Key takeaways

-

The GPO model was designed to benefit both health systems and suppliers. But medtech suppliers say that the value they receive from the national GPOs has diminished.

-

Hospitals and health systems also are questioning the value they receive from national GPOs. This has opened the door to competition from smaller, more focused purchasing organizations.

-

Meanwhile, potential disruptors are moving in with alternative, technology-enabled solutions.

-

Although large health systems are increasingly open to negotiating their own medtech contracts, half of the market consists of smaller provider organizations that still depend on GPOs.

-

For medtechs, these trends present an opportunity to achieve higher retained value. To optimize this value, however, medtechs will need a nuanced strategy that acknowledges the business remaining under GPO control.

Medtech companies have long had a complicated relationship with group purchasing organizations (GPOs), especially the national GPOs. GPOs offer opportunity for greater market coverage and efficient contracting, both of which benefit medtechs and their provider customers. At the same time, there is pervasive and not-so-subtle grumbling about the marketplace influence GPOs can wield and the level of reciprocal value realized by medtech companies.

Despite these misgivings, medtechs continue to “grin and bear it.” This is due in part to long-entrenched practices, as well as to fears of retaliation from GPOs, which can limit market access. These fears have been supported by high-profile attempts at disintermediation by Medtronic and GE Healthcare over the past decade that ultimately washed out.

But like many other dynamics in healthcare, the interplay between GPOs and medtechs is poised for change. Health systems are becoming increasingly sophisticated, taking more control of their supply chains and becoming more demanding toward their supply chain partners. The once-collegial member community of GPOs is becoming increasingly transactional, with GPOs shifting focus and member engagement models. How a medtech should respond is a nuanced question, but the opportunity for change is at hand.

The shifting GPO environment

When GPOs emerged in the healthcare industry decades ago, the model was designed to bring value to hospitals and health systems by aggregating demand and negotiating lower prices among suppliers. Importantly, the model also intended to return value to suppliers via volume conversion and product-brand promotion. This historical approach has proliferated into many different models today.

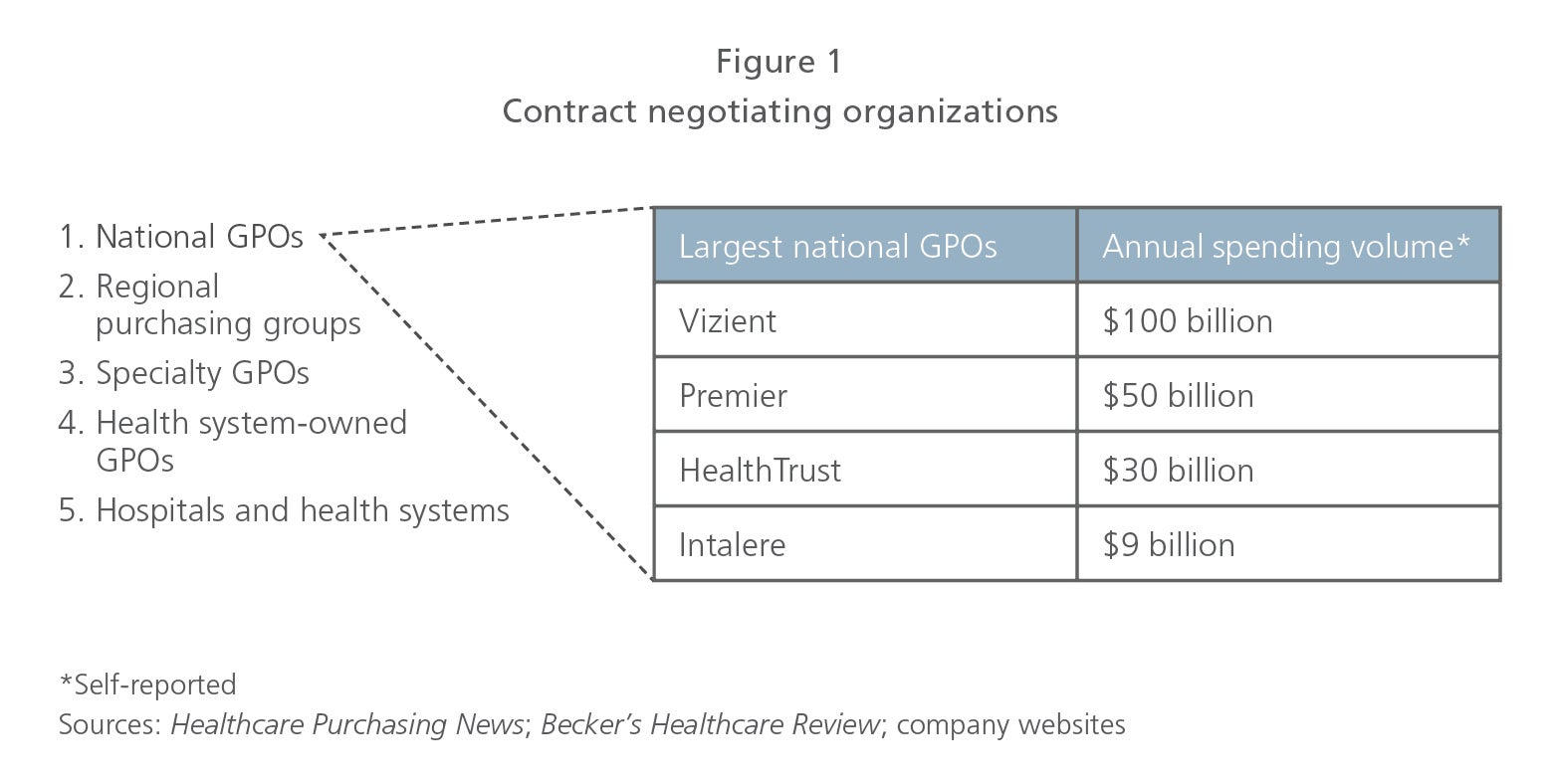

The trade association representing GPOs, the Healthcare Supply Chain Association (HSCA), states that more than 600 organizations in the U.S. participate in some form of group purchasing. Significant variability exists among these organizations, and classifying them into clear segments can be tricky. We broadly identify five categories of organizations that are negotiating contracts, four of which are types of GPOs, and all of which must be managed and navigated by medtech companies. In Figure 1, the degree of affiliation between member organizations generally becomes tighter as you go down the list.

In their conversations with L.E.K. Consulting, medtech suppliers have consistently asserted that the national GPOs’ ability to return value to manufacturers has diminished markedly over time. Key factors that have contributed to this deterioration include the spread of multisource contracting and the Walmart-like breadth of manufacturers and contracts listed. Additionally, as health systems have gotten larger, they are applying significant pressure on suppliers and using GPO contracts as a benchmark for further negotiations. This undermines the utility of the GPO contracts.

But perhaps the tipping point for shifting attitudes among medtechs may be the recently reported bumps in administrative fees charged by some national GPOs. These increases go well beyond the long-standing industry benchmark of 3%. “We’re on the threshold of a very big change,” says John Strong, former head of Consorta and longtime supply chain expert. “The national GPOs have been pushing their fees to 5-8%, even 9% in some cases. Providers are starting to ask themselves how these increases are affecting the unit prices they see on products — and how much they’re really getting back.”

As Strong alludes, the debate about the value of national GPOs is raging not only among medtechs but also among the nation’s hospitals and health systems. The 2015 merger between VHAUHC Alliance and MedAssets, which formed Vizient, is frequently cited as triggering the reevaluation of GPO relationships among a number of providers. Vizient is now by far the largest of the four national GPOs, with an estimated $100 billion in annual purchasing volume (see Figure 1). Core to the debate are the level and type of value that can be realized in an era of reduced member loyalty and growing sophistication among major hospitals and health systems.

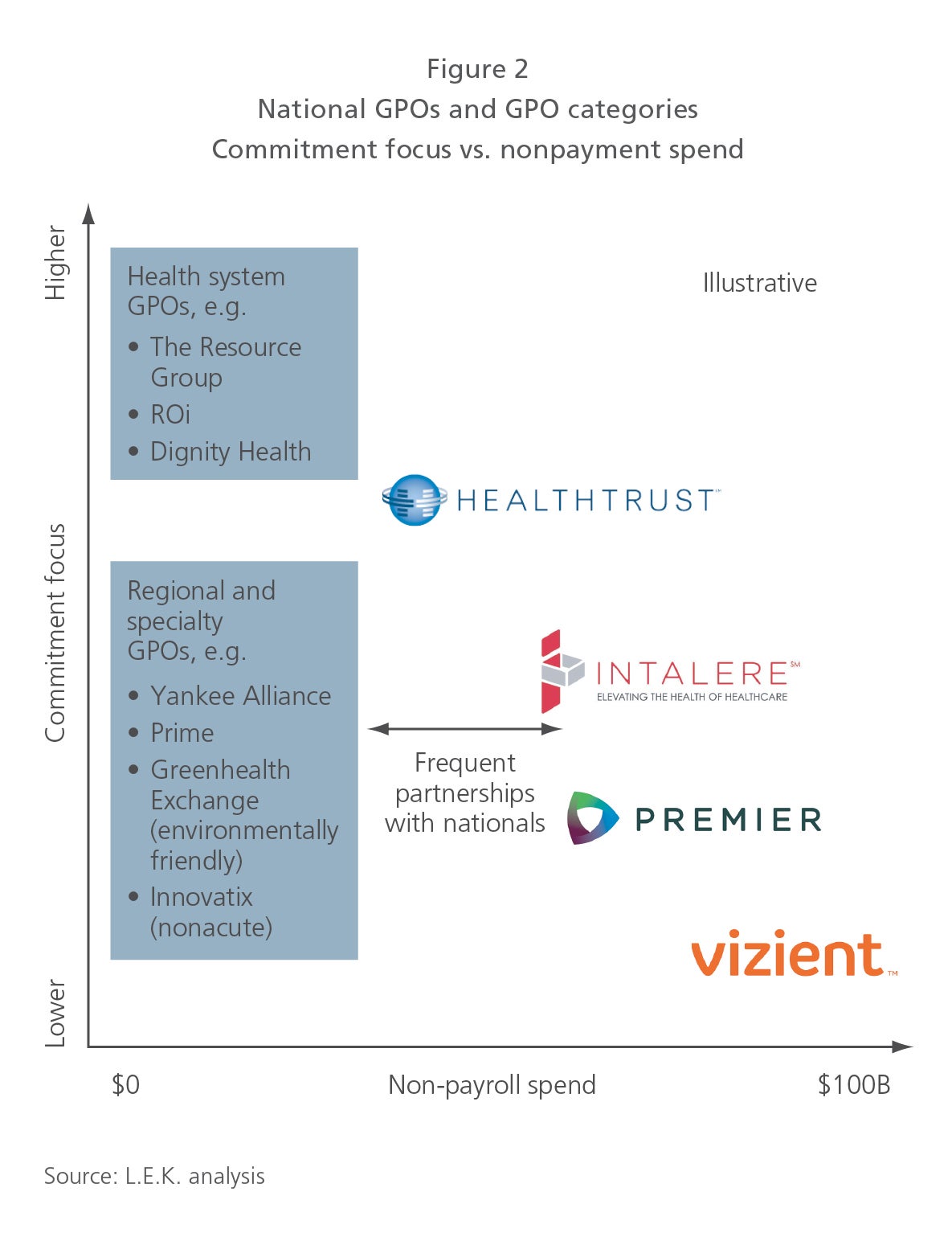

These factors have opened the door for the more highly focused, relatively smaller GPOs, which have coexisted with the national GPOs but are now growing in prominence (see Figure 2). Over the past few years, regional purchasing groups (RPGs), health system-owned GPOs and specialized GPOs have all reported strong growth.

These GPOs are exploiting their tighter focus as a means to deliver differentiated portfolios and greater value. For example, regional and health system-owned purchasing groups emphasize services tailored to local needs and sole-sourcing to deliver more efficient demand aggregation and higher levels of compliance. Specialized GPOs drive differentiated value via targeted product categories (e.g., pharmacy, environmentally friendly products) and/or customer bases (e.g., nonacute, specialty specific). The buying groups also tout their ability to provide improved reciprocal value to their participating suppliers.

In response, the national GPOs are increasingly pushing their models and market positioning beyond pure contracting to more holistic management of the supply chain dynamics that drive total cost of ownership. Longtime investments in data and analytics, particularly by Premier (PremierConnect) and Vizient (Savings Analyzer), are seen as key to this evolution. Each leverages large data repositories for supply chain insights.

Still, it’s evident these same national GPOs are doubling down and attempting to combat competition head-on in all forms. Vizient, Premier, HealthTrust and Intalere have all built closer ties to RPGs and made renewed investments in regional steering committees and affinity groups. Some are also offering and promoting tools to assist members with their direct contracting activity, such as the aptitude platform from Vizient. The breadth of activity by the national GPOs comes across as a bit defensive, and they appear to be hedging their market bets, thereby prompting ongoing questions about their longer-term vision, effectiveness and depth.

Potential disruptors making a move

Strong market forces and stakeholders have kept traditional healthcare supply chain practices entrenched and left incumbents focused on evolutionary, not revolutionary, improvement. But today’s technology and market dynamics make historical barriers seem less daunting. Moreover, the demand for price transparency and cost efficiencies continues to escalate, creating opportunity for new solutions.

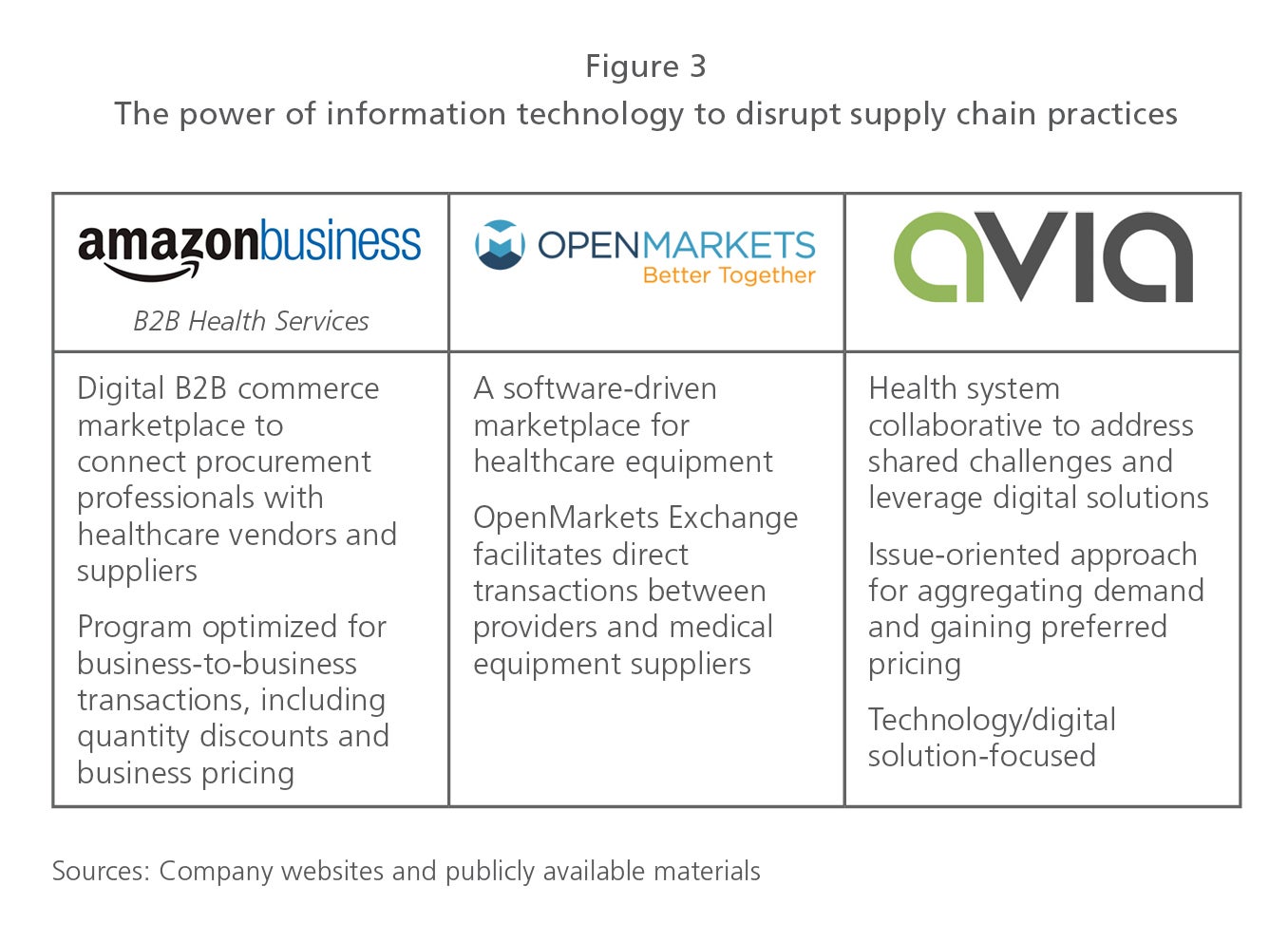

Startups such as OpenMarkets and AVIA Innovator Network recognize the long-standing inefficiencies and have built technology-enabled channels to connect product and service suppliers directly with providers. Their solutions promote cost efficiency and price transparency as well as stronger collaboration between providers and suppliers.

But Amazon is the main party to thank for putting the healthcare industry — including medtech manufacturers, GPOs and distributors — on notice. Amazon is ramping up and rolling out its B2B Health Services program. With a history of upending established business models, and boasting a $475 billion market cap, this powerhouse certainly has the capability to shake up supply chain practices, including contracting (see Figure 3).

Balance of power shifting to large health systems

The shape of the GPO sector, and supply chain practices more broadly, will ultimately be determined by the customers responsible for the spend — in this case, the nation’s hospitals and health systems.

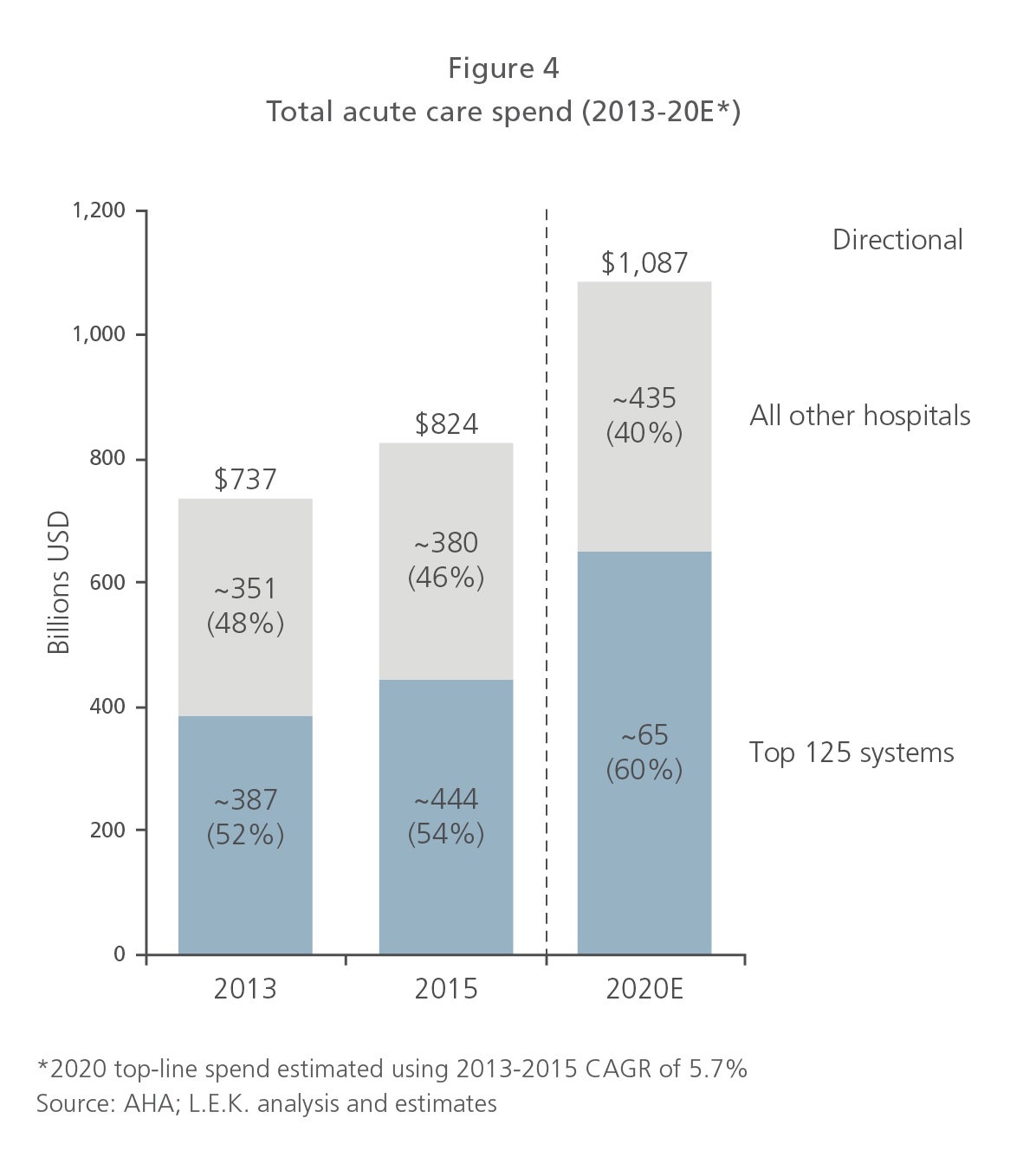

Medtech manufacturers and GPOs alike place much of their focus on the nation’s largest health systems, and for good reason: The top 125 systems represent approximately 2,200, or 43%, of the nation’s 5,100 or so hospitals, and in 2015 they accounted for 54% of total acute care spend (see Figure 4). The top 125 systems are an effective and critical channel for medtechs to target in order to achieve commercial success. Furthermore, the top 125’s command of medtech mindshare and resources will only continue to grow. We estimate their proportion of spend will grow to 60-65% of total acute care spend by 2020.

Large health systems are increasingly leveraging their scale and resources to aggregate demand, push for supplier rationalization, invest in supply chain analytics, and drive product standardization and compliance. Some health systems are also increasing their investment in distribution centers and logistics in order to gain broad-based ownership of the supply chain.

As the large health systems continue to consolidate the market, and as they grow their supply chain sophistication and capabilities, they are better equipped to negotiate their own high-value contracts while simultaneously establishing deeper partnerships with their suppliers. Recent multiyear, systemwide agreements are a reflection of this movement, though still relatively rare and typically related to capital equipment. Two examples: the 15-year, $500 million enterprise managed services model between Philips Medical and WMCHealth in New York State, and the 14-year managed equipment services agreement between GE Healthcare and Heritage Valley Health System in Pennsylvania.

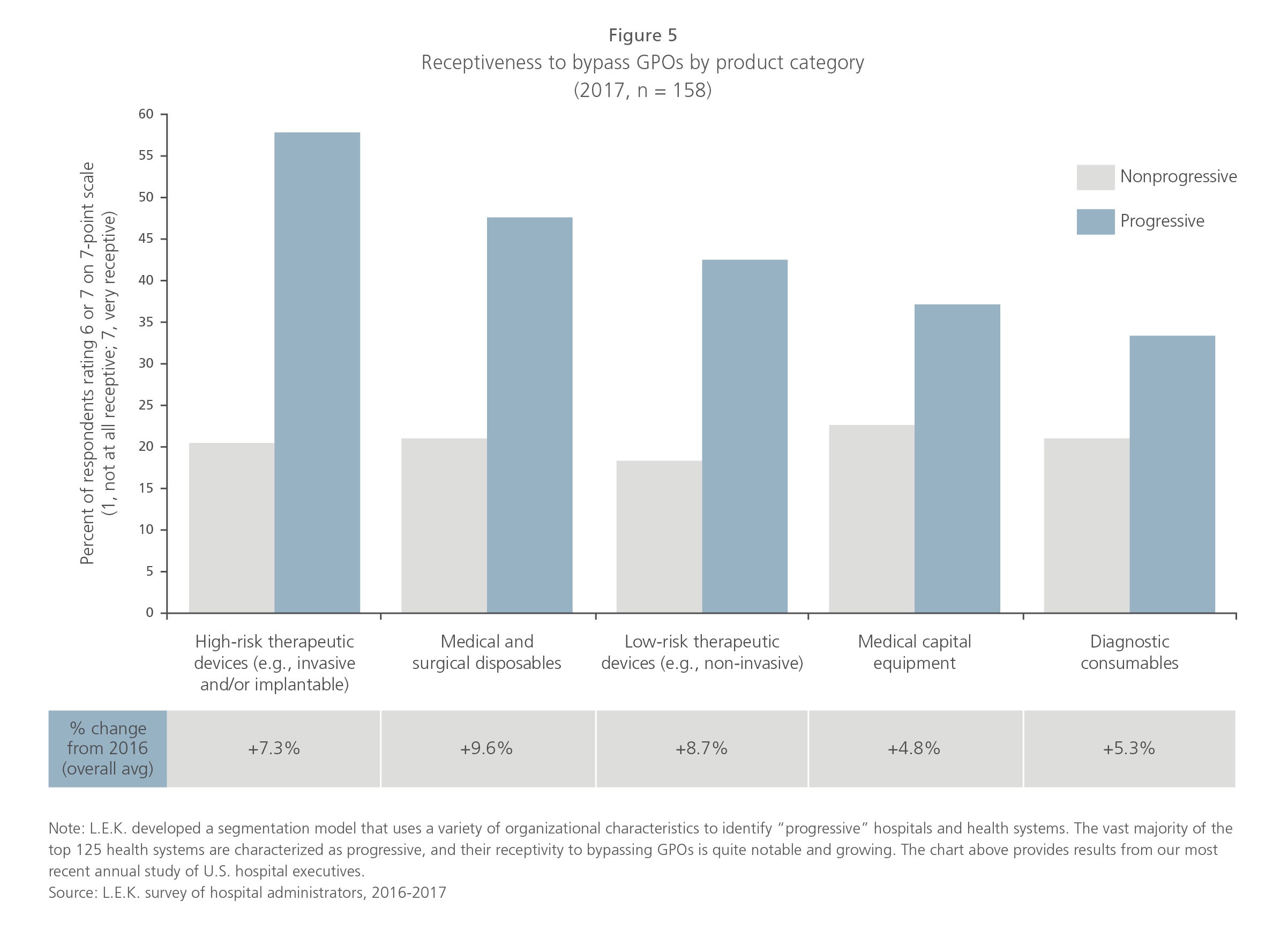

In an annual study L.E.K. conducts with hospital administrators, we find progressive health systems are increasingly receptive to bypassing GPOs for their medtech contracts (see Figure 5). Additionally, some leading health systems have established their own GPOs. The Resource Group (Ascension), ROi (Mercy) and Dignity Health Purchasing Network are three prominent players born from large progressive systems, with several others emerging.

These developments are leading to growing friction in the GPO business model. Large, progressive health systems are increasingly owning and controlling their own supply chain destinies. At the same time, national GPOs are attempting to engender loyalty from these very same organizations by building out their own, sometimes similar, capability sets and providing higher-value services. At risk of being lost in the middle are the GPOs’ smaller-budget members in the broader market.

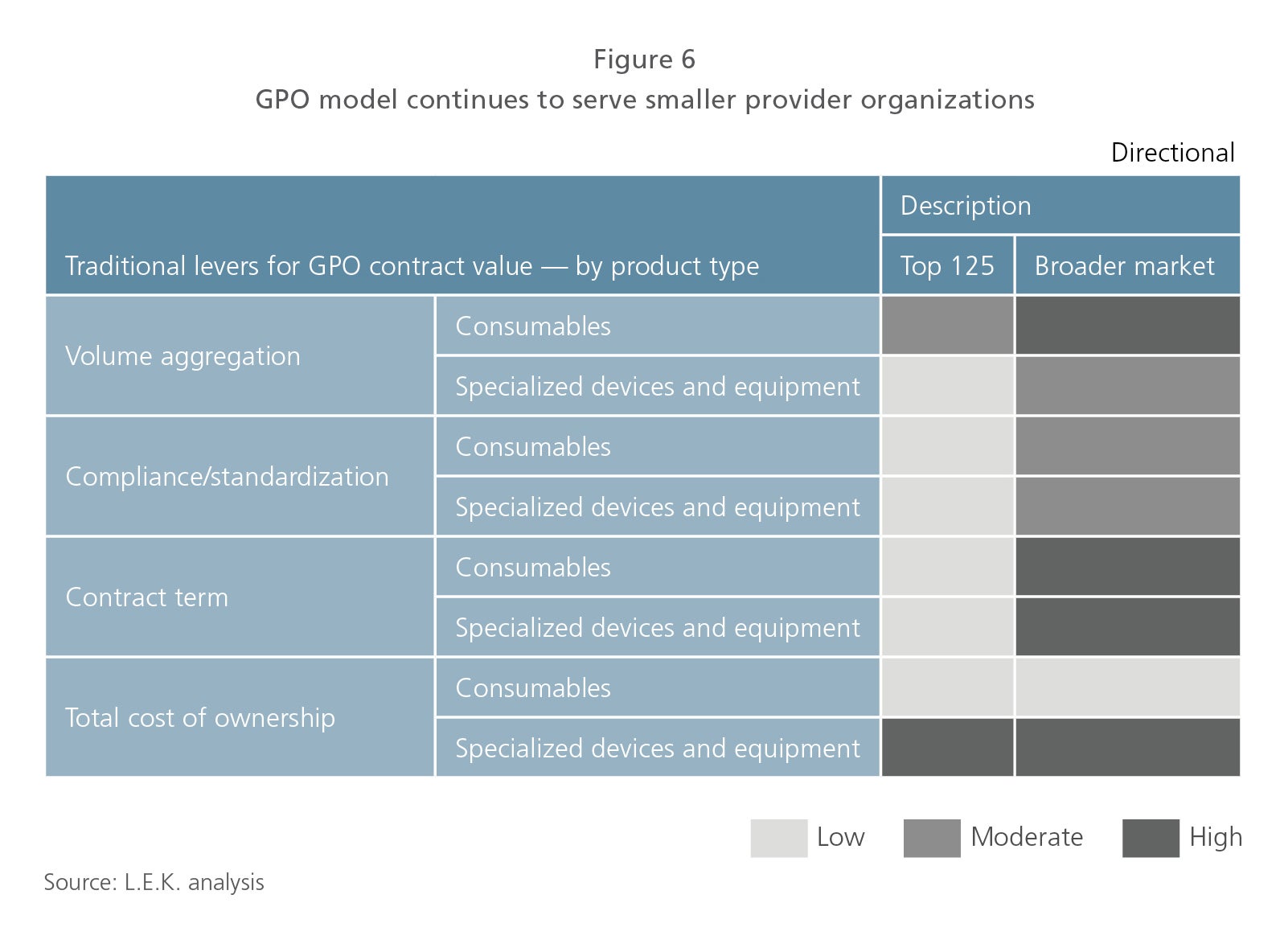

Correspondingly, medtech companies are increasingly finding that their top health system customers are demanding deeper and more direct partnerships, which marginalizes the role of the GPO. Medtechs, however, cannot ignore the other half of the hospital and health system market. Although significant in the aggregate, these provider organizations account for the long tail of the demand curve, often reflecting a lower degree of centralized purchasing and smaller respective volumes. For these customers, the traditional GPO model continues to offer both providers and medtechs value as well as efficiencies (see Figure 6).

Medtechs and GPOs: Where do we go from here?

For contracting-related value, the center of gravity for negotiation leverage is being pushed increasingly toward the larger health systems as well as toward meeting regional/local and specialized purchasing needs.

These shifts are changing the dynamic between hospitals and health systems and the range of GPOs in the market, offering medtechs greater negotiation leverage and the opportunity to achieve higher retained value. Medtechs must recalibrate their existing GPO relationships as well as their willingness and determination to make some calculated trade-offs. Furthermore, the entry of potential disruptors, such as Amazon, will require medtechs to respond both proactively and strategically.

Making changes to long-standing practices will inherently increase relationship and contract management complexity, but the potential upside benefits are substantial. These include deeper and more direct relationships with key customers, greater value retention, and higher conversion rates for products that remain on GPO contract.

For hospital and health system customers, the endgame is to achieve optimal efficiency and price. If medtechs had only the top 125 health systems to consider, they would likely transition to a direct contracting and supply model. Pragmatically, such a model doesn’t align with the reality of the market. GPOs will continue to play an important role in broader market access, so medtechs need to determine how best to navigate and manage these relationships thoughtfully.

Just as a one-size-fits-all sales model no longer suffices for medical device companies in the rapidly evolving provider landscape, nor will a singular approach work for medtechs in their dealings with GPOs. Medtechs will need to tackle a number of issues to shape a nuanced and stratified GPO strategy that is positioned for optimizing value. “Medtech suppliers need to look at it multidimensionally,” adds John Strong. “How much of the business do the GPOs really control? How much do we control due to the services, products and people that we have? What do we get in return for the fee? How much value is there in the ‘hunting license’ the GPO affords?”

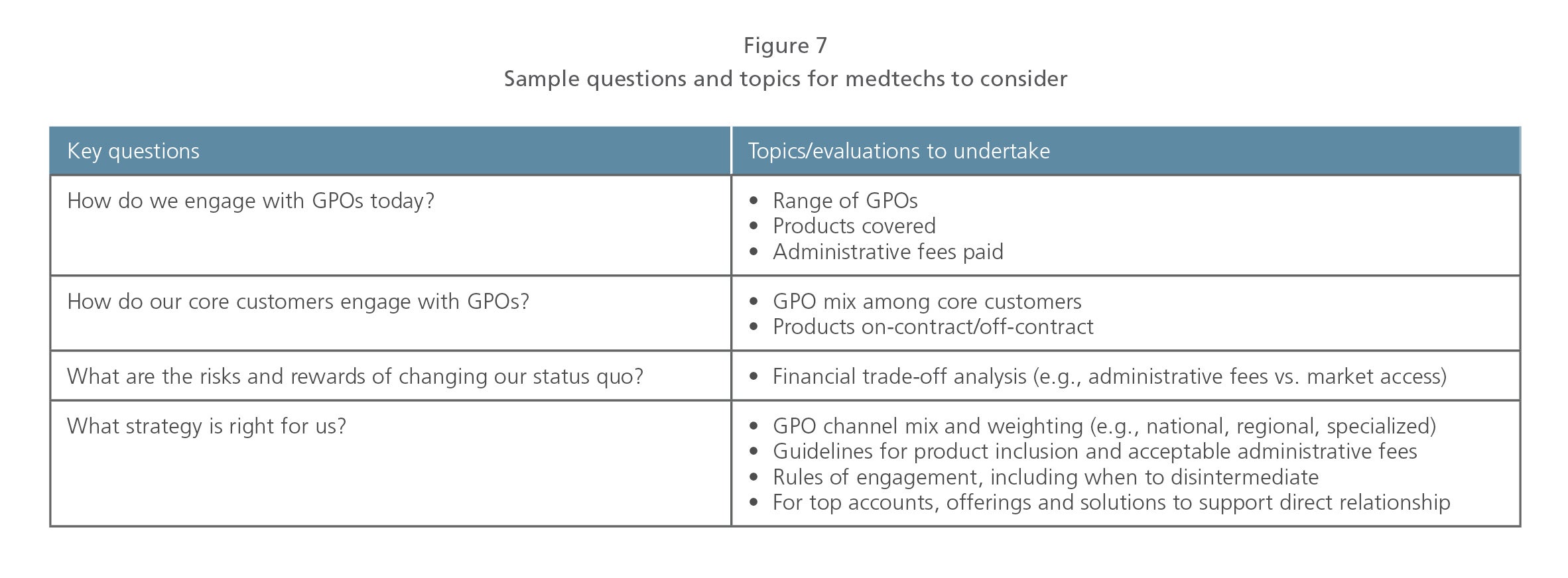

An initial framework to guide such an effort is outlined in Figure 7.

Traditional relationships between GPOs and medtechs are often perceived as one-sided. A key benefit of the changing market dynamic is the potential to rebalance these relationships. Although a degree of complexity can be anticipated in achieving such a rebalancing, we believe the market environment is now at a stage for medtechs to pragmatically and successfully reshape their GPO strategies.

04242019150411