Implementing congestion-specific pricing as a standalone mechanism in metro centres is challenging and may be limited in the behavioural outcomes it achieves. A holistic approach to road and congestion pricing across modes on a “mass – time – distance – location” basis would provide a better mechanism to drive the desired behaviour across the entire system. The ability to vary pricing across modes and peak periods will help alleviate behaviours that lead to congestion.

Conclusion

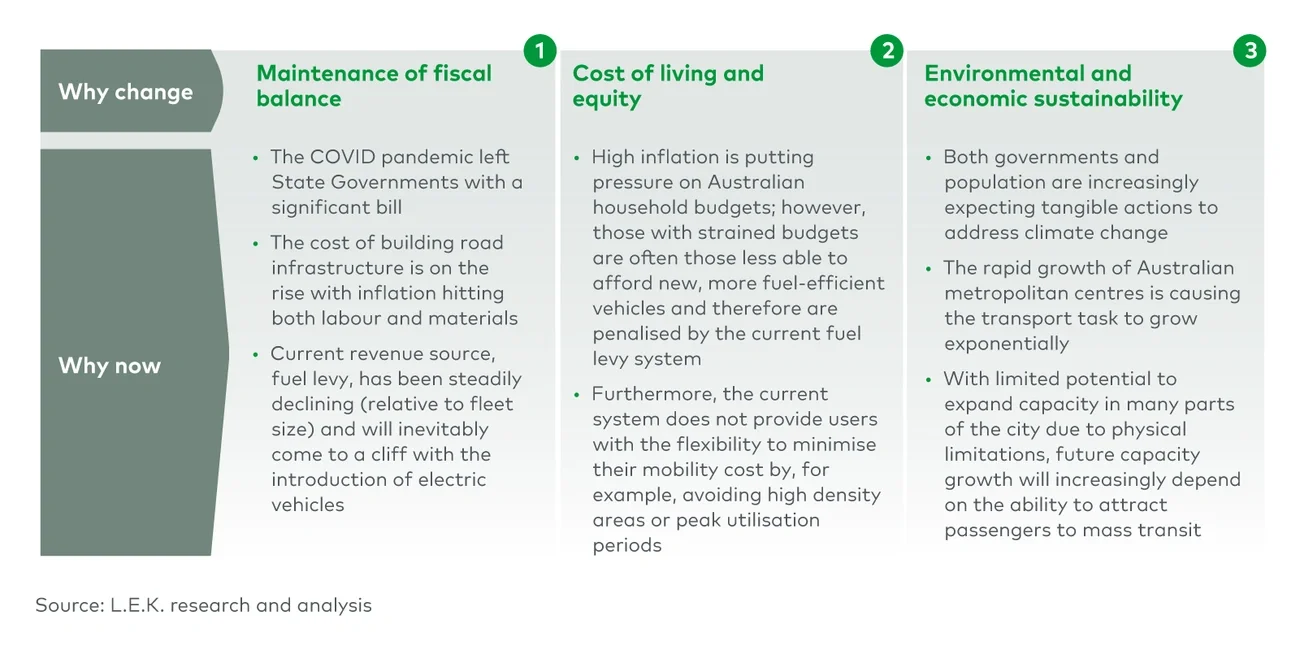

With technological and behavioural shifts already changing the way mobility is consumed in Australia, and increasingly stretching both the operational capacity of existing infrastructure and the funding used to maintain and provide such infrastructure, there is a sense of urgency to enact holistic mobility pricing reform to maintain the relevance, efficacy and equity of transport systems.

From a customer perspective, the future commodity will no longer be private or public transport but rather mobility per se, leveraging current and emerging/future offers including ride pooling and fleet owned and operated vehicles. Inevitably, customers will demand that pricing models be aligned with such a choice set, including (for example) subscription and dynamic pricing. Again, this will have profound implications in terms of its financial, economic and social perspectives.

There is significant scope for “moving the dial” with a clear vision in mind. Key outcomes include securing the funding environment, clarifying pricing signals and maintaining operational efficiency while preserving social equity. These areas do not exist in isolation and should be considered together so that incentives may be aligned and different policies and behaviours can exist in harmony.

It is crucial for policymakers to identify the behaviours and outcomes they are seeking to influence through the pricing of mobility options. Strategies should also be mindful of the linkages between the pricing of public transport and the pricing of private motor vehicle usage. Pricing transport holistically should help consumer mobility decisions to be more readily rationalised and achieve greater efficiency of operation across the entire transport network.

For more information, contact strategy@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting

Endnotes

1BITRE, Australian Infrastructure and Transport Statistics Yearbook (2022)

2, 10, 12Ibid.

3The Driven (2023); “Australia EV sales by model”

4The Insight Partners, Asia Pacific Ride-Hailing Service Market report (2022)

5L.E.K. 2023 Global Mobility Survey

6Australian Institute of Family Studies, “The relationship between transport and disadvantage in Australia” (2011)

7NSW Parliament (2022)

8Victorian Infrastructure Plan (2021)

9Productivity Commission, Public Transport Pricing (2021)

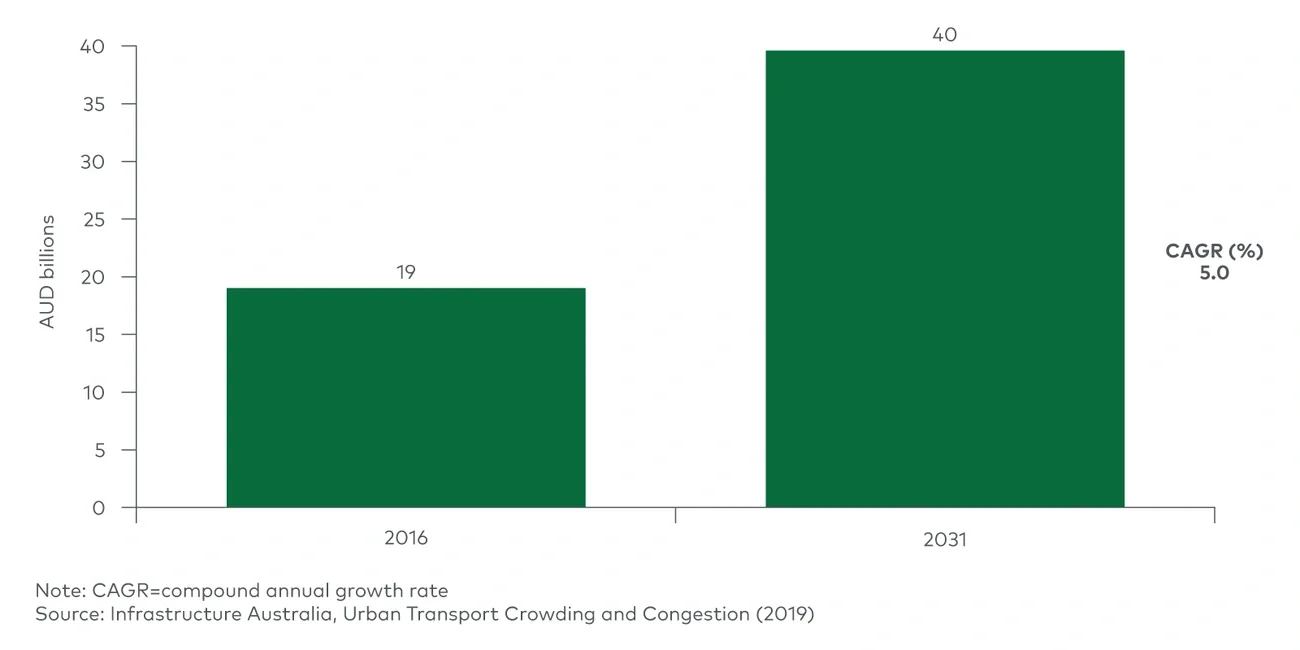

11Infrastructure Australia, Urban Transport Crowding and Congestion (2019)