Gas shortage has exposed the lack of resilience in energy networks

The September spike in European gas prices (to six times April’s level) has caused shockwaves throughout the energy sector. Over a dozen UK utilities have already gone bankrupt (e.g. Avro Energy, People’s Energy) with more expected, and consumer and industrial electricity prices are rapidly rising. Beyond energy, the security of the food supply and home heating have all been affected.

Global prices have similarly been rising across major APAC and US hubs, driven by both the energy transition and gas-specific factors. The broader energy transition is increasing demand for gas in the short term, driven by:

- Shift away from coal-fired power plants

- Weaker than expected generation in some renewable assets (e.g. wind at less than a third of 2020 levels in certain regions)

- Aging and retiring nuclear power plants

Gas-specific issues have compounded this, including:

- Supply shortages with weaker than expected deliveries from Norway/Russia, and the Maghreb pipeline shutdown

- Depletion of major swing supply assets (e.g. Groningen in the Netherlands)

- Limited storage in major European economies (e.g. the UK)

- Chinese competition for available liquified natural gas supply

- Rapid demand rebounds as industrial and consumer activity recovers from the worst of COVID-19

Governments are trying to implement a range of short-term policies to blunt the impact of volatility, but this spike has elevated longer-term questions regarding the resilience and sustainability of transitioning electricity networks that are almost entirely reliant on gas for balancing renewable supply.

Increasing renewable electricity generation alone is not a sufficient solution because intermittency is a fundamental and potentially very expensive problem

Increasing renewable penetration will help diversify many countries’ sources of electricity, combat climate change and provide low-cost electricity (excluding storage and grid stabilisation costs). However, in isolation, renewables cannot substitute for gas in the grid:

- Dispatchable renewables, where operators have some control/certainty over supply to meet demand, are difficult or impossible to scale up (e.g. hydropower, biofuels)

- Intermittent renewables are low cost and highly scalable (e.g. wind and solar); however, their supply is uncertain across timescales:

- Solar power’s output is available in northern grids only at relatively low demand times (i.e. around midday) and is seasonally variable

- Wind is a function of complex weather systems with unpredictable outputs

- Solar power’s output is available in northern grids only at relatively low demand times (i.e. around midday) and is seasonally variable

As a result, renewables impose a cost of uncertainty on the grid at a system level and cannot directly substitute for gas.

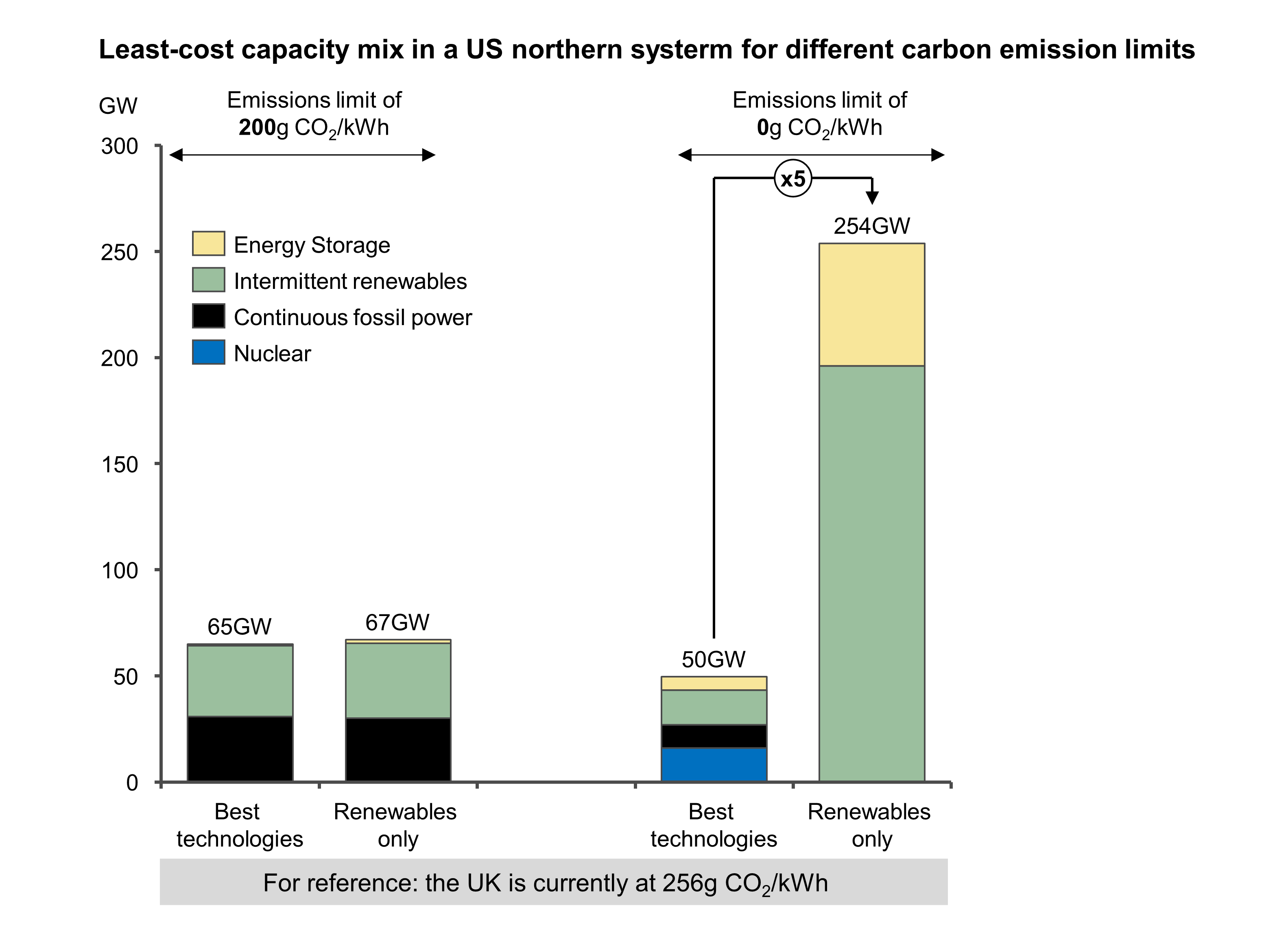

There are only three options to provide clean electricity and manage intermittency

Of the three options, only nuclear can meet both the requirement to manage (longer-term) intermittency and deliver clean electricity.

- Combining renewables with energy storage can address the intermittency challenge. There is a strong commercial case for the development of combined models, particularly for short-term storage (<24 hours), that could be addressed by utility-scale battery storage, particularly as the technology improves and costs decline. However, long-term storage (>24 hours) solutions are much more uncertain, with limited suitable sites for compressed air etc., and uncertain technological/commercial models for hydrogen or power-to-gas storage facilities.

- Combining gas generation with carbon capture utilisation and storage (CCUS) requires a significant new market to be created, requires a technological leap forward to allow for CCUS at Scale, and retains the same challenges of price volatility and energy security that we are currently facing. Currently existing CCUS systems capture much, much less (c. 30%-35%) than the 2050 target of 85%-95%. Placing an economically rational price on carbon emissions will likely be necessary to incentivise significant adoption and improved performance.

- Nuclear provides clean power and meets required carbon goals with minimal grid investment. Historically, major roll-outs of large reactors have been used to limit exposure to energy price volatility (e.g. France in the 1970s). Nuclear has traditionally provided a secure ‘baseload’ with year-round power, but new technologies could enable nuclear to serve a materially greater proportion of the load curve. Over the past two decades, installations have been slow to complete and limited, and nuclear has not been extensively deployed as a solution to climate change, given political resistance and high costs for large projects ($130-$200/MWh) relative to other fuels. However, recent months have seen a resurgence in interest, driven by increased political support (potential inclusion of nuclear on EU Sustainable Finance Taxonomy) and improving technology/economics (e.g. small modular reactors (SMRs)).

The case for nuclear in a net-zero world is becoming very strong

Deploying the right set of generation technologies (rather than just renewables) to support the transition to net zero materially reduces the required level of capacity buildout (and hence cost) whilst scaling up the ability to manage intermittent renewables. Over the medium term, nuclear will be essentially the only clean, dispatchable generation technology that minimises the cost of the transition.

The development of SMRs uses a fundamentally proven technology and addresses the long-standing problems with traditional large nuclear reactors: bespoke construction projects that usually experience enormous cost and schedule overruns. SMRs create a clear set of benefits for the utilities that manage the grid. Specifically, SMRs should:

- Reduce costs of nuclear power materially (from $120/MWh to $40-$60/MWh)

- Accelerate buildout at sites that are scalable (through standardised, factory assembled modules)

- Enable much more flexible and incremental capacity (<500MW) additions

- Fit into much smaller sites for a given level of capacity (up to two orders of magnitude smaller)

- Provide clean electricity to charge the rapidly growing fleet of electric vehicles; charging vehicles overnight helpfully increases baseload demand

- Serve demand more flexibly, through mixed hydrogen generation, industrial use and grid service models

- Provide clean electricity to power the production of hydrogen and other synthetic fuels (e.g. sustainable aviation fuel)

- Support other net-zero goals, including providing low-cost power for Direct Air Capture Facilities

SMRs also have an important role to play off grid where there is substantial demand for dispatchable power; for example:

- Traditional process industries: Serve a wide range of large plants in industries that include refining, chemicals, steel production and aluminium smelting; traditionally these have been served by combined cycle gas turbines

- Data centres: Power the rapid growing ‘hyperscale’ data centres — many of which are owned by ‘Big Tech’ and have very public existing green commitments

- Hydrogen and other synthetic fuels: To provide clean baseload electricity for electrolysis to generate hydrogen at scale (if that is not supplied on grid)

- Desalination: One energy intensive solution to the major global water scarcity challenge that will only become more acute over the coming decades

Obviously, the successful development and deployment of SMRs is not without risk and requires significant funding. The recent announcements by Rolls-Royce and the UK government are very welcome and encouraging in accelerating the development of this critical technology. Now is the time for new countries and companies to capture a significant economic prize.

This article was written by John Goddard, Senior Partner in L.E.K.’s Industrial practice and Vice-Chair of Sustainability, having founded the L.E.K. Sustainability Centre of Excellence, with Philip Meier, Senior Principal, and Luke Samuel, Manager in L.E.K.’s Industrial practice.

01052022150101