L.E.K. Consulting’s Southeast Asia practice is publishing a series of insights fielded by Lucid on the changes in consumer behaviour in Southeast Asia and India (together referred to as “SEA” in this report) following the novel coronavirus outbreak. Through these reports, we aim to detail the impact of COVID-19 on the consumer markets in the region. We acknowledge that COVID-19 poses a humanitarian health crisis and a challenge, unlike any other the modern world has witnessed. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this pandemic.

Edition 1: 10 April 2020 survey results

The COVID-19 outbreak has universally challenged all sectors and industries — each is faced with significant shifts in consumer and user behaviour.

“COVID-19 in SEA: Consumer Insights for Businesses” is a series of insights reflecting the results of a recurring consumer pulse survey. Administered approximately every month, the survey tracks the pandemic’s impact on consumer sentiment overall, as well as by segment, geography and product. Each edition offers an updated perspective on the current landscape and what the lasting impact is likely to be. To continue the discussion, please don’t hesitate to contact us.

Edition 1 reflects survey results from week ending 10 April 2020. The sample size of roughly 3,000 SEA consumers is representative of various age groups and occupations.

Containing the risk

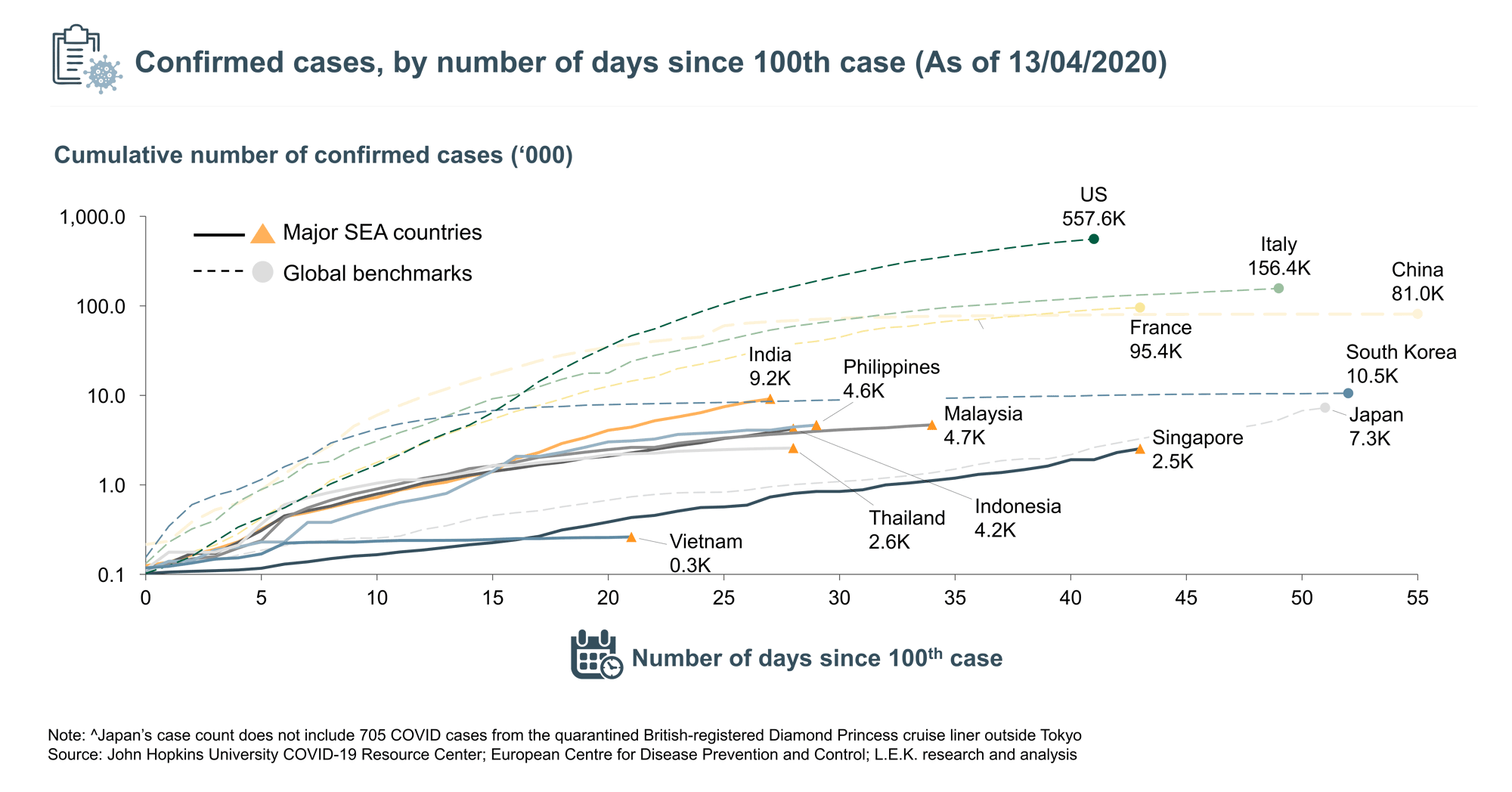

SEA countries have been quick in instituting measures to contain the viral spread. In most cases, healthcare systems in the region are not robust enough to support a full-blown epidemic and hence governments have endeavoured to be proactive. By adopting stringent and pre-emptive measures like lockdowns, circuit breakers and movement control orders, most SEA countries have managed to contain the impact on health of their populaces. As compared to epicentres like Spain, Italy and the U.S., the number of cases and deaths as a result of the virus have been considerably lower. However, the tremors of the outbreak are still felt in the region, with an increasing patient count in countries like India and even well-managed Singapore.

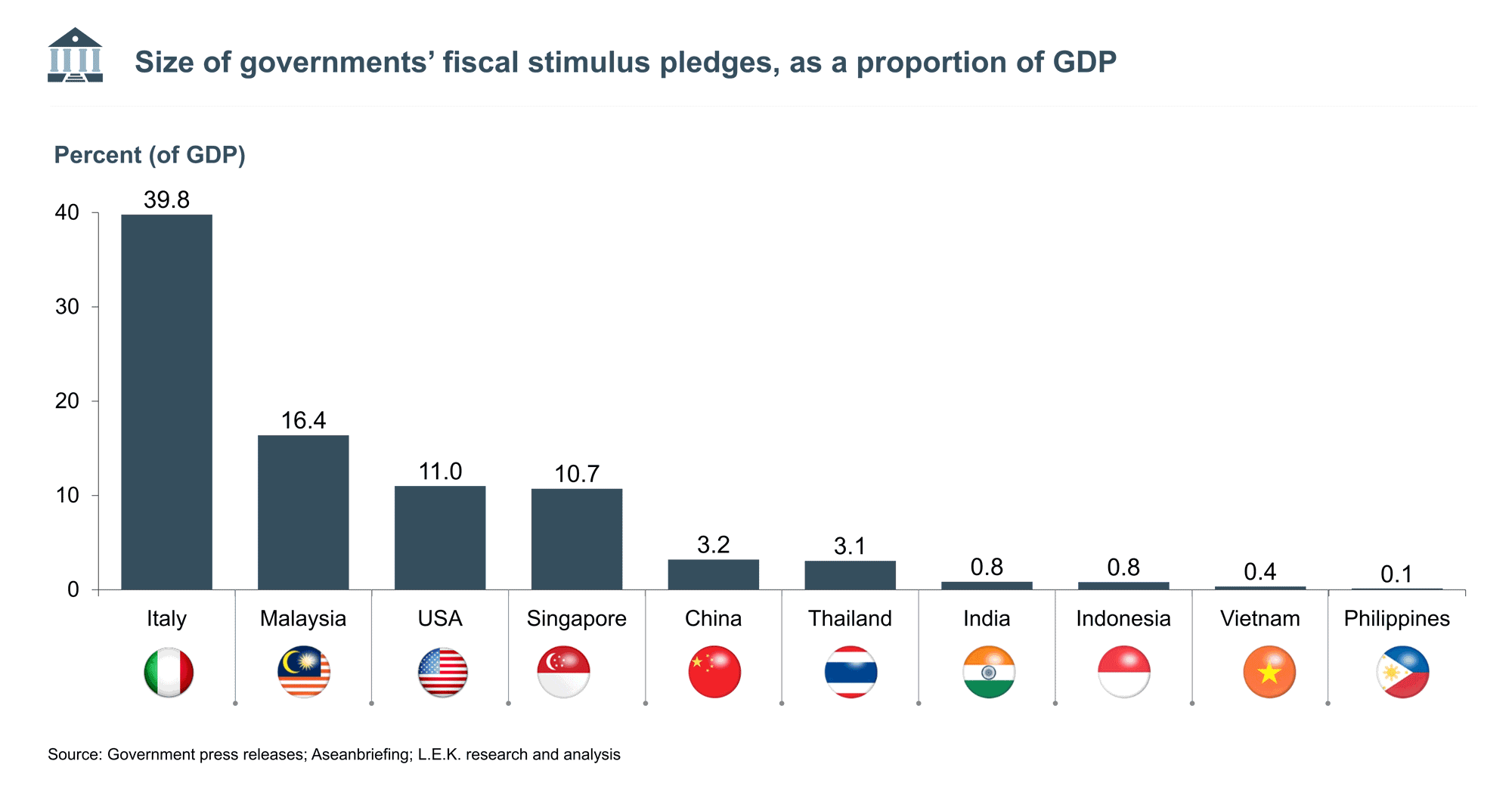

Injecting fiscal aid

To offset the predicted negative GDP growth forecast, most Southeast Asian countries have announced large stimulus packages through state loan and tax deferrals schemes. These measures will benefit the corporate entities and households in the region by ensuring subsidies, credit guarantees and a moratorium on loan repayments to afflicted stakeholders. Richer SEA countries such as Singapore and Malaysia have made significant fiscal commitments to support their economies, while emerging SEA countries have pledged smaller amounts (see Figure 1).

While governments try to instil confidence in industry participants, substantial economic impact already felt across various sectors is indicative of the demand trends to follow in the immediate future — possibly so even after the epidemic recedes.

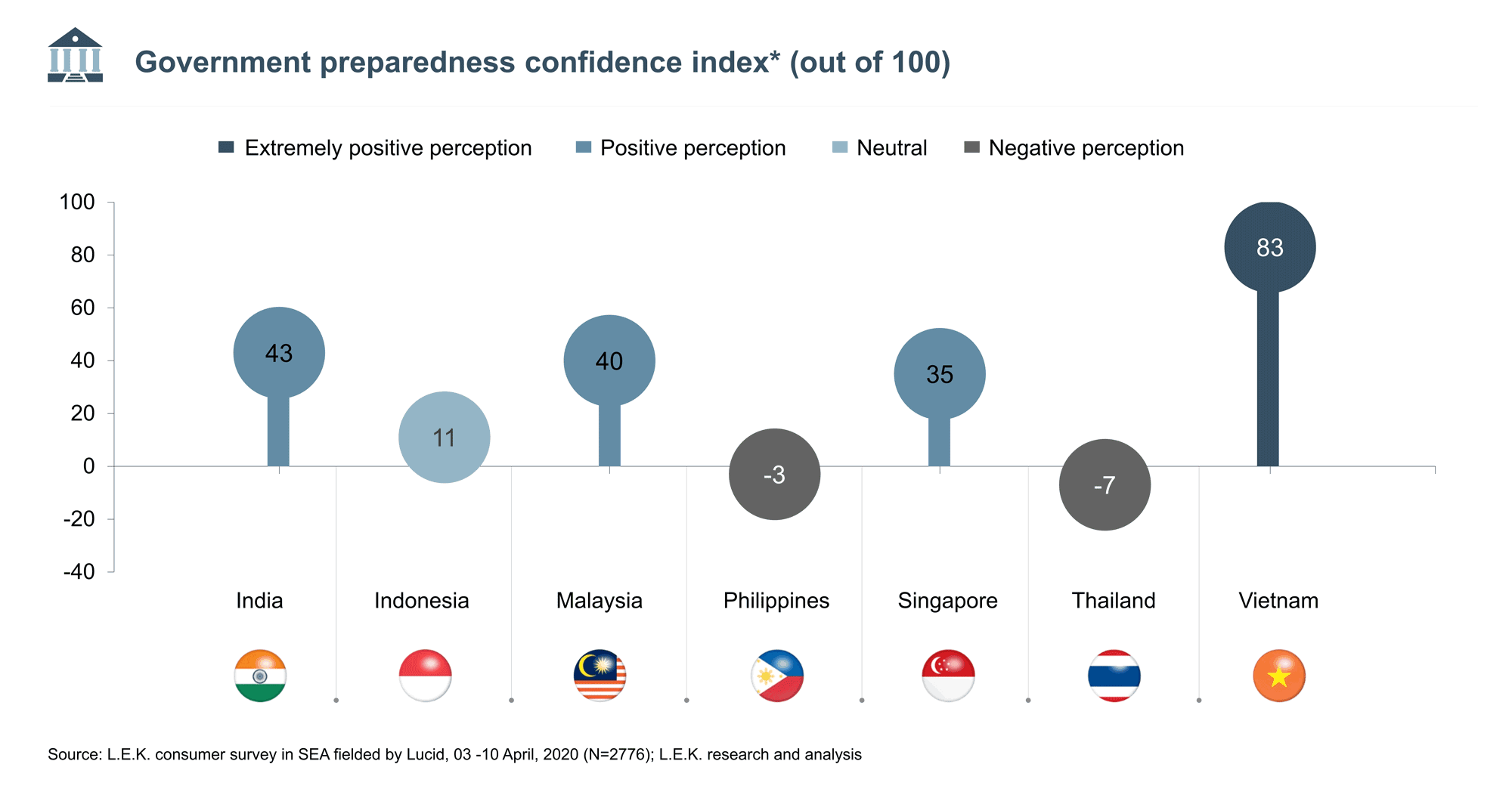

Consumers’ overall confidence levels in their governments’ preparedness to deal with the crisis was found to be highly correlational with how decisive the respective government was in imposing measures that would flatten the curve of the outbreak (see Figure 2). For example, in the case of Vietnam, 83% of respondents expressed high levels of preparedness, which could be linked to the proactive restrictions and testing measures adopted early on. In the case of Thailand, the delay in implementation of lockdown measures was found to be taking a toll on reassurance in government measures, whose confidence index was at -7%. Similarly, a second wave of infections in Singapore appeared to have reduced the population’s confidence in their government, with confidence index at 35, below Malaysia’s and India’s.

Survey findings and consumer behaviour

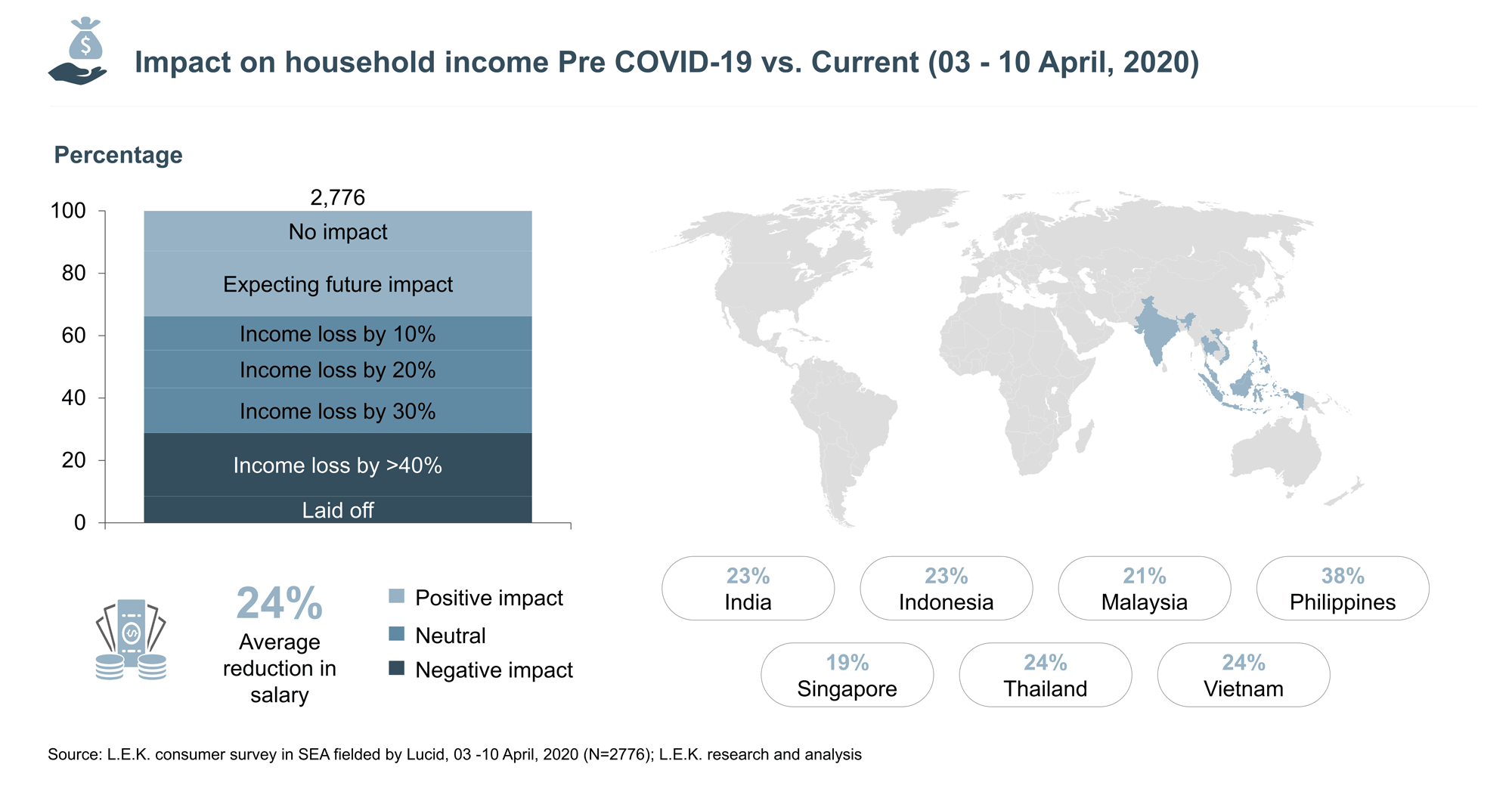

We surveyed ~3,000 consumers in India, Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam. These nations have taken early measures and enforced restrictions on movement, leading to lower numbers of cases and deaths relative to many Western countries. Although the spread of COVID-19 is relatively nascent in these markets (see Figure 3), our research indicates that incomes have already seen a significant impact, with respondents across countries reporting with an overall 24% reduction in salary across all countries. In particular Philippines, which has been in lockdown the longest, stands out with nearly 40% reduction in household incomes. Furthermore, 15%-30% of the respondents are expecting future impact on their compensation figures (see Figure 4).

The data in SEA appears to be consistent with official numbers coming from other parts of the world including the U.S., where nearly 10% of the labour force has lost their jobs.1

Furthermore, consumers across the region believe that the pandemic will peak in five to seven months.

The recent developments have translated to major ramifications on various sectors in the region. Our respondents’ buying behaviour is indicative of the general norm across the following markets.

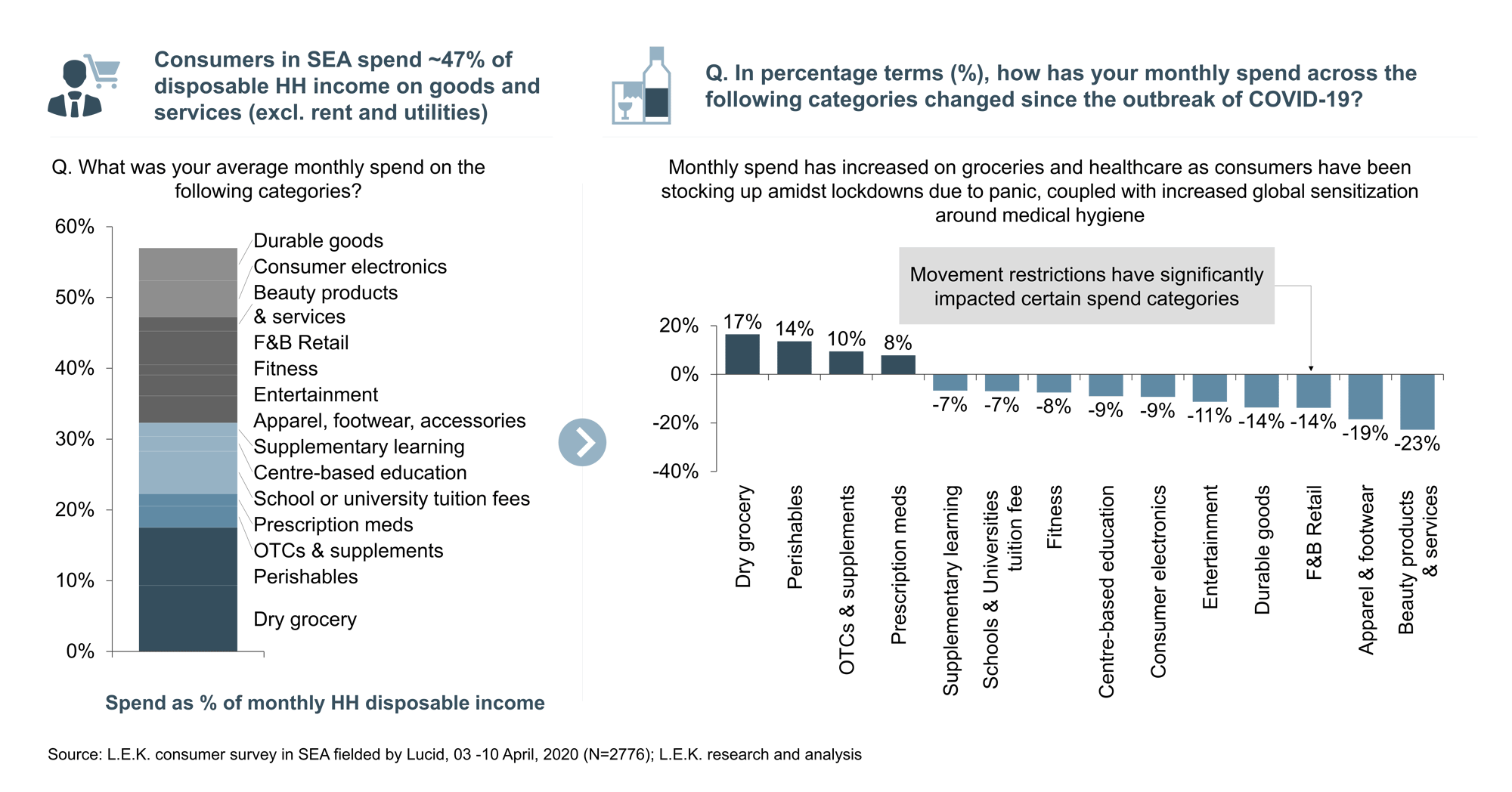

Groceries and healthcare products

Consumers in SEA (which includes India) spend ~25% of their disposable household income on essentials. With respondents allocating more of their monthly spend on groceries, perishables and healthcare products post COVID-19 across all countries, demand patterns have substantially risen (see Figure 5).

Due to bulk buying of products, driven by panic around partial or complete lockdowns, respondents have been quick to stockpile supplies for the near future. This stockpiling has not only been limited to fresh food and groceries, but also to healthcare products, especially over-the-counter drugs and preventive consumer health products as well as prescription medicines.

Discretionary purchases

Non-essential segments of apparel, beauty products and services, and durable goods such as furniture have seen the largest spending declines (see Figure 5). The declines are a result of (a) consumers deferring purchases, and (b) lack of access to physical stores due to lockdowns, both of which are critical to the buying process for these categories.

Food and beverage retail, entertainment and fitness

While conventional models in these sectors broadly book losses across all countries, more than 50% of respondents have switched to “at-home” substitutes, such as ordering take-out food or subscribing to online entertainment platforms (see Figure 5).

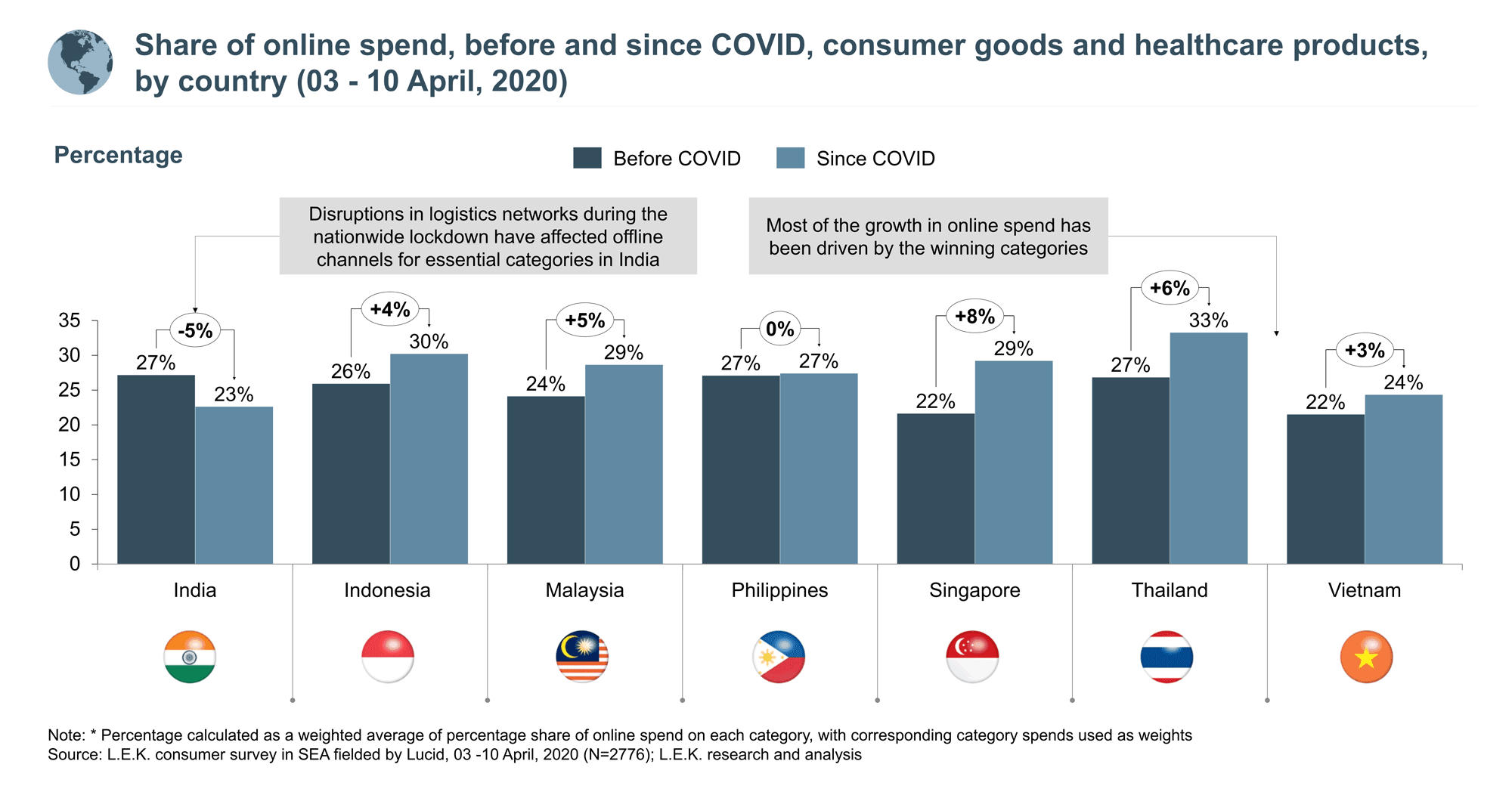

Overarching online trends

Our survey also shows an increasing trend towards online shopping. While this is to be expected, it is interesting to note that the increase is not as significant as many have been predicting. The lockdowns have impacted delivery and logistics capabilities, an issue quite pronounced in India for non-essential products, leading to an overall decrease in e-commerce (see Figure 6).

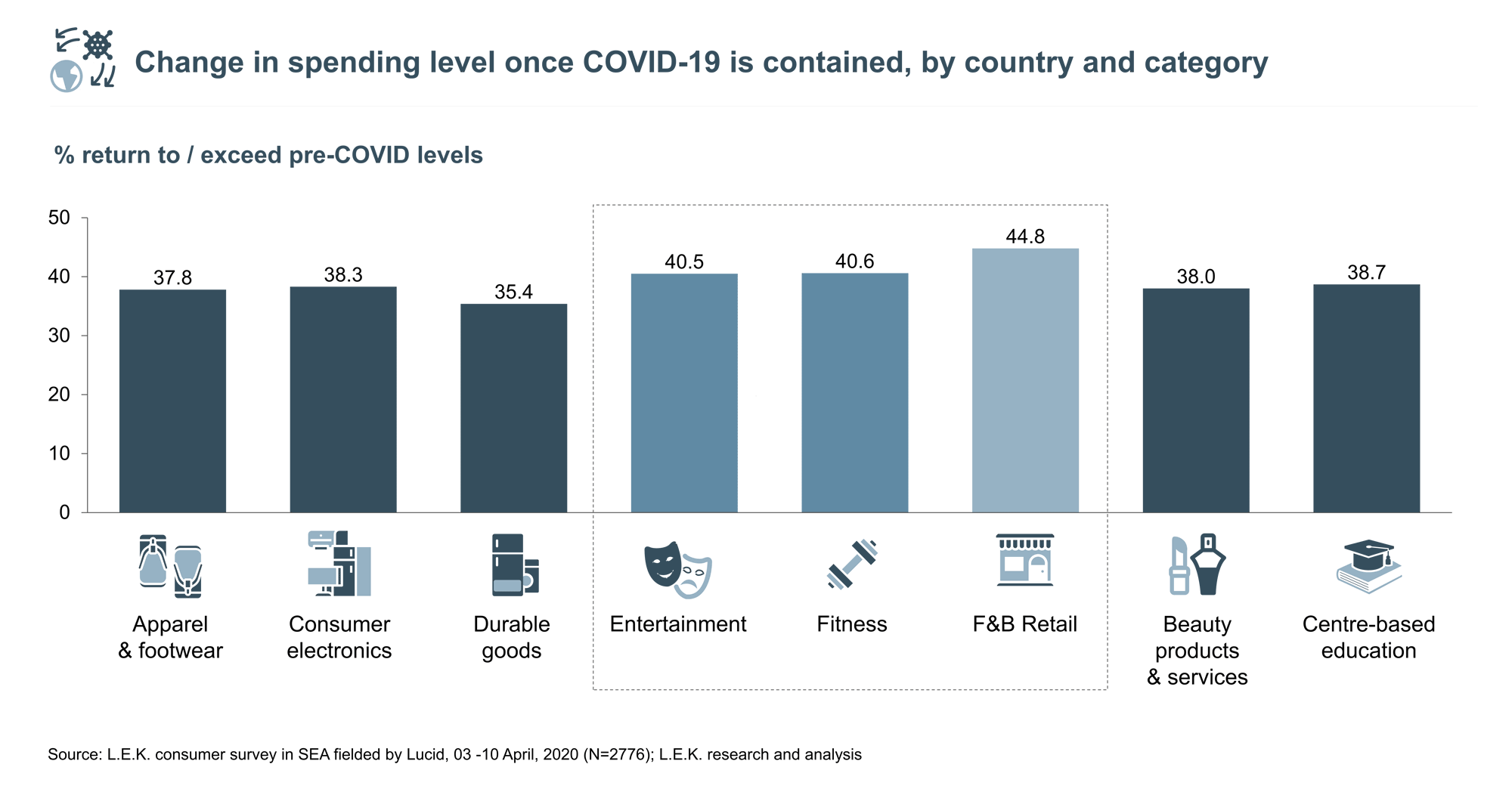

Rebounding from the slump

In our survey, consumers across the various countries consistently stated that they expected the COVID-related crisis to last five to eight months (with Singapore’s estimate of 10 months being the longest). Even after the crisis recedes, damage to consumer budgets brought on by decreased household incomes and consistent expenditures may persist in the medium term. However, social and experiential activities are likely to bounce back faster than other sectors, as consumers would be motivated to spend time in social settings, after having been out of contact with peers for prolonged periods (see Figure 7).

Our survey also discovered that respondents from different income brackets have proportionately increased spending on essential items, but high-income individuals have led excess buying of essential items. While non-essential items have been overlooked by all income groups in the current climate, the percent decrease in spending across these sectors is highest for the mid-income segment.

The most common question in many business owners’ minds is about the speed and shape of the recovery. Our research supports the theory that while possible for select categories, V-shaped recovery in the broad SEA consumer space is unlikely. The severity of the shutdown experienced by the SEA and indeed the global economy is being underestimated by many economists and market experts. While it is still too early to tell and outcomes will be determined by medical progress, our current view is of a gradual recovery starting Q3 2020 over the next three to four quarters is more likely (or a U-shaped recovery). However, there is still a lack of visibility and we expect to refine our outlook over time. Moreover, each consumer category can be expected to see different recovery curves.

An update on the data presented above will be published in the coming weeks. Watch this space to track market trends across Southeast Asia.

Endnote:

1Financial Times, “Markets and economists are still too upbeat on coronavirus,” 14 April 2020.

01262022160149