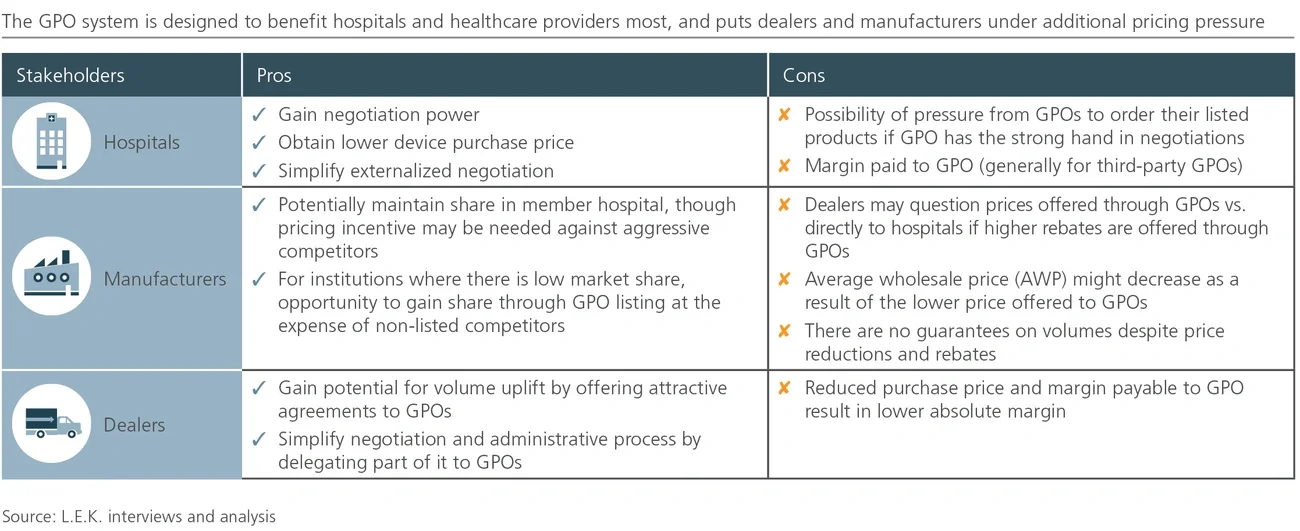

Traditional relationships between GPOs and medtechs are often perceived as one-sided, particularly in Japan where current GPO agreements do not guarantee volume commitments for discounts offered and are frequently renegotiated.

However, with the increasing financial pressures on the healthcare system in Japan and the associated increase in transactional purchasing behaviors in hospitals, hospital participation and demand for GPO services in Japan is expected to continue to increase. GPOs are expected to evolve their services as a means to deliver differentiated portfolios and greater value for their customers — with the emergence of, for example, regional-focused GPOs that provide services tailored to local needs and relationships, or specialized GPOs driving differentiated value via targeted product categories (e.g., consumables) and/or specialty-specific offerings (e.g., orthopedics).

In other markets such as the U.S., hospitals are increasingly relying on GPOs to help manage the complex system of purchasing, and GPOs have expanded their range of services to meet this demand. Beyond cost savings, GPOs offer services that include data analysis and benchmarking, innovative technology implementation, market research, and emergency preparedness and natural disaster response. GPOs also support hospitals in reducing medical errors by helping to standardize some of the product use in hospitals and educating clinicians on best practices.

Just as a one-size-fits-all sales model across hospital segments no longer suffices for medical device companies, nor will a single approach work for medtechs in their dealings with GPOs. Therefore, medical device manufacturers in Japan should consider the following action steps when developing their GPO strategy:

- Use GPO agreements to protect innovative products with low levels of competition or a distinct competitive advantage

- Identify GPOs where the hospital membership mix is likely to drive benefits to the organization, and to the extent possible, carve out agreements relevant to these accounts, including:

- Accounts where the organization currently has a low market share in products appropriate for GPOs, and where GPO participation would enable the manufacturer to access the account and key decision-makers in order to drive volume gains

- Accounts that constitute the long tail of the demand curve, which tend to be hospitals with a lower degree of centralized purchasing and smaller respective volumes; for these customers, the traditional GPO model offers both providers and medtechs value as well as efficiencies

- Identify accounts where there are strong relationships with senior clinicians likely to be involved in the GPO provider selection process, and leverage these connections to support listing

- Create commercial capabilities to support the organization in negotiations with GPOs, to ensure pricing and participation decisions — including financial analysis and business case development, monitoring and tracking of contract performance, contract negotiations, and ongoing GPO intelligence — are well informed and consistent across the organization

- Develop guidelines for product inclusion and acceptable discounts to ensure consistency across the organization

- Monitor the GPO landscape to identify new and emerging GPOs that might be focused on specialty or product categories aligned with the portfolio of the organization, and engage with these organizations early

- Identify opportunities in large accounts to develop direct partnerships that marginalize the role of the GPO and that provide greater opportunities to maintain share without paying GPO margins

- Partner with GPOs that are expanding their service offering beyond traditional price negotiations, and identify opportunities to work together (e.g., on reducing medical errors)