Key takeaways

-

Liquid biopsy applications span the entire cancer patient journey, from early detection to late-stage disease monitoring.

-

These applications may require one or a combination of the multiple liquid biopsy techniques that exist today.

-

The competitive landscape is broad and dynamic. Over 30 different liquid biopsy providers are operating in three market segments: early detection using circulating tumor DNA (ctDNA), therapy guidance using ctDNA, and particles and cells.

-

Liquid biopsy offers significant clinical utility as well as a market potential representing tens of billions of dollars.

A minimally invasive diagnostic that can help clinicians detect, diagnose and manage cancer patients has long been the dream of many healthcare practitioners. Over the past few years, highly sensitive molecular technologies — primarily Next Generation Sequencing (NGS) and digital PCR (dPCR) — have enabled researchers and clinicians to detect the presence of cancer genomic material (circulating tumor DNA or ctDNA) in peripheral biofluids, such as blood.

Alas, the field known as liquid biopsy was born on the backs of these novel molecular technologies. But liquid biopsy is not limited to ctDNA, and may include detection of other cancer-derived particles, including exosomes harboring tumor RNA and circulating tumor cells (CTCs).

Despite all the press and hype, the term “liquid biopsy” is often used without a precise understanding of its different applications and technological approaches. In this Executive Insights, we lay out the key clinical applications, describe the various liquid biopsy technologies and highlight key companies that are turning this dream into reality.

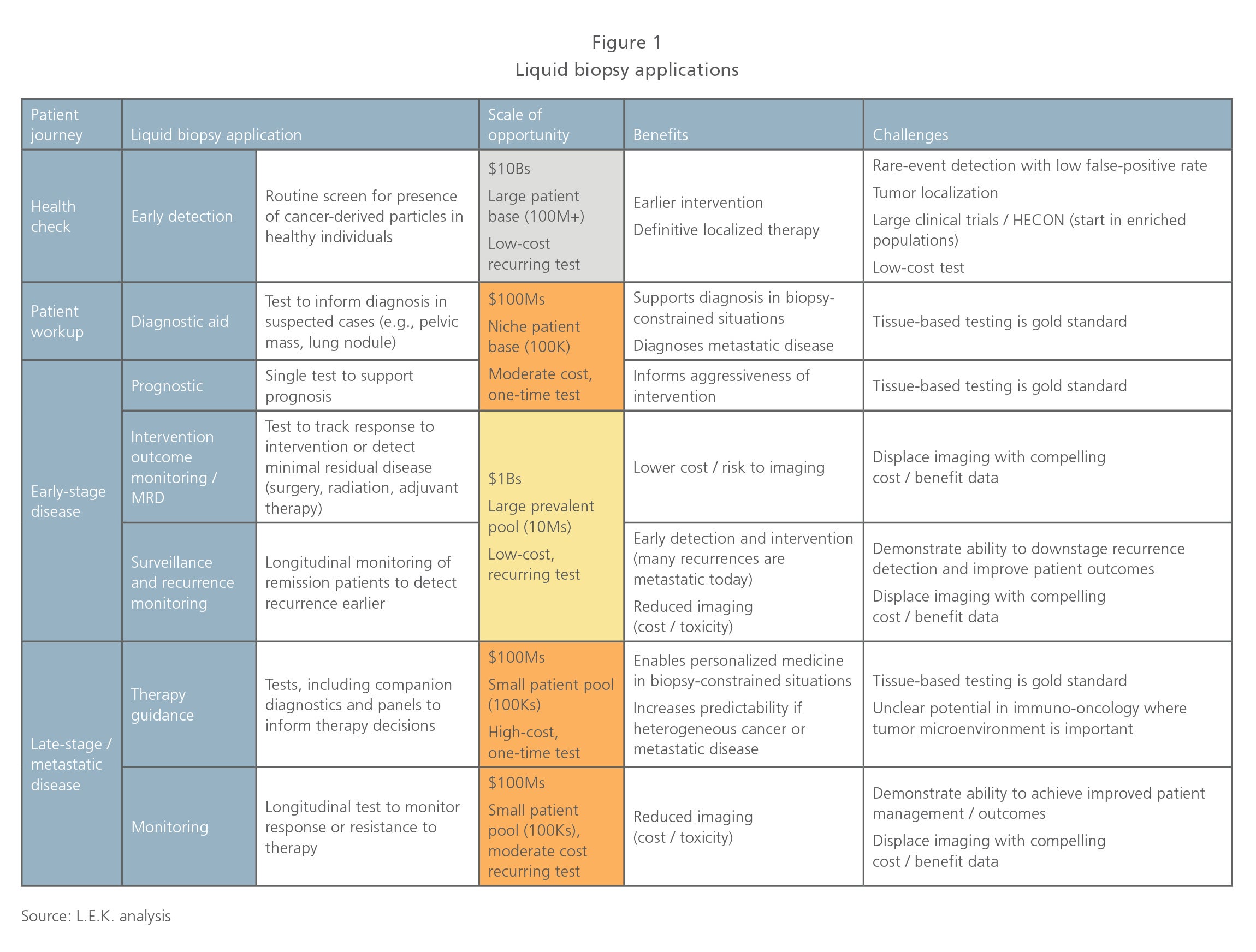

Liquid biopsy applications span the entire cancer patient journey

Liquid biopsies’ potential clinical applications are broad and span the entire cancer patient journey — from screening healthy individuals in hopes of detecting cancer early, all the way through profiling resistance to targeted therapies in late-stage treated cancer patients (see Figure 1).

While therapy guidance is the leading application today, monitoring and early detection are expected to represent the most sizable and impactful applications in the future. Early detection has the potential to downstage cancer detection, enabling definitive intervention (e.g., full tumor resection), and could become a routine part of health checks, similar to mammograms and colonoscopies. Monitoring applications are myriad and have the potential to reduce the current dependence on imaging, as well as potentially detect recurrence or resistance earlier than traditional approaches, again enabling earlier intervention or changes in management.

In aggregate, analysts estimate the market potential for liquid biopsy applications to represent tens of billions of dollars, making liquid biopsy one of the most scalable opportunities diagnostic companies have encountered in decades.

Multiple liquid biopsy techniques exist

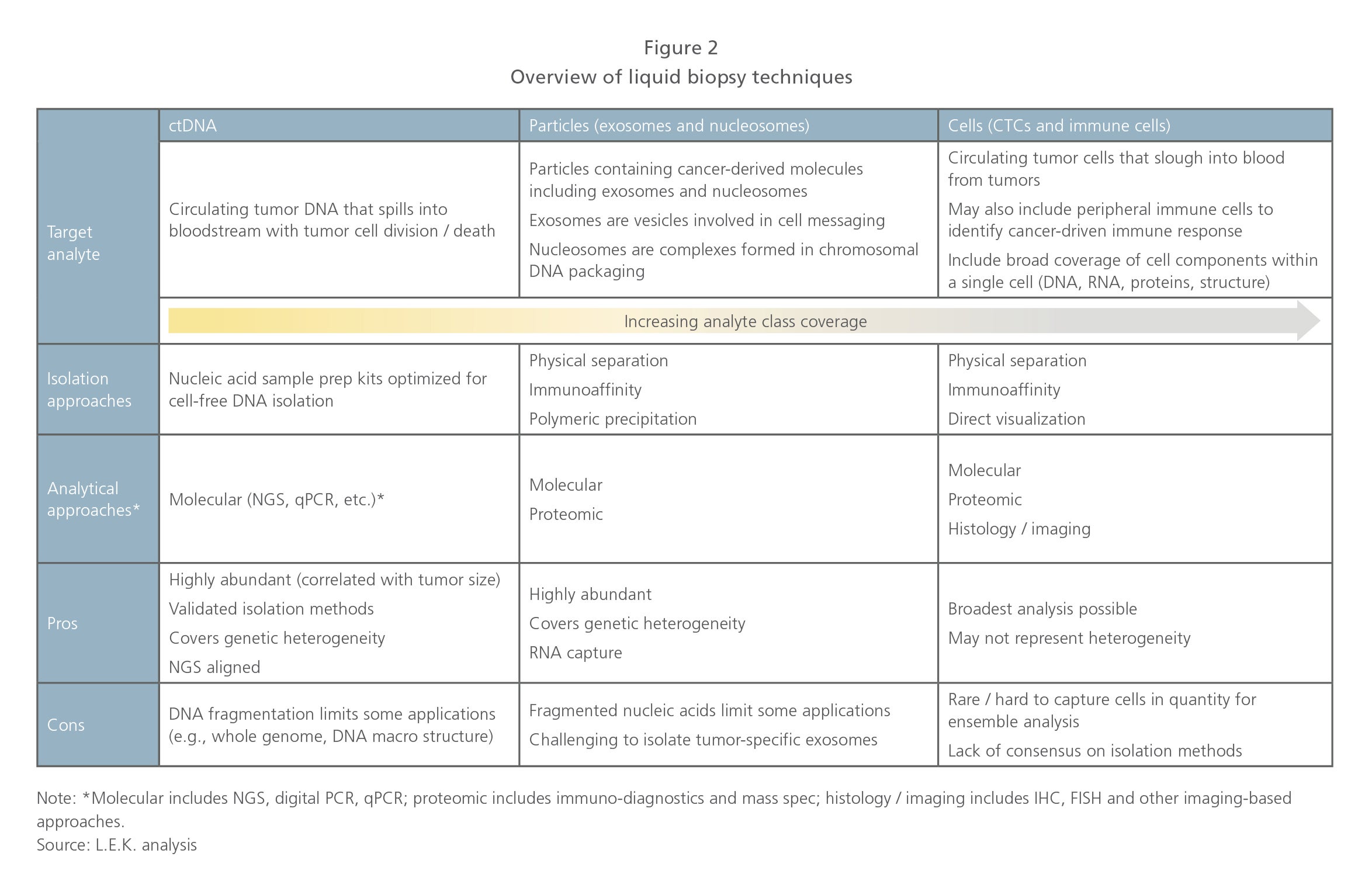

Central to liquid biopsy techniques is the capture and analysis of tumor-derived particles, which may include nucleic acids, proteins, exosomes, nucleosomes and cells. Since tumors divide, die, communicate and migrate, it is possible to find traces of their existence in biofluids. However, since these tumor-derived particles are typically rare, analytical approaches require very high sensitivity (NGS or digital PCR) or upfront enrichment (e.g., CTC cell capture).

There are multiple technologies used in liquid biopsy (enrichment and analysis), and it appears diverse approaches (and combinations thereof) may be required to address the breadth of potential applications (see Figure 2). Among all techniques, the combination of deep sequencing circulating tumor DNA or “ctDNA” using next-generation sequencing (NGS) represents the majority of current activity, but targeted (qPCR, digital PCR) approaches to measuring ctDNA are also being leveraged.

Beyond ctDNA, there is also significant activity in capturing and analyzing exosomes (vesicles involved in cell messaging), nucleosomes (chromosomal DNA packaging units) and circulating tumor cells (CTCs), as these contain a broader selection of tumor-derived analytes — including DNA, RNA and proteins — and may bring deeper insight into cancer biology versus ctDNA alone. While not based on detecting tumor-derived particles, capturing and analyzing immune cells is also emerging as a complementary technique in liquid biopsy and may be relevant in early cancer detection, as well as in guiding and managing patients on immunotherapy.

The competitive landscape is broad and dynamic

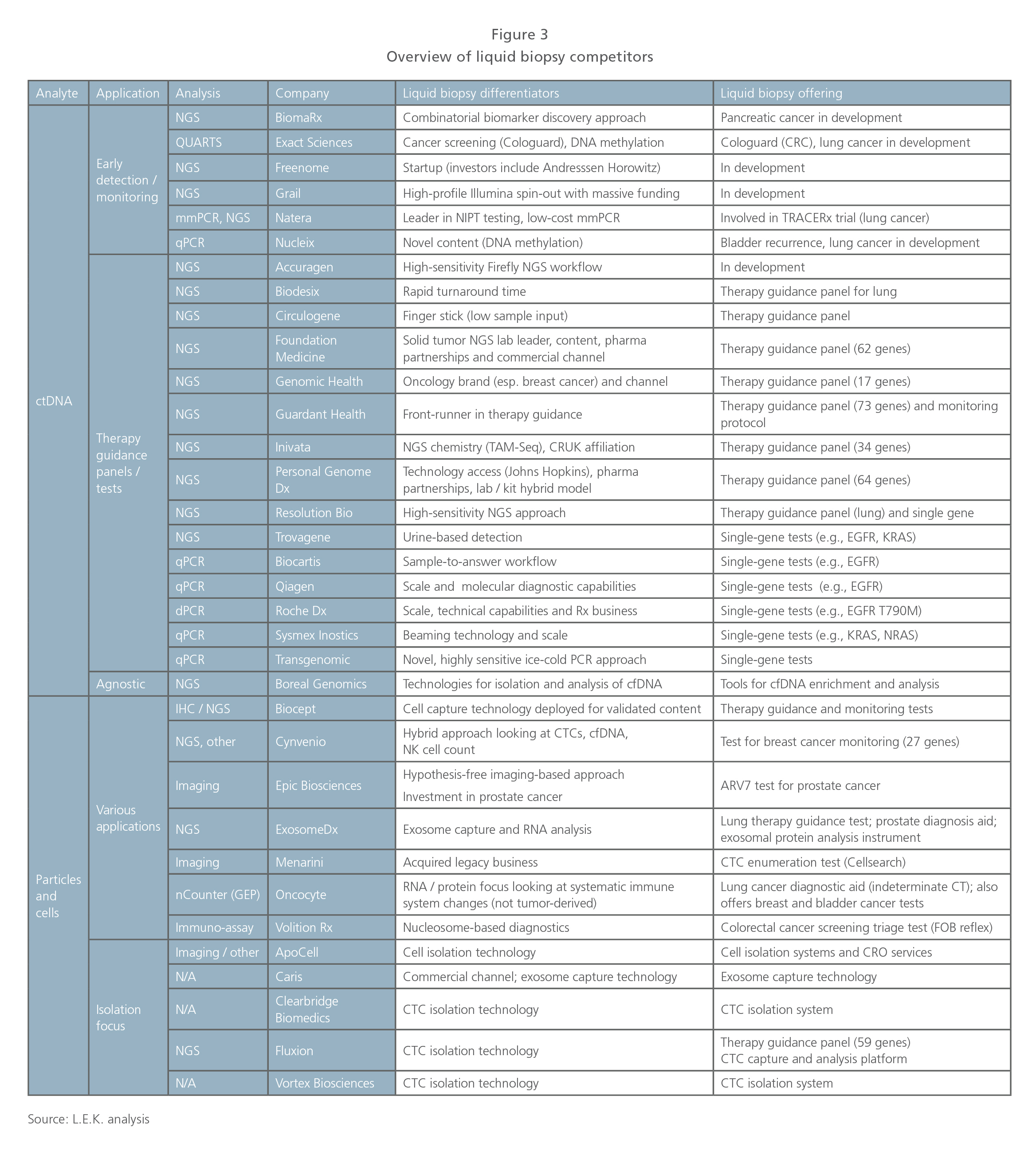

To date, we have identified over 30 different liquid biopsy competitors (see Figure 3). And while each competitor may have unique differentiators and offerings, we have attempted to categorize them into distinct segments based on a mix of technique/technology and current application focus.

Differentiation in the nascent clinical liquid biopsy space today appears to be driven by a mix of technology (e.g., sequencing chemistry, cell capture technology and informatics) and investment in clinical trials/data to support utility. Commercial differentiation is minimal as few companies have reached the scale where this represents a meaningful differentiator. The intellectual property landscape is also dynamic and expected to support company differentiation in the future.

Looking across the competitive landscape, we define the following clusters:

Early detection using ctDNA. Probably the most exciting segment (given its potential to impact health screening in the general population) includes various players seeking to develop offerings in early cancer detection and screening.

Competitors in this segment are expected to differentiate with clinical data to support test utility. Clinical studies for the general screening population are likely to be massive (~100K patients) in scale and require significant longitudinal analysis.

Grail is the poster child in the early detection space, having raised $1 billion in VC funding and recently embarked on a 120,000 patient study for early breast cancer detection. Many others are eyeing the early detection space, and some may ease their way into the general population applications through trials in at-risk patients, or as a reflex to other screening methods (e.g., low-dose CT, fecal occult blood).

Therapy guidance using ctDNA. This segment is the most crowded and is seeing actual clinical application today in metastatic patients. There is a core group of players deploying NGS-based liquid biopsy panels to support therapy guidance in biopsy-constrained situations. The clear front-runner here is Guardant Health, but many other competitors — several of which also play in the solid-tumor panel NGS space (e.g., Foundation Medicine, Personal Genome Dx) or have some differentiating technology enabling higher sensitivity or smaller sample input amounts — are also present.

Many traditional oncology diagnostics companies (e.g., Roche, Qiagen) have targeted single-gene tests based on PCR in the therapy guidance space, including regulated kits for companion diagnostic biomarkers such as EGFR. Players in this space are also likely to transition into monitoring applications for tested patients (looking at resistance or recurrence in treated metastatic patients).

Particles and cells (exosomes, nucleosomes, CTCs and immune cells). This is a heterogeneous segment developing varied clinical applications based on analysis of captured particles or cells. In some instances, competitors are enabling existing biomarkers to be measured from blood (e.g., Biocept, Exosome Dx) whereas others are developing novel content (e.g., Epic in prostate cancer and Cynvenio in breast cancer).

Epic is unique in that they do not enrich CTCs; rather, they image cells in a monolayer. Epic has focused efforts on prostate cancer and recently launched an ARV7 test to guide prostate cancer treatment. Cynvenio is interesting in that they are combining multiple techniques for their breast cancer recurrence monitoring test, which includes ctDNA and CTC DNA sequencing, as well as NK cell enumeration. Oncocyte is focused on blood-based immune cell function analysis. Another group of competitors in this space offers tools for CTC capture using various approaches, but is not focused on specific applications.

Significant opportunities lie ahead

The market opportunity associated with liquid biopsy represents one of the largest and most dynamic diagnostics/healthcare opportunities. While we are excited about the market potential and clinical utility, we urge pharma stakeholders, tools companies, diagnostic developers and other market stakeholders to carefully consider the impact liquid biopsy may have on the oncology landscape and what it will take to play and win.

08032020080826