Differing perspectives of Retailer and Supplier and appropriately pricing distribution

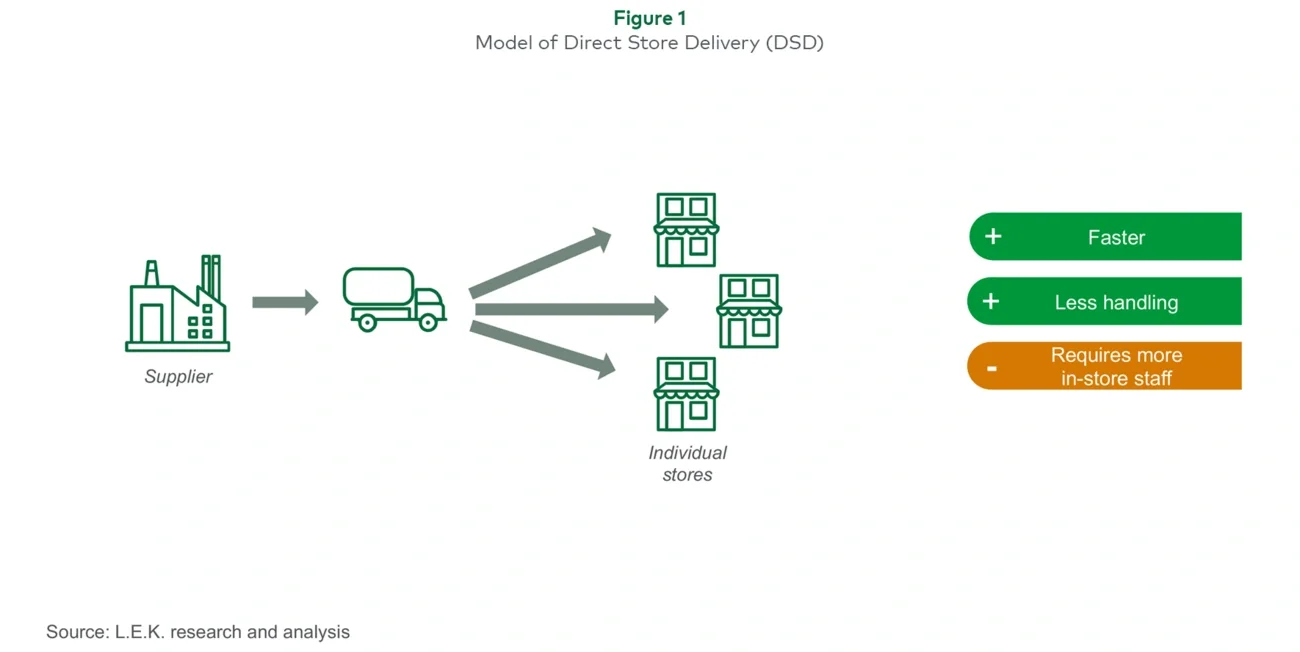

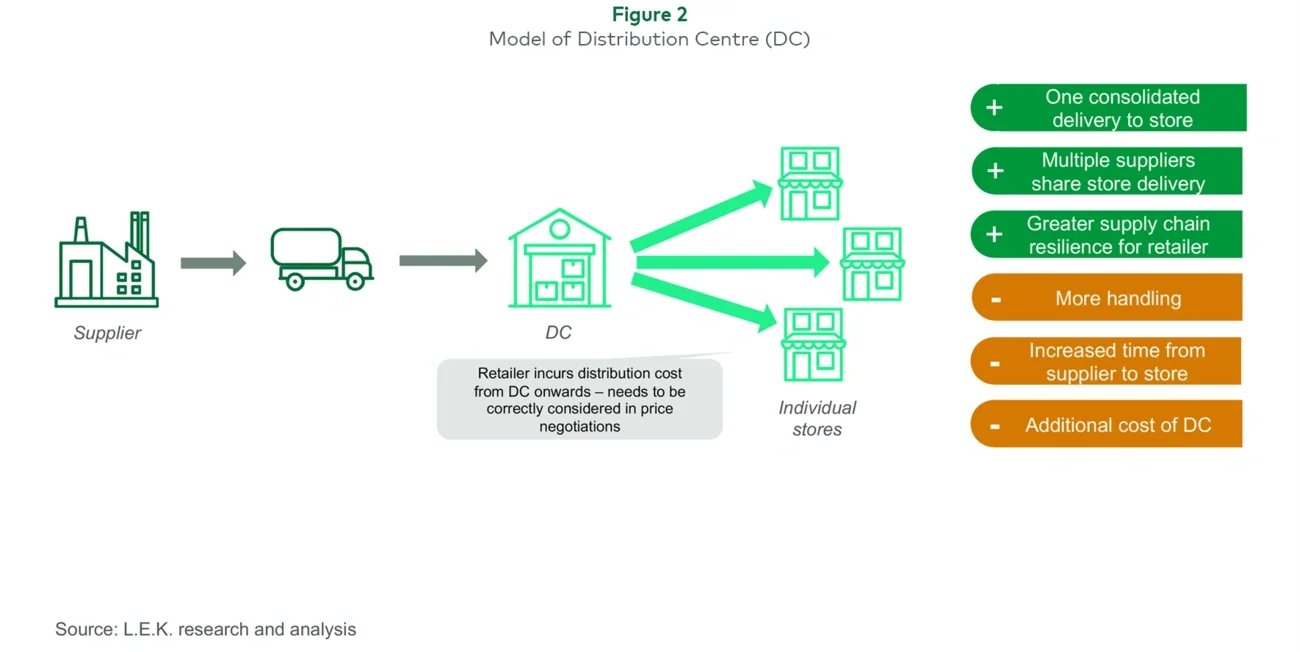

The use of DSD or a retailer’s DC shifts the responsibility and costs between the supplier and retailer, and naturally is a part of calibrating the price paid by the retailer to the supplier (i.e. the retailer should pay more to the supplier for DSD rather than just one delivery to a DC).

For a retailer considering setting up a DC, understanding if the new costs will be offset elsewhere is essential. When a retailer has a DC, correctly understanding the true cost of using their DC is key to knowing what discount is required from a supplier vs. one offering DSD.

For a supplier offering DSD, understanding at what price the retailer can utilise its DC is key to negotiating a fair price for distributing direct to store.

There is usually plenty of data to help a retailer or supplier understand these costs if it is collected, however retail buyers and suppliers typically have insufficient information at hand to correctly value the different distribution models, for example the benefit of alleviating pressure on a DC, or of reducing in-store labour requirements, would require careful analysis.

Future direction

While some high-profile suppliers in the US such as Kellogg’s and Nestlé have moved from DSD to the DC model in recent years, and Discount retailers in the UK, famous for their low-cost efficiency, continue to insist on the DC model, emerging trends and technological advances point to a bright future for the DSD model too, in specific circumstances.

Kellogg’s found that with significant advancements in warehousing technologies over the last decade, DC’s can deliver cost efficiencies for the supplier, its retail partners, and the customer, allowing for value creation across the supply chain. Similarly, Nestlé were able to reduce their headcount by 4,000 by switching to a DC model.

Sector by sector it is important to consider how market developments may impact which model is best. For example, in print newspapers, a DC model is used which pools distribution with other publications for daily delivery (given the time sensitive nature of the product), but separate from other products (e.g. F&B etc). However, the long-term decline in volumes, combined with increasingly efficient DC systems, may mean sharing distribution with other products could soon become a better option.

Understanding the true cost position and the emerging trends will enable suppliers and retailers to stay ahead of developments and maintain robust, low-cost supply chains. L.E.K. closely monitors emerging challenges, including fuel and labour costs, congestion and traffic, as well as warehouse costs, and will continue to work with suppliers and retailers to choose and optimise the best distribution model to suit their changing needs.