CPG manufacturers are currently facing a raft of macroeconomic challenges: Consumer elasticity has returned, concerns about operations as well as labor (specifically availability) persist, and manufacturing and portfolio complexity is compounding the effects of both.

But by optimizing their SKU assortment — and in the process, optimizing both their packaging and procurement — CPG companies can relieve margin pressure, improve operational efficiency and, by extension, reduce labor concerns to drive profitable growth of their respective overall brands.

With that in mind, L.E.K. Consulting has observed more than 20 large public CPG companies that have been embarking on portfolio optimization programs. While their individual reasons and goals may differ, their efforts make clear that before launching a strategic portfolio optimization program, there are some core questions every CPG company needs to answer in order to ensure the program’s success.

To start, let’s look at the current challenges facing brand owners.

How the post-COVID-19 economy is impacting CPG manufacturers

While price increases have been easy for CPG manufacturers to implement over the past few years, now manufacturers are either slowing them down or, in some cases, outright reversing them. At the same time, consumer elasticity is increasing, as evidenced by decreasing savings rates, the resumption of student loan repayments and the increasing number of 30-day credit card defaults, rising interest rates, and the reduction of government programs like SNAP, which are making consumers even less tolerant of price increases and have them looking for options to “trade down” or “trade out.”

Compounding the challenges for CPG manufacturers are operational concerns that have arisen due to the rapid shifting of packaging types (e.g., as food and beverage manufacturers converted production from foodservice packs to retail or to-go packs in 2020-21 and back to retail as in-person dining resumed) and channels (e.g., to ecommerce, foodservice), as well as record low unemployment (which makes finding employees difficult).

Meanwhile, innovation, which was deprioritized during the pandemic, has returned as CPG manufacturers seek to drive organic growth. But it has brought with it greater manufacturing and portfolio complexity driven by an increasing number of flavors and package sizes, as well as supplier/procurement complexity (i.e., more suppliers and vendors that need to be managed). In other words, that complexity stretches from end to end, from the customer all the way back to the supply chain.

Key levers CPG manufacturers can pull

To ease margin pressure, lessen supplier complexity and, in the process, reduce labor concerns, CPG manufacturers can implement:

- Portfolio optimization — This involves eliminating the SKUs that are less productive, difficult or time-consuming to produce, duplicative of other SKUs, or not profitable

- Packaging optimization — Harmonizing packaging types, materials, price packs, etc. across multiple SKUs/product lines will optimize their packaging

- Procurement optimization — A review of suppliers and formulations will enable manufacturers to consolidate suppliers and achieve procurement synergies, as will harmonizing ingredients

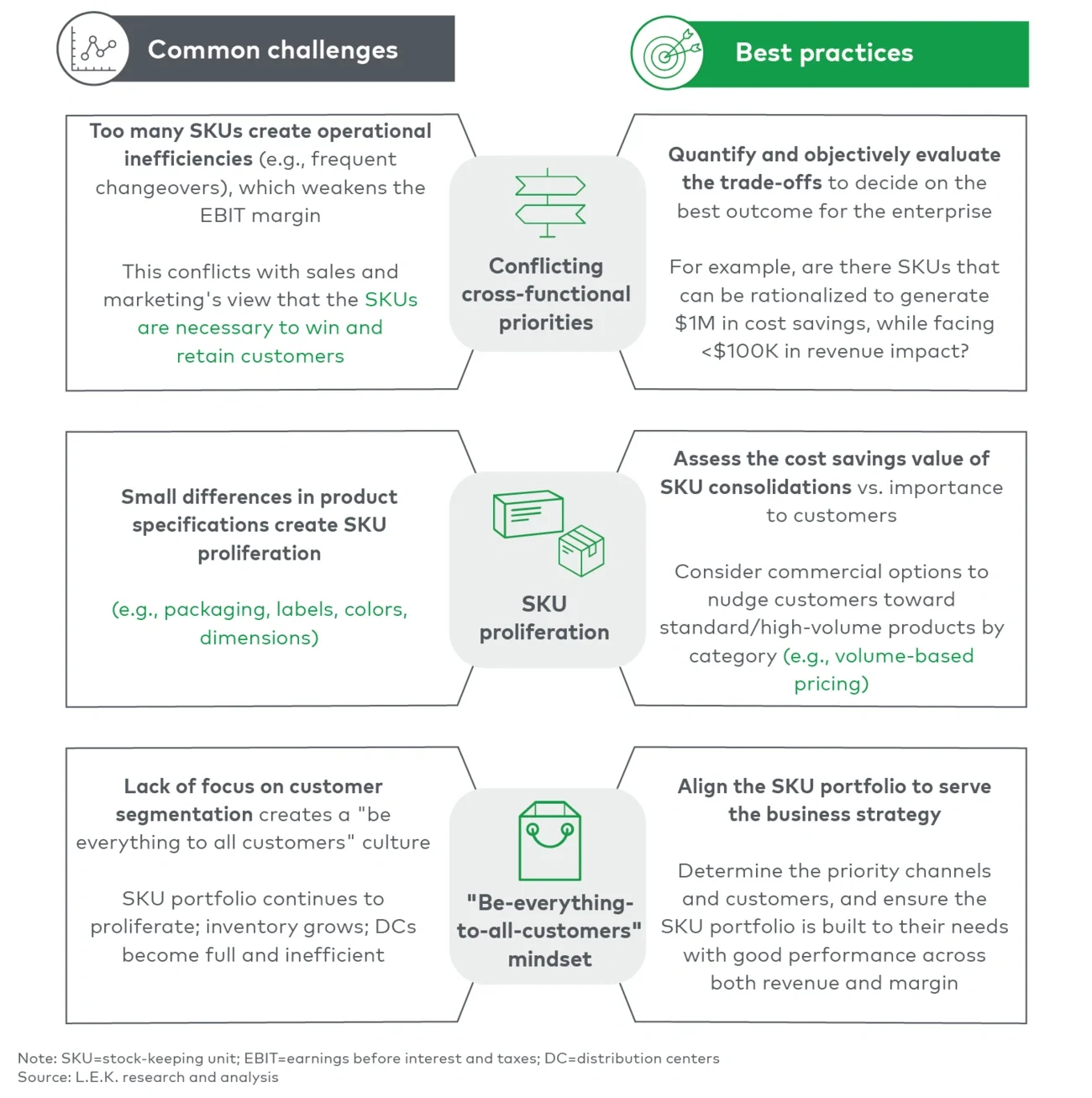

Each of these steps will help the organization, and its management, focus on “core” SKUs and return to profitable, operationally sound innovation.

From an operational standpoint, reducing SKU complexity and short runs will limit the time/machinery required for packaging and increase uptime but reduce changeovers. Procurement efficiency will improve due to the reduction in supplier count and order complexity combined with the benefit of additional volume discounts.

Logistics and inventory management costs will also fall due to the reduction in storage complexity, having fewer low-velocity SKUs in the warehouse, and the improved ease of shipping. And because there will be fewer SKUs to keep track of, CPG manufacturers will be able to improve resilience and service levels, resulting in improved levels of customer service.

Steps CPG leaders have taken

The portfolio optimization programs undertaken by some of the largest CPG companies demonstrate just how impactful such optimization can be. For example, in 2020 Kraft Heinz reduced some 20% of its SKU count to focus on high-growth SKUs, simplify its supply chain and increase its service levels. In 2021, Smucker’s set out to eliminate the 30% of SKUs that generated just 3% of revenue so it could focus on retail rather than foodservice and, in the process, better orient the organization toward its strategic goals. And most recently, in 2023, Hain embarked on a program to increase organizational focus, shelf space and brand awareness for its core SKUs by cutting 50% of its SKU count “long tail.”

In an analysis of the portfolio optimization efforts of more than 20 public CPGs, three core themes emerge:

- Driving distribution of core SKUs is the goal

- Operational efficiency is a key focus

- Systematic strategic optimization processes drive meaningful cost savings on an ongoing basis

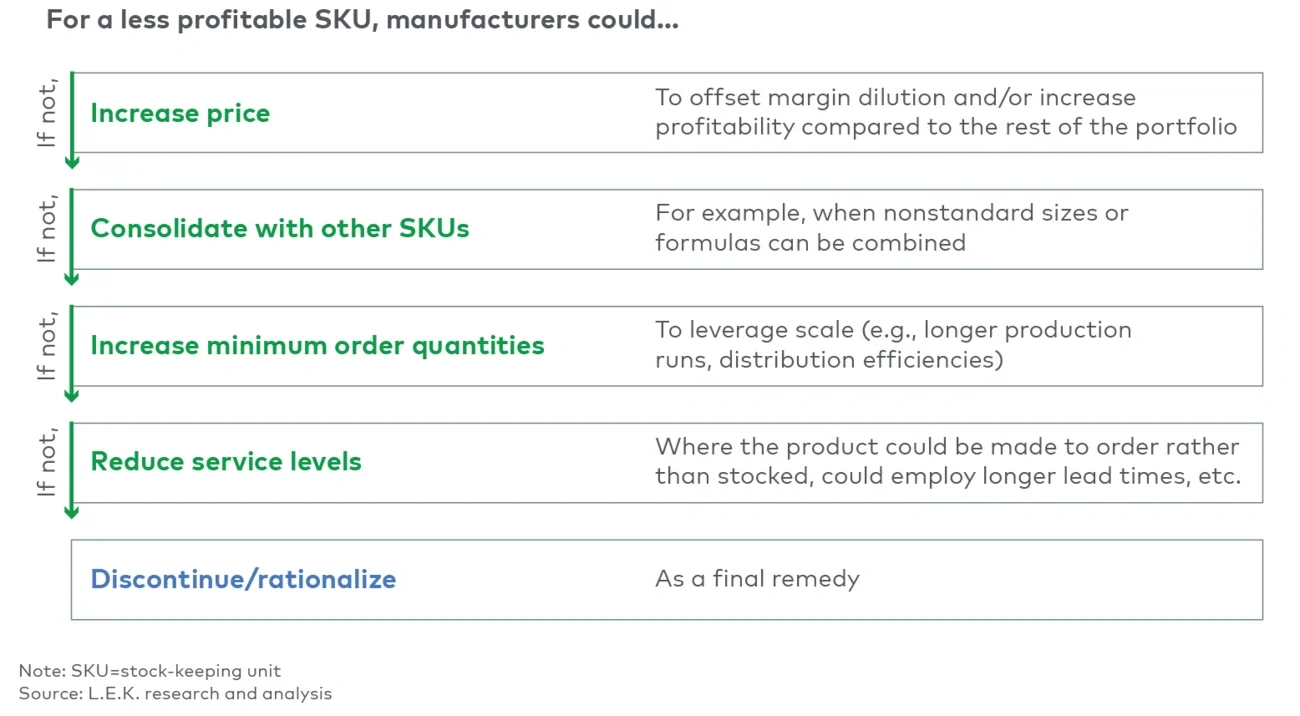

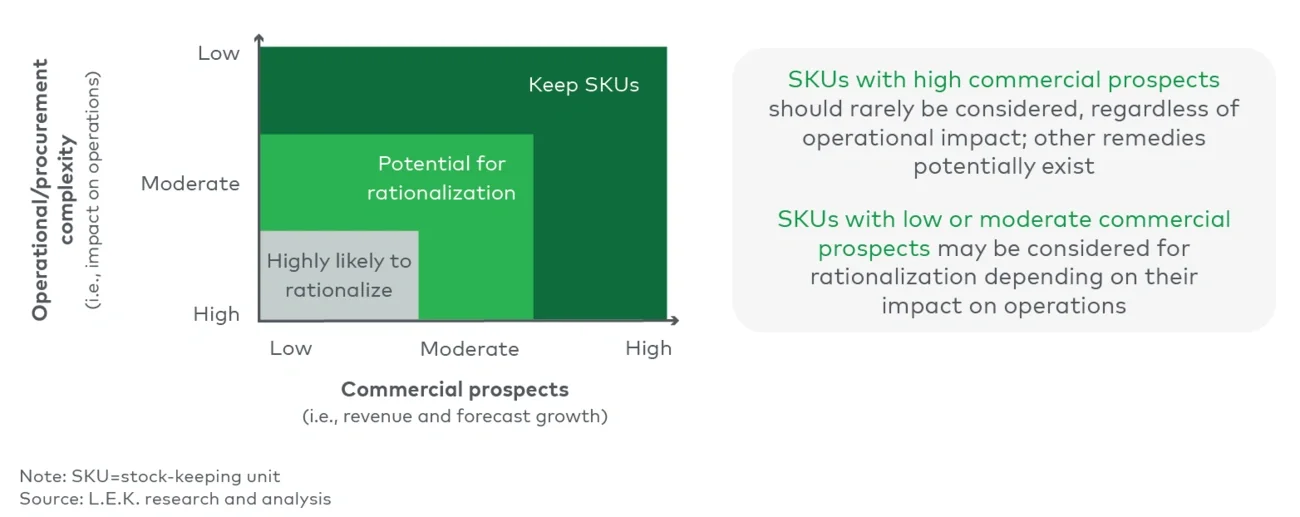

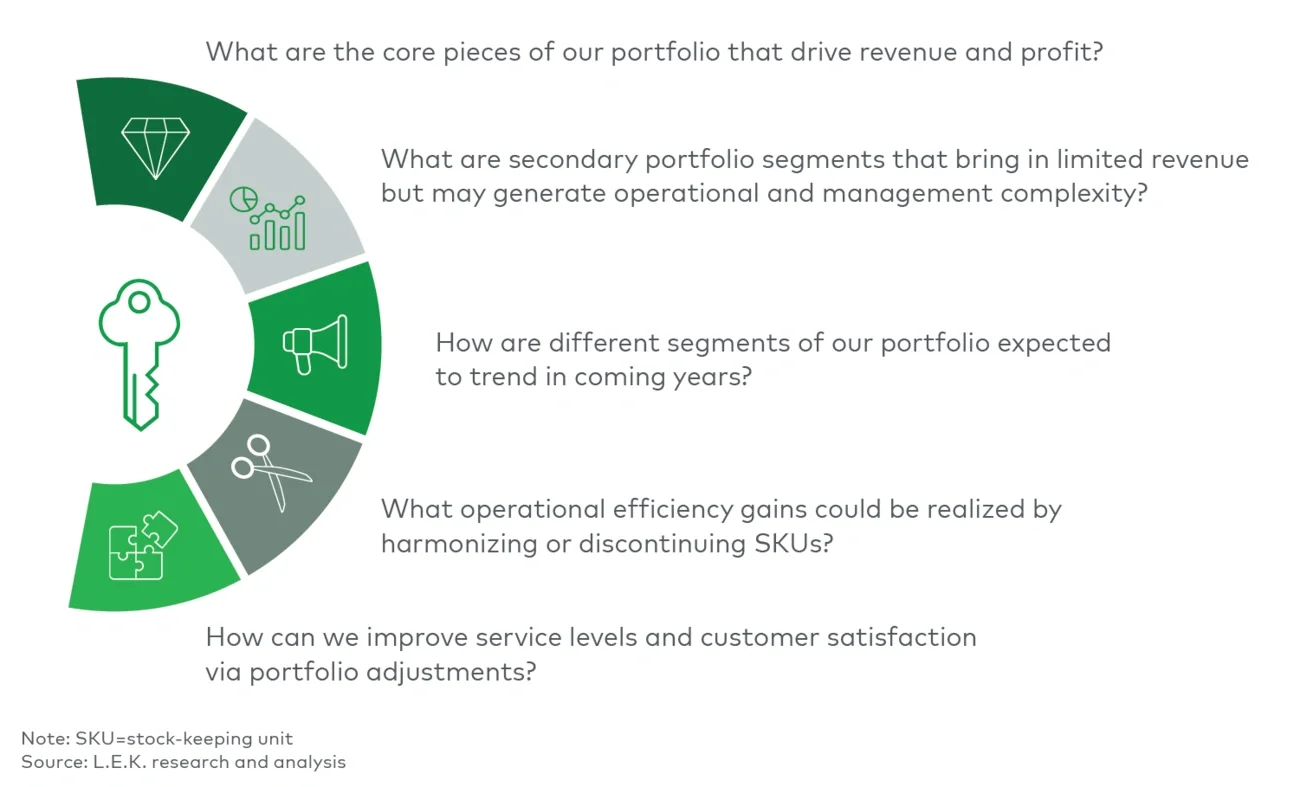

CPG companies should start by taking a holistic look at their portfolio, doing rigorous activity-based costing to identify the “true profitability” of each SKU and assessing whether SKUs that are less profitable have a strategic role to play in the broader portfolio.

They can take a number of steps to bolster their portfolios — namely, increase the price of less profitable SKUs, consolidate them with other SKUs, increase minimum order quantities and reduce related service levels. But as a last — or perhaps best — option, they could optimize their portfolio by discontinuing those SKUs (see Figure 1).