Key takeaways

-

It is critical for biopharma companies to have a robust National Comprehensive Cancer Network (NCCN) strategy that encompasses multiple cross-functional stakeholders across all stages of a drug’s life cycle to maximize the patient and commercial impact of lifesaving cancer treatments.

-

NCCN recommendations are considered to be the gold standard for public and private insurers to use in making coverage decisions for both labeled and off-label use of new and existing oncology medicines.

-

NCCN recommendations drive drug adoption in earlier lines of therapy and in other indications (i.e., beyond primary/registrational indication), including off-label use.

-

In this Executive Insights, we discuss best practices that innovative biopharma companies should pursue to reinforce a company’s NCCN submission and maximize reimbursement, access and adoption in the oncology marketplace.

National Comprehensive Cancer Network (NCCN) recommendations are considered to be the gold standard for public and private insurers to use in making coverage decisions for both labeled and off-label use of new and existing oncology medicines. NCCN recommendations drive drug adoption in earlier lines of therapy and in other indications (i.e., beyond primary/registrational indication), including off-label use. It is critical for biopharma companies to have a robust NCCN strategy that encompasses multiple cross-functional stakeholders across all stages of a drug’s life cycle to maximize the patient and commercial impact of lifesaving cancer treatments.

Oncology is an extremely attractive market for biopharma companies. Total worldwide sales are expected to grow from ~$125 billion (~15% of total worldwide market share) in 2018 to ~$235 billion (~20% of worldwide market share) in 2024, which is a compound annual growth rate (CAGR) of ~11%.1 Additionally, ~35%-40% of blockbuster drugs launched between 2011 and 2016 were oncology drugs,2 and most came with a high price. However, despite recent advances in drug development, there is still a significant unmet need across almost all cancer types, driving a significant amount of R&D investment and a large pipeline with thousands of drugs under development by hundreds of companies. Consequently, these complex dynamics impose unique planning challenges for biopharma companies such as:

- Driving or catching up with the rapid pace of innovation (e.g., emergence of biomarker-based pan-tumor therapies) and evolving treatment paradigms such as targeted therapies3 and staged treatment

- Navigating the uncertain, expensive and long FDA approval process

- Gaining favorable payer coverage in an increasingly competitive and value-focused environment

- Maximizing the addressable patient population size

- Facing fierce competition across all stages of a drug’s life cycle

- Planning and managing indication expansion to extend a treatment’s life cycle and finally

- Securing payer coverage for use beyond the FDA-approved label (i.e., “off-label” or “expanded indication,” which is a significant component of many successful oncology treatments)

Some of these challenges also complicate decision-making for physicians (e.g., choosing among treatments and making sure they are covered by insurance), patients (e.g., deciding between competing options), employers (e.g., determining how to provide appropriate access to novel treatments), and government, as well as private payers (e.g., deciding on the appropriate level of access to provide).

Importance of CMS-recognized drug compendia

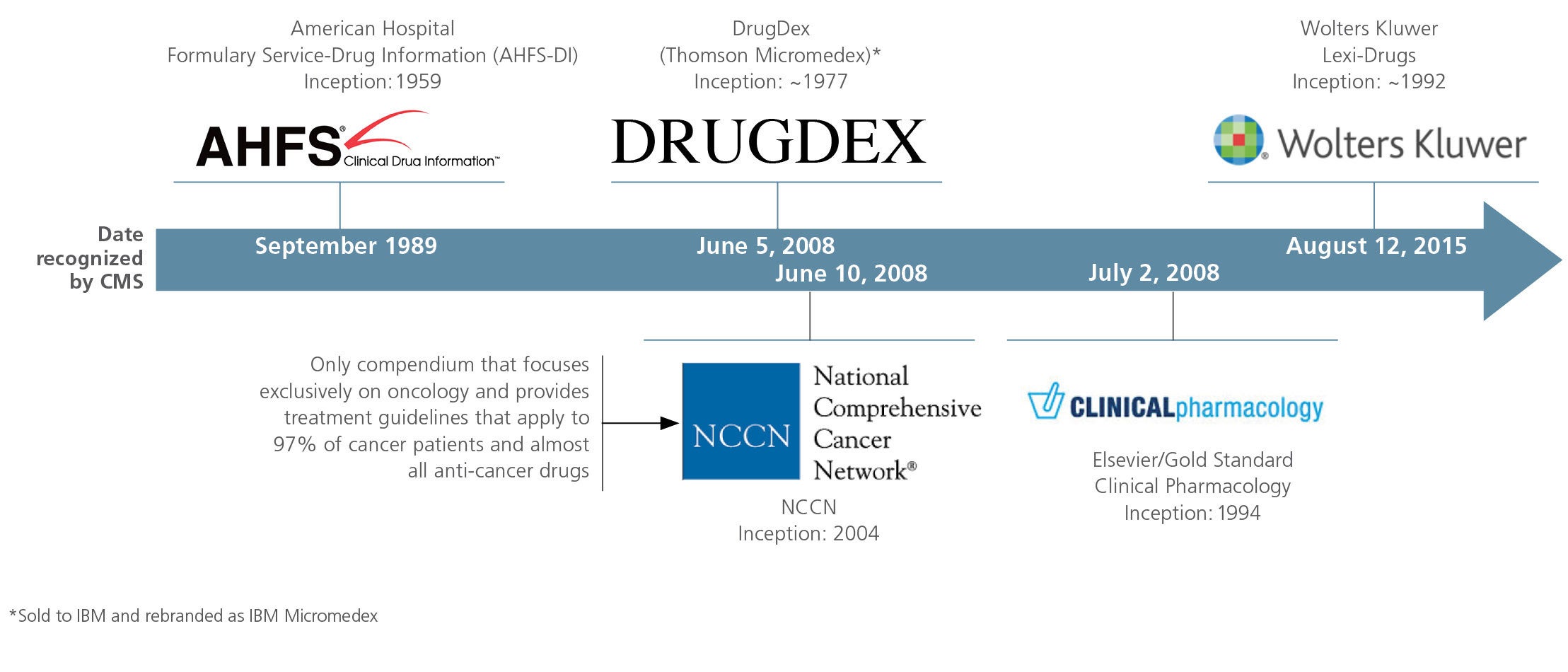

To help navigate the complexities mentioned above, several organizations have developed drug compendia that contain information compiled by experts based on clinical evidence about the drug’s characteristics (e.g., pharmacologic profile, dosage, clinical performance) and that may include recommended uses. Currently, there are five drug compendia recognized by the Centers for Medicare and Medicaid Services (CMS) for use in the determination of medically accepted indications and to inform coverage decisions (see Figure 1).

The guidelines or recommendations for clinical use made by these compendia have a substantial impact on both government coverage determinations and private payer coverage, including national or regional coverage decisions. Further, reimbursement of each drug’s use beyond its FDA-approved label (i.e., off-label use) is typically provided if at least one of the five compendia determines the use is medically appropriate. Given the importance of drug compendia recommendations and their impact on patient access, it is critical for biopharma companies to have a well-planned and comprehensive “drug compendia strategy.”

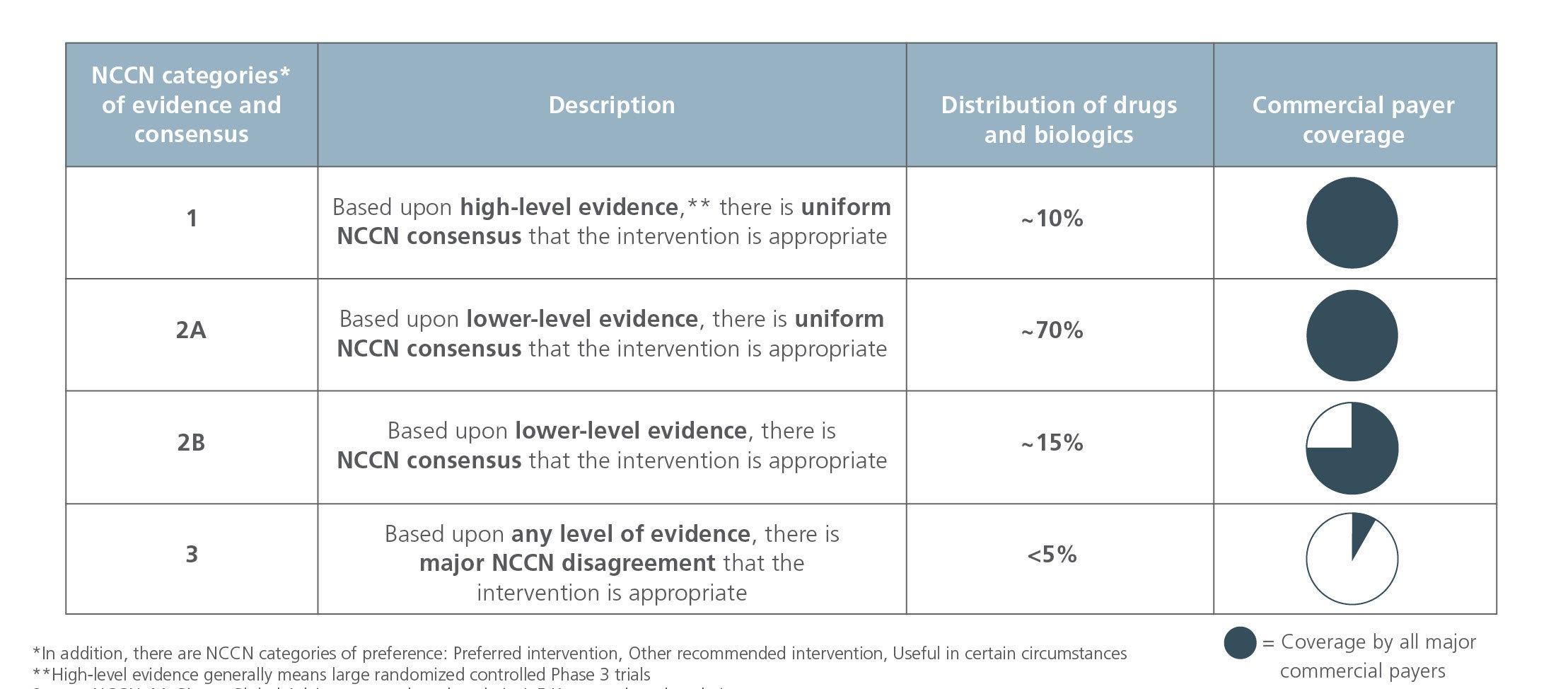

Among the five CMS-recognized drug compendia, NCCN is the only one to focus exclusively on oncology. NCCN, with its alliance of 28 member institutions, including more than 1,300 clinicians and researchers, and its evidence-based and iterative guidelines and consensus-driven management, is considered by clinicians and payers as the gold standard for oncology drug evaluation and use. (UnitedHealthcare, for example, has tied its oncology coverage decisions exclusively to NCCN guidelines since 2008.) The development of NCCN guidelines that cover 97% of cancers affecting people in the U.S. and more than 5,000 entries in the compendium is based on a comprehensive and frequently updated review of the best available clinical evidence. Biopharma companies can file a de novo submission of data for a new drug with its first indication for NCCN evaluation or can request to propose new data or clinical evidence for an approved drug’s performance in a new line of therapy or cancer type. A multidisciplinary panel of experts assesses the submission based on the level of clinical evidence (i.e., quality, quantity, consistency of the data) and then derives a recommendation based on four categories (see Table 1). A unanimous positive consensus will grant a category 1 or 2A (the most common) recommendation, which ensures coverage by all government and major commercial payers. Conversely, a category 3 recommendation (i.e., the lowest) does not support coverage from most major payers. NCCN submissions and subsequent recommendations are independent of FDA approvals and can be pursued before or after those approvals. Further, most payers cover off-label use of oncology drugs that have a category 1, 2A or 2B recommendation from NCCN. Given the significant impact of NCCN recommendations on coverage and patient access, it is critical for biopharma companies to consider the importance and timing of guideline and compendia submissions at both the pre-launch and post-launch/life cycle management stages.

Commercial impact of NCCN recommendation

To better understand the impact of NCCN submissions and guidelines on commercial performance, we assessed two discrete scenarios in which an NCCN recommendation significantly impacted a drug’s addressable patient population size: (a) indication expansion (i.e., a new cancer type) and (b) advancing line of therapy.

a. Indication expansion

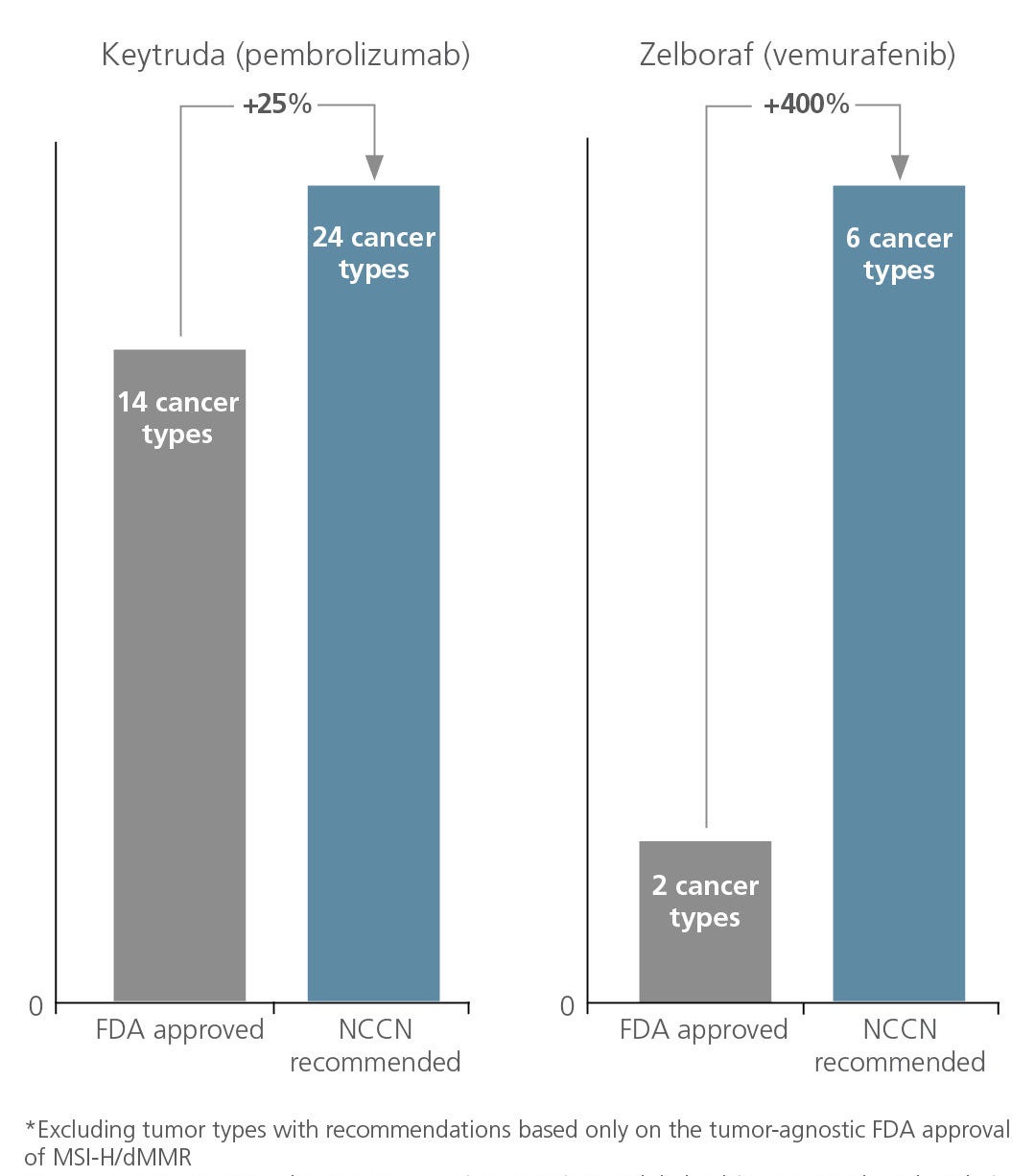

Indication expansion is a common strategy for biopharma companies to pursue in order to extend the life cycle of their cancer therapy, especially as they continue to accumulate clinical data through “real-world evidence” or through investigator-initiated or company-sponsored studies. Two example drugs help illustrate this opportunity: (1) Keytruda (pembrolizumab) and (2) Zelboraf (vemurafenib).

- The FDA has approved Keytruda, a blockbuster checkpoint inhibitor from Merck, for 14 tumor types.4 Based on our analysis, the company secured NCCN recommendations for an additional 10 tumor types, which resulted in a potential increase of 20%-30% in addressable patient population size (see Figure 2). Merck conducted more than 25 clinical trials5 and published multiple scientific articles showcasing the clinical evidence for the drug’s use beyond FDA-approved indications.

- Roche/Genentech secured FDA approval of Zelboraf first for late-stage melanoma in 2011, and then for Erdheim-Chester disease in 2017. Based on our analysis, the company secured NCCN recommendations for four additional tumor types, which resulted in a potential increase of 200%-300% in addressable patient population size (see Figure 2). We observed that the manufacturer pursued at least five clinical trials for Zelboraf following the first FDA approval, including a basket study of several rare malignancies, and published the results in at least four peer-reviewed journal articles between 2015 and 2017. The NCCN recommendation for Zelboraf use6 in metastatic colorectal cancer came in August 2017, citing clinical evidence from an investigator-initiated Phase 2 randomized controlled study that was presented at the 2017 ASCO Gastrointestinal Cancers Symposium.

b. Advancing line of therapy

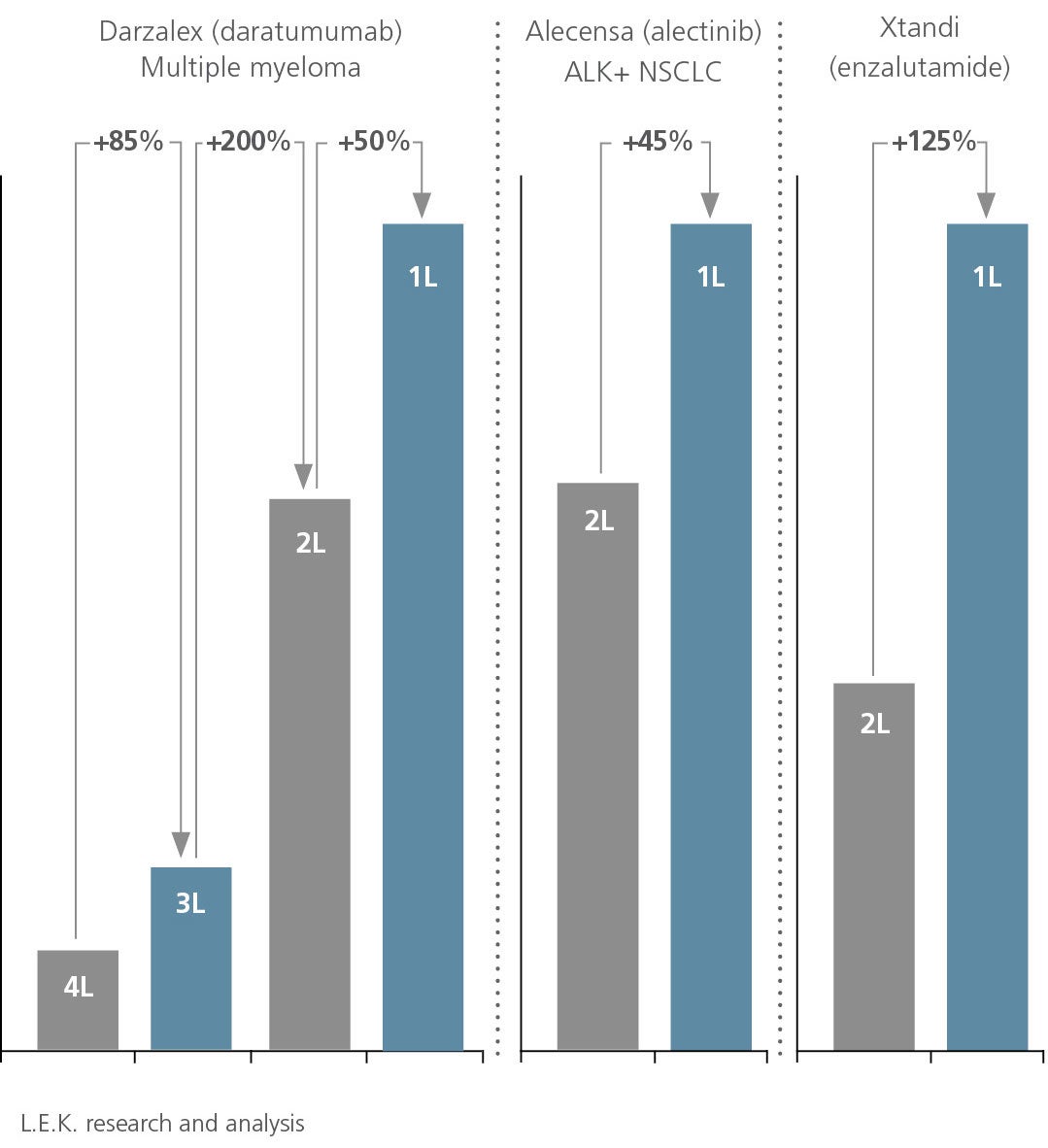

Groundbreaking discoveries in cancer disease biology and targeted therapies have resulted in a dramatic shift in oncology treatment. Various drugs are now used across different lines of therapy (e.g., staged) for different disease subpopulations (e.g., different levels of severity), including combination therapies. The increased competitive intensity and the “race to the market” have resulted in a large portion of drugs failing to achieve the full commercial potential at launch (i.e., lacking a label that maximizes the addressable patient population size). As a result, biopharma companies have increasingly pursued attempts to advance their drugs’ use in earlier lines of therapy and to extend their life cycle and potential. We examined the impact of NCCN recommendations about advancing the line of therapy on the addressable patient population size, along with a timeline of NCCN recommendations relative to FDA approval for three drugs: (1) Darzalex (daratumumab), (2) Alecensa (alectinib) and (3) Xtandi (enzalutamide).

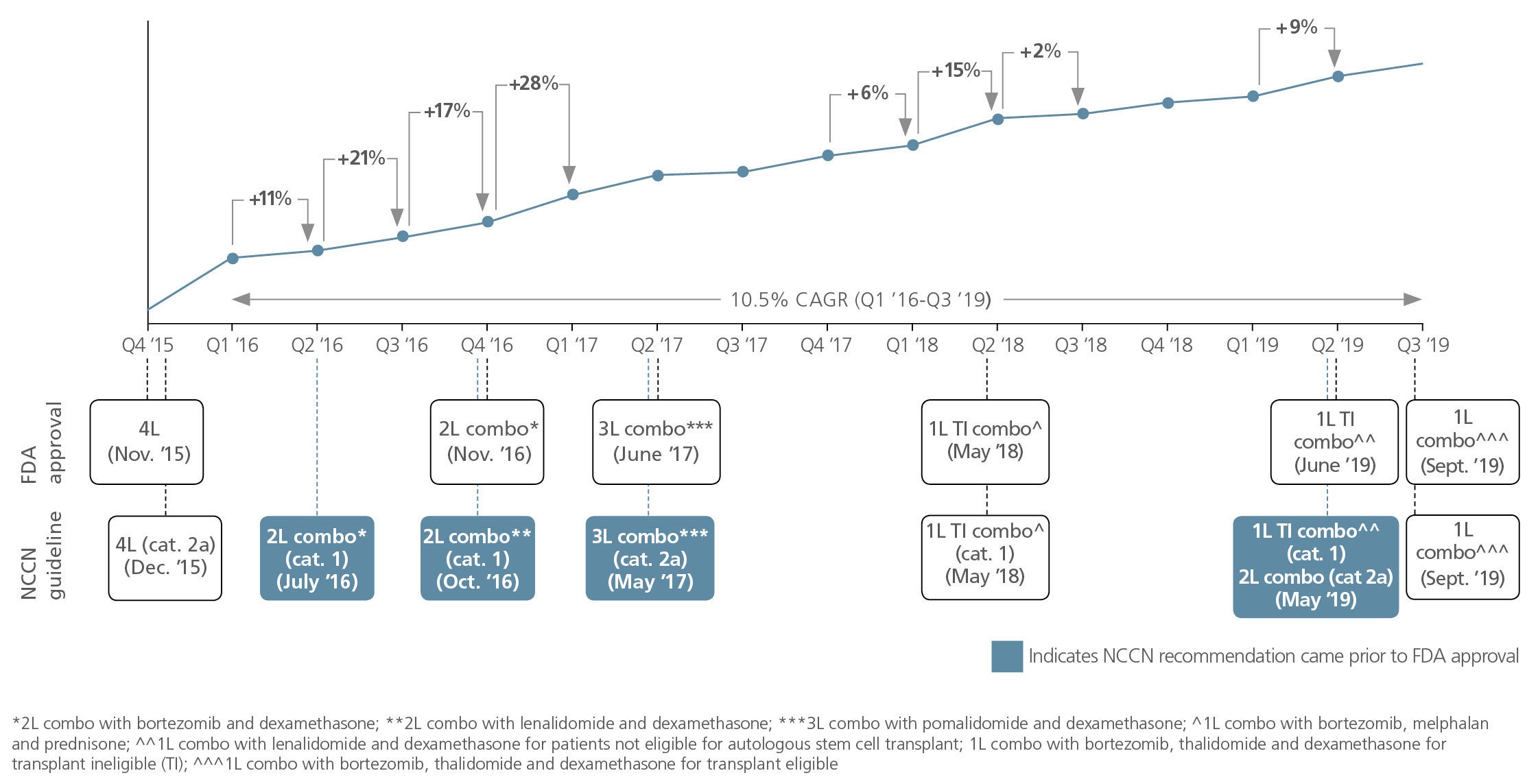

- Darzalex first secured FDA approval for fourth-line treatment for multiple myeloma (see Figures 3 and 4A). However, within one year of approval, Janssen pursued an NCCN recommendation for second-line treatment (2L) and obtained a category 1 recommendation, which resulted in sales volume uplift of 25% within three months, aligned with the publication of clinical trial results demonstrating the drug’s use in an earlier line of therapy. FDA approval for 2L came approximately six months after the NCCN recommendation. In aggregate, Janssen obtained eight NCCN recommendations, including two without any FDA approval, three that came prior to FDA approval and three that came after FDA approval. All NCCN recommendations aligned with publications demonstrating clinical evidence (from at least four additional Phase 3 clinical trials) in support of advancing the drug to an earlier line of therapy. These advancements in line of therapy collectively increased the addressable patient population size seven or eight times compared to the size of their first launch (see Figure 4A).

Figure 4A

Timeline of treatment line progression and sales volume uptake

Darzalex (multiple myeloma)

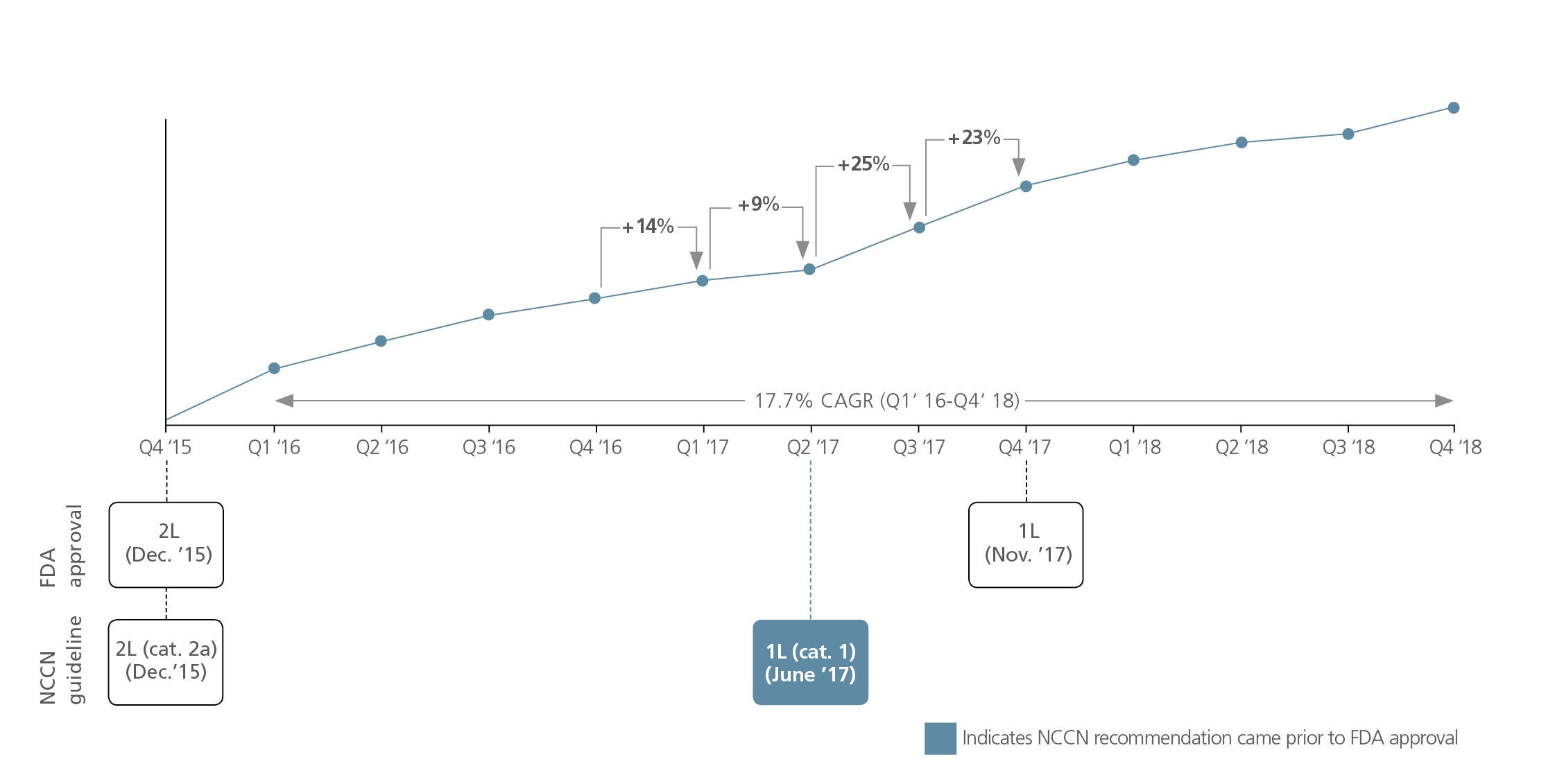

- Chugai/Roche’s Alecensa (alectinib) first secured FDA approval in second-line ALK+ NSCLC, after which the manufacturers pursued an NCCN recommendation for first- line treatment following the results of a Phase 3 trial. This category 1 NCCN recommendation resulted in a sales volume uplift of 25% in the next quarter and an overall increase in addressable patient population size of 40%-50% (see Figure 3). FDA approval came about six months after the NCCN recommendation (see Figure 4B).

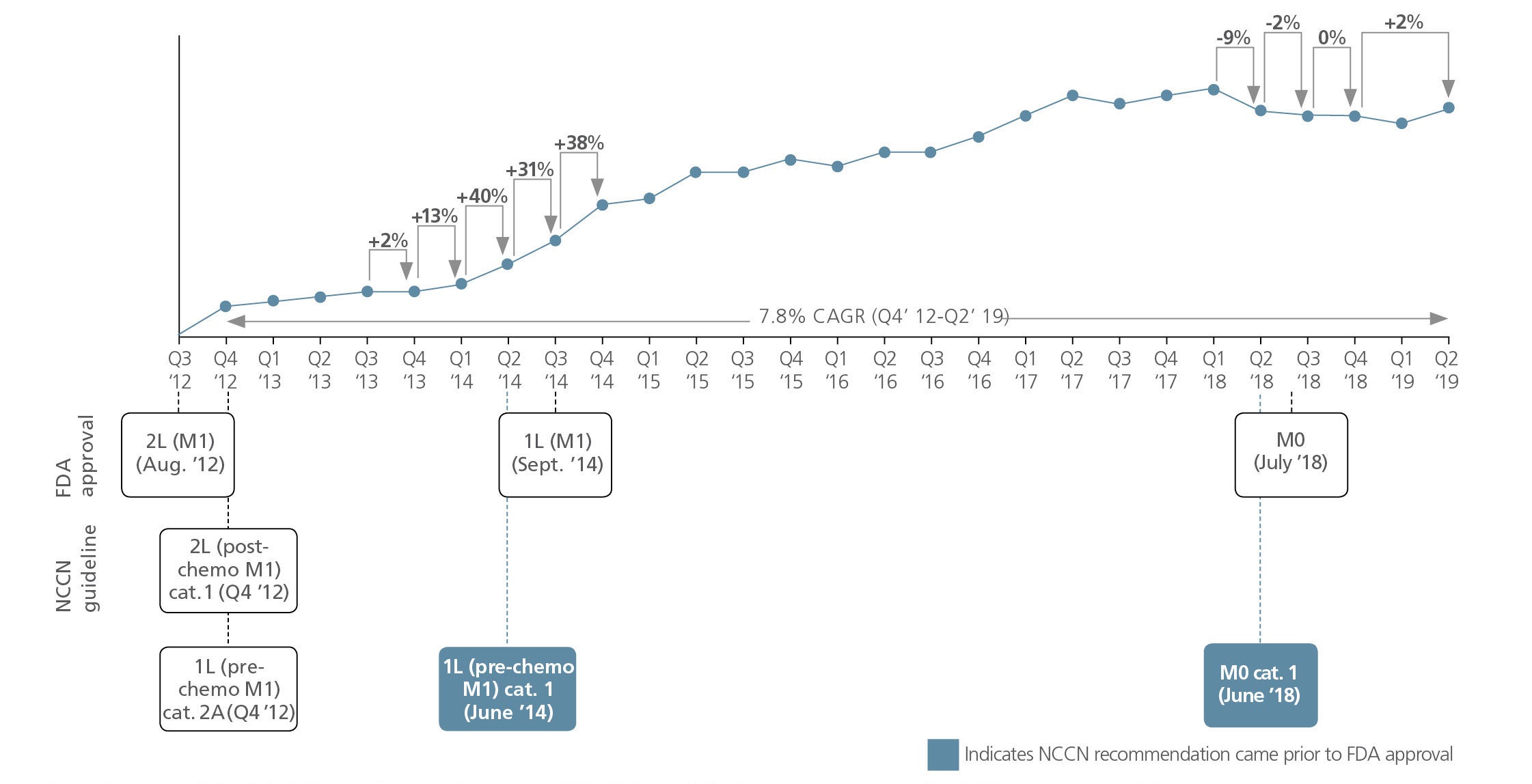

- We noticed a similar trend with Pfizer/Astellas’ Xtandi (enzalutamide) in metastatic castration-resistant prostate cancer (mCRPC). The NCCN recommendation for first-line (pre-chemotherapy) treatment preceded FDA approval, which resulted in sales volume uptake. Interestingly, the NCCN recommendation aligned with the publication of clinical trial results showing improvement in overall survival when Xtandi was used in first-line (pre-chemotherapy) treatment for mCRPC (see Figures 3 and 4C).

In summary, NCCN recommendations for drug use in earlier lines of therapy drove significant uplift for these drugs and, importantly, often preceded FDA approval.

Discussion

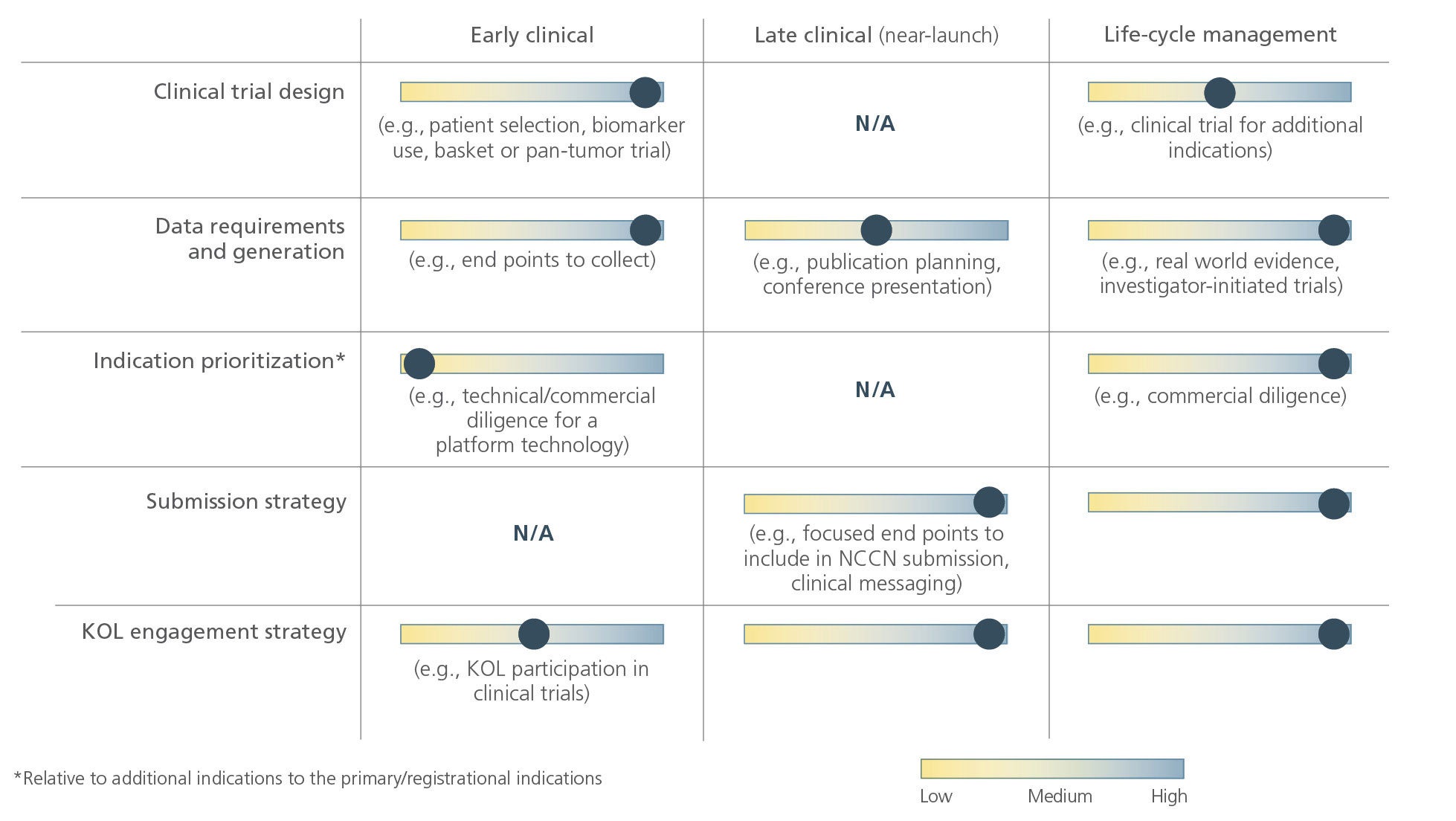

Our analysis clearly highlights the importance of a guideline and compendia submission timeline and favorable recommendations for a drug’s reimbursement coverage, access and adoption. Therefore, it is critical for biopharma companies to develop a world-class guideline and compendia strategy to maximize the impact of their products. A robust guideline and compendia strategy should encompass multiple departments (e.g., medical affairs, brand, market access) across all stages of a drug’s life cycle (see Figure 5).

Based on our experience, there are a number of best practices that innovative biopharma companies should pursue and integrate to maximize reimbursement, access and adoption. First, assess the data requirements within the targeted cancers (e.g., conducting analog drug analysis, benchmarking) to drive favorable NCCN review and integrate findings into the trial design. Second, as the drug advances through clinical trials, strategically articulate the emerging clinical evidence (e.g., conference presentations, publications), and emphasize validated end points and outcomes from large clinical trials in the NCCN submission. Third, as clinical evidence accumulates, start engaging key opinion leaders to gather their perspective on potential adoption and to conduct additional data collection and analysis, which can further reinforce the company’s NCCN submission. Fourth, explore opportunities to advance the drug to an earlier line of therapy and expand to additional indications through KOL research and real-world evidence gathering, and leverage investigator-initiated studies for NCCN submission (investigator-initiated studies are typically pursued following launch of the primary/registrational indication). Since off-label use based on clinical evidence and expert opinion is routinely assessed and recommended by NCCN, it creates significant opportunities for biopharma companies to maximize a drug’s impact.

In summary, it is critical for biopharma companies to develop their compendia and guideline strategy, including identifying data and evidence needs over time, by cancer type, line of therapy and off-label use. This will maximize public and private reimbursement, access, and ultimately adoption in the increasingly competitive oncology marketplace.

Endnote:

1EvaluatePharma World Preview 2019 report

2L.E.K. Launch Monitor

3L.E.K. Biomarker Database

4Excluding tumor types with recommendations based only on the tumor-agnostic FDA approval MSI-H/dMMR

5Initiated from 2014 onward

6Combination with cetuximab and irinotecan into the guidelines as a treatment option for patients with BRAF+, previously treated metastatic colorectal cancer

01082024090151