L.E.K. Look Forward Into 2024, the European Perspective

With decarbonisation now a top boardroom priority and a major investment focus, creating a strategy that takes account of the complexities the energy transition brings is a commercial priority. L.E.K. Consulting partner Rebecca Scottorn takes stock of our recent global Energy Transition Study and looks forward to the energy transition trends to watch out for in 2024.

Look Forward to how the energy transition momentum is building

Building a clear picture

Building a clear picture of current energy transition (ET) dynamics in the industry is an important priority for us here at L.E.K. Now in its fifth year, our proprietary study plays an important role in informing our views and fueling key quantitative and qualitative measures that can be shared with our clients.

Our 2023 study focused on ET and decarbonisation trends facing the energy industry, highlighting how perspectives have shifted since the last study in 2022. This year, we added more perspectives from non-exploration and production companies, including utilities, renewables companies and investors, to help build an even broader picture. The scope of the 2023 survey is also more global, with more focus on Europe and Australia as well as the US.

During July and August of 2023, we canvassed 300 experienced energy executives from significant companies, and complemented these survey results with over 20 roundtable discussions with senior-level contacts, all with an interest or specialism in the energy transition. We focused on building an understanding of how capital is being allocated, the impact of the macro environment, and what ET means for organisational and investment models.

The evolving role of energy players

The role of energy players in the ET is evolving, with a challenging macroeconomic environment and energy security concerns driving a more cautious approach for some players.

Many have refocused on their core operations and are focusing on decarbonising current operations, with some challenges in investment in emerging technologies. This has been driven by high interest rates, energy security concerns and strong demand for traditional hydrocarbons.

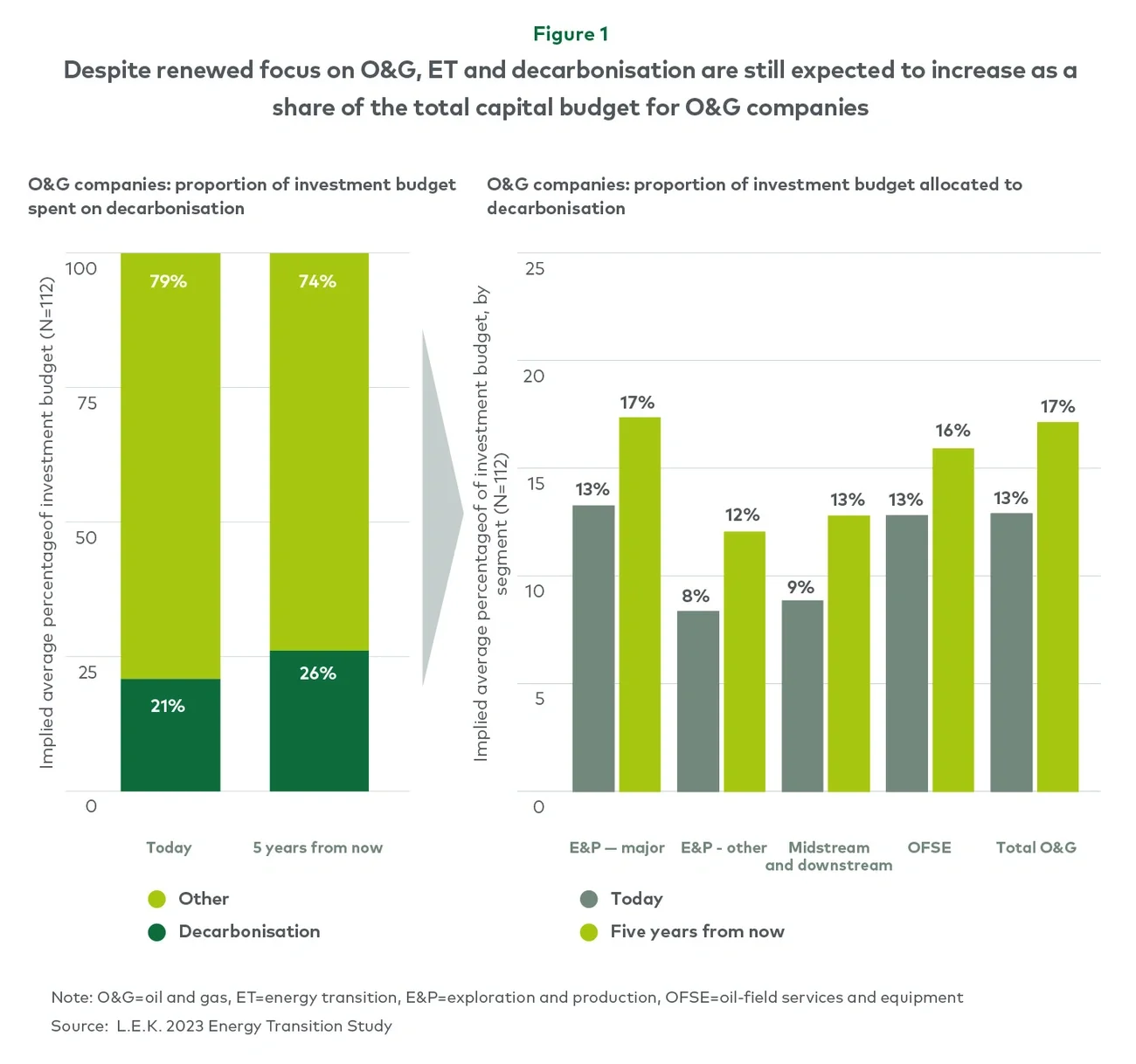

A refocus on oil and gas (O&G) assets is leading to more interest in decarbonising the hydrocarbons. O&G companies have prioritised reducing emissions, increasing energy efficiency and more accurately measuring their carbon footprint (see Figure 1).