In the 1980s, one of the world’s fastest supercomputers, the Cray-2, cost around US$30 million1, weighed 2,500 kilograms, consumed 195 kilowatts of electricity and had a 900-litre liquid cooling system. Today, an Apple Watch has similar processing speed, but costs only around US$500, weighs 30 grams, runs all day on battery power, has sensors that can run an electrocardiogram (EKG), is connected to the internet, makes phone calls and always knows where it is thanks to GPS. This development took 30 years, but due to exponential acceleration, advances of a similar magnitude will soon take only three years. Given the exponential rate of change, companies and their leadership have to continually reinvent themselves to survive.

Executive Insights

Riding the Digital Health Wave: The L.E.K. Digital Excellence Framework

Riding the Digital Health Wave: The L.E.K. Digital Excellence Framework

November 4, 2020

Key takeaways

The healthcare sector has lagged behind other industries when it comes to the impact of digital technologies, but this is changing rapidly.

New products and services aim to diagnose sooner and more effectively, improve treatment, cure and manage diseases, increase system efficiency, improve access and convenience, and prevent disease onset.

L.E.K. has developed the Digital Excellence (DEX) framework to help companies navigate the complex challenges of becoming more digital, based around five key areas: Reimagining strategy, reorganizing the business, rebuilding infrastructure, refocusing on customers, and reinventing the business model.

Companies should not wait to act. Digital leaders outperform laggards by a factor of five to seven times in terms of revenue and/or valuation growth over a two-to-three year time frame.

Seismic change hits healthcare

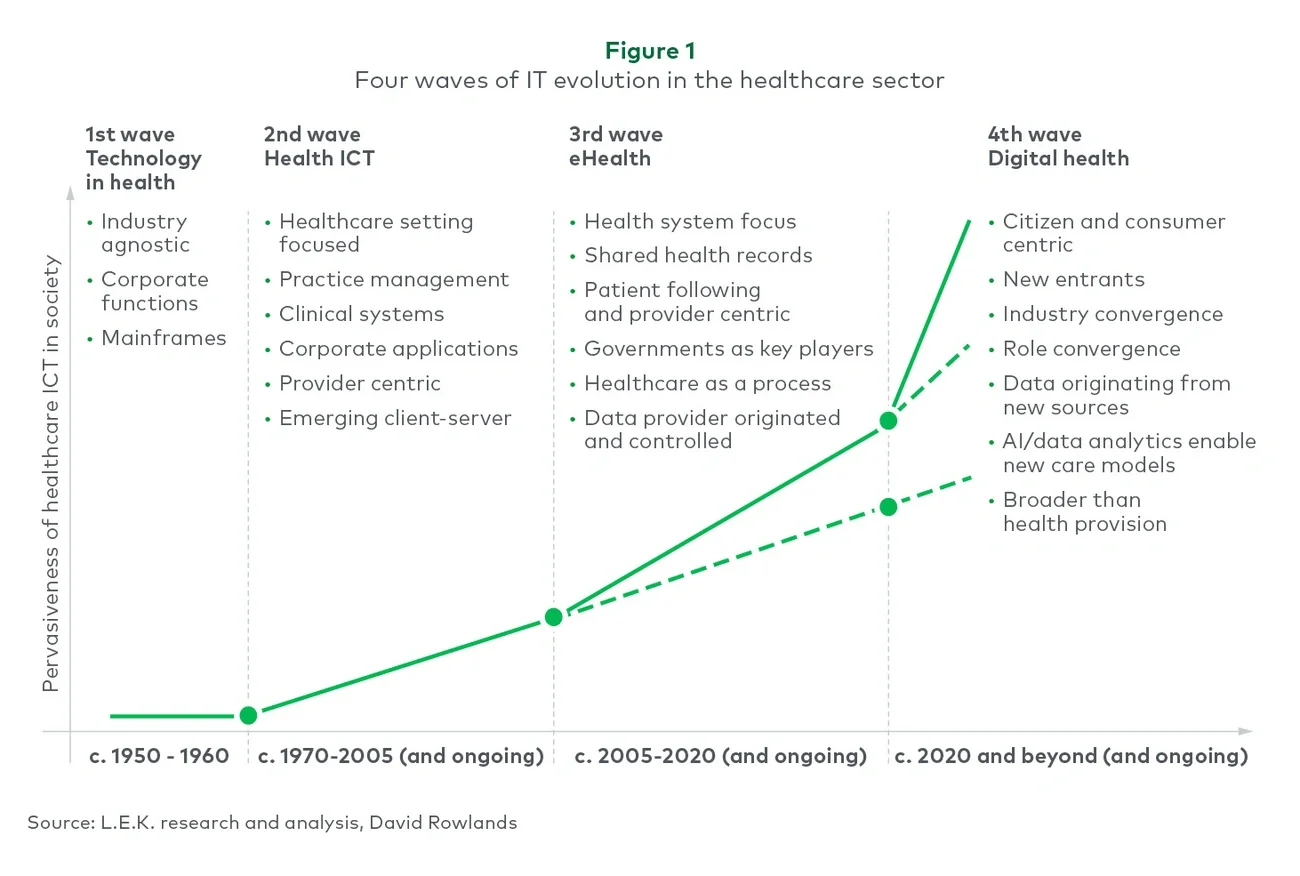

The healthcare sector has lagged behind other industries when it comes to the impact of digital technologies, but this is changing rapidly. Private companies and the public sector are investing heavily in digital health, often referred to as the ‘fourth wave’ of the healthcare technology revolution (see Figure 1).

Image

This fourth wave is characterized by rising consumer expectations derived from experiences with consumer technology leaders such as Facebook, Amazon, WeChat, and Google, the ubiquity of mobile devices and a host of new digital technologies, including apps, cloud computing, blockchain, data analytics, quantum computing and artificial intelligence (AI). The main aims of new products and services enabled by these technologies can be summarised into six categories:

- Diagnose and triage earlier and better

- Treat more effectively

- Cure and manage disease

- Flatten the cost curve and increase system efficiency

- Increase access and convenience

- Encourage healthier lifestyles and prevent disease onset

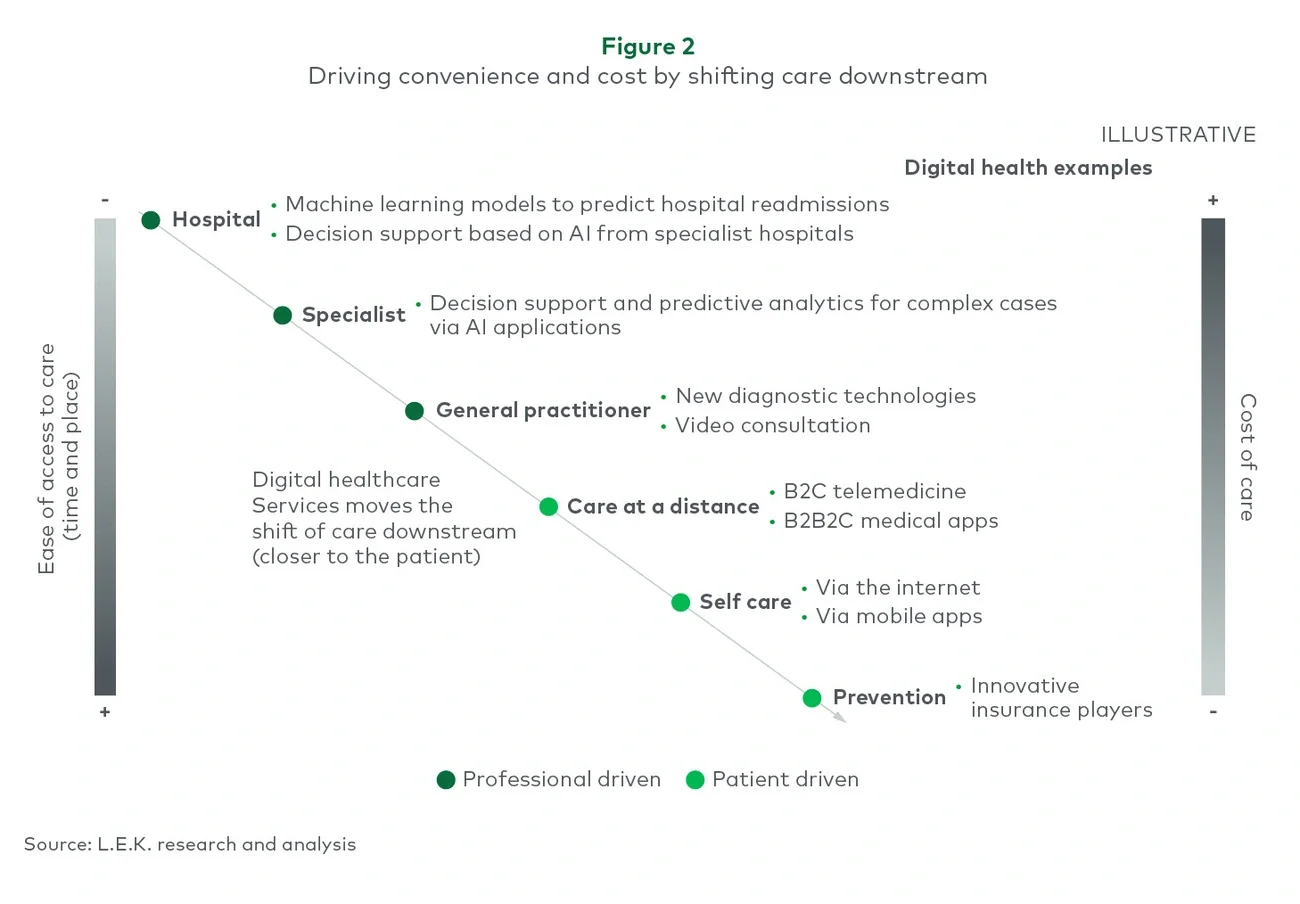

New offerings often meet multiple objectives. For instance, as technology capabilities increase, products and services can be shifted to lower-cost care settings, such as patients’ homes and pockets. This, in turn, increases convenience, and often quality.

We call this ‘shifting care downstream’ — from hospitals to clinics, general practitioners (GPs) and ultimately patients — and it comes in various forms (see Figure 2). At the complex end, specialist solutions — such as IBM’s Watson for Oncology or RapidAI for stroke care — enable less specialized hospitals to have AI-powered assistants to provide advanced decision support for their medical staff. At the other end of the spectrum, a number of technologies move care very close to the patient. Ada, for instance, is an AI-powered symptom checker that can remotely identify a host of common and rare diseases, instead of requiring a vulnerable or potentially infectious patient to go to a clinic or waiting for a general practitioner to become available. It is available for patients to download and use free of charge. China’s PingAn Good Doctor already has three million monthly paying users, leveraging digital technology to achieve levels of productivity per clinician that are unthinkable in traditional healthcare settings. In other examples, six-lead EKGs and urinalysis can now be carried out in your home using new sensors and analytical technologies. Even clinical trials are being virtualised so that some patients rarely see a clinician, despite using an experimental therapy. Not all conditions or diseases will be able to be treated remotely, but the trend is clear.

Image

An influx of capital

It is still early days in the evolution of digital health, but already a vast number of companies with no history of operating in the healthcare sector are investing heavily. They are drawn by the projected growth of the global healthcare industry to US$12 trillion in 2022 — up from US$8.5 trillion in 2018 driven by a global population that is becoming older, wealthier and more in need of all that the sector has to offer.

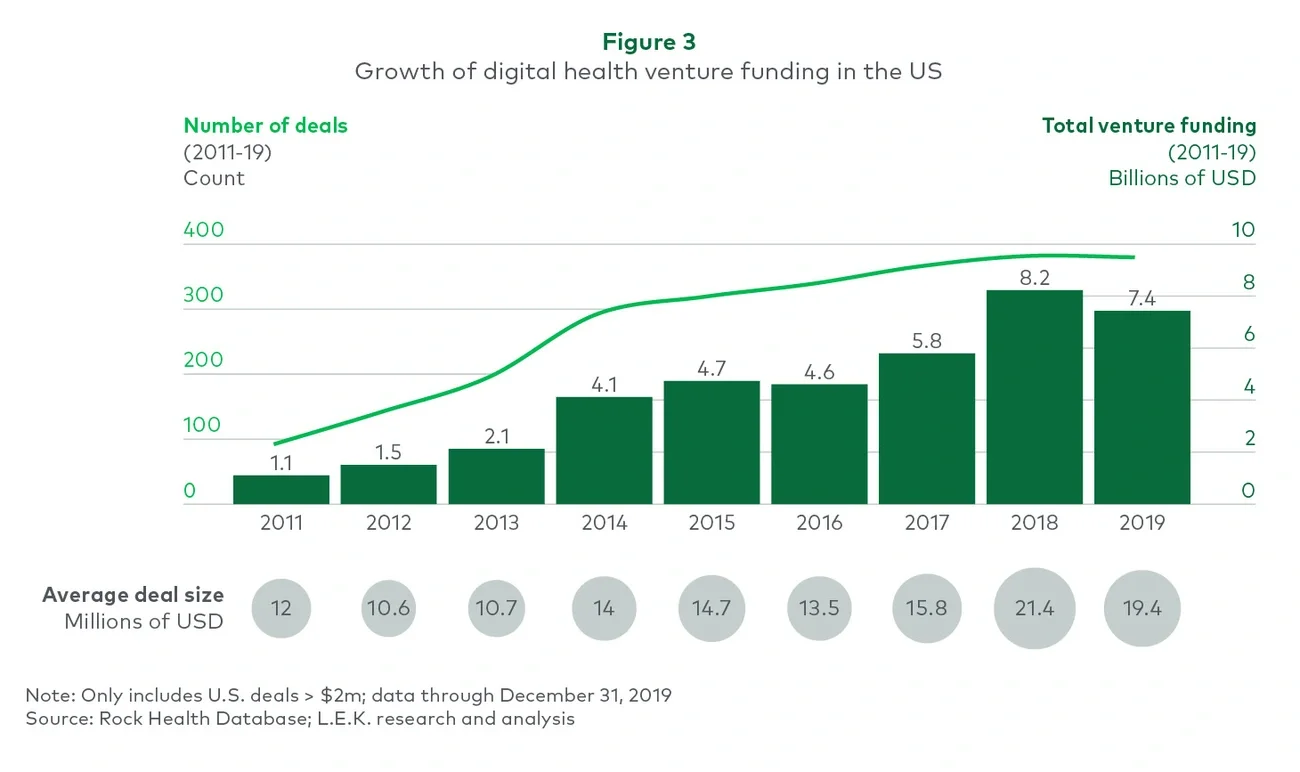

Over the past decade, entrepreneurs have seen investments in their digital health start-ups rise dramatically. In the US, total venture funding rose from US$1.1 billion in 2011 to US$7.4 billion in 2019, with the average deal size increasing to US$19.4 million, up from US$12 million over the same time period (see Figure 3). Even by the end of Q3, 2020 has already broken the record set in 2018.

Image

The traditional healthcare sector players — pharmaceutical and medtech companies, insurers, and healthcare service providers — are facing mounting competition from start-ups. One of the larger mergers (US$18 billion) in recent years took place between two relative newcomers, Teladoc (founded in 2002) and Livongo (founded in 2008). PillPack, an online pharmacy founded in 2013, was acquired for US$750 million by Amazon in 2018. Doctolib, a booking service and telemedicine platform founded in 2013, had a US$1 billion ‘unicorn’ valuation only six years later.

Meanwhile, many of the tech giants, including Amazon, Google, Tencent, Ant Group and Apple, see the healthcare sector as an attractive opportunity for expansion. In the words of Apple CEO Tim Cook, ‘If you zoom out into the future, and you look back, and you ask the question, “What was Apple’s greatest contribution to mankind?” It will be about health2.’

Legacy health sector participants are worried about the threat of start-ups and technology companies, with boards and CEOs increasingly asking questions such as: “What should we focus on to best defend our business?”, “Is our strategy digital enough?”, “How can we get a more digital valuation?”, “Are we moving to digital fast enough?”, “How do we best transform our culture and business to digital?” and “How can we establish a digital mindset amongst our employees?”

To help companies answer these and other questions, L.E.K. has developed a Digital Excellence (DEX) framework.

The L.E.K. Digital Excellence (DEX) framework

The DEX framework is designed to help companies navigate the complex challenges of becoming more digital. Their management, boards and investors can use the framework in a variety of ways, including:

- Guiding digital strategy and business case development

- Reviewing digital aspirations and priorities

- Conducting digital readiness self-assessments — for example, via L.E.K.’s Digital Health Index tool

- Adding an important element to the due diligence process when evaluating M&A opportunities (both buy- and sell-side)

- Supporting longer digital transformation engagements

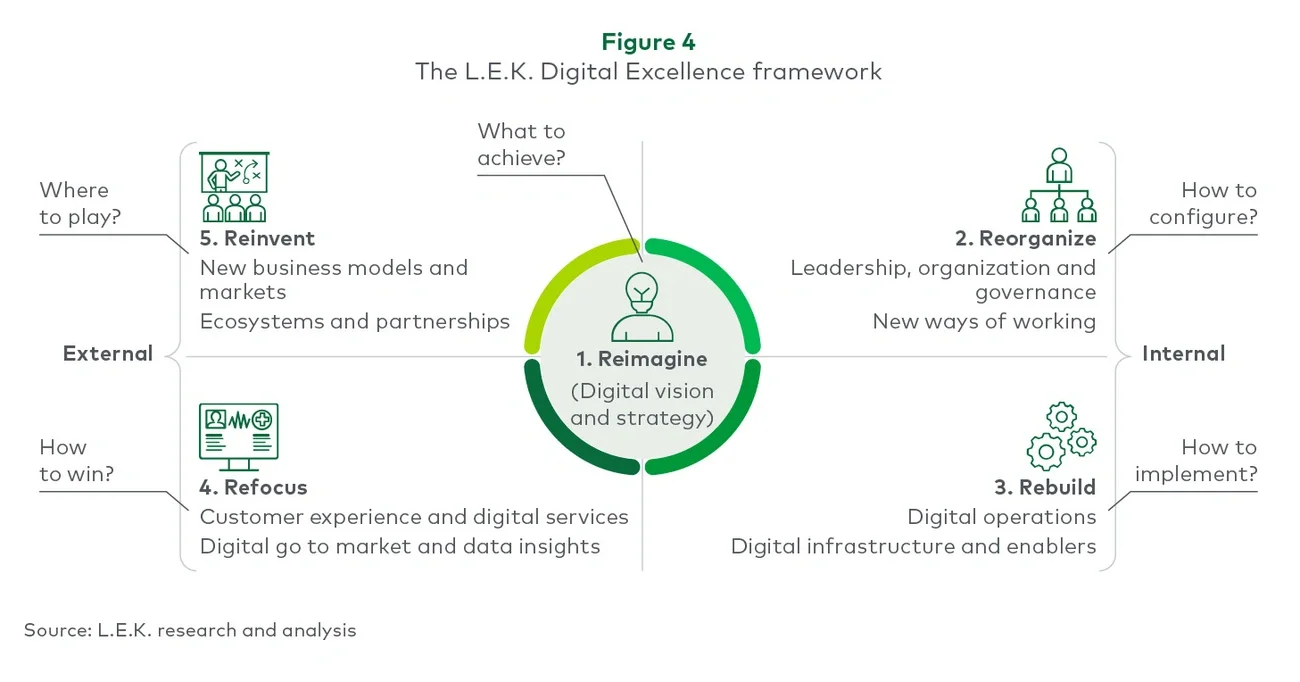

Based on our experience and research, we see five key areas underpinning digital excellence for healthcare companies (see Figure 4):

- Reimagine — developing a digital strategy

- Reorganize — building a digital organization

- Rebuild — establishing a modern digital infrastructure

- Refocus — developing a relentless customer focus

- Reinvent — continuously renewing business models

Image

The typical strategy cascade begins by asking the questions about ‘where to play’ and ‘how to win’ — enabled by new business models and relentless customer focus — while the next question of ‘how to configure’ is answered with infrastructure and organisational changes.

Reimagine

First, companies must reimagine their business for the digital age. Already, big tech companies are reimagining themselves as healthcare businesses. The traditional healthcare companies must do the same with respect to technology, adopting a tailored digital vision, strategy and implementation plan. For example, companies from pharma and medtech heritages are building virtual clinics via telemedicine, while established service businesses are establishing a ‘digital twin’ of their business by creating a software duplicate of their operating model. This can help them expand globally without requiring physical infrastructure, much like Uber creates a global service experience with the drivers and vehicles always being local.

Amazon has embarked on a healthcare-focused expansion strategy. One key element is entry into the online pharmacy space by offering drug deliveries, a natural extension of their mail order model. To implement this strategy, they acquired PillPack for US$750 million, breaking into the US$500 billion prescription medicine market.

Reorganize

Companies must reorganize their business. They need new capabilities to drive innovation, digital and culture change, and to offer better customer experiences. This often involves creating new leadership roles such as a chief digital officer and/or a chief experience officer and implementing new ways of working: continuous innovation, design thinking, agile development, and the close coordination of development and operations (devops). Studies3 show that these approaches, taken together, can double productivity, shorten time to market, significantly increase quality and customer satisfaction, and greatly improve return on investment.

Polpharma created a new chief digital officer role and launched a ‘digital community’ and supporting collaboration tools to enable new ways of working throughout the company. Cleveland Clinic, one of the top hospital systems in the United States, has embarked on an agile transformation, with new working practices. For example, they have gathered together teams of clinicians to create social contracts, take part in biweekly retrospectives, and plan their work and deliverables as a group, supporting them with mobile apps and wireless internet of things4 (IoT) applications.

Rebuild

Companies must rebuild their operations and infrastructure to maximize the benefits of digital technology. This includes looking at ways to harness digital to further standardize, automate, and enhance front- and back-office core operations. In parallel, companies must support these new paradigms with appropriate digital infrastructure and enablers. This could include building data repositories to train AI, partnering with digital agencies, and selecting developer and cloud platforms (e.g. Apple, Amazon, Google, Microsoft, IBM).

Novant Health, a US-based multistate hospital and outpatient network with more than 600 locations and five million patients, recently announced the migration of its Epic electronic medical record system to an enterprise cloud infrastructure. The move is designed to enhance business agility while reducing costs.

Refocus

Companies must refocus their business on an optimal customer experience and digital services, and continuously seek to eliminate pain points, whether they are operating in the B2C or B2B world. This requires digital go-to-market mechanisms and data insights. A key differentiator is being able to offer a better customer experience at an equivalent, or ideally lower, price point. Creating data analytics capabilities, partnering with digital agencies and creating in-house design centres are just some of the approaches that many companies are currently implementing.

The Royal Children’s Hospital in Melbourne, one of Australia’s top medical centres, has created an award-winning mobile app (Okee in Medical Imaging) designed to help children overcome their fear of undergoing an MRI scan. The result is a superior customer experience for both children and their parents.

Reinvent

Companies must reinvent themselves with new partnerships that allow them to build and participate in emerging digital ecosystems — loose networks of companies, suppliers and other stakeholders. New business models and markets need to be evaluated. These might include leveraging the crowd economy (e.g. linking patients to one another or with healthcare professionals), the free data economy (i.e., providing free services to one customer group that are paid for by third parties), the smartness economy (e.g. AI as a service) or the subscription economy (i.e., paying for a digital service on a monthly or annual basis).

Memorial Sloan Kettering Cancer Center, the largest and oldest private cancer hospital in the world (founded in 1884), partnered with IBM to create a digital twin that uses AI to duplicate its cancer practices. That software is now in use in more than 200 hospitals across Asia, significantly expanding the hospital’s business footprint and data capture. Qantas, Australia’s flagship airline, collaborated with insurance provider NIB to create a health insurance company that uses a well-being app and allows customers to earn frequent flier points for activities such as walking, running and cycling.

Tencent, the maker of WeChat — a platform with 1.2 billion monthly active users — has made investments and alliances across the digital health spectrum with Chinese and international businesses such as DXY, Babylon, Medlinker and ZhongAn insurance amongst others.

Roche has publicly announced partnerships with Flatiron, Syapse, GNS Healthcare and Owkin in AI alone.

Taking the temperature of companies’ digital health

The first questions for businesses beginning a digital transformation are always “How ready are we?” and “What should we do next?” L.E.K.’s DEX framework provides business leaders with a way of evaluating their organizations’ capabilities — and those of their rivals. So, how does this model work in practice?

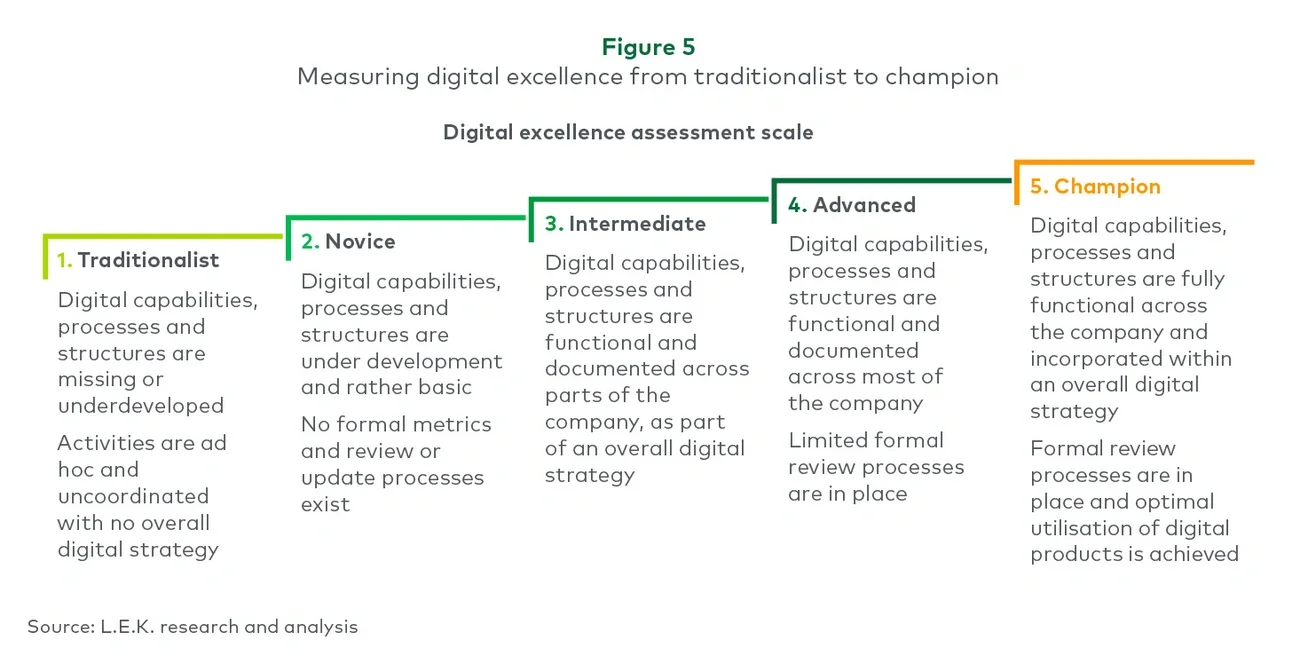

To conduct an assessment, we survey clients and assign them to one of five categories based on their responses across a range of success factors, such as digital strategy, ecosystem development, and organisation (see Figures 5 and 6):

- Traditionalists are the least digitally evolved. Important digital features are either missing or underdeveloped, while digital activities are ad hoc and uncoordinated and lack any overall digital strategy.

- Novices possess basic digital capabilities.

- Intermediates have functioning digital capabilities in specific areas, but they are not resident across the entire enterprise.

- Advanced organizations possess digital functionality that stretches across most of the company.

- Champions are the most digitally evolved group. Their digital capabilities are fully functional across the company, they are guided by an overall digital strategy, and they make optimal use of their digital products and services.

Image

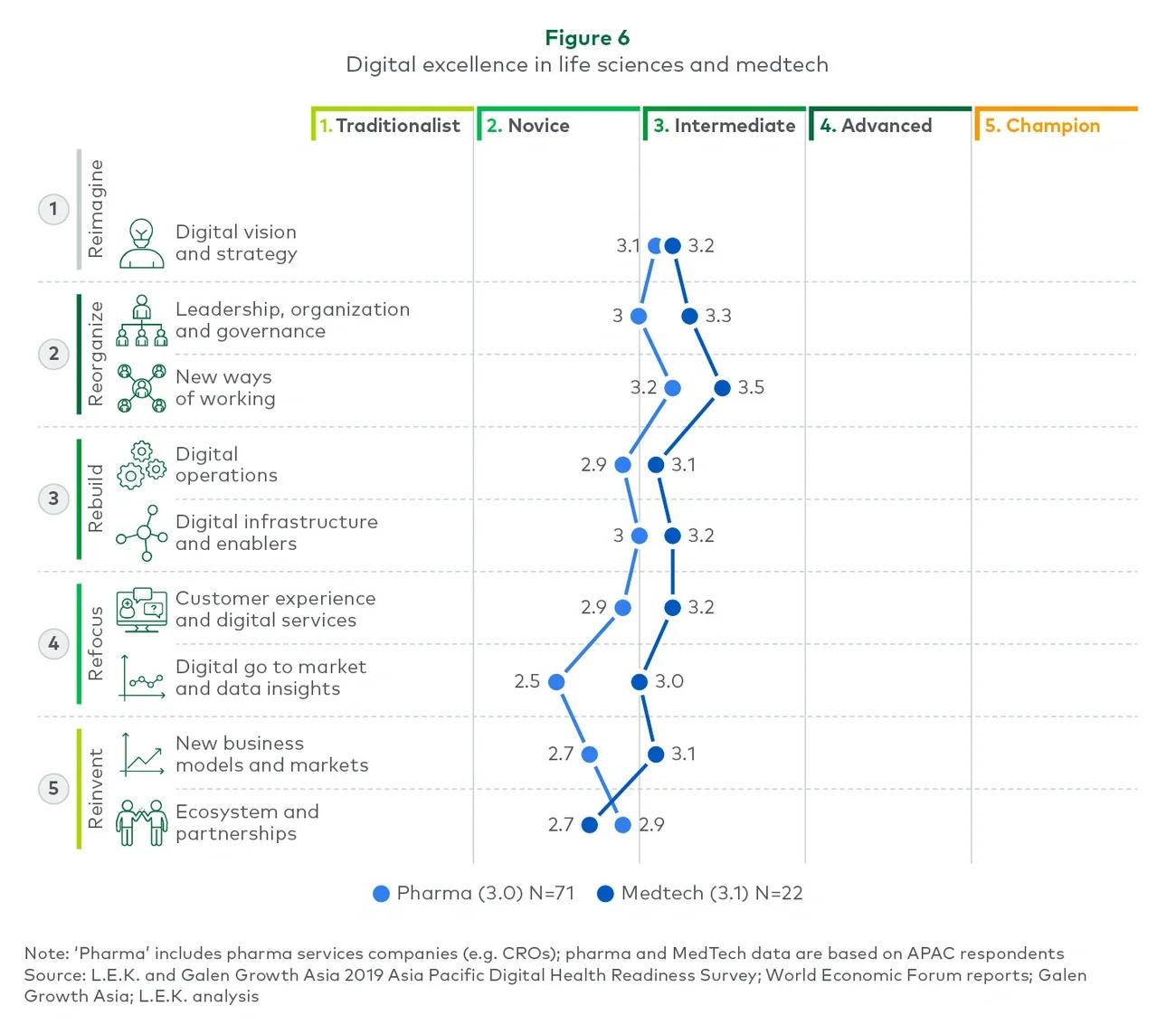

From data collected in DEX surveys so far5, we found no companies that were Champions or Advanced when it comes to digital health. Medtech and pharma companies were also close together, averaging between the novice and intermediate levels (see Figure 6).

Image

Go digital — there is no time to waste

Companies do not need a crystal ball to know that they need to develop their digital capabilities as soon as possible. The pace of change is extraordinary, with energetic new players from the tech sector and other industries entering the healthcare world, and new start-ups developing radical solutions on a daily basis. Private equity firms also need to take a deep look at their portfolio companies and think about how they can use a digital lens to drive value quickly and better exit their investments in the future.

Companies should not wait to act. Studies6 have shown that digital leaders outperform laggards by a factor of five to seven times in terms of revenue and/or valuation growth over a two-to-three year time frame. As well as shareholders, customers, and most importantly patients, will be the winners from a purposeful move to digital, regardless of what happens next. By contrast, companies that delay their digital efforts may well end up marginalized in the race to remain relevant in the healthcare sector of tomorrow.

Endnotes

1 In 2010 dollar value’

2 CNBC interview, reported 8 Jan. 2019

3 See e.g. David F. Rico, ‘What Is the ROI of Agile vs. Traditional Methods? (2008)

4 Merriam-Webster: ‘the networking capability that allows information to be sent to and received from objects and devices (such as fixtures and kitchen appliances) using the Internet’

5 So far, surveys were focused on the medtech and pharmaceutical sectors — 93 companies were surveyed, of which 71 were pharma and 22 medtech

6 E.g. digital leadership studies by isobar and ExO Work

Related insights

You might also be interested in these insights.

English