Key takeaways

-

C-store operators are bringing a sharper focus to retail best practices — a strategy that appears to be paying off.

-

The industry saw sales growth of nearly 9% in 2018, with in-store sales hitting a record $242 billion.

-

But advancing technology, an intense competitive landscape and shifting consumer tastes may be putting this resilient industry to its greatest test.

-

In this Executive Insights, we discuss the five strategic imperatives C-store owners and operators should consider in light of these market realities.

From airport kiosks to downtown bodegas, travelers and locals alike rely on convenience stores for the last-minute everyday items they need. C-stores, as they’re known in industry parlance, have held sway in the grab-and-go arena since the day in 1913 when a Pittsburgh gas station began to sell food. Today, more than 153,000 convenience stores are in operation across the U.S.

But the 24/7 shopping experience has come a long way from beer, beef jerky and bags of ice. With growing frequency, C-store operators are bringing a sharper focus to retail best practices and the customer experience. The result? Many stores now offer a much more sophisticated environment where shoppers can find familiar staples alongside fresh prepared foods and coffee to rival the corner roaster’s — all promptly served up in a clean and bright space.

A growing emphasis on the store, centered on foodservice

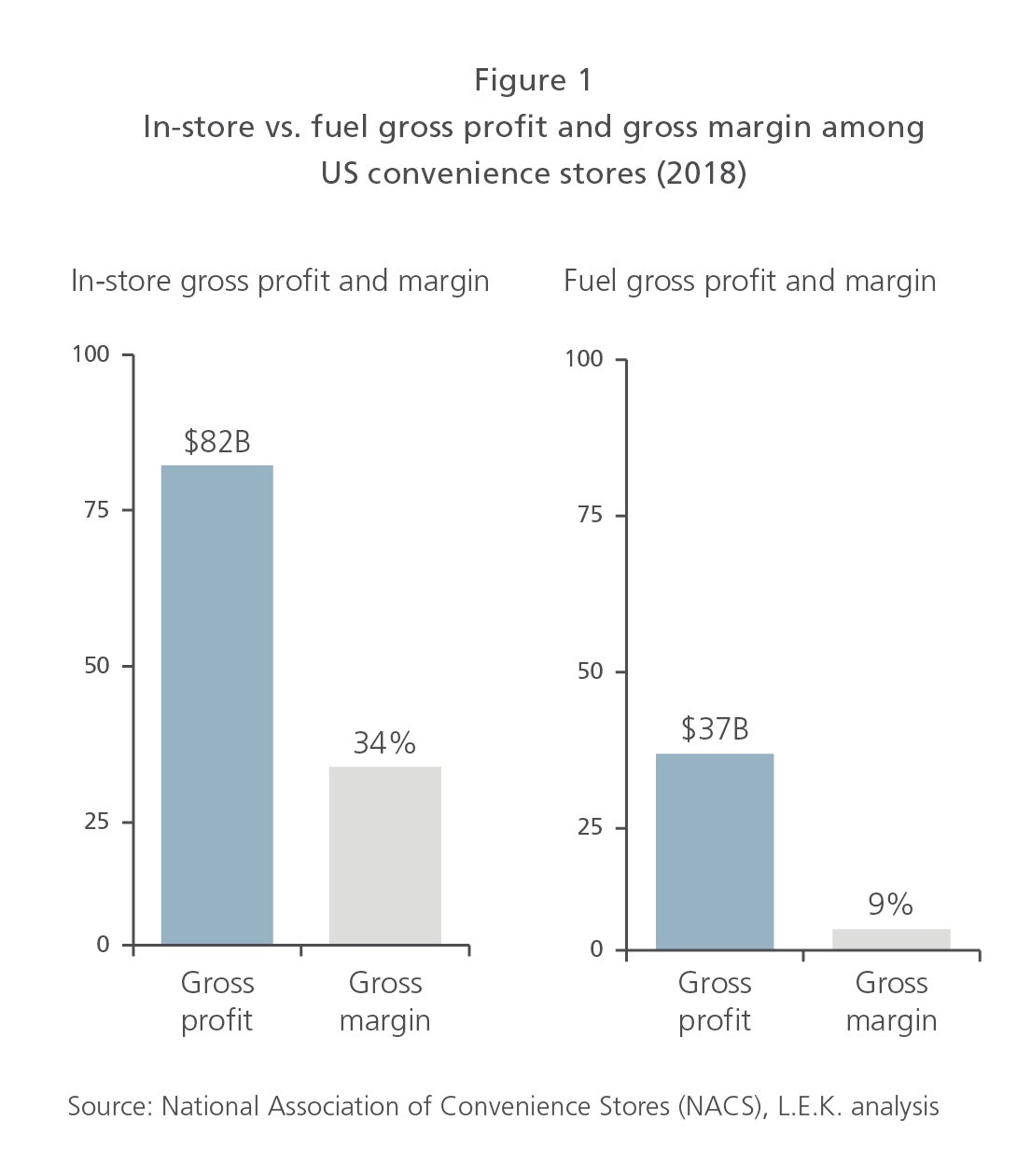

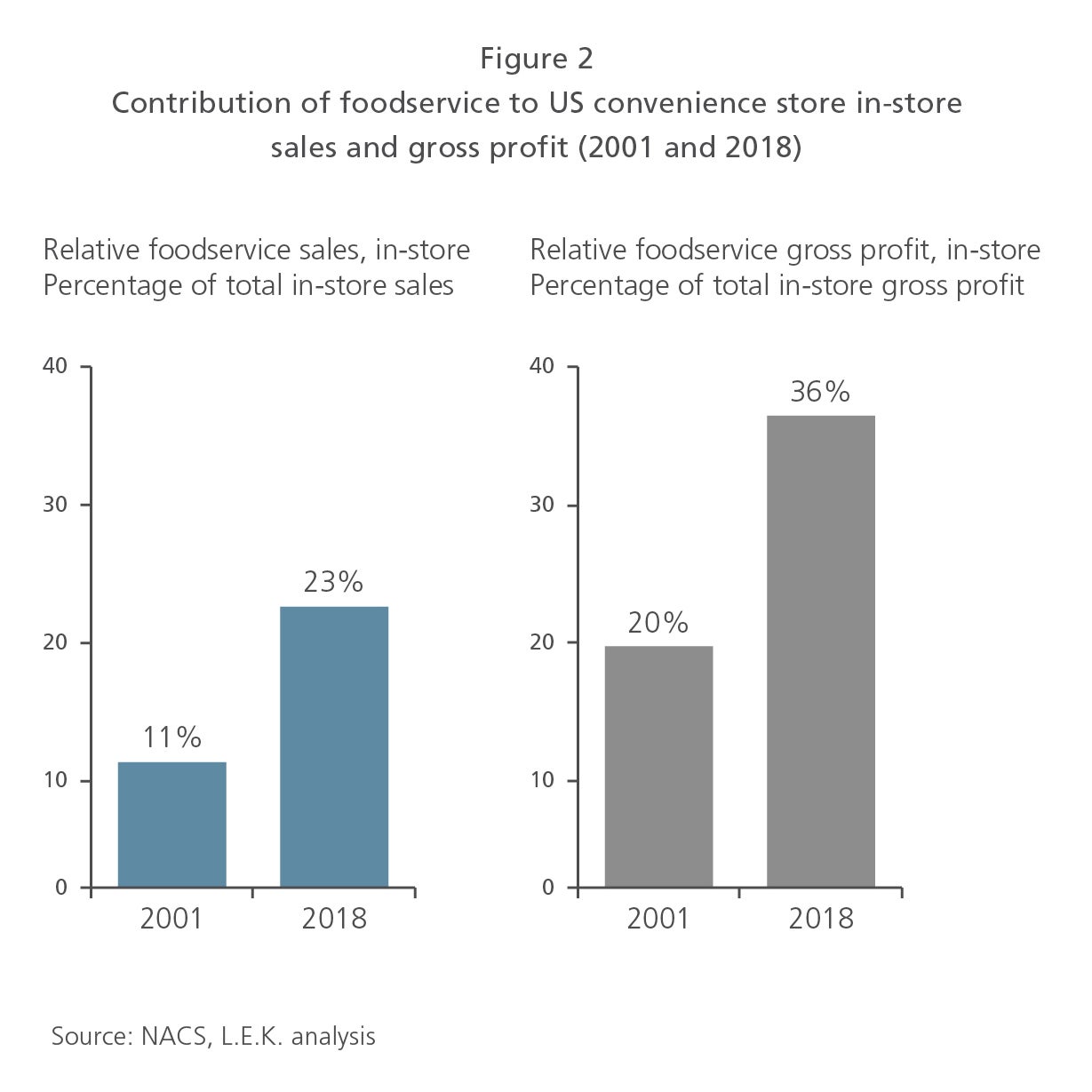

So far, the strategy appears to be paying off. The industry saw sales growth of nearly 9% in 2018, with in-store sales hitting a record $242 billion and generating more than twice the gross profit of fuel sales (see Figure 1). Foodservice accounted for around 23% of inside sales, more than double its share in 2001 (see Figure 2). Foodservice is also a high-margin category and contributes over one-third of C-store in-store gross profit (see Figure 2).

These results reflect store operators’ ongoing efforts to expand the quality, service and selection of their edible offerings. Today, next to standard-issue soft drinks and churros, shoppers often encounter branded coffees, premium shakes and meal offerings that can rival the quality of many quick-service restaurants. Customizable fare such as made-to-order sandwiches, hot soups and sides — even items from the grill — are making their way onto C-store menus, driving traffic for meal-based (versus gasoline-based) missions.

That’s not to say the pump is a thing of the past. Fuel still accounts for the lion’s share of sales at C-stores and is a critical traffic driver for the stores. And in 2018, fuel sales at convenience locations surged 13.2%, helped along by rising gas prices. However, gross margins for fuel are often less than a third of what they are for food. Against this backdrop, growing foodservice has become a critical profit lever for C-stores and the focus of a flurry of major initiatives.

Storm clouds on the horizon

Longer term, fuel sales will face even more pressure. While U.S. gasoline consumption is high today, there are indications that motorists are stopping to refuel less often. That’s likely to continue in the wake of improving fuel economy and the growing adoption of alternative-fuel vehicles. The implications are worrisome: In addition to lower fuel sales and profits, fewer gas fill-ups lead to fewer in-store visits and diminishing sales and profit.

C-stores will also need to address cultural shifts. Convenience stores currently account for 71% of nicotine distribution in the U.S., but cigarette use is down by more than half since 1990, with at least 90% of U.S. adults projected to be nonsmokers by 2025. The impact up to now has been muted because drugstores and select mass merchants have walked away from the category, enabling C-stores to fill the breach. With much of this channel consolidation now behind us, however, C-stores will start to feel the brunt of the secular decline in cigarettes.

Then there’s intensifying competition in the broader foodservice arena. Convenience stores aren’t the only retailers to have noticed consumers’ growing appetite for prepared and ready-to-eat foods. Grocery stores, warehouse clubs, discount stores and even drugstores are jockeying for position in this flourishing market, changing their store formats to accommodate convenience-driven shopping trips. The most formidable competitors? Quick-service restaurants (including the high-growth fast casual segment) are on the offensive, and are innovating their menus, rolling out loyalty programs, and staying sharp on pricing and promotions in order to protect their turf. All this is raising the bar for C-stores as they reexamine the quality and innovation they bring to their foodservice offerings.

Finally, there’s the ramp-up in home delivery. Increasingly, grocers are replenishing staples (and more) with one- and two-hour delivery services directly to the consumer’s door. Combined with the piping-hot growth in restaurant delivery sales, it’s a safe bet that on a growing number of occasions, C-store consumers will trade hitting the pavement for tapping a smartphone screen.

Navigating a complex environment

So the good news is that transformation efforts are paying off. The bad news? It’s just the end of the beginning. Amid shifting preferences and disruptive trends, operators have more work to do to sustain the C-store value proposition.

Getting it done requires careful navigation. Convenience stores have expanded well beyond their traditional blue-collar clientele, but often that just means everyone visits a C-store occasionally. To become a regular destination for a more diverse group, the C-store has to wind its way into people’s daily and weekly routines by enabling them to fulfill a much broader set of trip “missions.”

That’s no small task. Each C-store mission carries with it an array of consumer demands — such as proximity, good value, sought-after products, pleasant store atmosphere, and food and drinks that actually taste good — in a seemingly endless number of combinations. Moreover, the same customer can have very different preferences from mission to mission, making it even harder to prioritize and service so many need states simultaneously.

In summary, consumers rely on the C-store for a wide range of occasions, and their needs are a cocktail of unending variety. Counterintuitively, this makes the simple convenience store one of the more complicated businesses in retail.

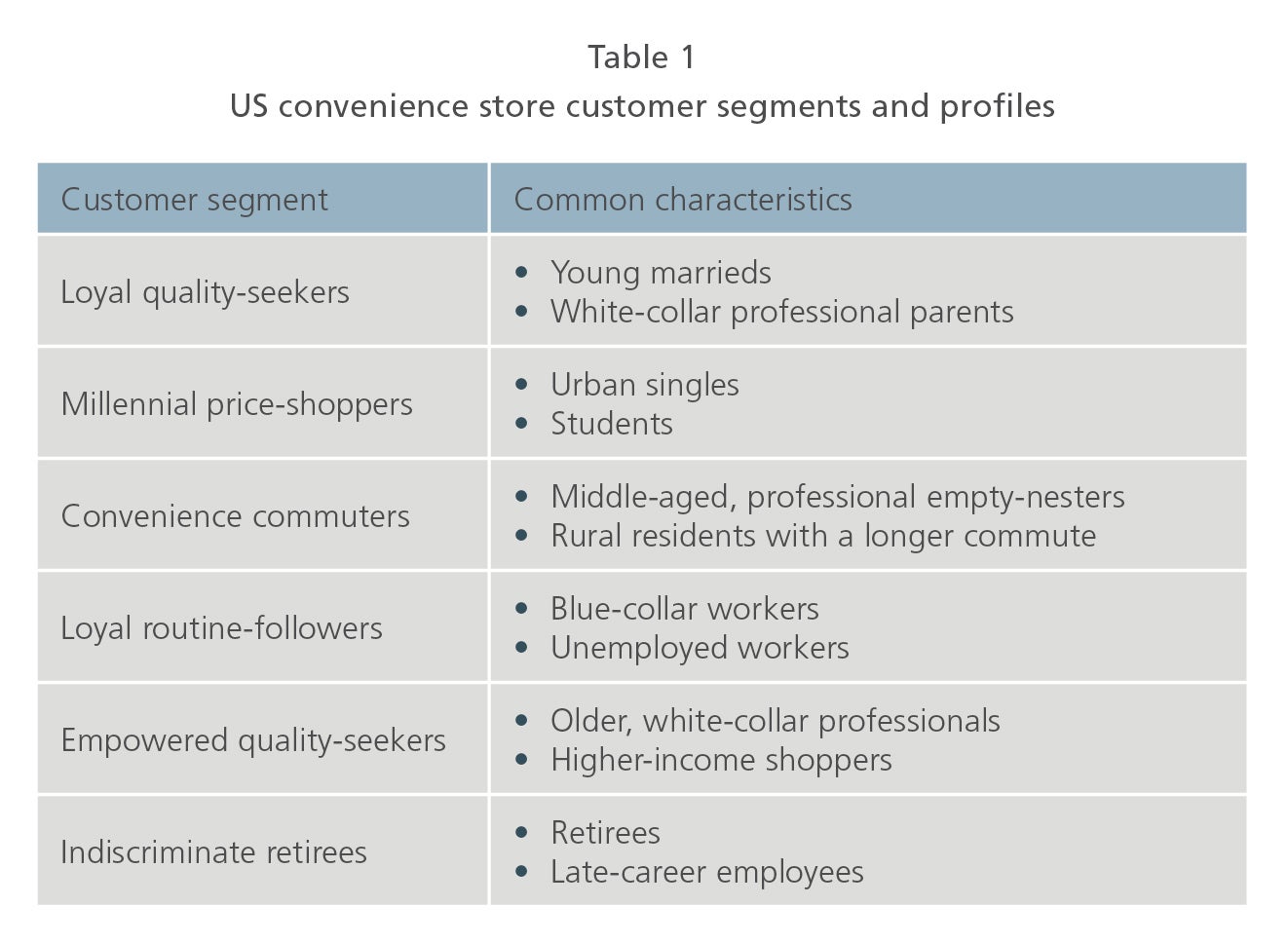

Even so, there’s an order to the complexity. L.E.K. Consulting surveyed 1,500 shoppers on their convenience-store habits. From their responses, we were able to identify six distinct customer segments occupying the C-store consumer landscape (see Table 1).

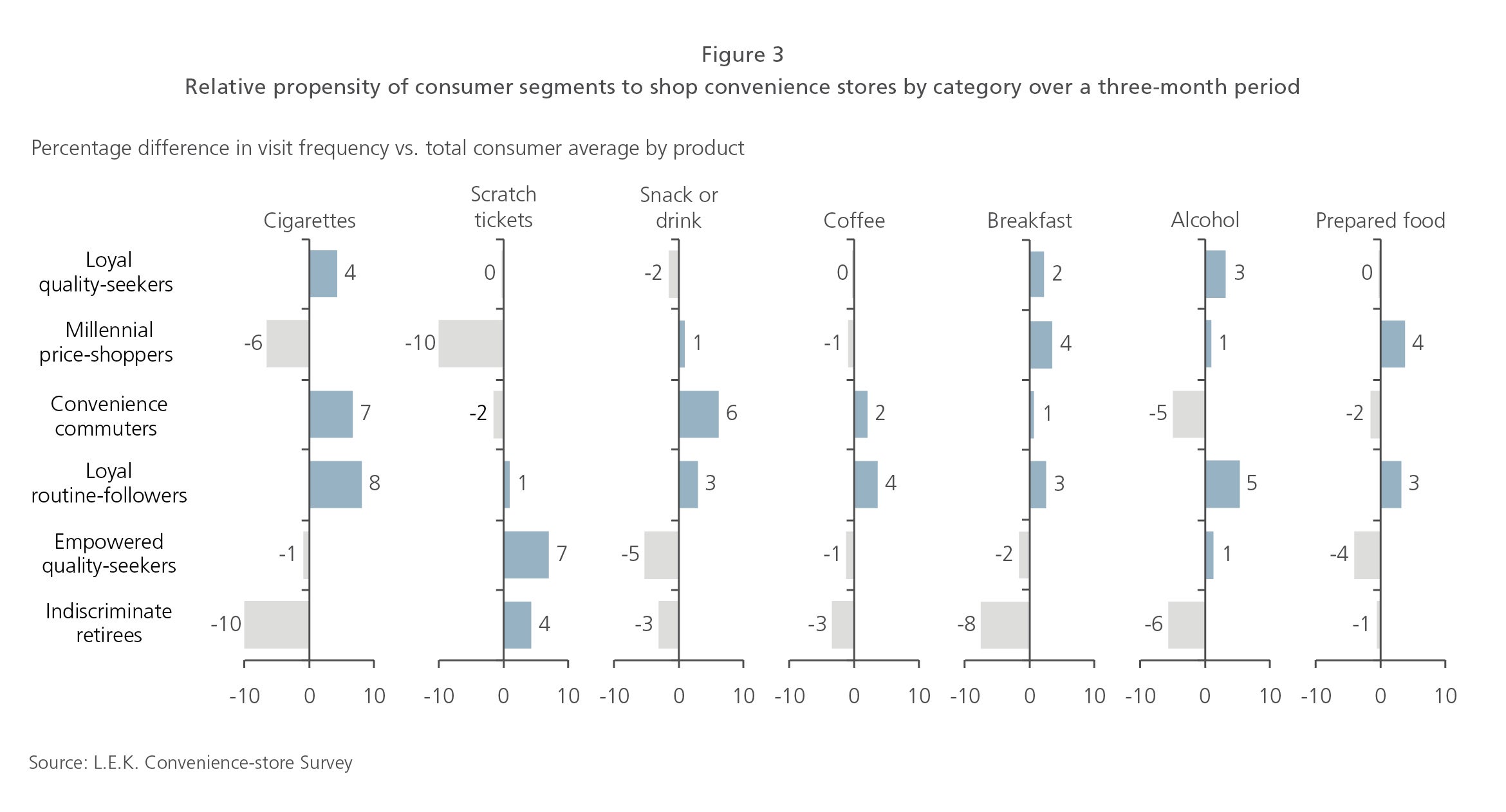

Each segment has different habits that must be understood. For example, indiscriminate retirees’ C-store trips are dominated by trips for lottery tickets, and this group is the least likely to buy cigarettes, coffee, breakfast or alcohol at a convenience store. By contrast, loyal routine-followers have a much greater appetite for C-stores — especially for coffee, breakfast and prepared foods (see Figure 3).

As we mentioned, shoppers’ needs can also vary significantly even within consumer segments, depending on the mission they’re on. For example, a convenience commuter looking for a quick bite has a very different set of criteria when running between business meetings than when running between weekend errands and children’s sporting events.

Getting to top of mind

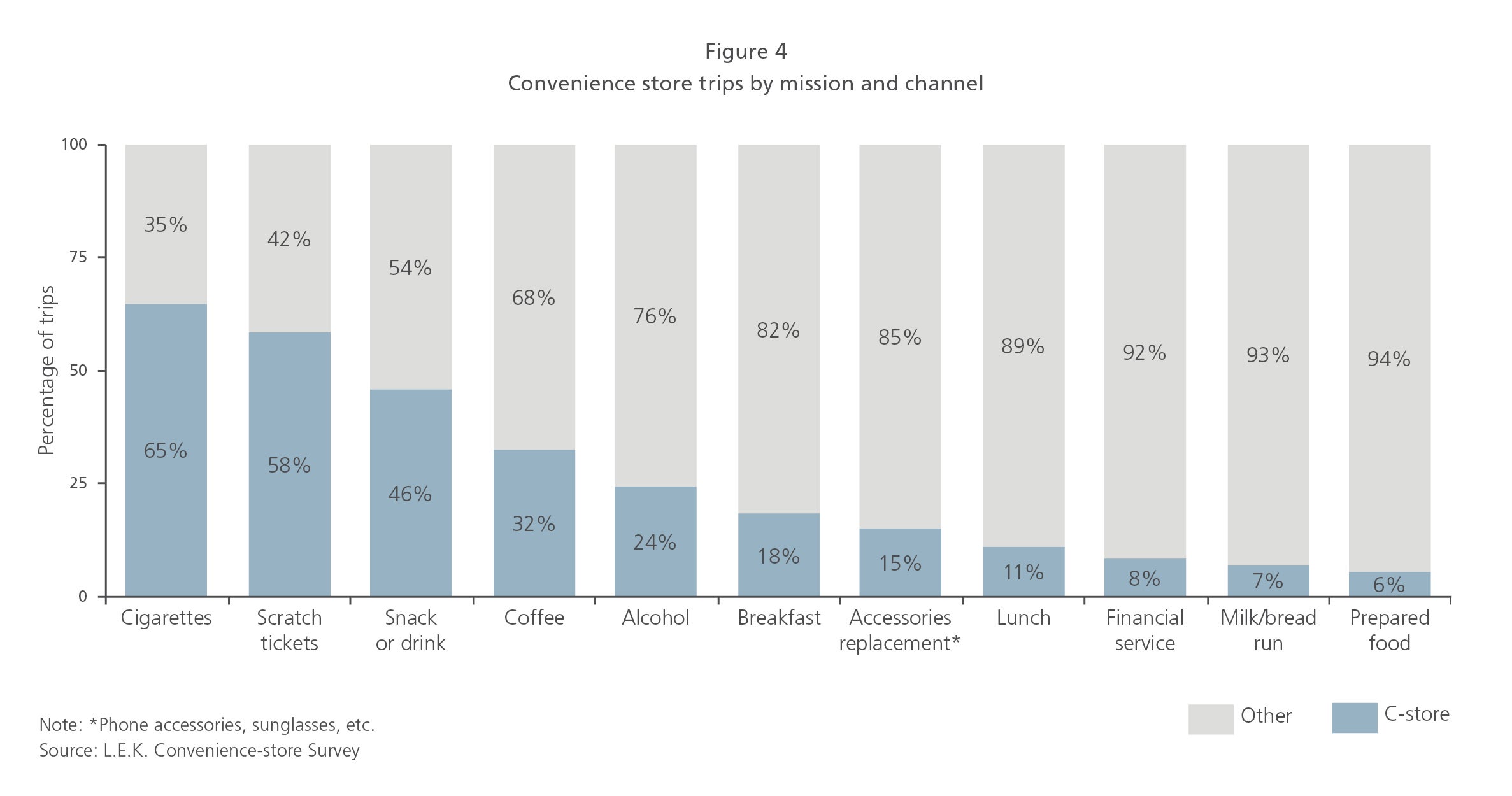

For all the expectations consumers have of them, however, convenience stores just aren’t top of mind for many missions — food runs included. In fact, of all the times survey respondents went out for milk, bread or prepared food during the preceding three months, they say a convenience store was their destination less than 10% of the time (see Figure 4).

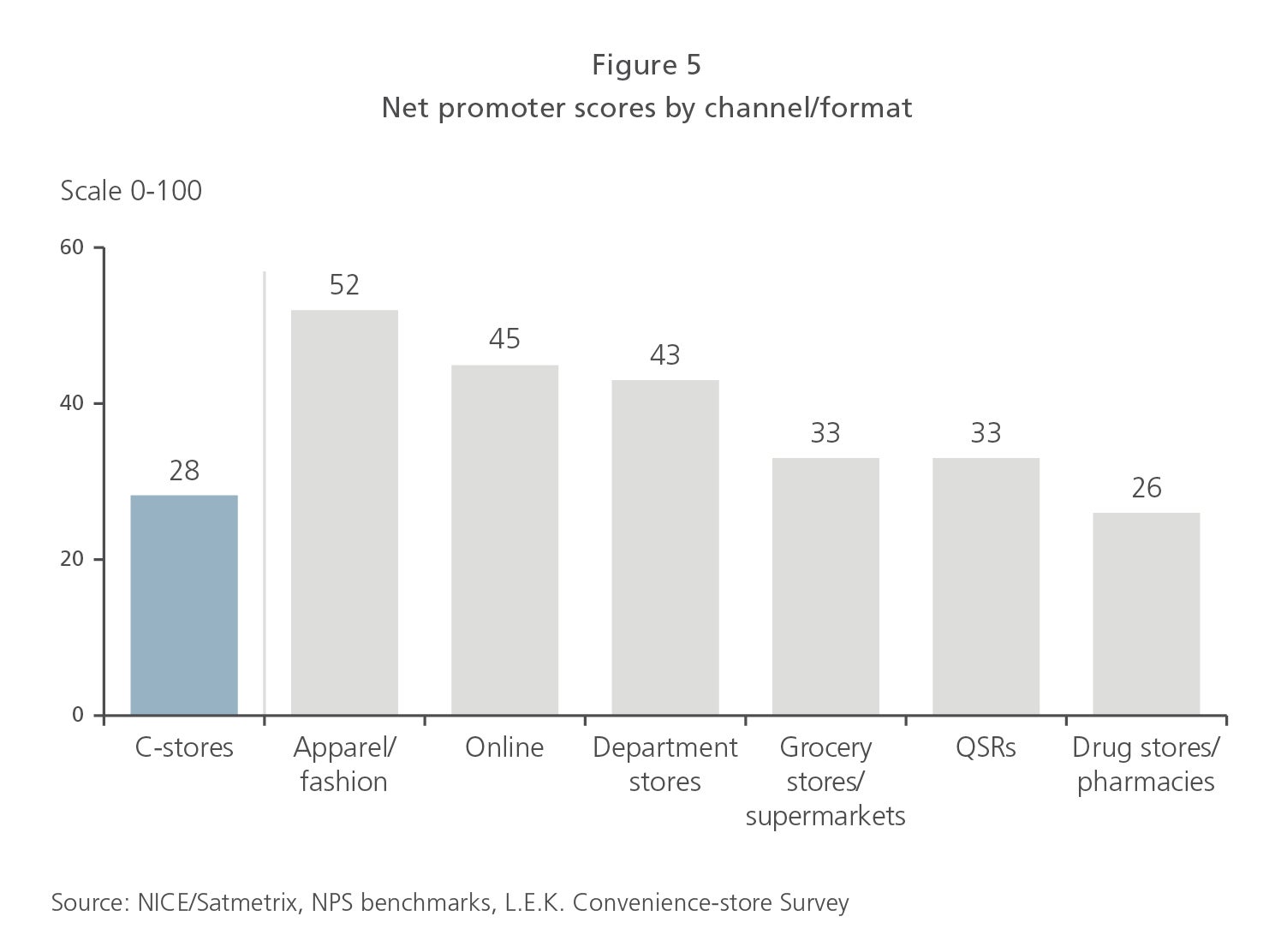

Neither is loyalty very high. The net promoter score (NPS) for convenience stores varies by segment, ranging from a high of 40 among empowered quality-seekers to a low of 19 among millennial price-shoppers and indiscriminate retirees. But in general, convenience stores have a lower NPS than many retail segments and quick-service restaurants (see Figure 5).

This is problematic for a business that’s aiming to take market share from formidable competitors. Connectivity and trust help take risk out of the equation, making it easier for customers to take a chance on a different experience — such as buying an acai bowl from a convenience store rather than a local juice bar.

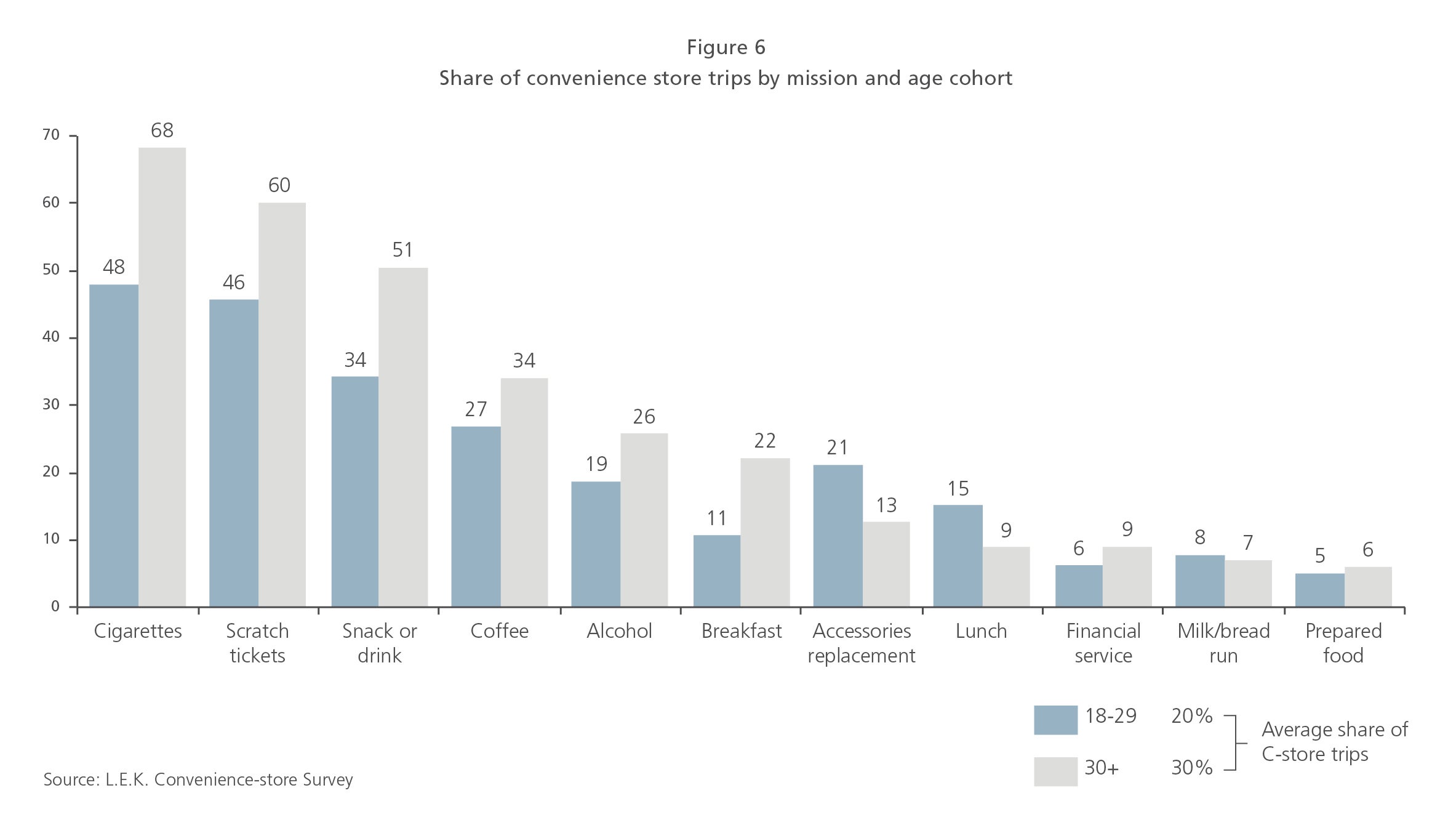

To illustrate, consider the low NPS that C-stores have among the millennial price-shopper segment. Young consumers’ low affinity for C-stores is evident in their shopping habits. On average, C-stores earn about a 10% smaller share of in-store trips among consumers under 30 years of age than they do among older consumers (see Figure 6). If young consumers retain this sentiment toward C-stores as they age, the result will be a perennial leaky bucket of business for C-stores, making this a core strategic issue for the industry to address.

Millennials are significantly less likely to visit a convenience store for cigarettes, scratch tickets, coffee and other common C-store offerings. At the same time, they’re more discerning: Brands, store layouts, product quality and food quality all matter more to this segment than they do to older consumers. Millennial price-shoppers also have a markedly greater preference for convenience and technology-enabled solutions (think pre-ordering, delivery and mobile apps). The upshot? The bar for winning the business of younger generations is high, and will require convenience stores to deliver on multiple fronts. This will involve careful navigating to make the right decisions and trade-offs that will pay off.

Taking control of the future

In light of these market realities, convenience store owners and operators should consider five strategic imperatives:

- Prioritize “ownable” consumer segments and missions. Of the key customer missions that comprise your brand’s business, determine which ones your brand can own, given the competition and the relative advantages you have.

- Recalibrate the meaning of “convenient experience.” Look for the frictions in your customers’ journeys and come up with novel ways to alleviate them, from store design and better food selection to technological and operational change.

- Act like a true brand. Use the evolution of the C-store format as an opportunity to recast what you stand for in a way that resonates with target customers and allows you to build closer connections with them. Then deliver on it consistently across the entire store experience.

- Launch or reconfigure loyalty programs. Add or revisit features like rewards, limited-time offers and brand partnerships to arrive at the mix that keeps target customers engaged — while yielding a stream of insights to power imperatives one, two and three.

- Earn back young consumers. Realign your product assortment, shopping experience and other attributes — even community engagement and brand positioning — with the needs and values of this critical, high-opportunity source of future business.

Convenience stores have survived a century’s worth of change. But advancing technology, an intense competitive landscape and shifting consumer tastes may be putting this resilient industry to its greatest test. As C-store operators rethink their Cokes-and-smokes image, they confront a future that demands smart strategies for bolstering their value proposition, creating greater consumer engagement and taking the business through the next phase of an exciting evolution.

01272020140141