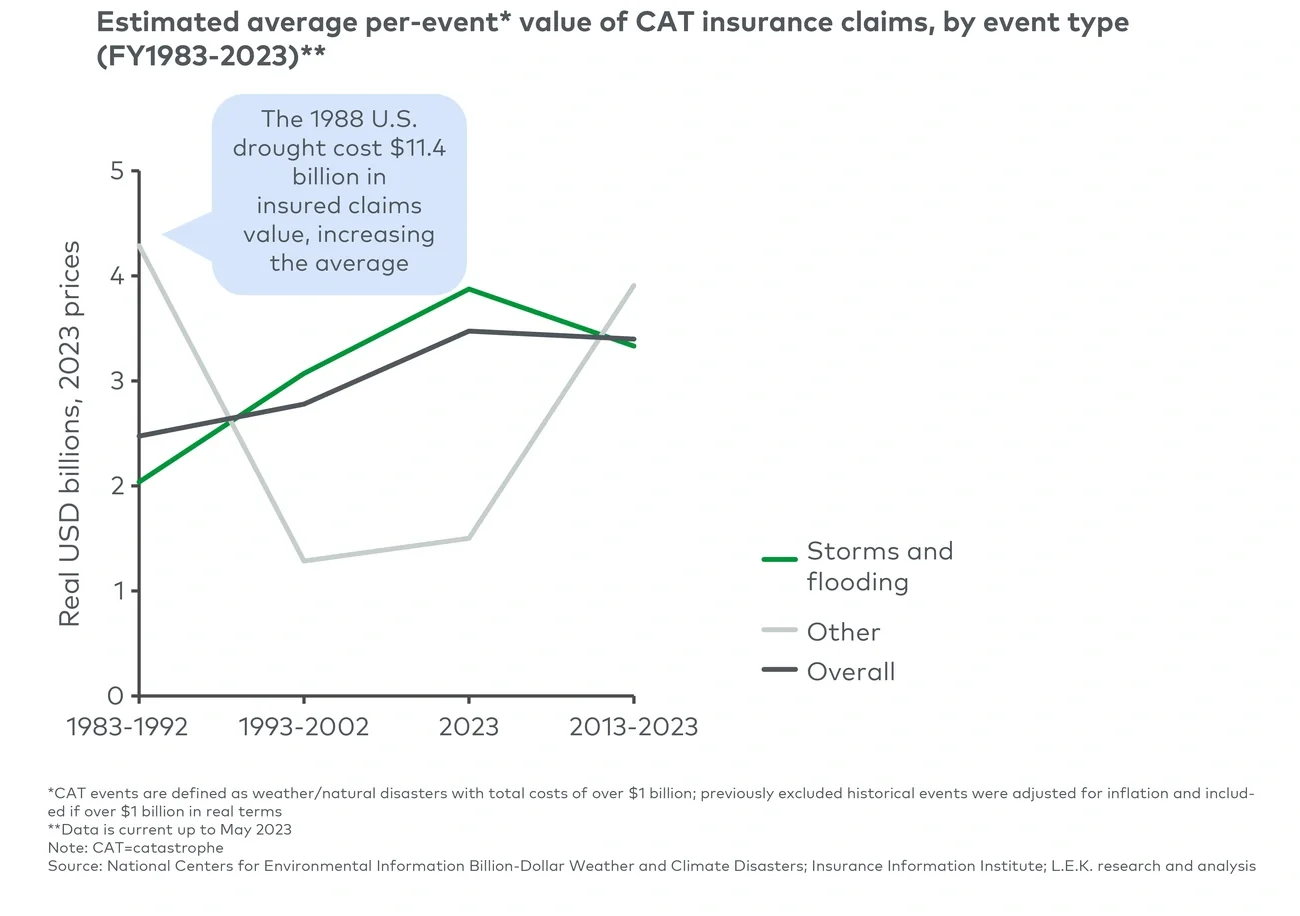

This trend is supported by L.E.K. Consulting’s analysis of demand for roofing shingles, which separates weather-driven demand from age-driven demand and points to an average annual increase of 0.7% for the former. This increase is broadly consistent with the growth of the installed base. Another factor that may increase the impact of CAT events is the growing population in coastal areas, where damage is often greatest. In short, episodic weather events provide an upside to players focused on the restoration industry.

Even a drop in coverage rates is unlikely to have a major impact on the industry

One potential risk to the restoration and remediation business is the possibility that the rising cost of insurance rates, in part due to the growing number of CAT events, will cause homeowners to forgo insurance altogether, leading to lower levels of coverage. Indeed, multiple states have raised rates since the start of the year, making this a risk that needs further evaluation. For instance, according to The Wall Street Journal, Arizona, Texas, North Carolina, Oregon, Illinois and Utah approved increases ranging from 20% to 30%.

Despite this, the rate of homeowners with insurance coverage has remained broadly stable as rates increase. The national average home insurance premium is estimated at $1,428, and although rates can be significantly higher in some states (e.g., Florida), many homeowners may still absorb higher increases. Moreover, even if coverage rates were to nudge down, many homeowners will still need to address water damage and mold regardless of whether they have coverage.

Claim No. 2: The sector depends on insurance relationships

Insurance providers play a key role in the renovation and remediation value chain. Therefore, understanding the insurance environment and the circumstances under which insurance companies will and will not pay for claims is critical for players in this space. It is also important for them to build and sustain local relationships with both insurance company loss adjusters and third-party loss adjusters. But the renovation and remediation ecosystem is a lot more complicated. Let’s explore this variability in greater detail.

When insurance influence is higher (commercial side)

National insurance channel partners (e.g., AIG, Travelers) often have a preferred vendor list or managed vendor networks with multiple providers across geographies (two to three per region) based on such factors as speed of arrival, responsiveness and overall customer service, time to completion, and breadth of service offerings. Often, large insurers formalize agreements with preferred vendors to establish pricing and ensure high priority for their policyholders in case of an event.

In situations where insurer influence is high, there are a number of ways for restoration players to distinguish themselves. For instance, because policyholders view the contractor’s performance as a reflection of the insurance carrier’s service, customer service and speed of arrival are particularly important to insurers when choosing preferred providers. Breadth of service offering is often a key differentiator because insurers want to minimize hassle for their policyholders and have one point of contact for the loss.

When insurance channel influence is lower (commercial side)

In other situations, the influence of insurers carries less weight. Commercial multifacility end users, in particular, are most likely to plan in advance of events and set up master service agreements (MSAs) with renovation and remediation providers. MSAs typically include response time guarantees, established pricing and performance standard metrics. Large national accounts usually have agreements with three to six providers, and selection tends to be contingent on immediate availability and proximity to the specific location in need of services. Commercial multifacility users are also continually seeking ways to centralize and streamline processes.

While insurance relationships are key, they are not the only set of relationships to manage. Restoration and remediation service providers can obtain leads and business from a variety of sources. For instance, within the residential subsector, specialty trades like plumbers and roofers may need to refer homeowners to a reliable provider for a service they do not offer, such as mold remediation. One survey found — consistent with other surveys and data sources — that providers use multiple lead generation methods, including referrals, adjuster and insurance company relationships, customer networking, and digital marketing, as effective approaches.

Claim No. 3: Restoration and remediation is an inherently local business, making scaled platforms a challenge

It is certainly the case that restoration and remediation requires many skills that favor locally based businesses, including a good understanding of local markets; strong relationships with referral partners, property management companies and homeowner associations (HOAs); access to skilled labor; and effective communication and responsive service capabilities.

But national models can also be successful and offer a number of benefits, not the least of which is the ability to serve national accounts effectively across their portfolio of properties. The field is certainly wide open. The U.S. building restoration market is highly fragmented, consisting of local or regional players that most often specialize in only one service or trade. Large vendors offering more geographic coverage and a variety of services are less common, but they are popular options for insurance companies looking to add high-quality providers to their preferred vendor networks. Nevertheless, the direct repair program model — in which insurers refer vendors to their customers — has only been adopted by insurance companies in the past decade, and remains somewhat nascent. Consumers choose to use a vendor from an insurance provider’s preferred network only 20% to 50% of the time.

Scaled players in this space also benefit from broad exposure that can drive higher brand recognition, win new customers and encourage repeat usage. They are also more likely to be attractive to recurring business entities such as HOAs that are looking for an end-to-end partner. This gives them the opportunity to interface with all the various stakeholders, referral partners and decision-makers to create a streamlined process for each project.

Given the variability in CAT events in any given year, as well as their size and short-term nature, large players are in a better position to quickly relocate staff and equipment to the area of need. The ability to mobilize an installed base of equipment nationally enables higher utilization relative to local players. Diversification across regions can also “smooth” demand across variable, localized events and needs.

Being able to provide multiple services across a broad geography allows remediation and renovation providers to capitalize on high-demand periods like CAT events, and it also makes them a more attractive partner for insurance companies. Their breadth of expertise gives them the ability to handle larger, complex jobs, such as technical restoration. They can also leverage shared services across branches and apply local or regional best practices across their entire network. Perhaps even more important, strong relationships with managed repair networks and suppliers give larger players priority access to equipment and improved price negotiating power.

Finally, large-scale players are more likely to benefit from cutting-edge technology. They can use it to dynamically assess damages or apply it to complex restoration situations (e.g., electronics replacement, semiconductor replacement, repair of machinery). For example, BELFOR, a national disaster restoration business, has a Technical Services business unit that specializes in the inspection, assessment, decontamination and repair of a range of assets, including machinery, equipment, electronics and semiconductor tools. This service offering spans applications and opens the door for larger, more complex jobs.

Ultimately, an ideal business model is one that combines the benefits of a small business — a performance culture, an equity holder with skin in the game, local relationships and local reputation — with the benefits of scale, including established systems, purchasing power and national/regional relationships, particularly with property owners of multiple facilities.

In this industry, the devil’s in the details

For more information, please contact industrials@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting LLC