Residential landscaping

Comparison to commercial landscaping

Residential landscaping shares several similarities with commercial landscaping, although with notable distinctions. Both sectors offer a range of services, from basic maintenance to design and development projects. However, market dynamics differ; while commercial landscaping often involves larger projects with more equipment, higher capital expenditures and more experienced teams, residential providers cater to smaller-scale projects with quicker turnaround times and less upfront cost.

The demand for landscaping services in both sectors is influenced by the overall construction market, with growth being stronger during periods of increased construction activity. Additionally, water-efficient landscaping trends impact both markets, with a surge in water restrictions leading to a notable shift toward sustainable alternatives such as turf. As both sectors navigate challenges and capitalize on opportunities, the consolidation trend observed in commercial landscaping is also influencing the single-family residential landscaping market, albeit with distinctions based on project scale and service offerings.

Diverse landscape needs in residential settings

Single-family residential landscaping reflects the diverse needs and preferences of homeowners, ranging from basic lawn care and maintenance to elaborate landscape design and construction projects. Some popular trends include sustainable landscaping, low- maintenance solutions, outdoor kitchens and living spaces, and water-efficient landscaping. Common services offered by single-family residential landscapers include:

- Landscape maintenance and lawncare. Mowing, aeration, trimming, weeding, fertilizing, seeding, pest control, irrigation system maintenance, dethatching, soil testing, mulching, pruning, trimming, edging

- Landscape design and construction. Hardscaping (patios, walkways, retaining walls), softscaping (planting, mulching), lighting, water features

- Specialized services. Tree removal, snow removal, holiday lighting, outdoor fire pits and grills

Though ubiquitous, not all landscaping services are necessarily considered an essential service

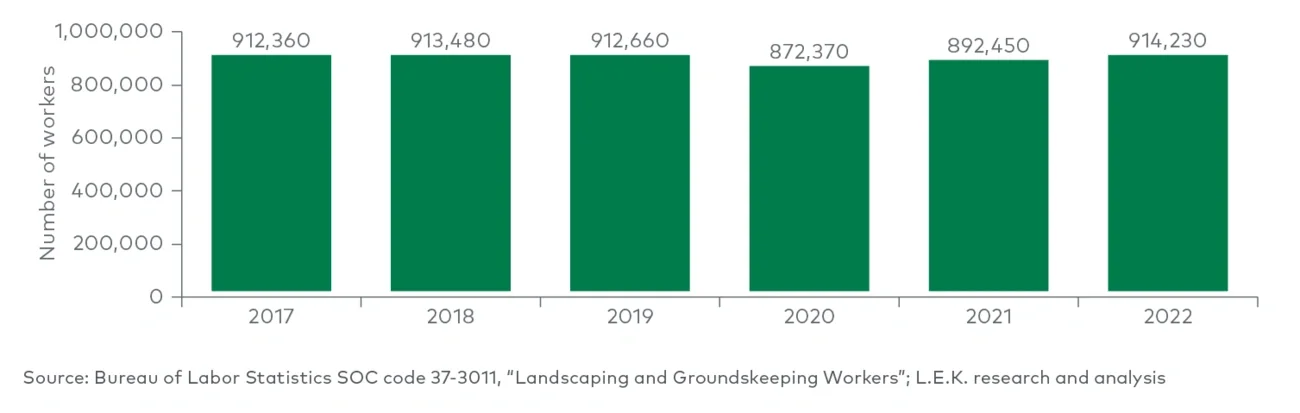

Landscaping demand growth typically follows that of the residential construction market and is stronger when new construction is stronger. During a recession, general landscaping maintenance is “stickier” than full-scale landscaping redesigns or redevelopment. Some homeowner associations and municipal governments also have requirements for residential lawns to remain below a certain height, supporting the market in downturns. Furthermore, lawn and landscaping services are the most common “do-it-for-me” services hired, with 43% of the population utilizing these services (per HIRI). This percentage is expected to rise as younger generations (who increasingly outsource services) move to the suburbs and rent or buy houses with more green space. These outsourcing trends, alongside a decrease in buying lawn equipment and supplies, indicate rising and enduring landscaping services demand over the long term.

Water restriction impact on residential landscaping

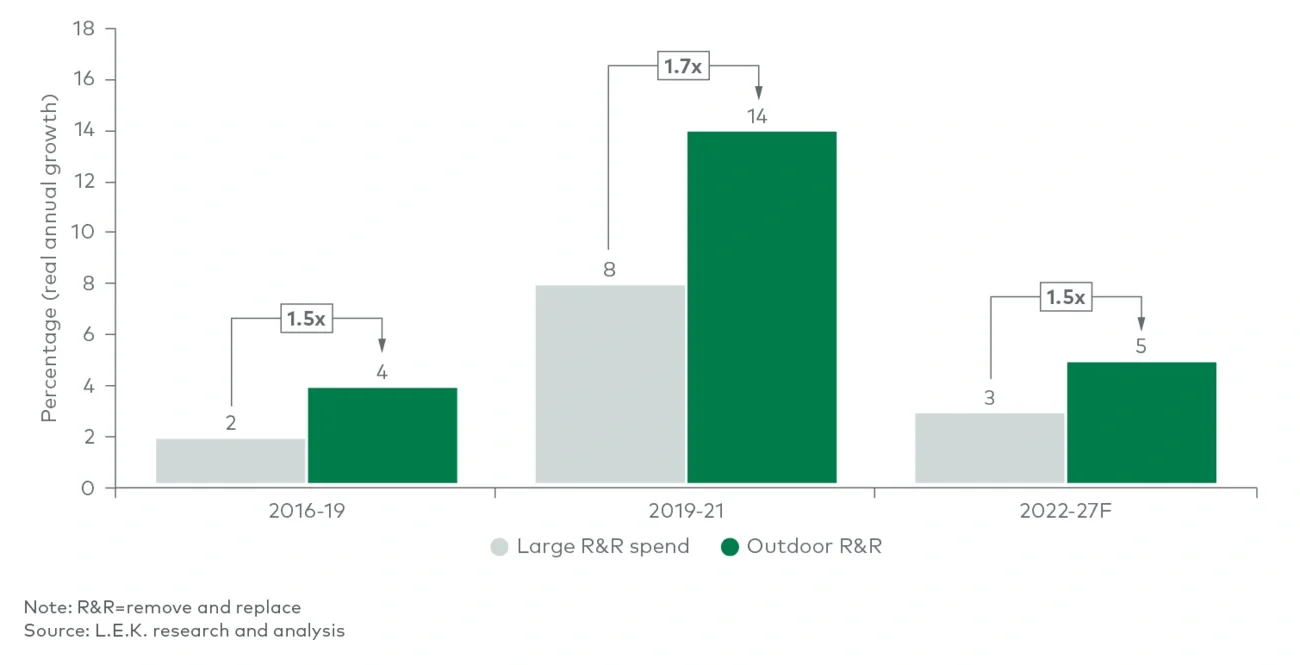

In addition to homeowner association and municipal government requirements, a surge in water restrictions has spurred a notable shift toward water-efficient alternatives for residential yards, with turf gaining prominence as a sustainable solution to conserve water. This shift can serve as a tailwind for landscaping companies, presenting a dual opportunity. While the installation of turf eliminates the demand for the traditional maintenance services that landscaping companies often provide for natural grass, it also opens a new avenue for landscaping companies to specialize in the installation of artificial grass. As water-efficient landscaping gains traction, the demand for turf installation as a sustainable solution is likely to grow, and farsighted landscaping companies can leverage this trend by offering expertise in turf installation.

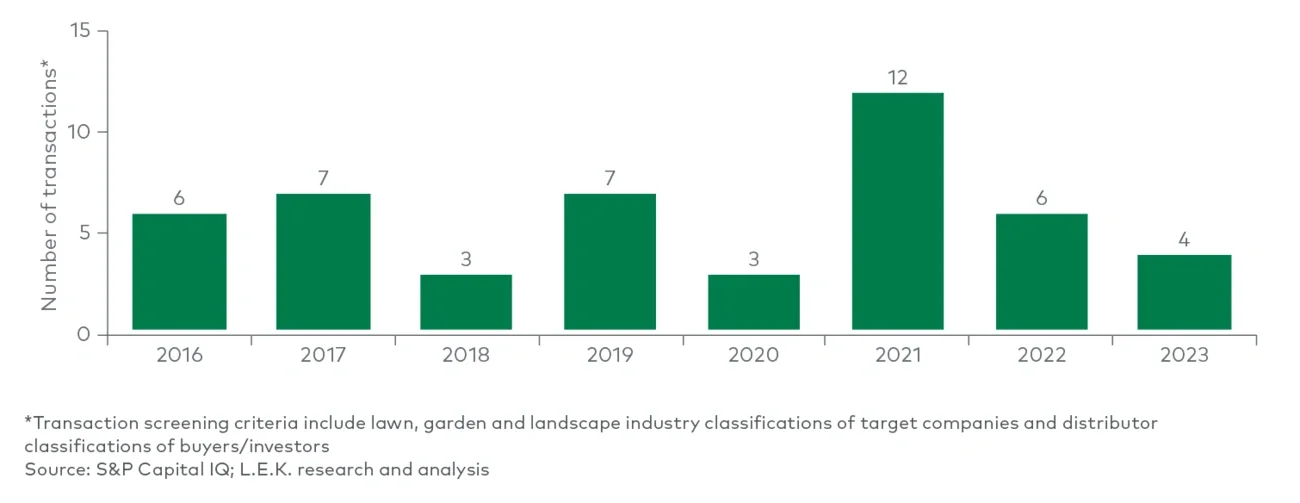

Consolidation of residential landscaping

The market for single-family residential landscaping services can be considered more fragmented than commercial landscaping is. Commercial landscapers often price larger projects served with more equipment and larger, more experienced teams. Single-family residential providers, by contrast, incur less upfront cost, given smaller-scale projects and less expertise required, and can begin servicing customers more immediately.

How to win

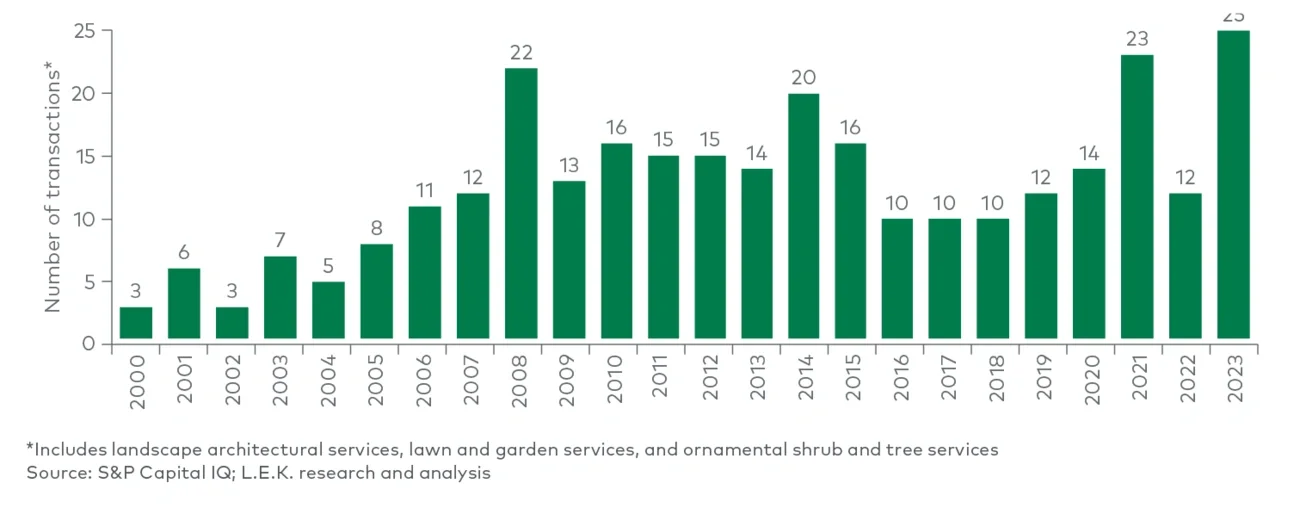

Winning in the commercial landscaping industry requires capitalizing on the benefits of scale and gaining market share. The growth of landscape maintenance is primarily a function of the footprint of commercial locations, which grows slowly. Landscape development, on the other hand, can experience fast growth, but it is a smaller part of the overall commercial landscaping market and is a function of new construction.

Commercial landscaping players that achieve scale through the breadth of services they offer, the specialization of their staff, and a greater geographical presence than the competition’s become more attractive and reliable partners than local players do. At the same time, acquiring local or smaller players (typically in new markets) as opposed to growing organically, and increasing payroll for the same number of laborers, gives larger players direct access to a labor pool. It can also help them grow their offerings as the industry shifts toward sole-source contracts and as clients seek comprehensive landscaping solutions. Businesses can acquire a larger breadth of landscaping services and can even venture into other development services such as planning and design.

That said, players that do win in this space need to figure out how to apply their scale to better serve small, local property owners in a way that provides homegrown, personalized service at a competitive price. On one hand, greater scale and density can enable a local provider to deliver that same service over time, while scale economics — namely density, purchase terms, use of technology for efficiency and more — have the potential to make larger players more competitive in the eyes of smaller commercial customers. And winners can find more-concentrated niches. For example, more than 90% of tree care work for the utility end market is performed by large companies.

The commercial landscaping industry has wrestled with myriad challenges in recent years, but demand for its services is returning, along with favorable trends and a more robust labor market. As the benefits of scale become increasingly obvious, the consolidation of this fragmented industry is poised to continue well into the future.

In the competitive market of residential landscaping, success hinges on a combination of adaptability, service differentiation and strategic growth. Winning residential landscaping companies can capitalize on their agility, offering personalized and local services that cater to shifting customer preferences. Embracing water-efficient alternatives such as turf and staying attuned to sustainability trends can position companies favorably in a market increasingly conscious of environmental considerations.

Moreover, fostering a strong local presence, efficiently managing labor and costs, leveraging technology for operational efficiency, and maintaining competitive pricing contribute to a winning strategy. As the residential landscaping sector experiences its own consolidation trends, companies that strike a balance between scalable operations and localized, customer- centric approaches are well positioned to thrive in this evolving market landscape.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Endnotes

1Nowak, David J.; Greenfield, Eric J. 2018. “US Urban Forest Statistics, Values, and Projections.” Journal of Forestry. 116(2): 164-177.