COVID-19 in the US: Consumer Insights for Businesses — Edition 2, Part 1

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

In partnership with Civis Analytics, we’re publishing a series of insights on the consumer response to COVID-19. Our goal is to help our consumer-facing clients monitor sentiment and behaviors as they take shape during this unprecedented period.

At the same time, we acknowledge that the pandemic is a humanitarian crisis first and foremost. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

The COVID-19 crisis has thrown us into uncharted economic territory. Still, one thing is certain: Consumer behaviors are changing significantly.

“COVID-19 in the U.S.: Consumer Insights for Businesses” is a series of insights reflecting the results of a recurring consumer pulse survey. Administered approximately every two weeks, the survey tracks the pandemic’s impact on consumer sentiment overall, as well as by segment, geography and product. Each edition offers an updated perspective on the current landscape and what the lasting impact is likely to be. To continue the discussion, please don’t hesitate to contact us.

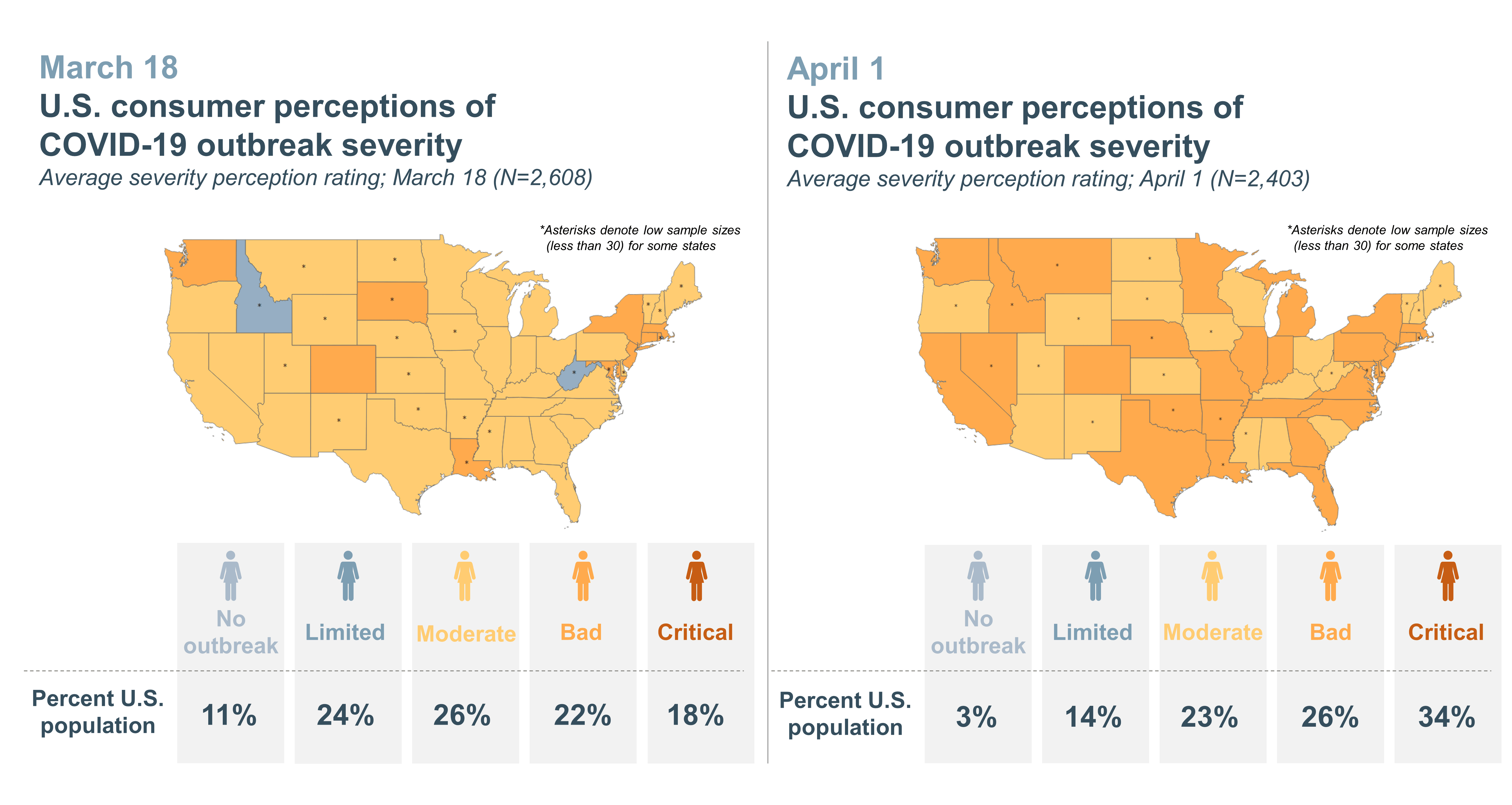

Edition 2 reflects responses captured on April 1, 2020, from ~2,400 U.S. consumers who are demographically representative of the general population. On various charts, we compare how responses have trended since Edition 1 of the survey (~2,600 responses captured two weeks prior on March 18, 2020).

Important note: All forward-looking data reported are a reflection of consumer sentiment/expectations as of the second edition of the survey and are not official L.E.K. Consulting forecasts.

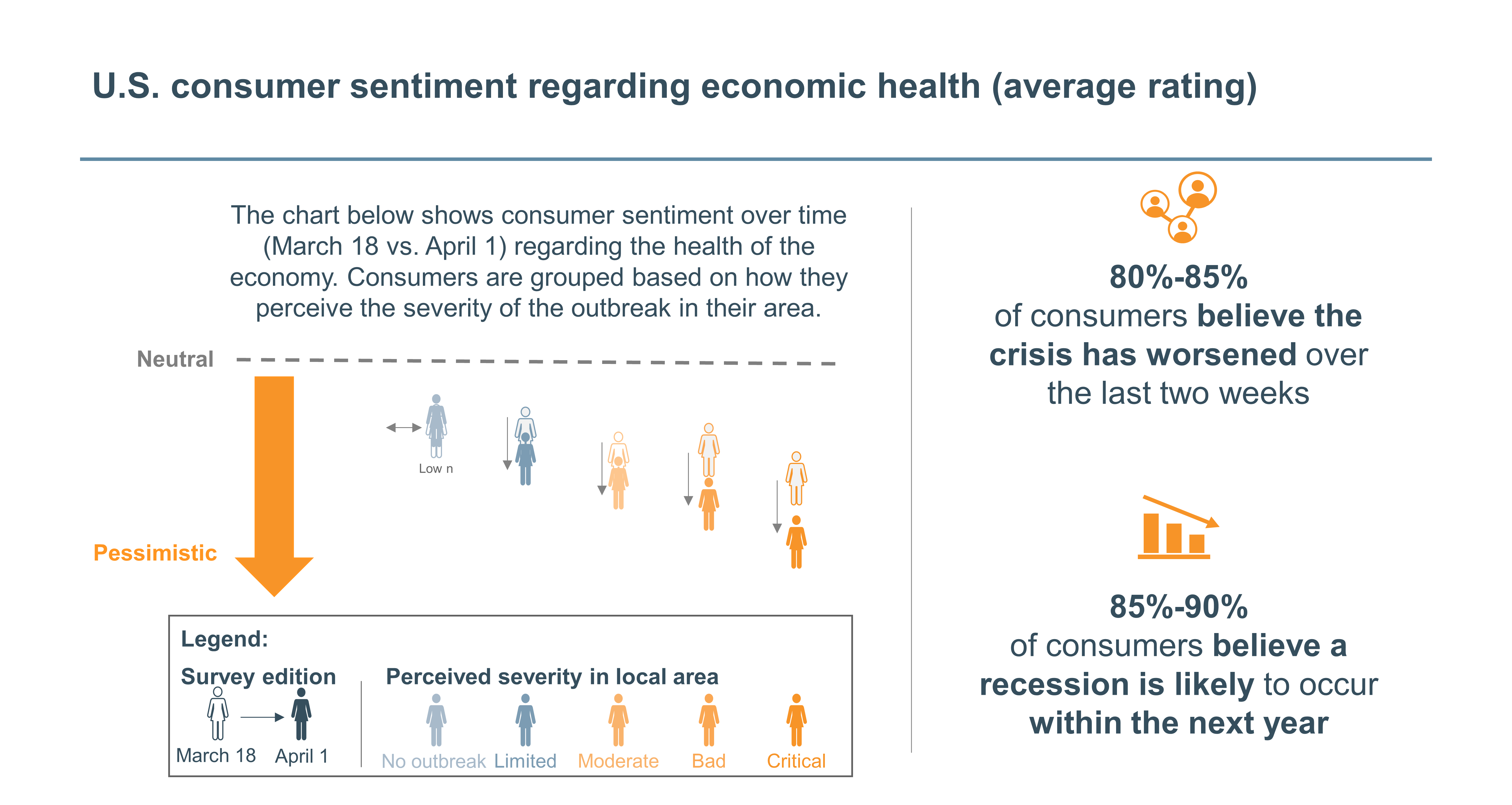

In what is first and foremost a humanitarian crisis, we start by evaluating consumer sentiment across the country. How severe consumers perceive the outbreak to be in their geographic area is a key driver of their emotions and mindset, both of which ultimately drive spending patterns and other behaviors.

By comparing the two editions of our survey (March 18 and April 1), we see that consumer sentiment is worsening:

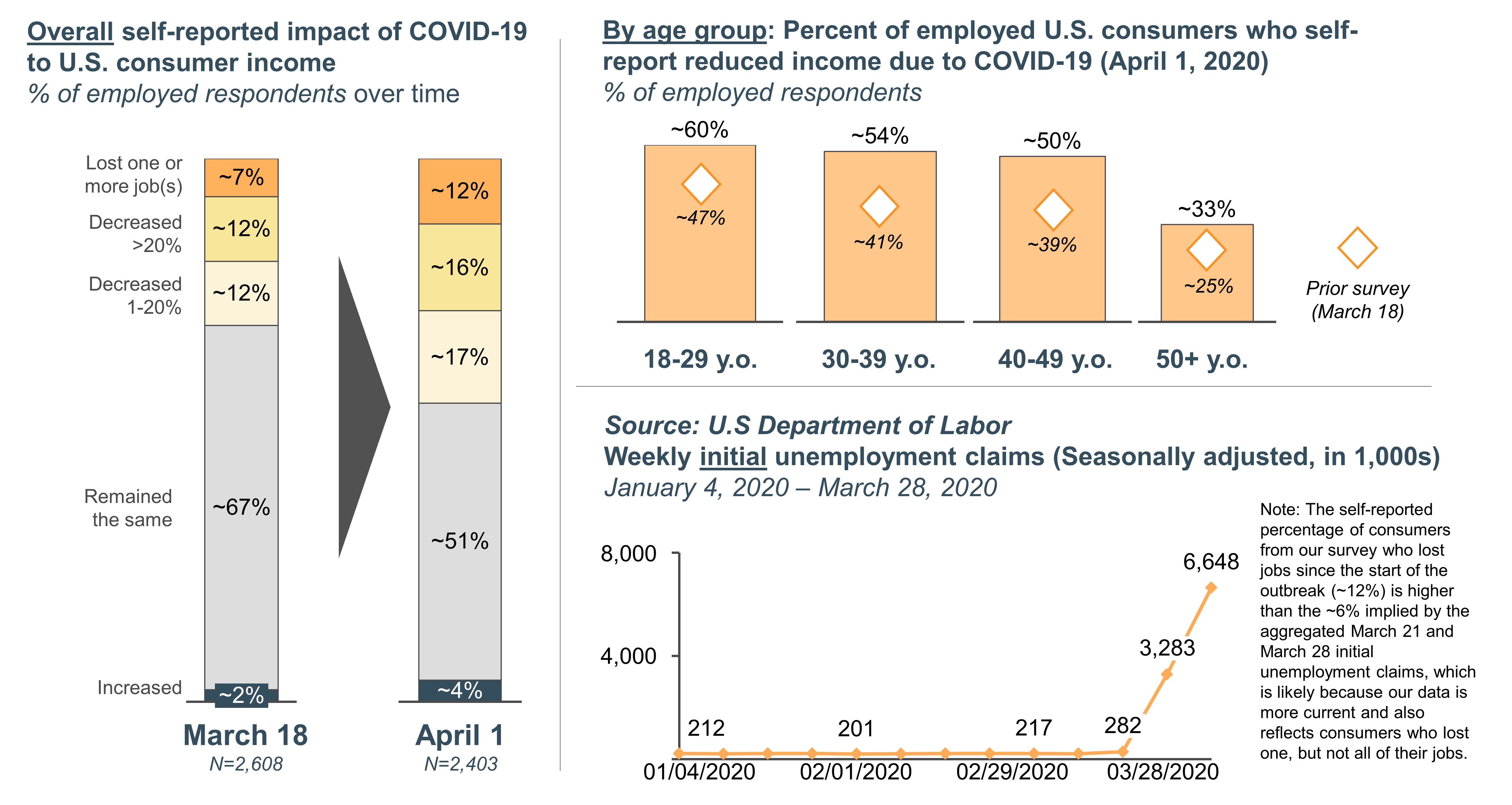

Consumers self-report significant and increasingly negative impacts to their income resulting from COVID-19. Approximately 45% of all consumers report a decline in their income vs. ~30% reporting so on March 18.

Specifically, ~12% report that they have lost one or more of their job(s) entirely (vs. ~7% two weeks ago). Another ~33% report that their overall income has been reduced since the outbreak began (vs. ~24% two weeks ago).

Young consumers appear to be affected the most. Approximately 60% of respondents ages 18-29 reported a decrease in income compared to just ~33% of respondents ages 50+.

These income trends from consumers are increasingly bleak. Unfortunately, they appear to be consistent with the trend seen in the latest initial unemployment insurance claims data from the U.S. Department of Labor. The latest report showed a sharp rise in the number of initial unemployment claims, from ~200,000 on March 7 to more than 3 million on March 21 and over 6 million on April 1, after a long period of relative stability.

Important note: The self-reported percentage of consumers from our survey who lost jobs since the start of the outbreak (~12%) is higher than the ~6% implied by the aggregated March 21 and March 28 initial unemployment claims, which is likely because our data is more current and also reflects consumers who lost one, but not all of their jobs.

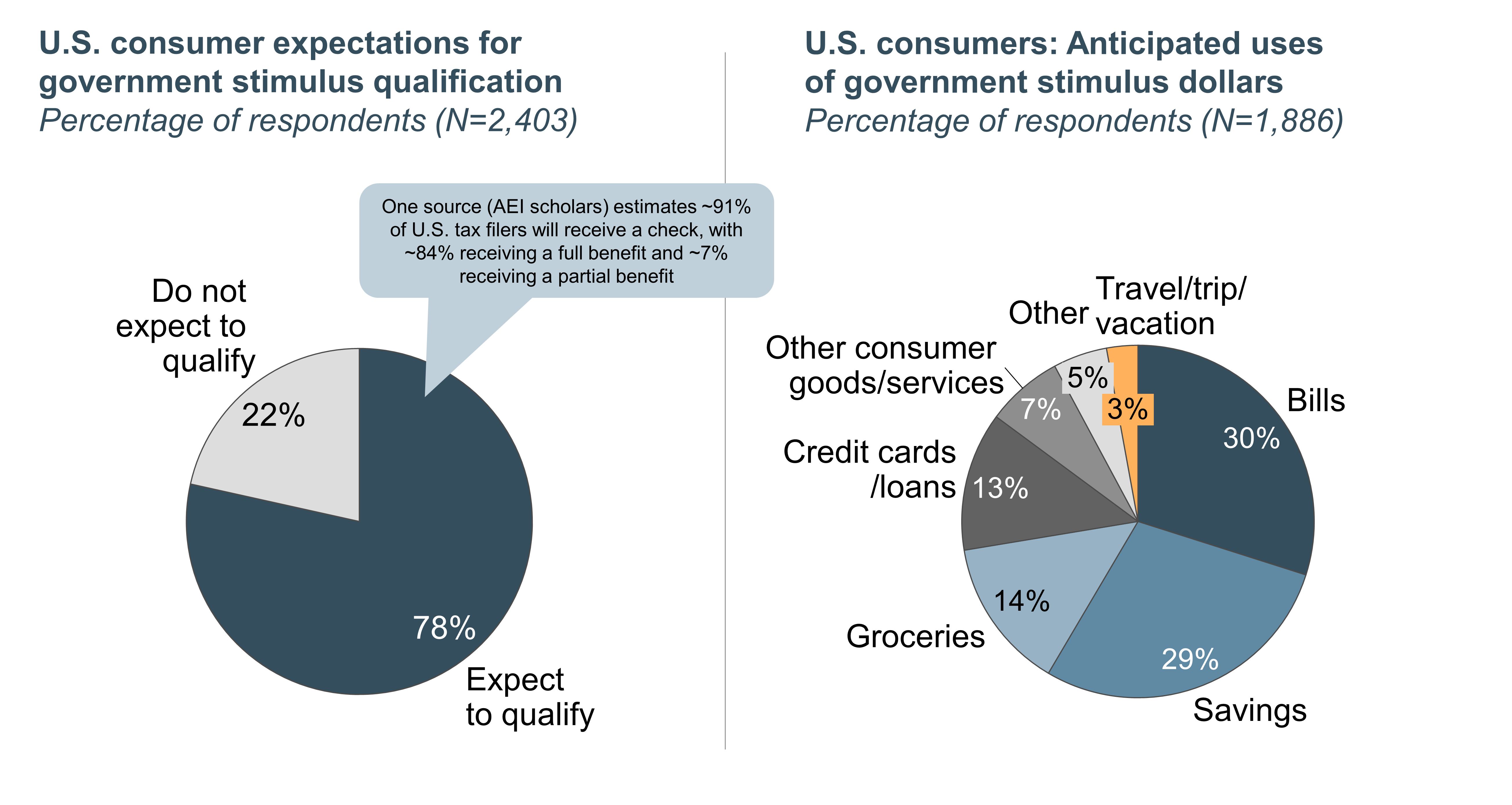

One-time stimulus checks from the U.S. government aimed at helping keep people engaged in the economy are likely to go out in the upcoming weeks.

The check amount will be based on 2018 or 2019 tax returns and is expected to total $1,200 per individual tax filer (or $2,400 for married couples filing jointly) with an increase of $500 per child for those individual filers with adjusted gross income up to $75,000 (or up to $150,000 for married couples filing jointly). For filers with income above those thresholds, the payment amount is reduced and then phased out for individual filers whose income exceeds $99,000 (or $198,000 for married couples filing jointly).

Nearly ~80% of consumers surveyed expect to qualify for stimulus funds vs. an estimated qualification rate of 91% from one source, with 84% receiving a full benefit and 7% receiving a partial benefit.

Consumers expect the majority (~85%) of stimulus dollars to go toward bills (30%), savings (29%), groceries (14%) and credit cards/loans (13%). This might imply that industries beyond groceries and utilities may only see a small boost from the rebate.

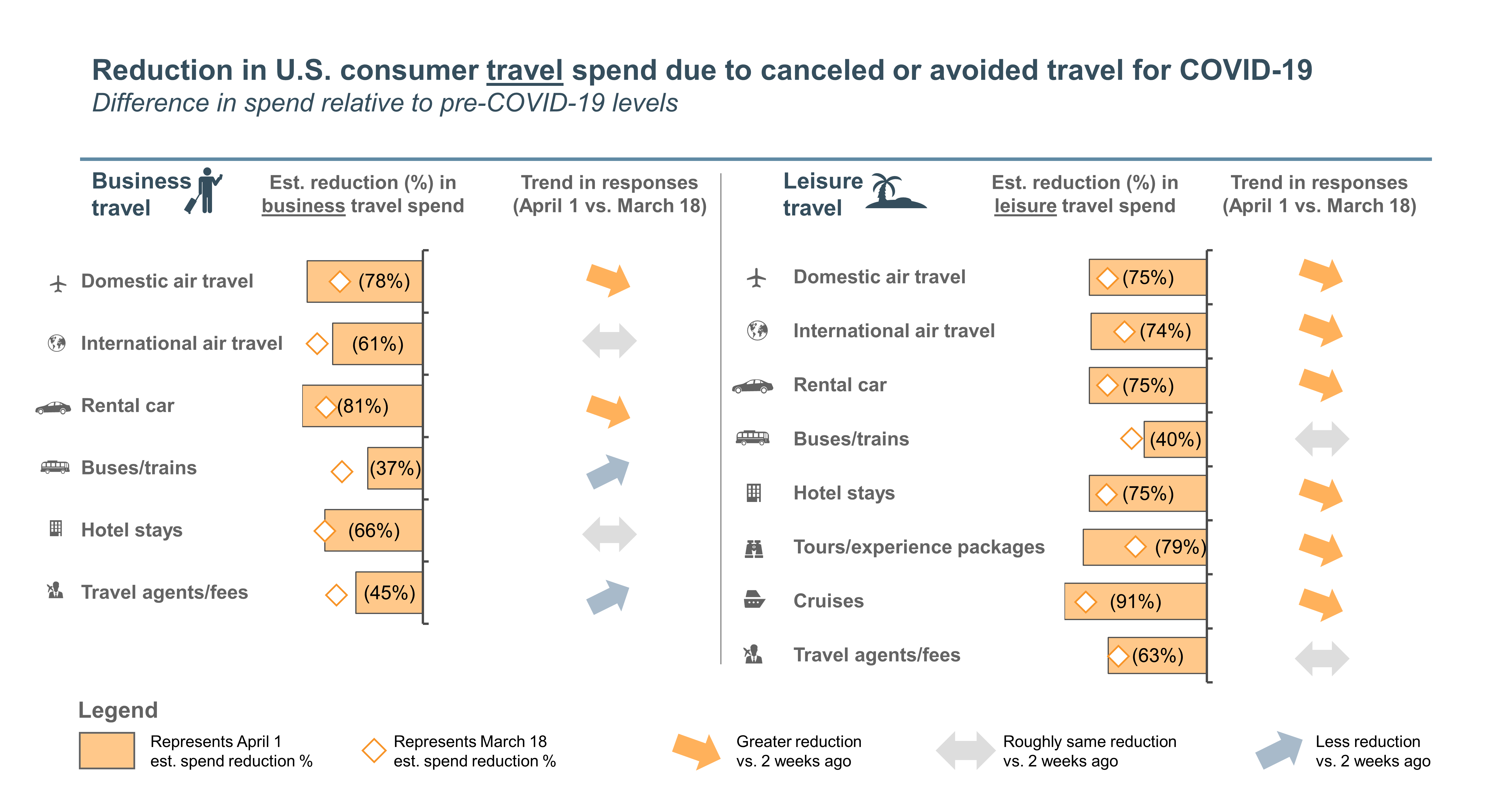

Next, we evaluate consumer travel spend — a sector hard hit from the very beginning of this crisis, and one that remains at the forefront of the news cycle.

Across all business and leisure travel categories tested, U.S. consumers self-report significant reductions in 2020 travel spend due to cancellations or avoidance, ranging from -40% to -80% of total planned spend.

Over the past two weeks, consumers report increased cancellation/refund rates for most categories.

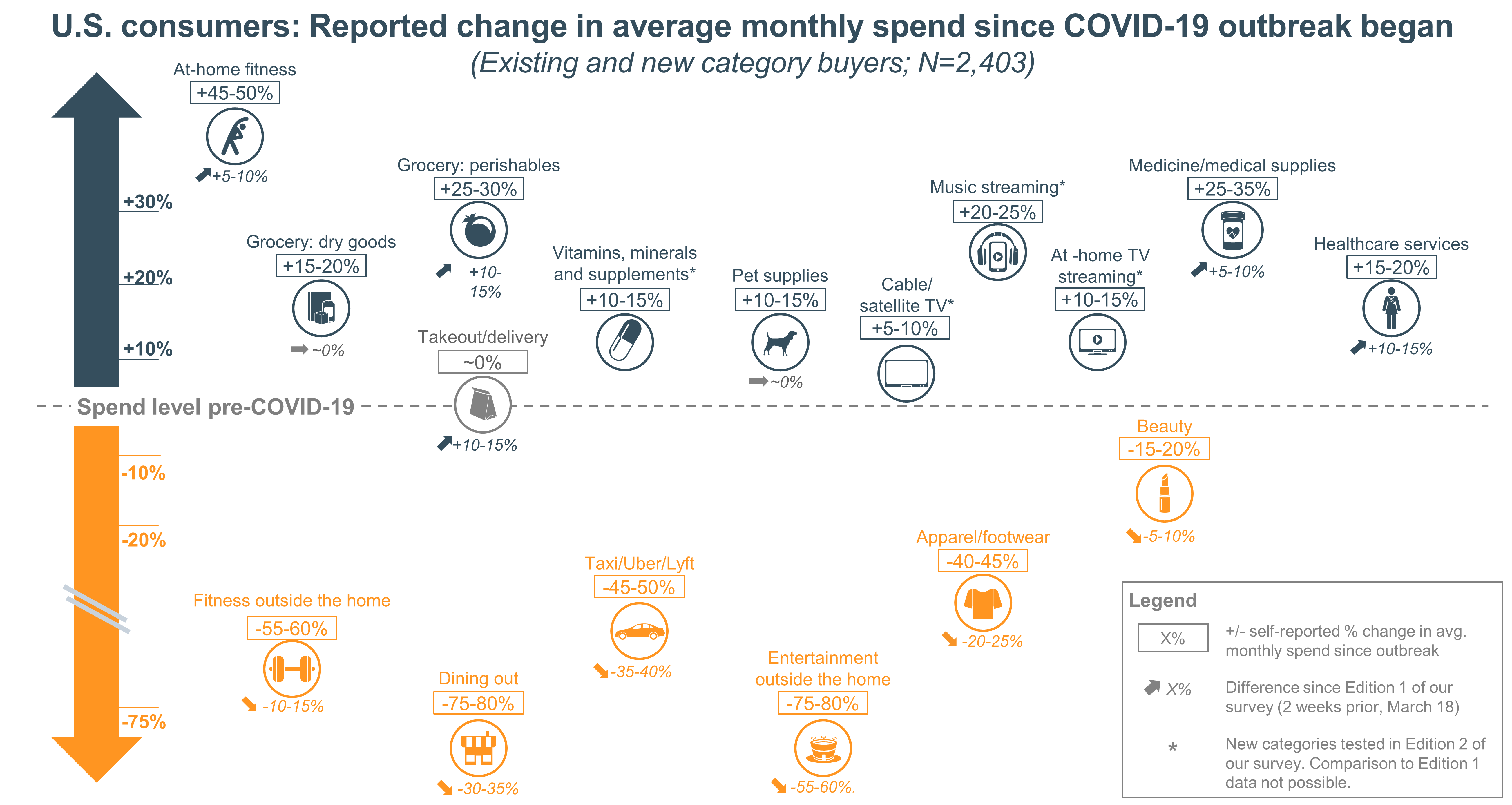

Beyond travel, consumer spend across a wide range of other categories has also changed significantly as a result of the outbreak.

Many categories, similar to travel, have experienced a decline in average monthly spend levels, according to consumers, specifically:

Notably, takeout spend was down 10%-15% as of March 18, 2020, but appears to be roughly back in line with pre-outbreak spend levels according to our latest survey. This feedback would suggest consumers increasingly turn to takeout as an alternative to home cooking. Recent news regarding how to order takeout safely has likely driven greater consumer comfort.

Other categories continue to see increased average monthly spend since the beginning of the outbreak:

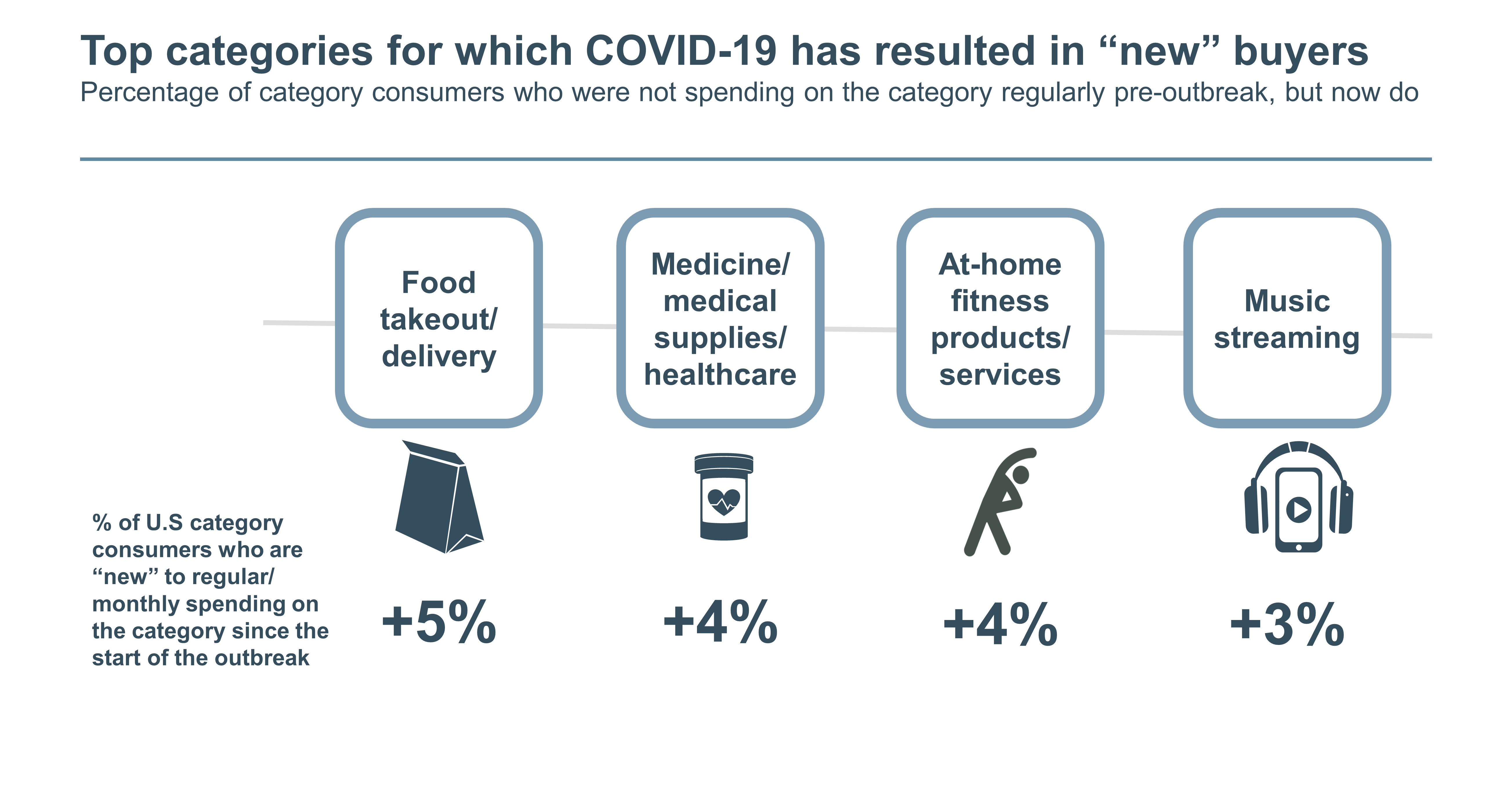

Consumers are participating in new categories as a result of the outbreak. The categories that have seen the most new consumers as a result of the outbreak are those that cater to consumers’ current home-based lifestyles and those that provide entertainment for consumers:

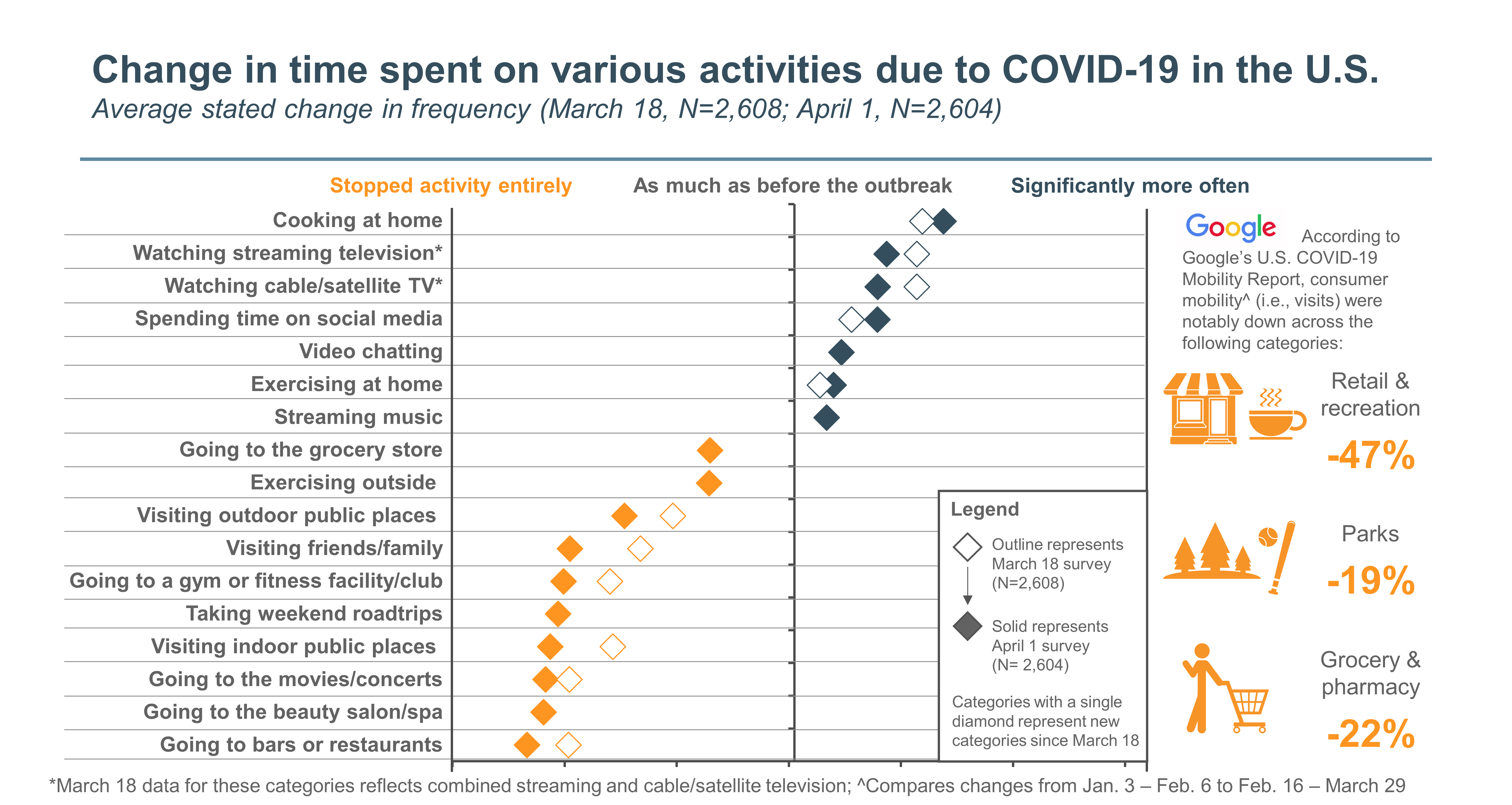

As social norms and restrictions evolve in response to COVID-19, consumers are increasingly adjusting their broader behaviors to limit their own exposure and protect others.

Naturally, consumers are reporting significant increases in at-home activities, particularly cooking at home, watching television, browsing social media, video chatting and exercising at home.

Consumers are limiting activities with high-exposure risk due to government restrictions and establishment closures, as is the case with bars/restaurants, gyms and events (e.g., the South by Southwest Conference). Also, self-imposed social distancing is driving a decline in traffic to public places (e.g., malls and stores, even grocery stores) and visits with friends and family.

Over the past two weeks, consumers indicate they have spent more time cooking, engaging with social media, and exercising at home. Unsurprisingly, time spent visiting outdoor places, going to the gym and seeing friends has continued to decline since March 18.

It remains uncertain which, if any, of these behavioral changes will persist once the COVID-19 outbreak is contained. In the near term, these changes create a need for brands to explore how they can meet consumers where they are and engage with them in novel ways. Whether it is through a live digital fitness class or expanded social media activity, brands are finding opportunities to maintain engagement.

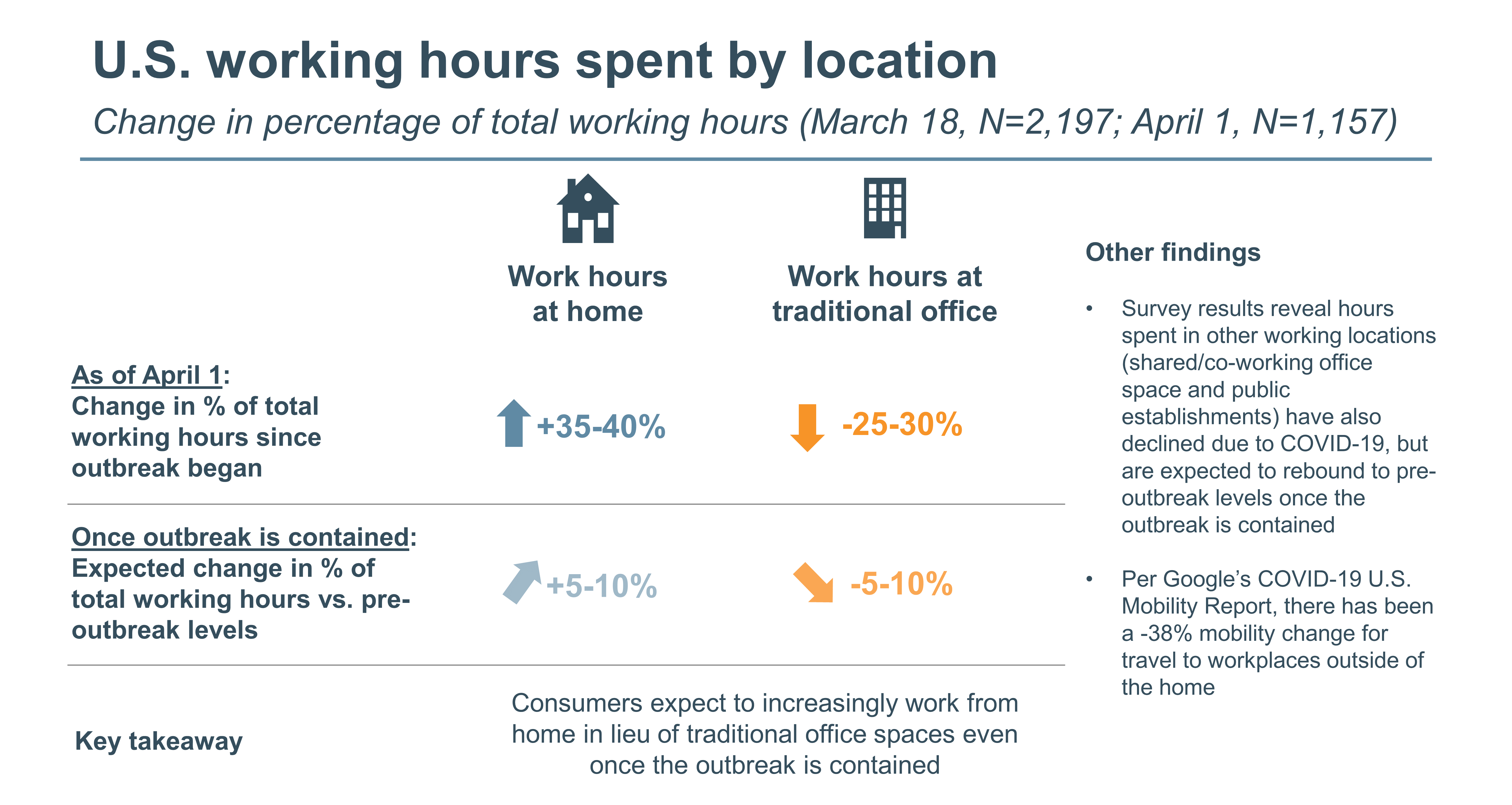

Where employees work has also been impacted by this crisis and may be impacted longer term.

During the outbreak, the percentage of working hours conducted at home has grown while working hours in all other locations (traditional offices, shared/co-working offices and public establishments) are down.

When asked to imagine a post-COVID-19 future, consumers say they expect a lasting impact on their work locations, with hours spent working at home greater, and hours spent working in traditional offices lower than before the outbreak.

Hours spent in other working locations (shared/co-working office space and public establishments) have also declined due to COVID-19, but are expected to rebound to pre-outbreak levels once the outbreak is contained.

Stay tuned for additional analysis from Edition 2 of our survey regarding consumers’ expectations for a post-COVID-19 future, to be published later this week.

As a reminder, we’ll be conducting recurring consumer pulse surveys approximately every two weeks to continually monitor consumer attitudes and behaviors.

We understand that many of our clients are facing new disruptions and increased uncertainty in their business outlook. In addition to this work, all of our sector teams are preparing insights on how the latest developments are shifting consumer attitudes, international business flows, commodities pricing and commercial priorities. Some of these changes are likely to endure well after the current pandemic has passed. While many of these changes will create challenges, there will also be new opportunities that emerge. We will be sharing our ideas and insights through our website and other media over the coming days and weeks.

We wish good health to you and your loved ones, and we look forward to continuing to support our clients through this difficult time.

To continue the discussion, please don’t hesitate to contact us.