EU's Green Deal sets out a bold ambition and proposes supportive revisions to three key policy directives

On 14 July 2021, as part of the European Green Deal, the EU announced a broad new package of policy proposals which aim to accelerate decarbonisation of the aviation sector and if fully implemented will have a significant impact on the EU aviation sector. This package of initiatives, however, will undoubtedly increase the costs for industry participants and passengers, but will they achieve their objectives?

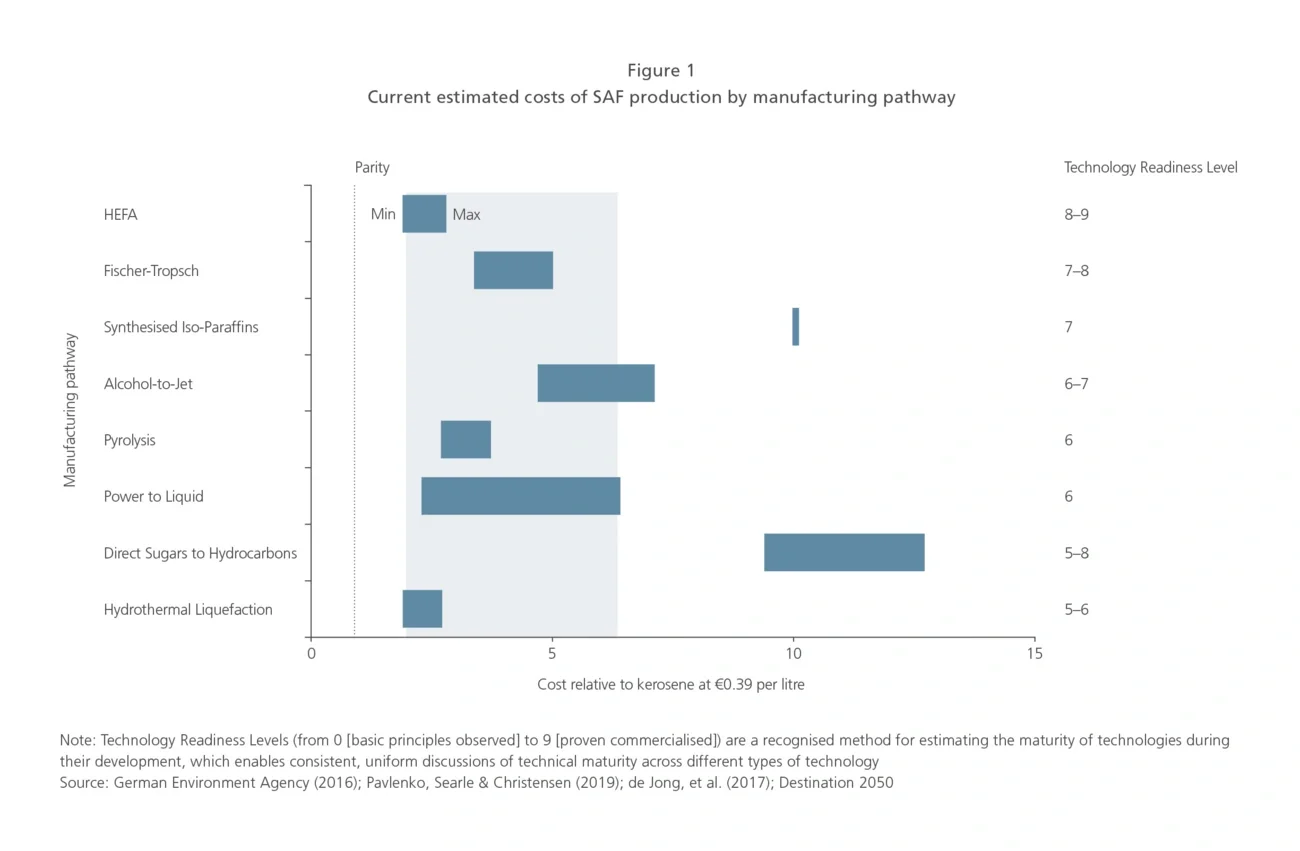

The new ReFuelEU Aviation Initiative mandates blending of sustainable aviation fuel (SAF) with fossil fuels at 5% by 2030, 32% by 2040 and 63% by 2050. The initiative applies to all fuel suppliers providing fuel at EU airports, and all airlines, whether EU or foreign, must annually uplift from each EU airport 90% of the fuel required for flights from those airports (to try to minimise unnecessary tankering). Currently approved processes specify a maximum blending ratio of 50%, but Rolls-Royce has announced plans to make all its civil engines compatible to run on 100% SAF, with tests under way.

The revisions to the Emissions Trading System (ETS) will see fewer free allowances for aviation, further reduction over time and increased auctioning, reflecting the EU’s desired ‘polluter pays’ policy, which will undoubtedly make fossil fuel offsetting harder and more expensive.

The revisions to the Energy Tax Directive will initiate a tax on aviation kerosene and align its rate to motor fuel as well as differentiating between first-generation biofuels (c. 50% of the proposed kerosene tax level) with advanced biofuels including synthetic liquid fuels (c. 1.5% of the proposed kerosene tax level).