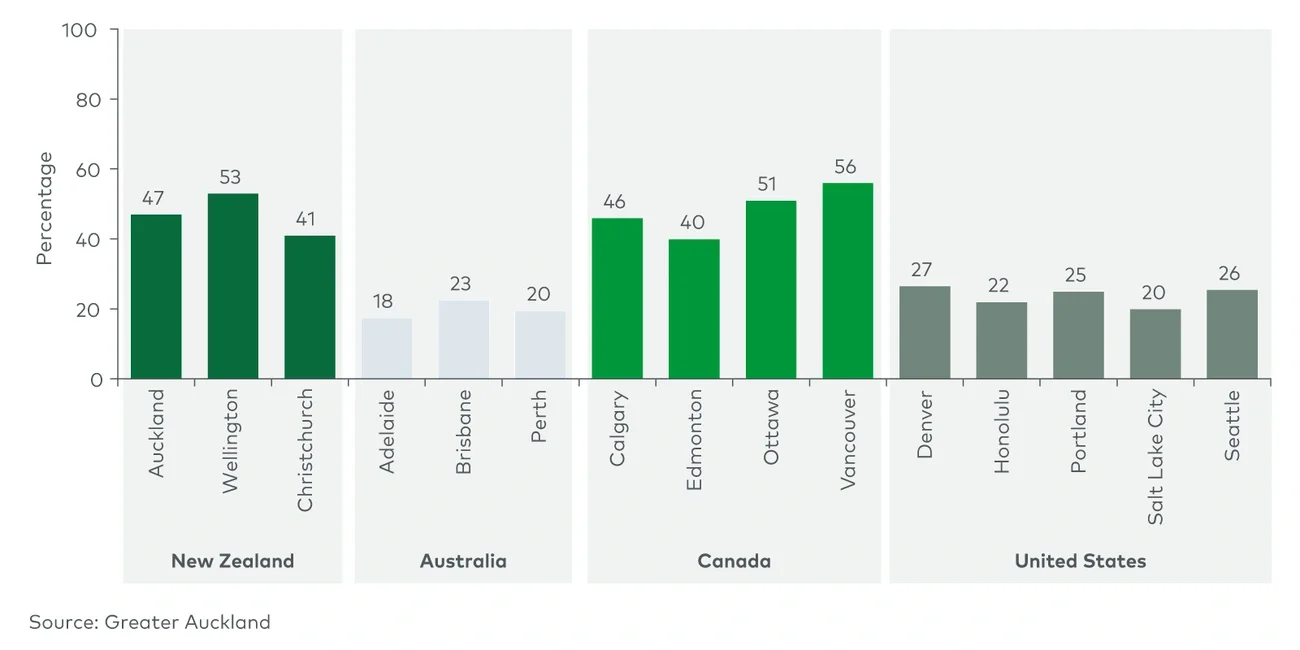

While the appropriate contribution that customers should make to the recovery of transit operating costs is a complex issue (including the need to provide a safety net for the transport-disadvantaged), it needs to be acknowledged that any fare policy reform that is not revenue positive will increase the required government subsidy. With government budgets under enormous pressure, this must be a key consideration. Moreover, as we continue to invest in new services, the magnitude of the required government subsidy increases, which is exacerbated by any change that dilutes farebox revenue.

While any fare reductions will support an increase in public transport growth, a long-understood challenge is that the farebox revenue derived from new customers is insufficient to offset the loss of farebox revenue from existing customers. In the language of economists, the demand for public transport is ‘inelastic’ (studies from the Journal of Public Transportation and Productivity Commission confirm an own-price fare elasticity of c.-0.3 on average, which typically varies between -0.2 to -0.3 and -0.4 to -0.5 for peak and off-peak services respectively). This is not only true in the morning and evening peaks, which have historically been dominated by commuters, but also in other time periods, albeit to a lesser extent.

We should also rightly look at the economic benefits of general fare reductions. In addition to being a poor means of ‘buying’ patronage, broad fare reductions do not have a strong economic case. The level of mode shift from the private motor vehicle and the associated reduction in congestion and associated environmental externalities by way of reduced greenhouse gas emissions does not have a compelling economic case. Direct road pricing is clearly the preferred means of providing the correct pricing signals associated with road use.

What are the alternatives?

If we accept that broad-based fare discounting does not have strong support on financial or economic grounds to support post-COVID-19 growth, where do we go?

There are a number of key suggestions:

Firstly, before committing to a permanent change, attempt a ‘trial and learn’ period. If the initiative has the potential to be revenue-positive, it should be possible to infer this from a trial, recognising that all public transport demand data has noise in it, which invariably makes before and after analysis somewhat harder.

Secondly, carefully consider what are our target markets. For example, it could be the case that additional support through targeted concessions may be a superior approach to broad-based fare changes.

Thirdly, with the benefit of contemporary (account-based) transit fare collection systems, it is time for transit agencies to embrace a yield management approach to fare setting and grow both patronage and revenue simultaneously — as opposed to trying to defy gravity by broad-based general fare cuts.

Lastly, consider how the forgone farebox revenue could be invested to improve transit service levels and/or quality factors such as frequency and coverage. A marginal dollar directed to improvements in service levels or service quality will almost certainly have a better financial and economic return than the equivalent dollar invested in reduced fares. Multiple studies show that service quality is a key driver of patronage, with research undertaken by the Victoria Transport Policy Institute suggesting an elasticity to service frequency and service expansion of 0.5 and 0.6 to 1.0 respectively.

For more information, contact strategy@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting LLC