The advanced air mobility (AAM) industry is rapidly taking shape around the world. AAM is on the cusp of commercialisation, with multiple electric vertical take-off and landing (eVTOL) aircraft manufacturers and operators competing to be the first to launch. There are over 200 aircraft designs in development and various business models. Many are in the design testing phase, with more than 30 companies engaging in certification with the US Federal Aviation Administration (FAA), and several in the process of certification with EASA (European Union Aviation Safety Agency).

Executive Insights

Advanced Air Mobility — Cost Economics and Potential

Advanced Air Mobility — Cost Economics and Potential

February 17, 2021

Key Takeaways

AAM has a number of possible applications, including medical transport, non-passenger recreation and infrastructure inspection.

Over time, the AAM industry could be worth several billions of dollars for a country like Australia, although it could take up to 8 to 10 years to deliver positive cash flows.

Demand for AAM will be highly correlated to price, and pricing will likely differ across regional and urban routes.

Commercialisation efforts are backed by material investments in the industry. Earlier this year, Toyota led a USD 394 million investment in Joby, Volocopter attracted a USD 113 million investment and China-based EHang’s IPO valuation was USD 650 million. The first commercial passenger flight is likely to launch within the next three to five years with piloted aircraft, before transitioning to remote piloted operations.

AAM has the potential to revolutionise urban and regional transport through reduced travel times and improved mobility options. In addition, the industry can be scaled with relatively small amounts of capital compared to other more asset-intensive transport alternatives such as road and general aviation.

The commercial returns of AAM can be very attractive, especially at scale and under a remote piloted scenario. This Executive Insights explores the commercial attractiveness of AAM, how the industry might scale and the triggers to profitability.

Figure 1

AAM potential market

Image

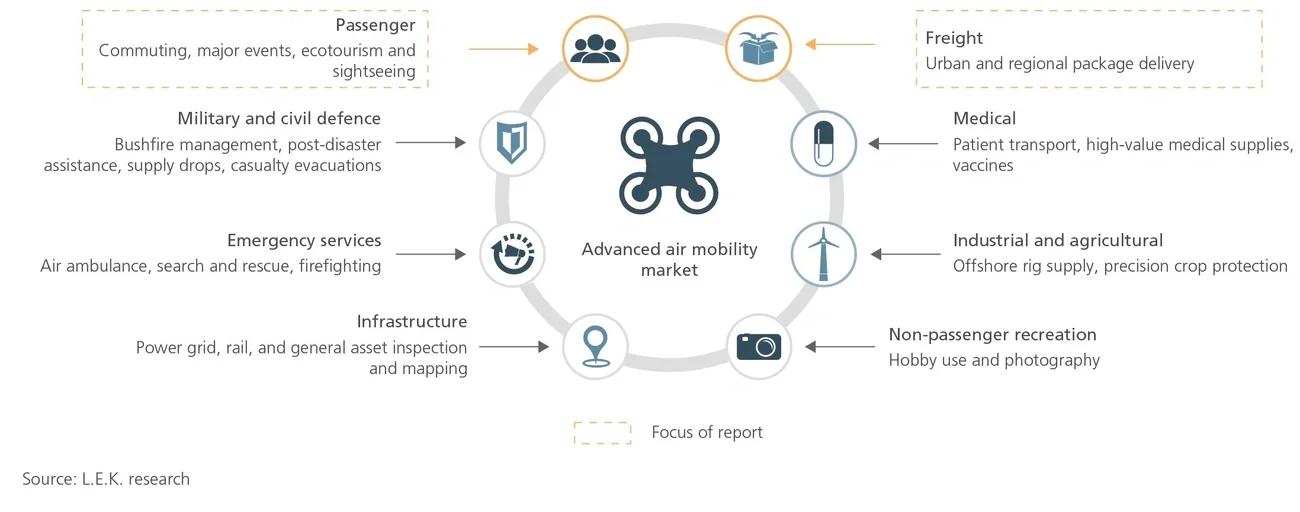

The possible applications for AAM via eVTOL aircraft are far reaching. The two biggest markets are passenger travel, for commuting, tourism, major events and sightseeing; and freight transport, for urban and regional package delivery (see Figure 1).

But there are a variety of other beneficial use cases: medical transport for both patients and critical supplies; offshore rig supply and agricultural crop protection; non-passenger recreation such as hobby use and for photography; infrastructure inspection and mapping for power grid, rail and other assets; emergency services use for search and rescue and firefighting; and military and civil defence applications such as bushfire management and post-disaster assistance.

This report focuses passengers and freight market segments.

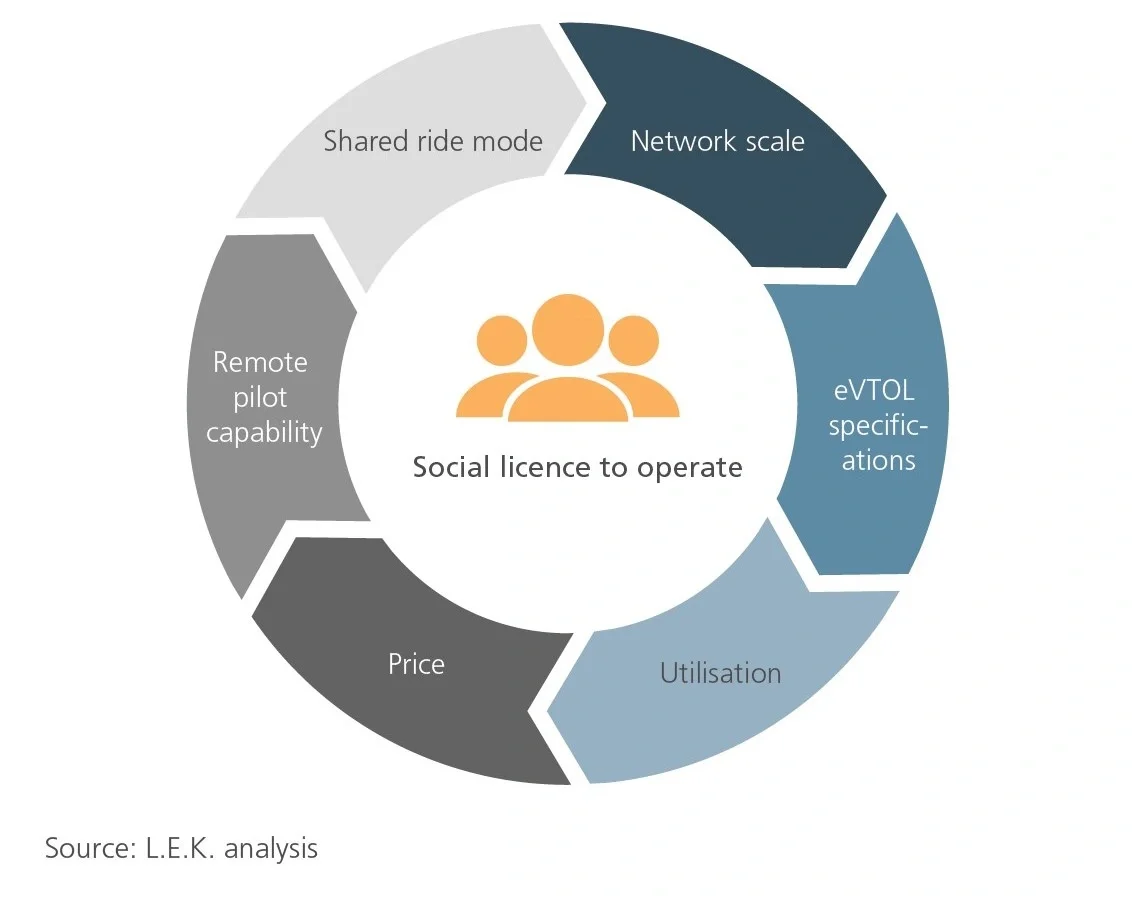

L.E.K. Consulting research suggests that there are seven key drivers that contribute to commercial attractiveness in the AAM market, each of which is complementary to and reinforces the others (see Figure 2).

Figure 2

Drivers of commercial attractiveness

Image

Network scale — As with many industries, the economics of AAM flight improve considerably with scale. Fixed overhead costs can be amortised across a larger transport task. Specifically, for AAM operations, as the number of nodes in the network grows, the number of potential operating routes grows non-linearly to accommodate scaled demand. Initially, when the network has a few vertiports (eVTOL take off and landing sites), there is a low share of trips that can be completed using one of the available routes; however, as nodes are added, connectivity improves. Even if nodes added later have relatively low traffic, there is significant benefit from the connection to existing nodes as well as associated network effects.

eVTOL specifications — As the industry matures, the cost of eVTOL aircraft is expected to reduce in nominal terms by c.15% in five years. Scale will also drive eVTOL aircraft production and construction efficiencies. In addition, the aircraft are likely to become capable of carrying more passengers. In a shared operating model, this dramatically improves the potential revenue per flight kilometre (km).

Utilisation — The term refers to the extent of flying time for eVTOL aircraft vs time spent charging, reloading passengers or going unused. For eVTOL operators building scale on a particular route, higher utilisation may deliver greater returns than building out the network to gain overall network connectivity benefits.

Price — At industry inception the cost to travel by eVTOL aircraft in urban areas is likely to be greater than USD 2.50/km. In context, this is about double a traditional taxi journey. This cost is expected to fall dramatically. With high levels of utilisation, remote pilot capability and increased capacity per aircraft, the economics improve dramatically, allowing the cost of eVTOL travel to eventually reach parity with today’s taxi prices.

Remote pilot capability — As the industry matures, analysts expect that will move towards remote piloting and eventually fully autonomous operations. This will increase the capacity of the aircraft itself by freeing up the seat taken by a pilot, and will reduce the cost to operate, as remote piloting will require less labour. The dual effects of this will significantly improve the profitability per flight kilometre.

Shared ride mode — A shared ride mode, which charges on a per passenger basis, is the ultimate goal for AAM operations, and will allow the most flexibility as the industry grows. It allows for more efficient utilisation of the assets and offers a step change in profitability.

Social licence to operate — Social licence is the acceptance granted to an organisation (or industry) by the community and is closely linked to meeting expectations and gaining community trust. It is achieved when the community trusts that the organisation or industry will act in line with its interests, beyond what is required by regulatory or legal obligations. Gaining the social licence to operate is critical to the successful launch and expansion of the AAM industry. However, no single party is responsible for achieving this. It requires the collaboration of multiple parties — federal government, council bodies, regulators, proponents and participants in the broader AAM ecosystem.

The commercial returns of the AAM industry are expected to improve significantly over time. L.E.K. forecasts that the AAM industry could be worth several billions of dollars for a country like Australia. However, it could take up to 8 to 10 years to deliver positive cash flows. The timing depends on the scale of investment, rate of market development and use cases.

To better understand the commercial attractiveness of the AAM industry, it is important to assess the dynamics of both supply and demand — which in the AAM industry are inextricably linked. Demand for AAM is expected to be highly correlated to the cost of the service. The success of the industry depends on its ability to reduce the cost of supply, making it more competitive (relative to alternative modes) with the public as a mode of transport and more attractive to the freight industry.

The following estimates are generalised costs across the whole of market deployment and are intended to represent a blend across the industry. Commercial attractiveness will vary depending on the extent to which key drivers of profitability can be enabled.

Supply

eVTOL capex and opex

Market estimates for eVTOL aircraft vary significantly by manufacturer and design. Generally, as the size of the aircraft increases, the cost increases. In the early years of development, smaller eVTOL aircraft seating two passengers could cost under USD 1.5 million, but a five-seater could cost more than USD 4 million. This price includes batteries, flight systems, rotors and associated technology, and is expected to decrease materially as production volume scales. Currently, the useful life of an eVTOL aircraft is estimated to be eight years. This varies by market participant but is expected to increase over time.

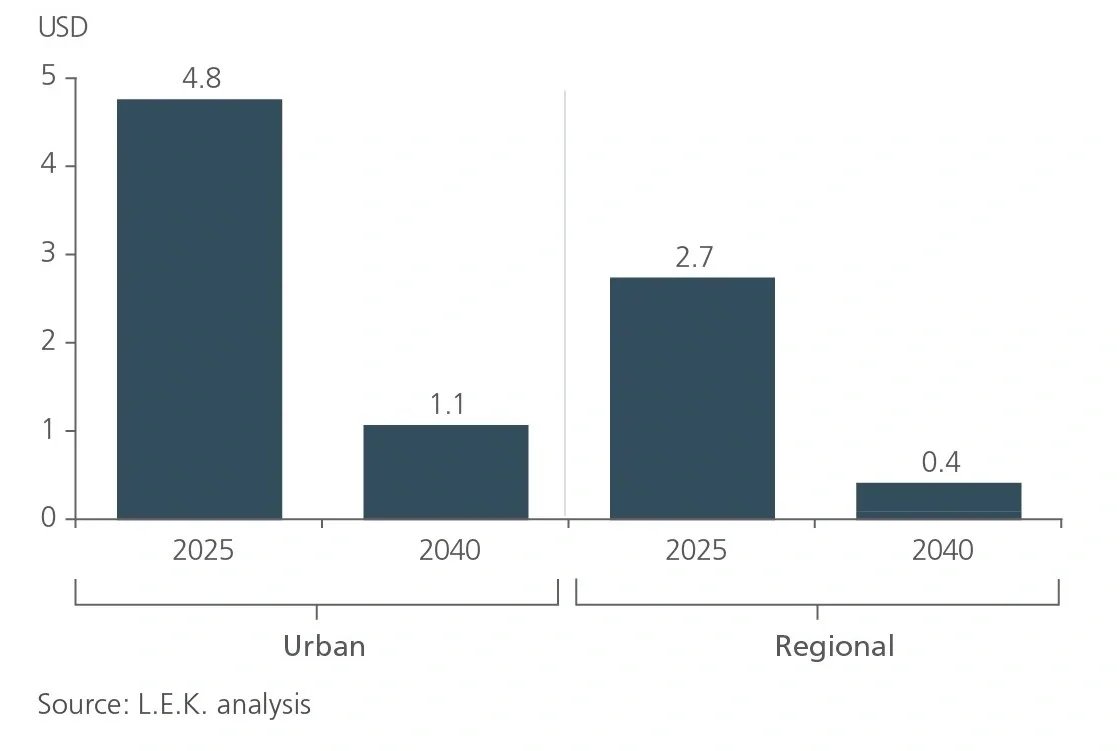

We estimate eVTOL costs per passenger kilometre to decrease by more than two-thirds between 2025 and 2040 (see Figure 3). Major cost components are pilot salaries and energy costs of recharging eVTOL batteries, as well as maintenance, repair and overhaul jobs to maintain aircraft airworthiness. The cost of operations on a per-kilometre basis are lower for regional services due to a much higher assumed average distance per flight.

Initial industry profitability in the early 2020s is depressed by the higher cost of pilot-flown operations. We expect that there will be a step change in price once remotely piloted operations commence. Profitability improves due to significantly reduced pilot and avionics costs and availability of an additional seat, increasing revenue in a per-passenger charging model. A further step change is expected when fully autonomous services commence.

Figure 3

eVTOL and veriport costs per km

Image

Vertiport capital and operating costs

Vertiports are key pieces of infrastructure for AAM operations. They are designated ‘hubs’ for eVTOL aircraft, acting as terminals where passengers board and disembark and freight is loaded and unloaded, akin to airports for traditional aviation.

There are a wide variety of proposed vertiport designs with different levels of sophistication, supporting facilities and total capacity — from a basic take-off or landing pad through to a multilevel terminal with extensive support facilities such as hangar areas and gates, waiting lounges, and maintenance and repair services.

Vertiports could be built by repurposing existing infrastructure such as helipads, retrofitting high-rise buildings, or developing new structures on underutilised land or on rooftops. Alternatively, they can be integrated with existing ground transport through multimodal mobility stations and built on or near a train station or bus interchange.

Similar to eVTOL aircraft, capital costs for vertiports differ significantly by design. Vertiport construction costs will vary depending on the specific site and foundational structure; ground-based vertiports are likely to have lower costs than those built above ground on existing infrastructure.

Ideal locations for the early vertiports are likely to be in built-up areas, connected to existing transport hubs (airports, train stations, etc.), meaning the industry should plan for high initial costs. Given this, our model assumes the cost of vertiports could be between c. USD 3.5 million and 12 million for a leading global city, depending on size, purpose, location, access to energy supply and construction method. Notably, there are novel modular approaches that could materially reduce construction costs.

Additional costs may also be incurred depending on electricity grid capacity at the particular location, or in particularly complex locations where traffic disruption needs to be considered.

Lastly, market entrants in the AAM industry will need to comply with existing air space, noise, safety and security regulations. There will be an associated cost to integrate and optimise the industry. In the early years of inception, it is likely that AAM will be integrated into the existing airspace construct.

For many cities, including Melbourne, Class C controlled airspace around major airports extends into the central business district, meaning some level of air traffic control is required. Whilst not expected to detract from the investment case, these costs need to be factored into any commercial assessment.

Demand

Demand for AAM will be highly correlated to price, as discussed above, and the amenity delivered by the network. In the short term, it will be important for operators to choose the most attractive use cases and build up utilisation on early routes before expanding the network. In a rational market, we expect that operations will gradually add vertiports/routes once a certain level of utilisation is achieved on the primary routes. As the number of vertiports in the network grows, the number of potential operating routes grows non-linearly to accommodate scaled demand. As vertiports are added, connectivity improves exponentially, and demand grows.

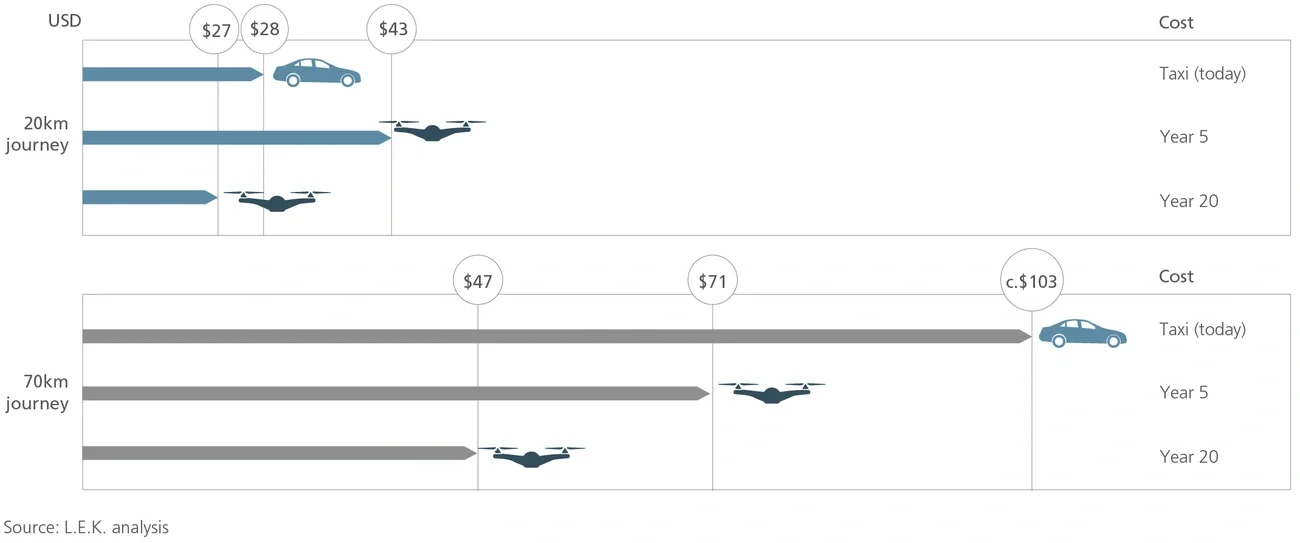

The price of AAM will reduce over time. Approximating taxi prices in the long run is very achievable (see Figure 4). In the short term we expect AAM to displace the helicopter and light general aviation market, at the end of their useful life (where appropriate take-off/landing infrastructure can be constructed), and to supplement routes that are impacted by congestion, have poor travel time reliability and/or lack cost-competitive transport alternatives. Longer term, as the price decreases, it will replace some taxi and ride-share services for addressable journeys. The extent of displacement will depend on the time frame in which autonomous taxi/ride share becomes a reality.

Figure 4

Example passenger prices

Image

Pricing is likely to differ across regional and urban routes, to reflect the difference in operating costs.

AAM is unlikely to replace mass surface-based public transport. Rather, it enhances the transport ecosystem, offering fast point-to-point connections where existing surface-based options are congested, circuitous or do not exist. In addition, there will be demand for AAM across a variety of other use cases including emergency services, search and rescue, and patient transport.

AAM is expected to be an attractive method of transport for express package delivery. Our analysis assumes that AAM could eventually capture around 30% of the express post/same-day delivery market. Exact market share will depend on the configuration of distribution networks and the comparable cost of road-based delivery mechanisms. Greater uptake can be expected where low-cost last-mile connection options can interface easily and cost-effectively with eVTOL deliveries.

AAM has the potential to be a city-shaping technology — delivering the benefits of travel time savings and increased regional connectivity and mobility, and accelerating the decarbonisation of transport systems.

The drivers of commercial attractiveness are mutually reinforcing. When the drivers are aligned, AAM has the potential to be highly profitable. As the network and eVTOL production scale, the cost of both operations and manufacture will decrease significantly. Improved range, along with a scaled network, will also improve the utilisation of the eVTOL aircraft. This will ultimately deliver lower passenger prices, which will increase demand and have a reinforcing impact on the ability of the network to scale. The introduction of remote pilot capability will also increase the capacity of the aircraft and decrease the operating cost, driving up profitability, particularly under a shared ride mode.

Whilst AAM is commercially attractive, there are still some risks which need to be mitigated if the industry is going to scale. Social licence surrounding safety, noise, visual amenity, privacy, affordability and accessibility may well prove to be the biggest factor in determining the success of this industry. Battery technology for long-range flights is also a significant limiting factor for scaled operations, as is airspace integration of eVTOL and traditional aircraft.

Along with these hurdles, certification processes for remote and autonomous eVTOL aircraft are less advanced and will have to be determined in the coming years. Infrastructure requirements are also a key component in the AAM ecosystem, and consensus around standards for vertiport design, operation and construction must be progressed. These are the most immediate challenges facing the development of the AAM market. If these issues can be addressed in a collaborative, efficient manner, there is a clear path forward to the commercialisation of AAM.

Related insights

You might also be interested in these insights.

English