As the demand for public transit continues to recover following the end of the pandemic, attention has been directed at the range of policy levers available to support ridership growth.

In an earlier Executives Insights we addressed the role of free and flat fares as potential strategies to grow transit ridership — but fare capping and subscription-based pricing are also being considered as a means of unlocking growth.

Fare capping

Fare capping is not new

Although not generally referred to as fare capping, periodical passes that offer unlimited travel over a fixed duration — daily, weekly, monthly or even yearly — are a form of price capping.

Before the emergence of the e-purse, with first-generation smart-card fare collection systems, such products were commonplace in the fares product suite. The e-purse provided the opportunity to mimic the periodical product by deducting a fare until the price cap was reached.

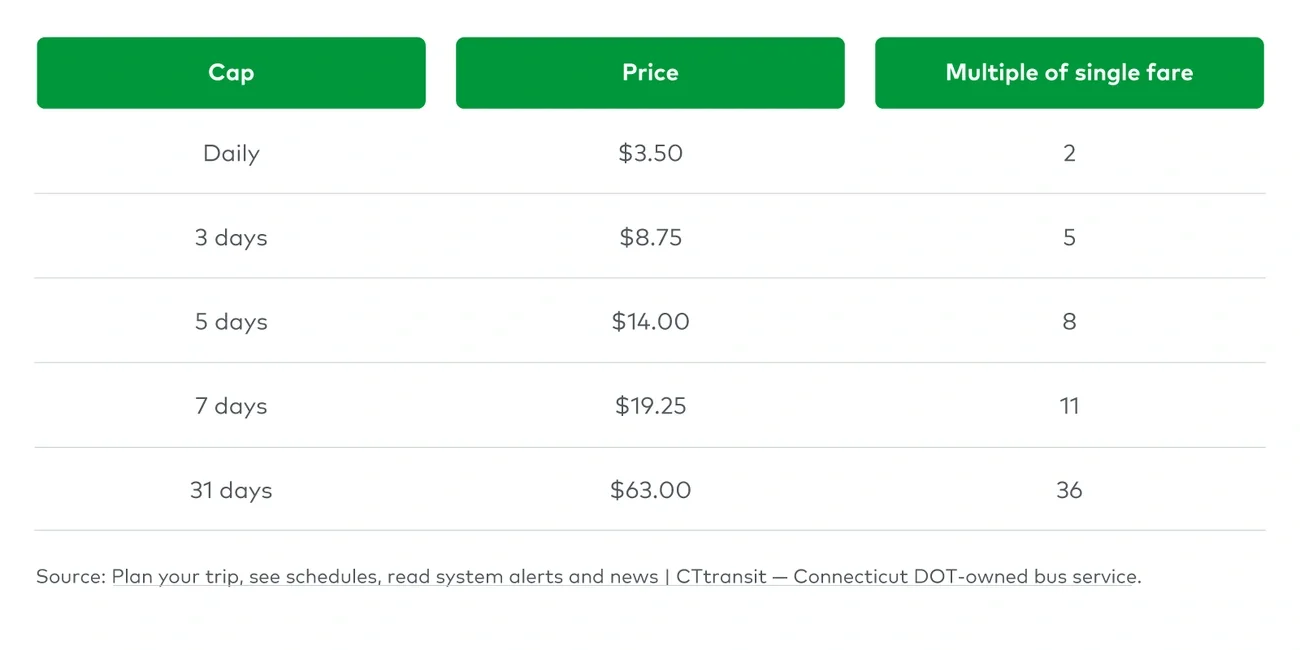

A daily cap is typically designed to provide free travel at the margin over and above the daily commute (e.g. inter-peak or off-peak travel) in selected cities. The table in Figure 1 below sets out the daily fare cap multiple (i.e. the number of equivalent-peak single fares). It shows that, with the exception of Toronto and Paris, a customer making at least three trips will reach the daily cap; that increases to at least four in Toronto and at least five in Paris.

The weekly periodical pass or a capped weekly fare remains a core product for many jurisdictions. For example, the seven-day London Travelcard has been an enduring product offering unlimited travel at any time on bus, Tube, Tram, DLR, London Overground, Elizabeth line and National Rail services for the zones determined by the customer.