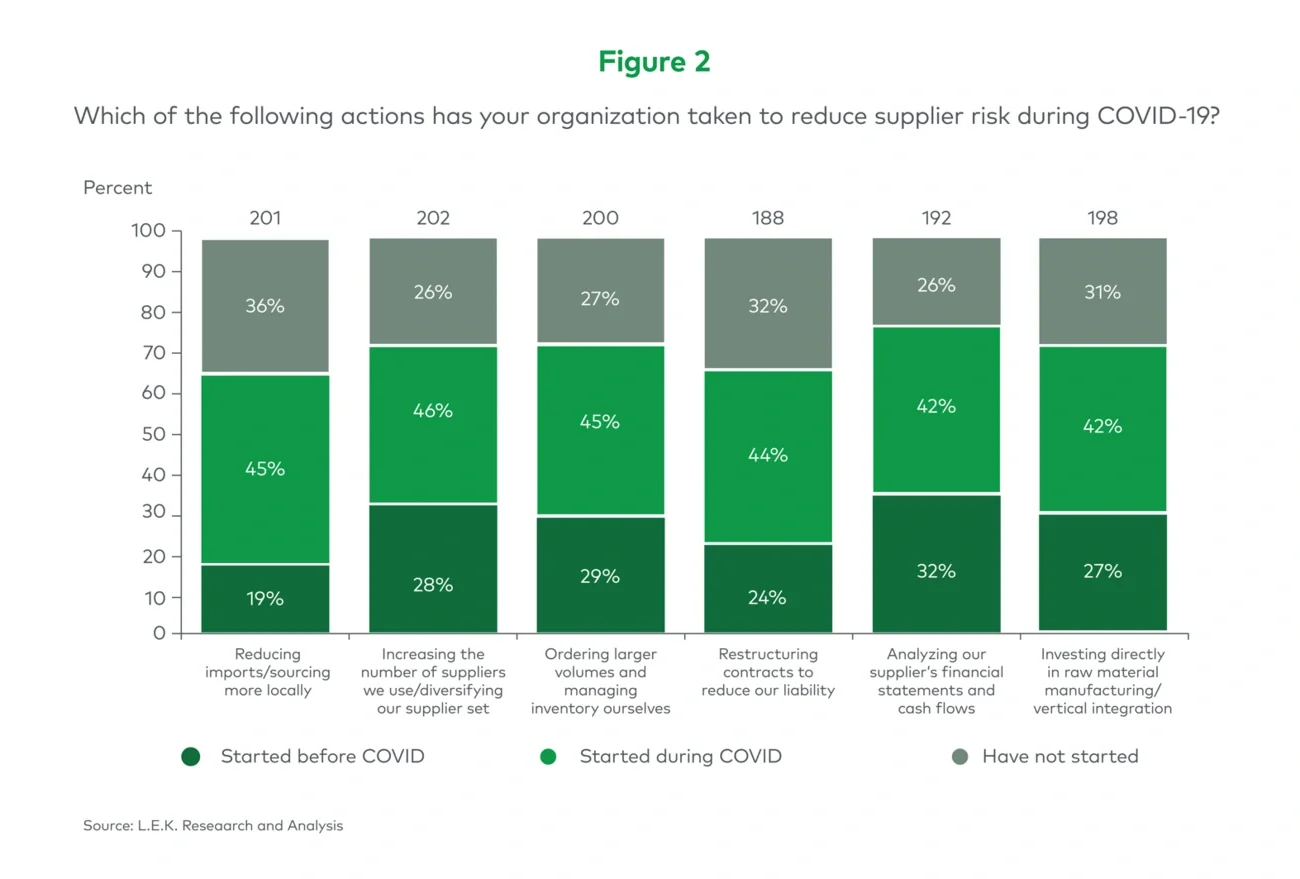

We are not the first to note the profound impact that COVID-19 has had on global supply chains. More recently, the Russian invasion of Ukraine has further tested and weakened this global network and placed even greater emphasis on the requirement for supply chain resilience. But resilience comes at a cost, and whilst ‘just in case’ may currently be preferred over ‘just in time’, the pressures to optimize use of cash and working capital have not gone away. With its exposure to global supply chains, the European specialty chemicals sector is one such industry that has been materially affected by these emerging challenges and conflicting pressures.

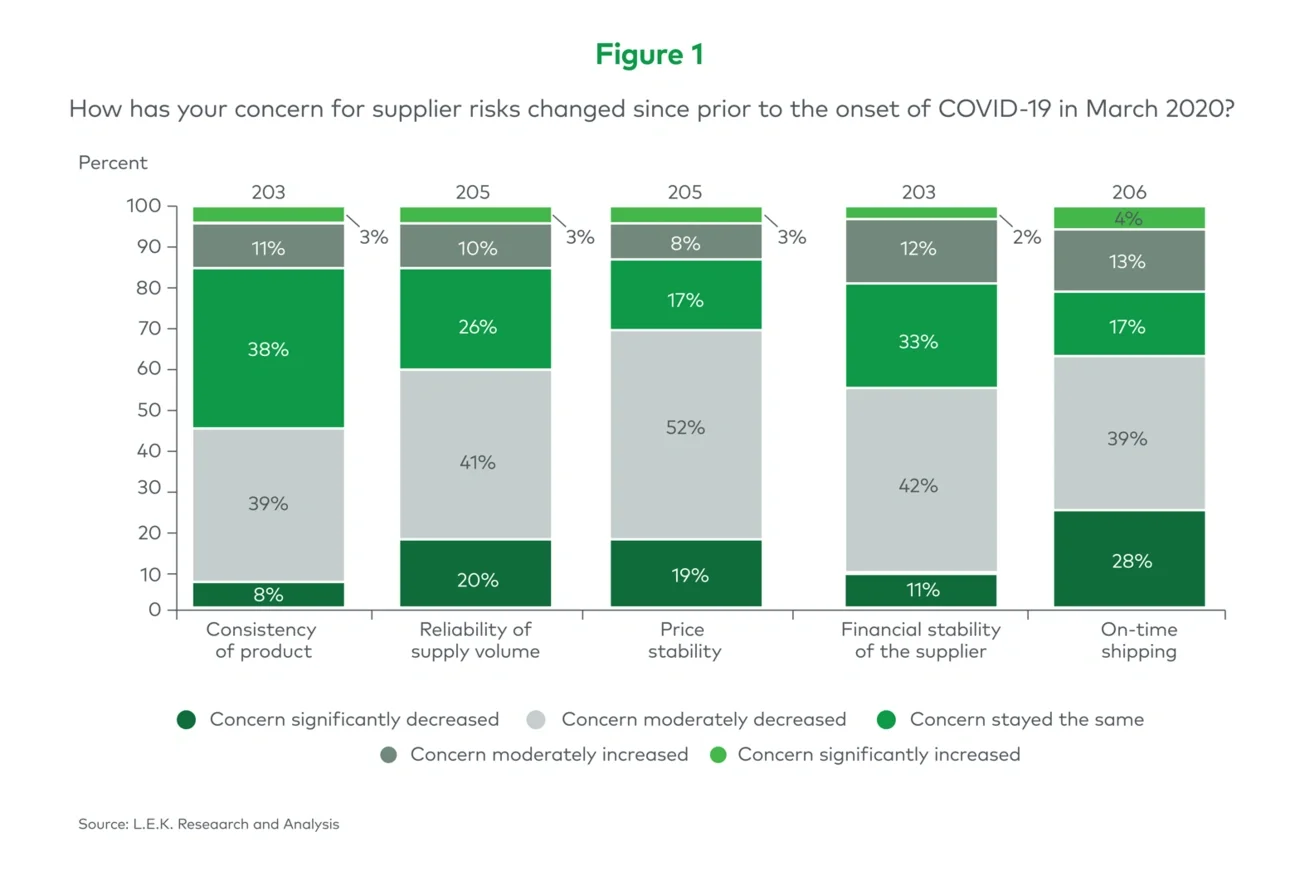

Our 2021/22 European Specialty Chemicals Survey identifies that price stability of raw materials, reliability of supply volume and on-time performance remain the chief supply chain-related concerns within the sector. Further, players are significantly stepping up efforts to increase security of materials by diversifying supply chains and are seeking to take less risk in pricing through their commercial contracting.

These are among the key findings of L.E.K. Consulting’s 2021/22 European Specialty Chemicals Study, a survey of 207 chemical sector professionals across a broad range of industries and functions. Our survey included leaders and senior decision-makers in France, Germany, Italy, Spain and the United Kingdom.

Read on to hear more about what they told us.

Price stability and reliability of supply are the chief supply chain concerns for the specialty chemicals sector

When asked to relay how their sentiment had changed in the past 18 months with respect to five specific supply chain areas, across all regions our panel reported significant increases in their level of concern: in particular, on-time shipping, reliability in supply volumes and the pricing stability of raw materials (see Figure 1):

-

Respondents from the United Kingdom reported the greatest increases in concern in reliability of supply volumes, perhaps because of the combined supply chain challenges associated with COVID-19 and Brexit

-

Conversely, across each of France, Italy, Germany and Spain, the number one area of increased concern was pricing stability