Key takeaways

-

The Brazilian government can’t afford the necessary investment to improve its water and sewage infrastructure for the estimated 83% of the population that is without treated water and the 50% without sewage collection.

-

Private operators are aiming for greater growth in the sector and investors are seeking opportunities — however, the pace of change is still slow.

-

Brazil can unlock the potential for improving its water and sewage infrastructure through four strategies.

-

Overcome barriers for working with private operators

-

Introduce a disruptive business model that brings together the public and private sectors

-

Design a mechanism for developing unbiased feasibility studies for use during the bidding process

-

Apply societal pressure

-

The Brazilian government cannot afford the necessary investment, so private operators are aiming for greater growth in the sector and investors are seeking opportunities — however, the pace of change is still slow. How can Brazil unlock the potential for improvement?

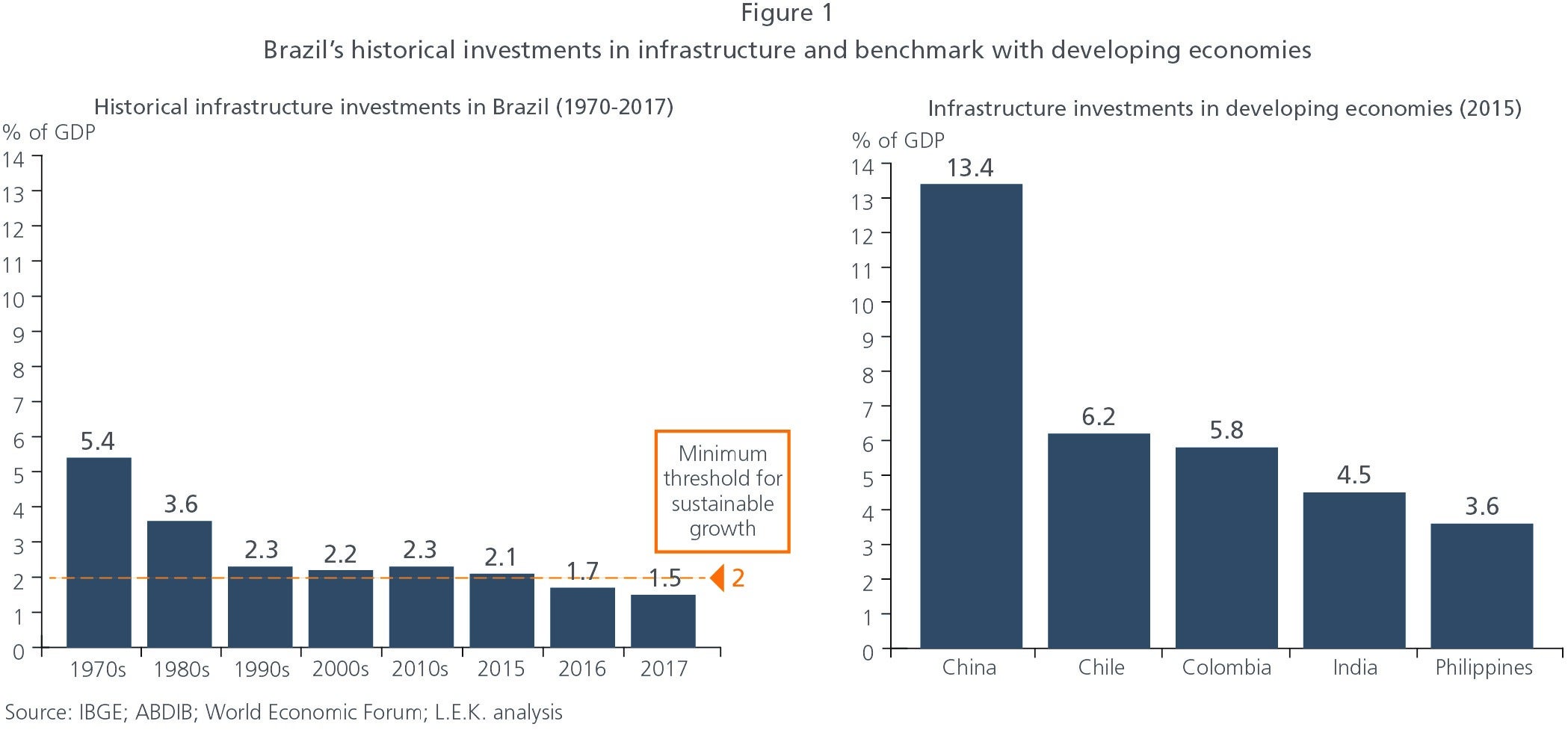

Over recent decades, Brazil has reduced its level of investment in the country’s overall infrastructure below the annual threshold of 2%, which is considered the minimum for sustaining healthy economic growth. The situation was made worse by the recession of 2015- 2016, which saw Brazil’s level of investment in infrastructure fall below that of other developing economies (see Figure 1).

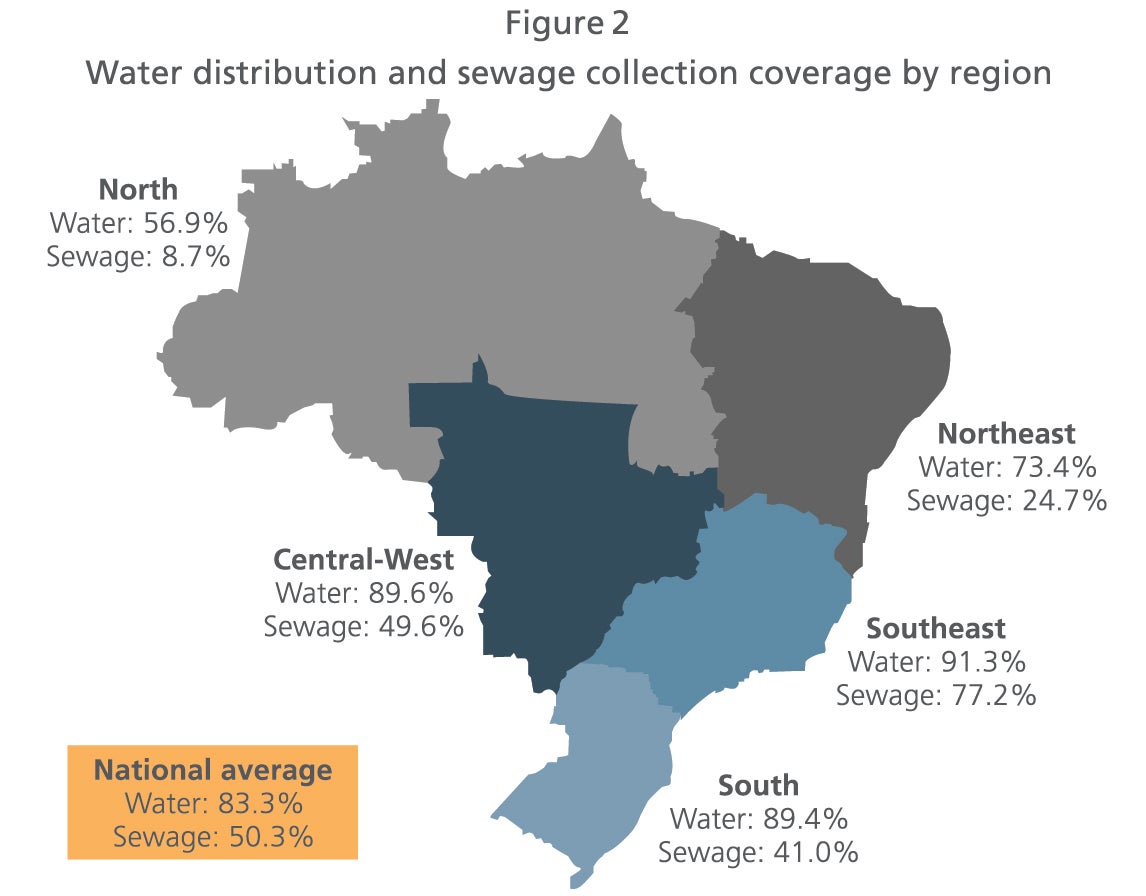

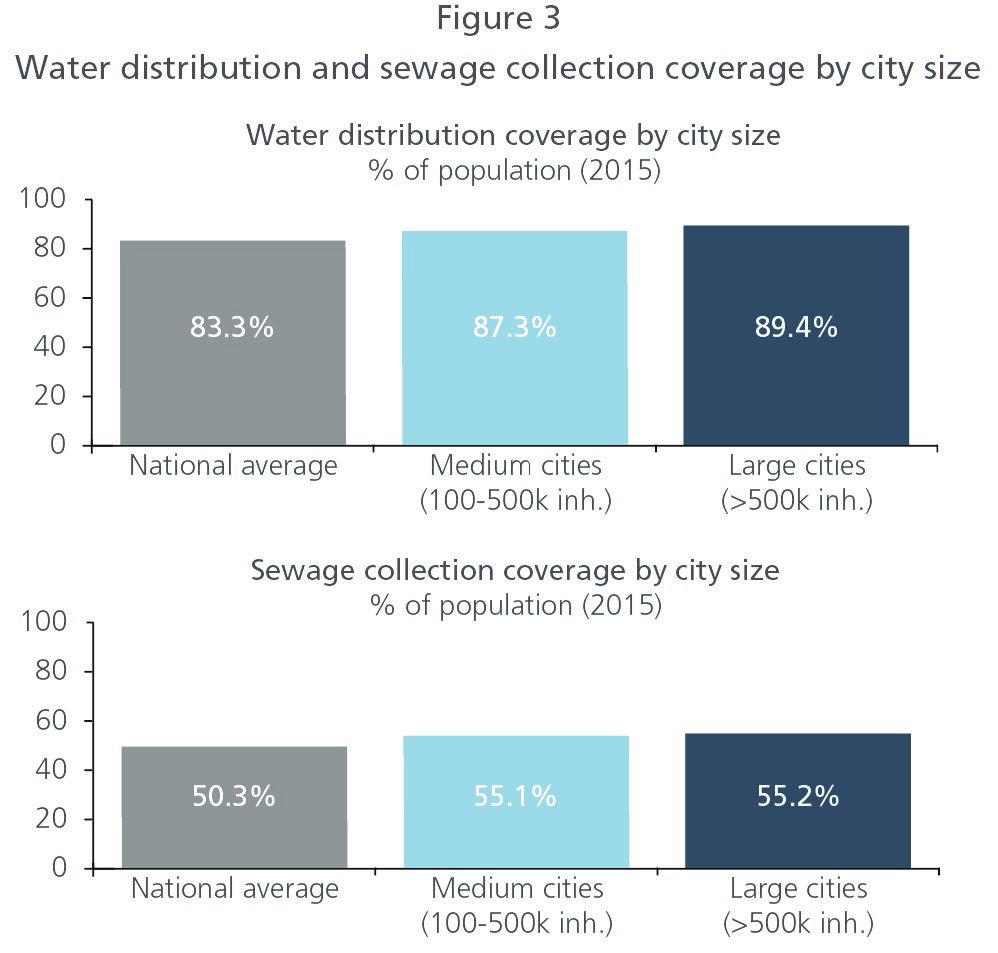

The sanitation sector accounts for less than 10% of investment in infrastructure in Brazil. Despite the central government’s ambition to provide universal sanitation in 2015, only 83.3% of the population had access to treated water; sewage collection was even lower, reaching only 50.3% of the population (see Figure 2). Contrary to popular belief that the problem is due to Brazil’s geographic size and low population density, provision in midsize cities is not far off the national average (see Figure 3), demonstrating that the gap is systemic rather than concentrated. In order to bring water distribution coverage to 99% of the population and sewage collection to 90%, the National Sanitation Plan designed in 2014 estimates around R$300 billion in investments is required.

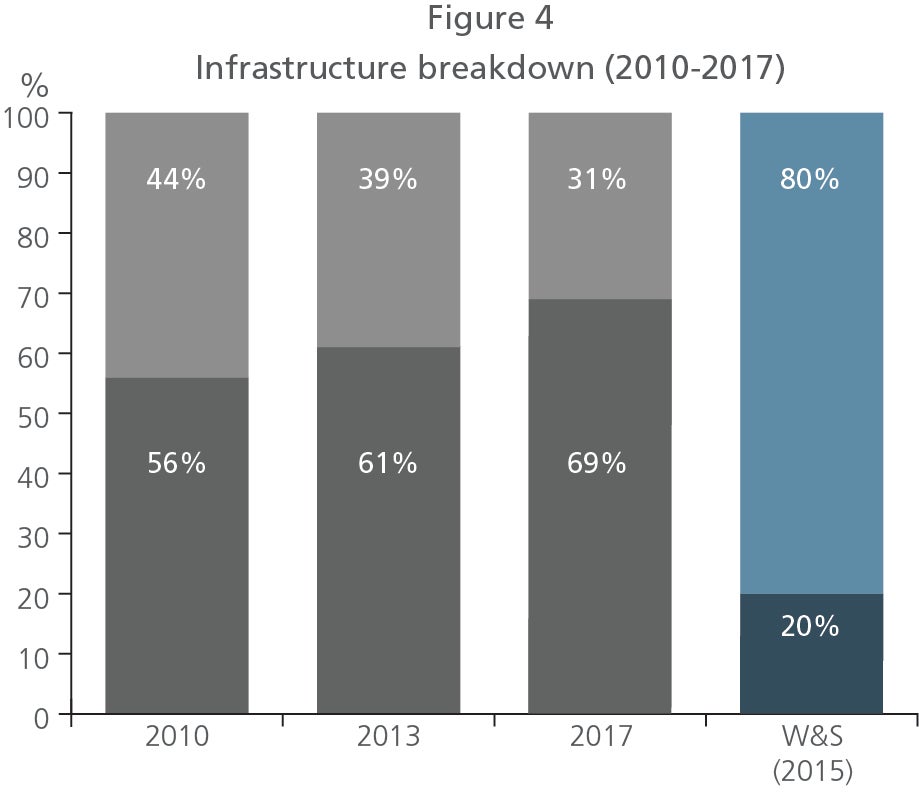

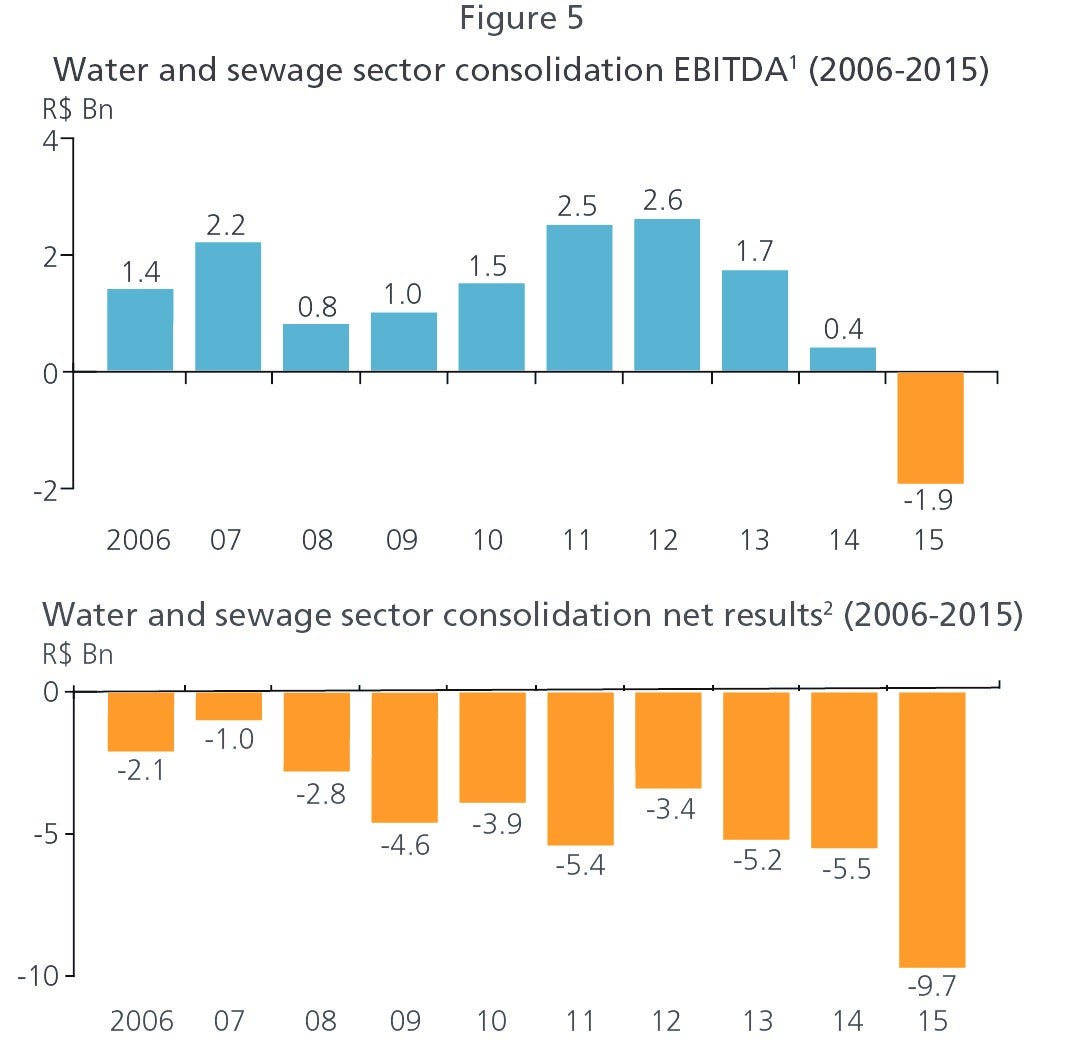

Within the water and sewage sector, the government has led more than 80% of the infrastructure investment, compared with only 31% in overall infrastructure investments (see Figure 4), with consistent financial inefficiency and construction delays over the years. Over the past 10 years, the sector has shown a financial loss, dampening enthusiasm for investment within the public sector (see Figure 5). Furthermore, the current national fiscal deficit, new regulations limiting government expenditure, and slow recovery from recession are jeopardizing the government’s ability to boost investment in the near future.

However, investments in water and sewage are urgently required and may bring important benefits for the entire population.

- According to the World Health Organization (WHO), for each dollar invested in sanitation, $4.3 is saved in health costs.

- Workers in areas with access to sanitation are up to 4% more productive than those without proper facilities.

- Real estate value is up to 13% higher in areas with access to water and sewage systems.

- Tourism loses approximately $3 billion a year due to the lack of sanitation infrastructure and its impact on the environment.

So, what needs to be done to close the sanitation gap in Brazil?

Find ways to overcome barriers for government to work with private operators. Private investment in the Brazilian sanitation sector is still limited to 6% of the market in terms of household coverage. Since the first private concession was established in 1999, the share of private operators in the sector has grown slowly. The main reason behind the modest participation of the private sector is the current regulatory framework, which leaves much of the decision- and rule-making in the hands of each individual city.

The sanitation regulatory milestone, Law 11.445 of 2007, set the main guidelines for the sector and was instrumental in providing the minimal level of confidence required by private investors. However, the technical and economic aspects (such as applicable tariffs) of sanitation operations were not detailed in the regulatory framework. Each city must design its own sanitation plan and define the guidelines for operation, leading to the absence of a national standard that investors can use as a reference. The decision to assign a private player as a provider of sanitation services (via concessions or public–private partnerships, or PPPs) remains the responsibility of each city, creating difficulties for the formation of large private enterprises. In addition, 70% of Brazilian cities are served by one of the 25 state-administered sanitation companies (Companhias Estaduais de Saneamento Básico, or CESBs). The presence of a CESB in a city creates significant political pressure against privatization of services.

Furthermore, most of the largest private operators found themselves embroiled in one of the biggest corruption schemes in recent history, the lavajato scandal, in which the country’s largest infrastructure contractors paid bribes to politicians of different parties to obtain benefits from government contracts. These events drove important movements in the market, such as Odebrecht Ambiental’s acquisition by the Canadian investment firm Brookfield (creating BRK Ambiental) and the restructuring of CAB Ambiental into Iguá Saneamento. These “new” players, together with others that once were second-tier (such as AEGEA Saneamento), will now lead the market development.

Moving forward, the public and private sectors should work together to collaborate on programs to tackle the challenges and solve the sanitation infrastructure gap.

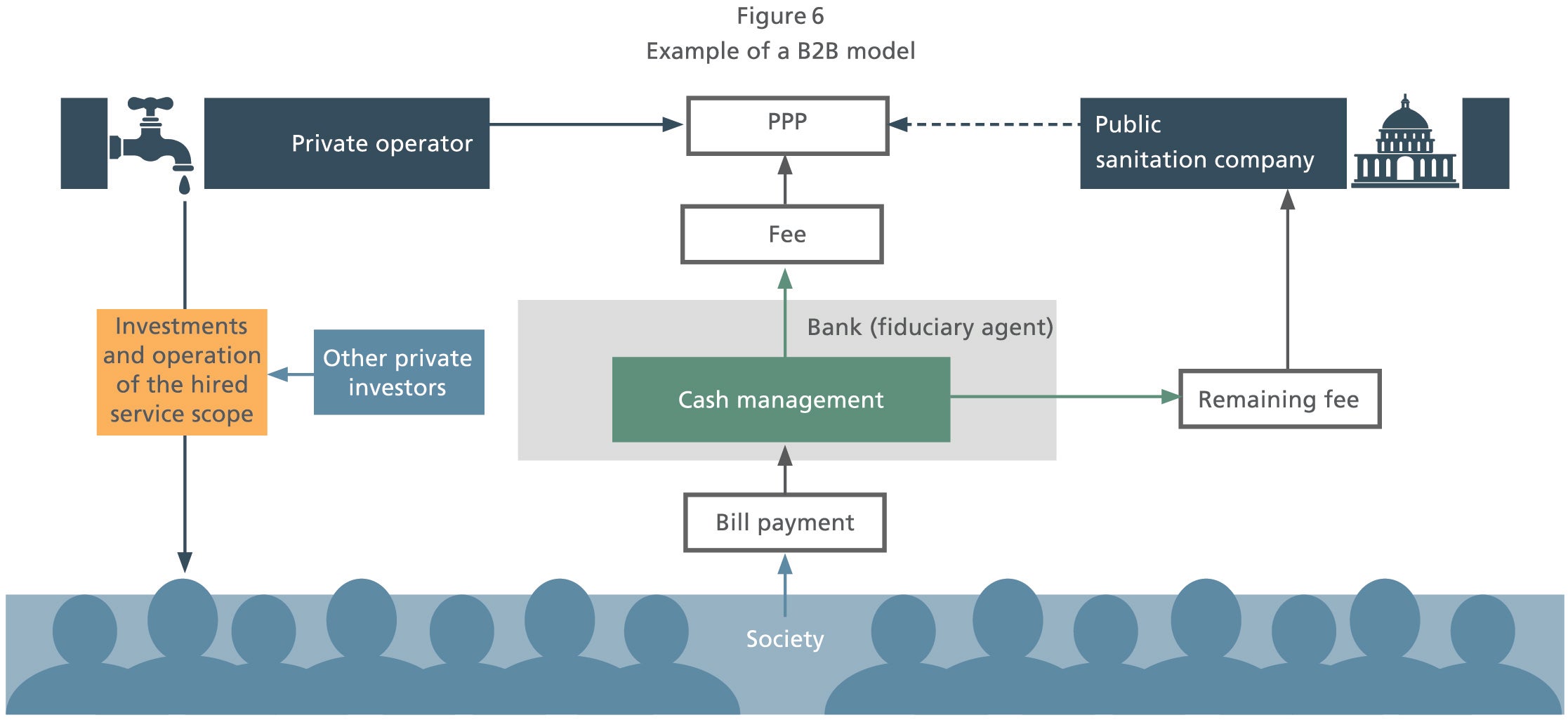

Introduce a disruptive business model that brings together the public and private sectors in collaboration, recognizing that privatization is not the solution. In this complicated context, the possibility of collaboration emerges. In the collaboration model, public operators concede parts of their services (especially those requiring large investments in the short term) through a PPP with an experienced private operator. Typically, in traditional concessions to the private sector, the new player is entitled to the revenues of both water distribution and sewage collection, while being responsible for expanding coverage to a predefined target during the concession period. In the alternative model, players opt for partial concessions or PPPs for sewage collection only (for example), where coverage is limited and investments are concentrated. Private operators bring their operational and investment capabilities, along with easier access to capital markets, while public companies continue operating existing services and assets (see Figure 6).

Further, all stakeholders could benefit from the collaboration model. Private operators access a large share of the market; public companies continue with their political assets (e.g., the right to keep the same company name in the city and the right to continue managing the assets and employees of the public company) and solve their investment issues. Furthermore, the general population gains access to a better service, and investors have a more solid opportunity to make money.

Design a mechanism that is legally viable and able to attract investors for the development of technical and financial studies by the municipalities responsible for the bidding process. One of the key success factors for modeling contracts is a well-developed feasibility (technical and financial) study. Over recent years, the market has used the PMI (Procedimento de Manisfestação de Interesse, or Procedure for Interest Demonstration) instrument, in which a private player conducts the study for a municipality or any other public entity. However, this mechanism is under pressure and is being questioned because of recent corruption scandals — in many cases, players that conducted the feasibility study were the winners of the bidding processes.

The market should pursue alternatives that protect all stakeholders from political interference. One option could be the creation of a trust fund managed by a neutral and trustworthy party, with clear compliance mechanisms to enable unbiased feasibility studies to be conducted.

Apply societal pressure. Finally, yet also important, it is critical that the public becomes part of the process and puts pressure on public management representatives to ensure that real and effective initiatives are implemented. For this matter, officials such as district attorneys (DAs) could play an important part in pressuring government.

This type of procedure is still rare in Brazil: Only 32 municipalities have established a TAC (Termo de Ajustamento de Conduta, or Conduct Adjustment Term) with DA’s offices, in a country where approximately 17% of the population have no access to water systems and approximately 50% have no access to sewage systems.

01072022130143