As the possibility of a recession looms and Americans adjust to the new normal following COVID-19, demand for retail private-label products is expected to rebound. The future for private label may be bright, but the road to profitable growth is by no means easy for producers.

Before the pandemic, retail private label was gaining share over branded products due to retailer investment and growing consumer preference. Then the trend reverted as consumers fled back to brands amid outsized supply-chain issues for private-label products.

Now private label is once again on a positive trajectory, amplified by recession fears and indicators that Americans are trading down on food and beverage spend. The next five years are projected to show private-label penetration continuing to outpace branded products. So, what does it take to win in this new environment? Let’s find out.

A strong track record of share gain

The earliest private-label programs were lower-priced copycats of national brands. Although some still are, the approach has evolved. Today, many retailers have sophisticated tiered private-label strategies aimed at meeting consumer needs across several pricing dimensions. On certain occasions, they even drive innovation. For example, Target’s Good & Gather private-label brand features more unique flavors than the retailer’s traditional Market Pantry private-label brand.

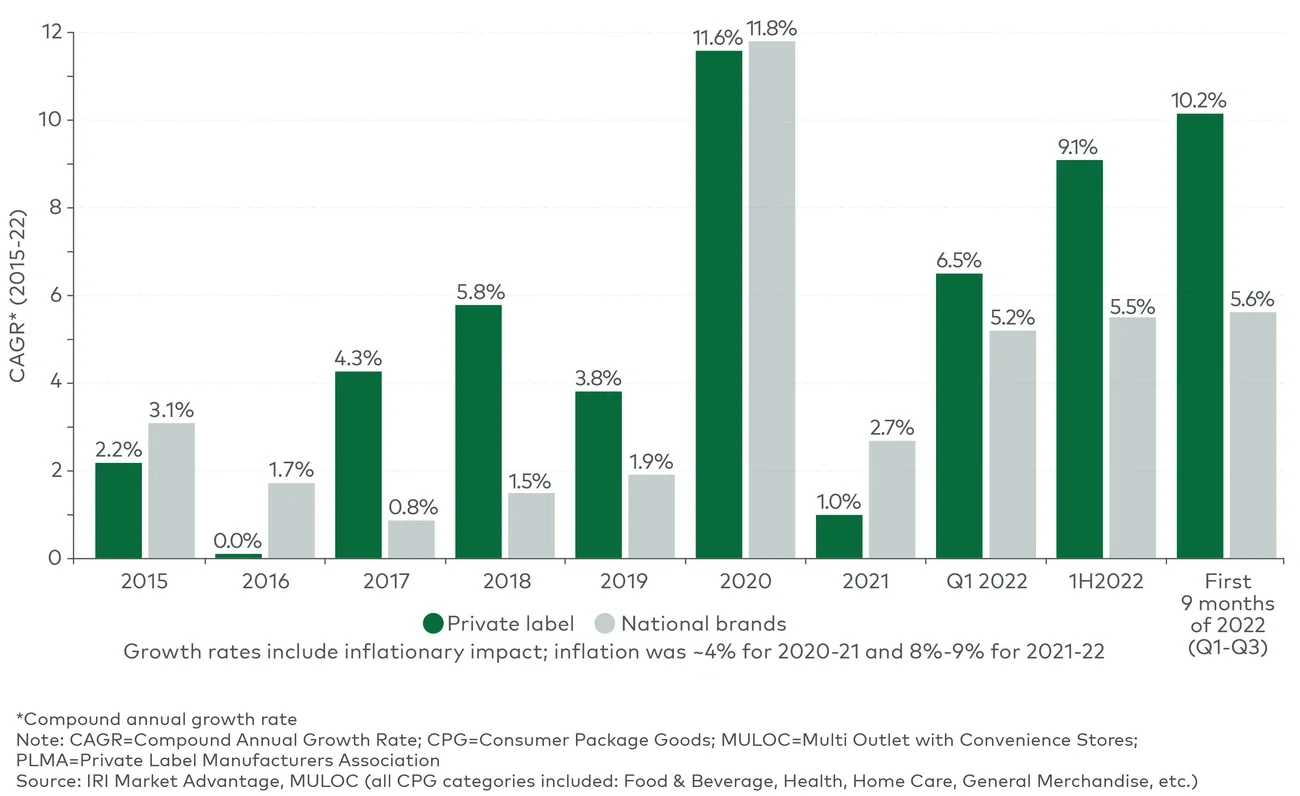

U.S. private-label sales, which historically have grown faster than national brands, stumbled during the pandemic (see Figure 1). Retail food and beverage sales skyrocketed as consumers stocked up and stayed home. The result was that private-label sales grew at an annual rate of 11.6% in 2020. But national brands grew even faster at 11.8%.

What happened? A desire for familiarity, paired with government stimulus spending, sent more consumers in search of national brands — particularly in comfort-food categories. At the same time, national brands that also produced private label made a conscious decision to prioritize fulfillment for their branded products so as not to damage brand equity. Private-label players lacked the scale and supply chain redundancy of national brands, so their issues with supply chain fulfillment were bigger. All these left retailers high and dry, with many private-label products missing from shelves into 2021. That year, the segment’s annual growth again lagged that of branded sales (1% versus 2.7%).

However, this disruption was short-lived. The first three quarters of 2022 found store brand sales up 10.2%, compared to national brand growth of 5.6%. Store brand growth has accelerated significantly throughout the year, from 6.5% in Q1 2022, to 9.1% in 1H 2022, and 10.2% in the first 9 months of the year (Q1-Q3). The third quarter growth was driven by a particularly strong month of September, in which store brand sales increased 12% compared to national brand growth of 6.5%. With U.S. economic indicators suggesting the possibility of a recession, consumers are beginning to tighten their wallets, positioning private label for further growth.