With interest rates increasing rapidly throughout 2022 and 2023, it’s hard to open a newspaper without reading about the challenges facing the Australian construction sector. Recently, Porter Davis Homes was another established name in home construction to collapse, leaving around 1,700 homes in various stages of construction.

The traditional volume home builder model has been challenged over the past few years – volume builders sell houses on fixed price contracts and ordinarily deliver the homes within several months. Over the past few years, heightened demand for homes driven by government stimulus has coincided with supply chain disruptions, labour shortages and escalating inflation, which has resulted in builders taking longer to deliver completed homes and having to absorb significant price escalations while revenue (from fixed priced contracts signed 12+ months earlier) has remained static.

This got us thinking about whether it’s all bad news, or if there are reasons to have some optimism in today’s challenging market.

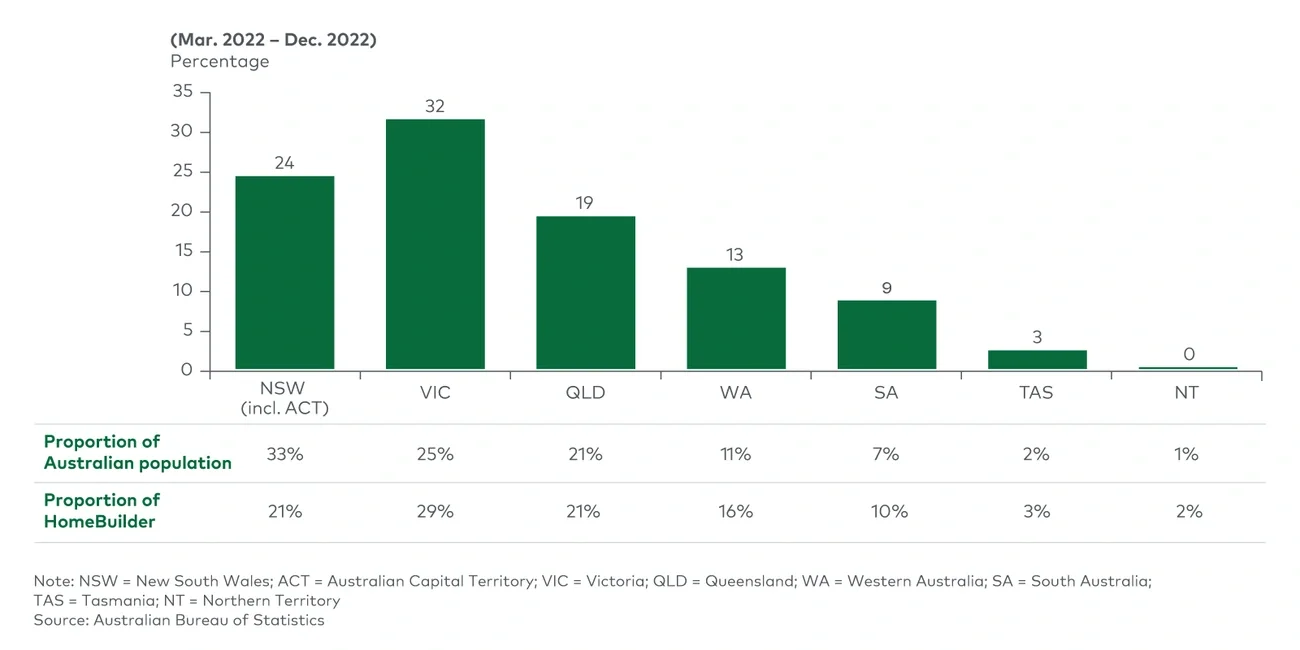

Victoria is a disproportionately large market for detached home construction, and downturns in home construction activity are therefore more impactful in Victoria

Victoria is home to around 25% of the Australian population, but its high rate of population growth and the expanding footprint of Melbourne and its surrounds support a much higher proportion of Australia’s detached residential construction activity.

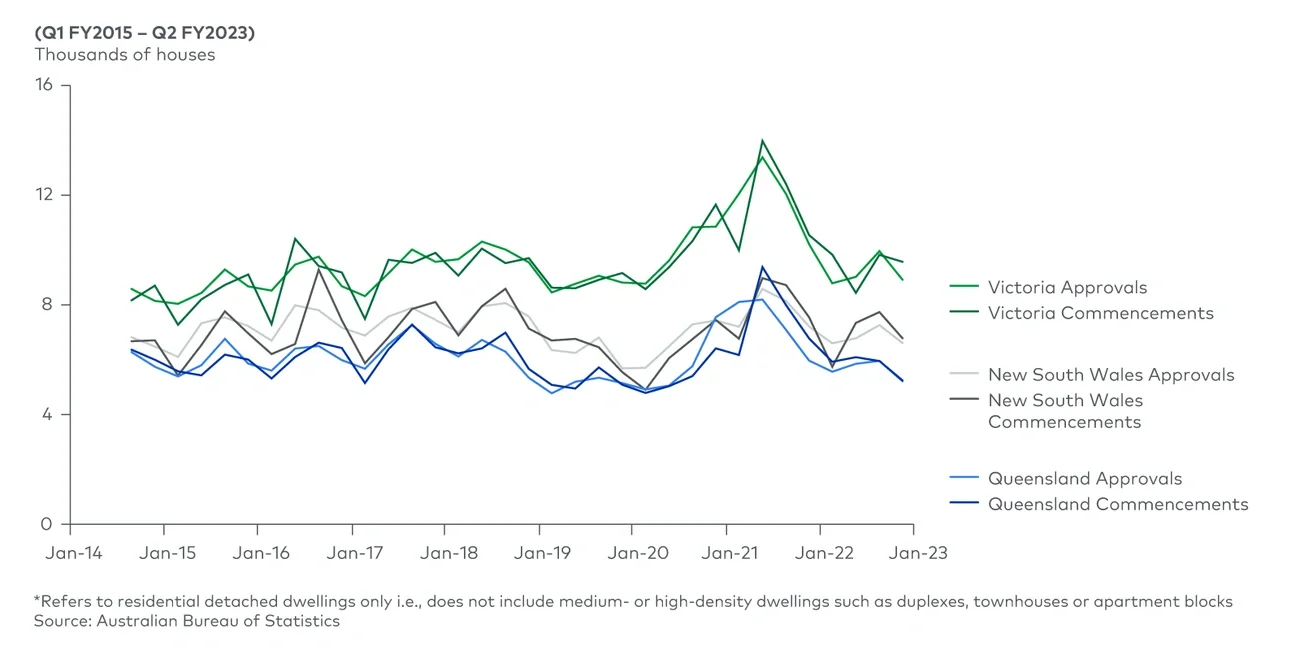

Victoria accounted for almost a third of all detached homes commenced from March 2022 to December 2022, consistent with building activity across states over the preceding five years (see Figure 1).