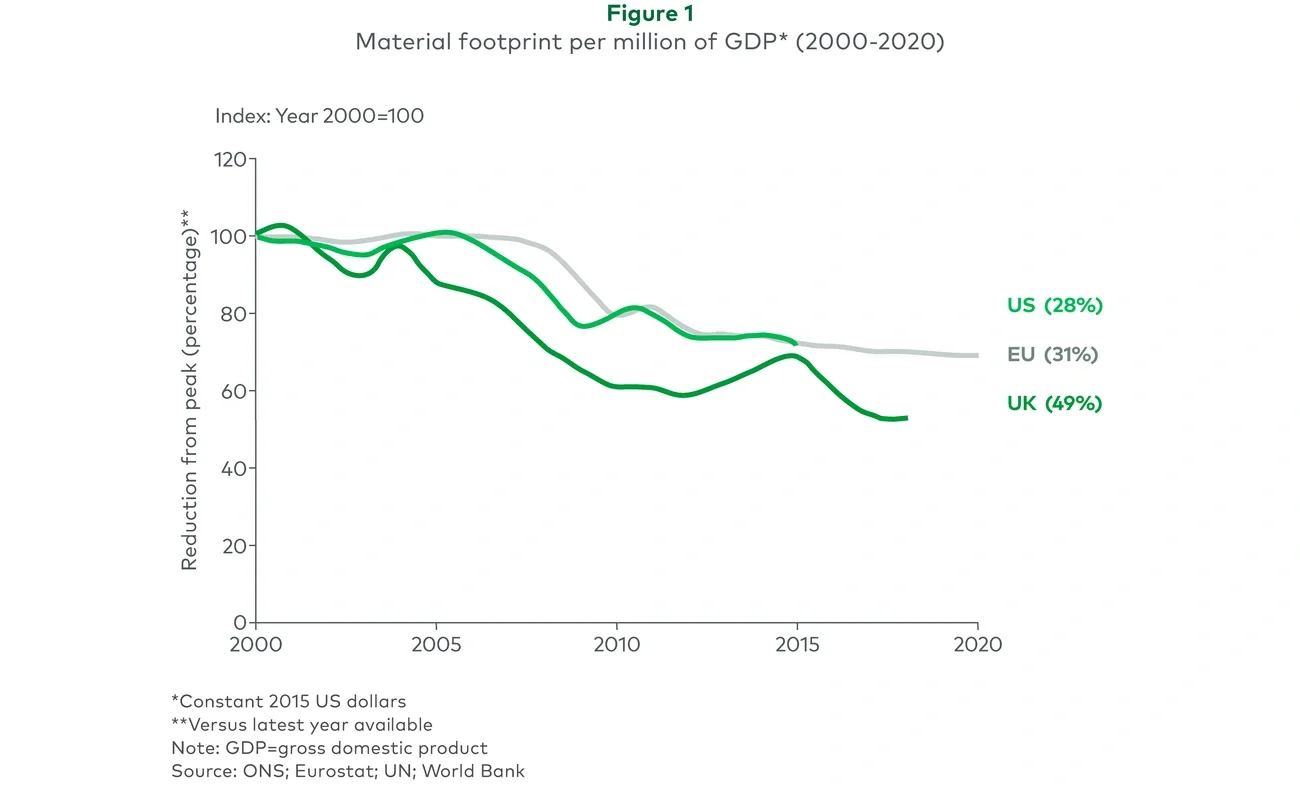

The trend is pretty clear — economic growth no longer requires more stuff. In fact, the divergence is very strong, and in 2018 UK GDP was 49% less material intensive than 2001’s peak (GDP is c.30% larger in real terms whilst material use is down c.30%). This applies widely across categories as well — the main categories of material consumption are biomass, metals, non-metal minerals and fossil fuels, and all categories show sharp falls in material intensity.

Meanwhile, total demand for materials globally is still growing, driven by China, India and other developing economies that have not reached peak stuff. The observation is not about supply shortages but instead about changes in how an advanced economy creates prosperity: it is becoming less dependent on material goods.

Why is GDP becoming less resource intensive?

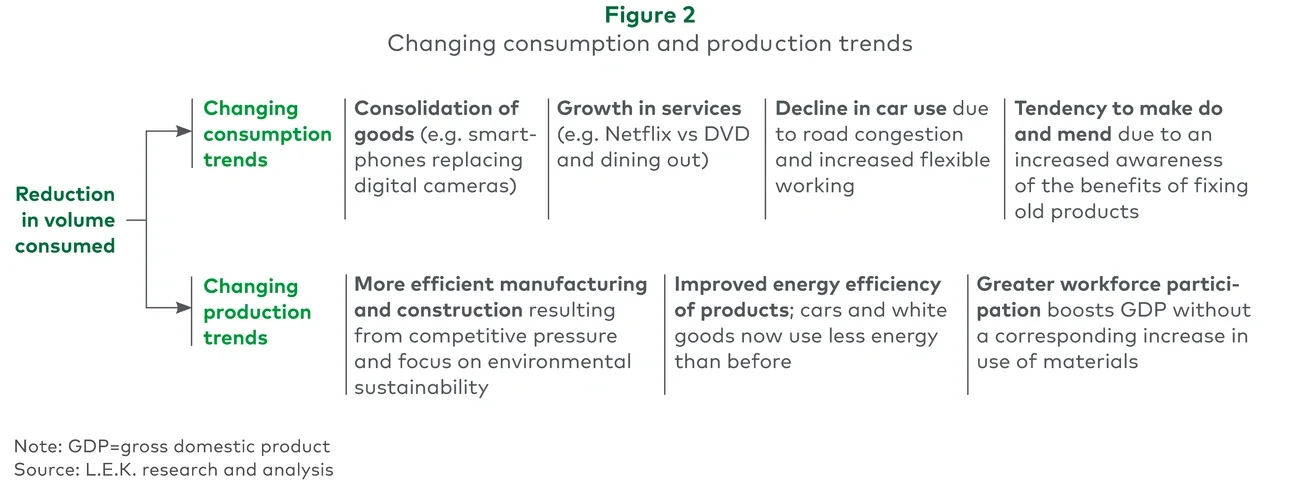

Broadly speaking, the main causes behind this peak stuff phenomenon and the divergence between economic growth and material usage can be grouped into two categories: either long-term, widespread changes in consumption patterns or changing trends in the way output is produced within advanced economies.

Most of the causes identified are long-term trends, so we can therefore anticipate continued reduction in tonnes per million of GDP in advanced economies, and that this will gradually become a wider trend globally as other economies mature and reach peak stuff.

Changes in consumption patterns:

-

The ‘iPhone effect’ – Technology has driven consolidation of goods. For instance, whilst the share of UK residents with smartphones rose to 85% by 2019 — replacing all sorts of other items (cameras, books, diaries, music, maps, torches, compasses, etc.) — digital camera ownership fell to 18%.

-

The rise of services – Services (as opposed to primary industries or manufacturing) have risen as a share of GDP, from 82% in 2000 to 88% in 2019 in the EU, as evidenced by the transition from goods such as DVDs, CDs and books to streaming services such as Netflix, Spotify and Kindle and the trend to eat out more — in the US this increased to 53% of total food sales in 2019, up from 43% in 2000. When consumers eat out, not much more food is eaten (on average less is wasted), so the amount of stuff used is not increased, but consumers also pay for restaurant service and hence GDP has increased.

-

A decline in car use and switch to public transport – Car use has been declining in developed economies, with a ‘peak car’ trend supported by a shift towards public transport. New passenger car registrations in the US declined over the past 20 years, with new cars c.46% lower in 2019 than in 2000. In the UK, public transport increased its share of total passenger miles travelled per capita from 13% to 17% between 2002 and 2019 (although since then car transport has rebounded faster in the short term from Covid-19).

-

Make do and mend – Global consumer sentiment about environmental sustainability, reducing waste, consciously reducing consumption and reusing products has decreased consumption. ‘Right to repair’ legislation in the UK and EU, which was introduced in 2021, is set to exacerbate this trend.

Changes in production (see Figure 2):

-

Improved efficiency of manufacturing and construction – Competitive pressure and focus on environmental sustainability have led to a need for greater material efficiency: using less raw material in manufacturing and optimising material use in construction. For example, TVs have become lighter; a 25-inch cathode ray tube TV would typically weigh 45kg, but now a 32-inch liquid crystal display TV would weigh less than a third of that, at 12kg-14kg.

-

Improved energy efficiency of products – New cars in Great Britain in 2020 used 32% less fuel per kilometre than in 2000. In the EU as a whole, the specific consumption of large appliances (measured in kilowatt-hours per appliance) has decreased steadily since 2000: by 2019, efficiency gains were above 30% for refrigerators, washing machines and dryers; for freezers and dishwashers, gains were a little lower at c.28%.

-

Increased workforce participation – Greater workforce participation over the past 20 years has contributed to a growing economy without a corresponding increase in consumption, as those working do not consume significantly more than non-workers. In the UK in 2019 the employment level reached 76%, up from 73% in 2001. (Although this declined in 2020-21, rates post-Covid-19 recovered to c.75.5% in 2022.)