Though claims that electric vehicles (EVs) will imminently and entirely replace traditional fuel vehicles (FVs) are premature, there is an industry consensus that substantial, ongoing EV development and significant, near-term EV adoption are inevitable. Under the current set of market conditions, L.E.K. Consulting predicts EV commercialization will produce three key sets of effects on the automobile industry, and L.E.K. has prepared preliminary response tactics that traditional FV manufacturers can employ in response to EV trends.

In September 2017, the vice minister of China’s Ministry of Industry and Information Technology (MIIT), Xin Guobin, spoke at the Forum on Chinese Automotive Industry Development and announced work had begun on formulating a timetable to ban the manufacture and sale of traditional FVs. This marked the first time MIIT had commented on the topic and prompted widespread discussion.

Prior to this announcement, a number of other countries had announced similar plans to ban traditional FV production — with some even setting clear timetables. The United Kingdom and France plan to ban the sale of gasoline and diesel vehicles from 2040 onward. Additionally, 10 other countries have announced similar plans. Although the United States has not issued a nationwide timetable, several individual states have proposed initiatives to move away from traditional FVs.

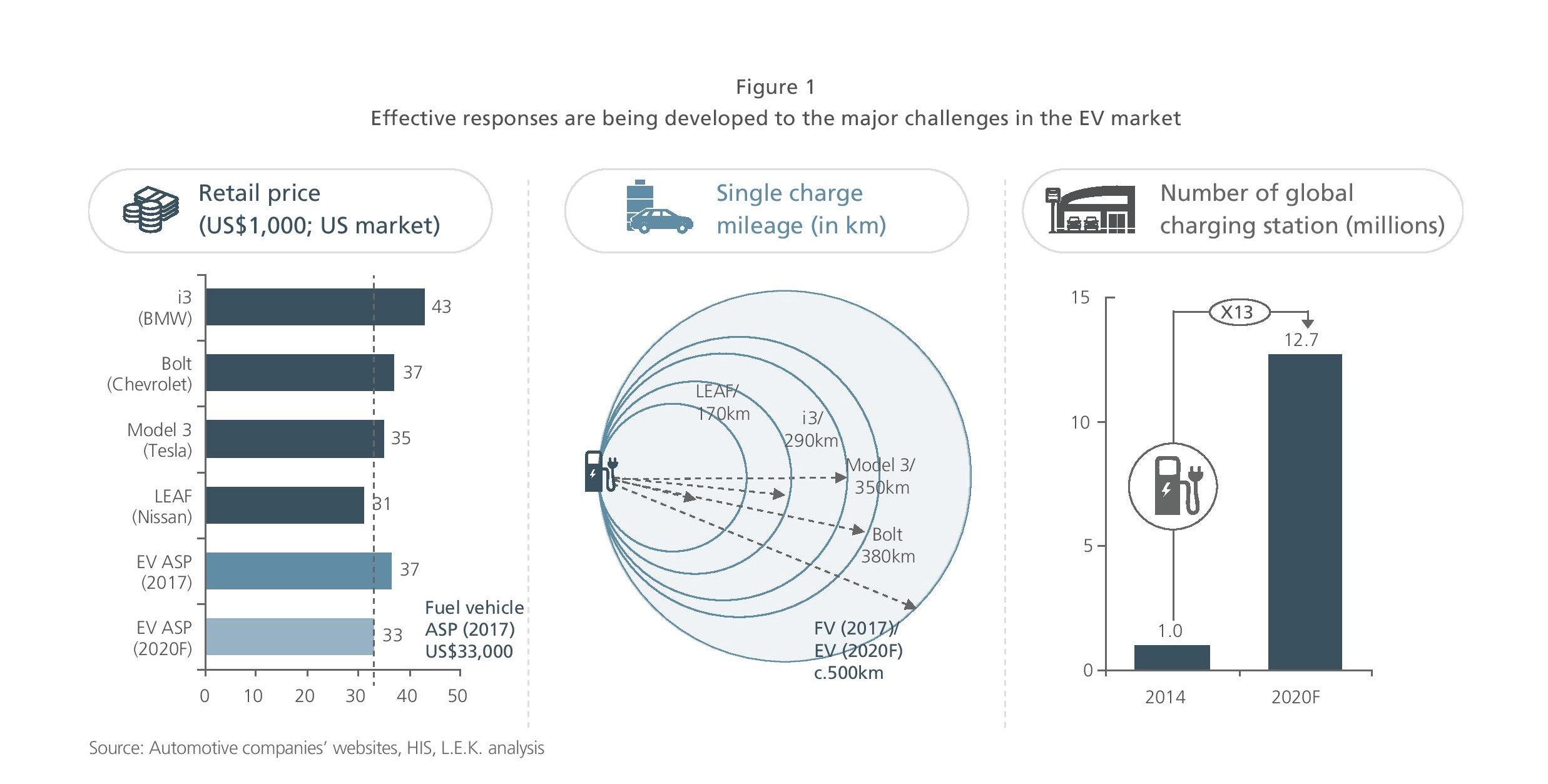

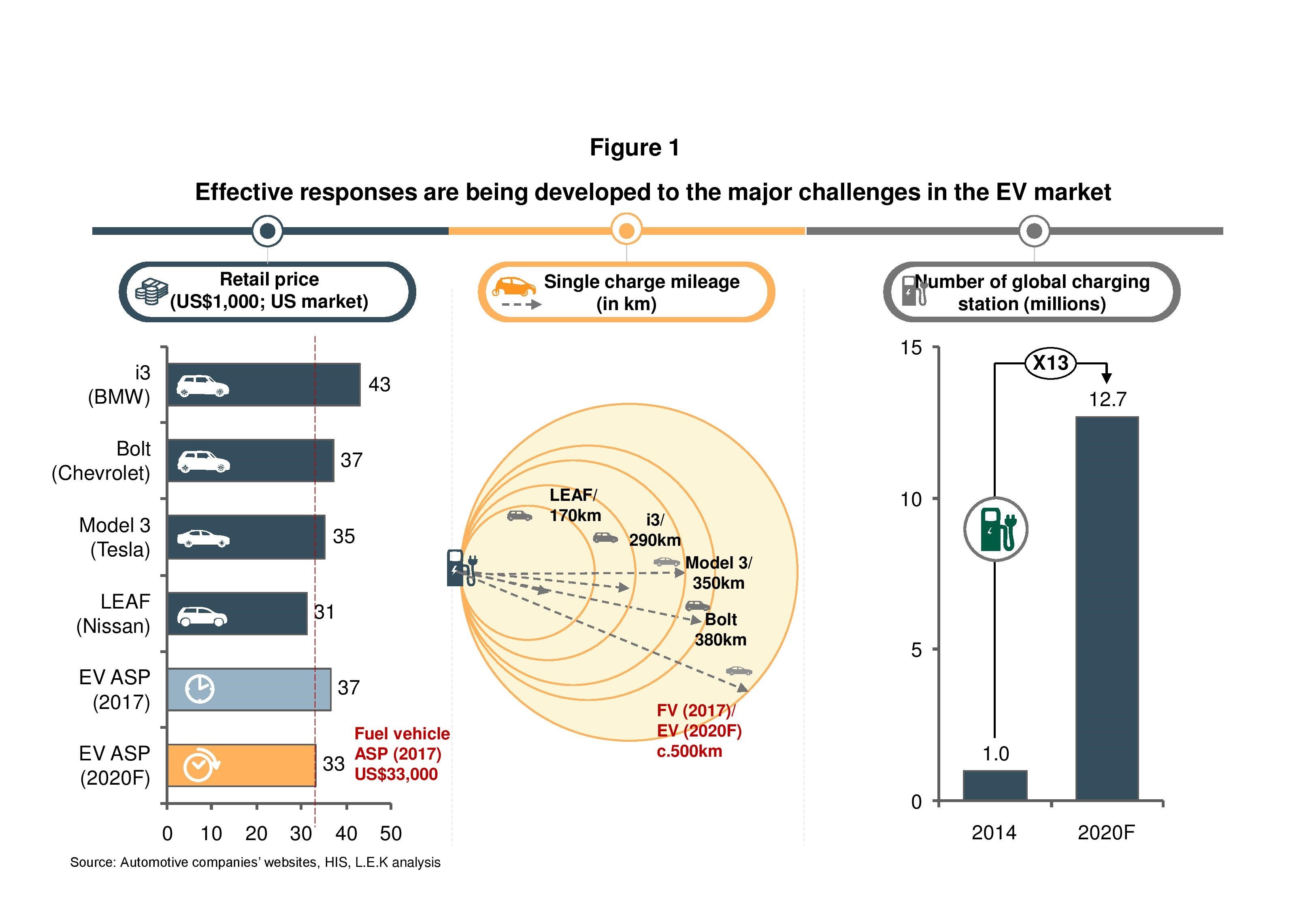

Major challenges to further EV growth fall into four key categories: pricing, mileage, charging facilities and regulatory mechanisms. Currently, these challenges are already being dealt with in gradual and effective ways (see Figure 1).

In the United States, the basic configuration of the latest Tesla Model 3 is priced at approximately $35,000, a price almost matching the median price of a traditional FV in the domestic market (about $34,000), and it has reported a battery life range of 350km. Traditional auto manufacturers are not far behind: LEAF (Nissan), Bolt (GM), i3 (BMW) and other models are also approaching traditional FVs in pricing and mileage. In China, startups like Nio and FMC (Future Mobility Corporation) are attempting to deliver durable, moderately priced EVs — and are positioned to serve an addressable market of upwards of a million users. Simultaneously, Chinese local authorities have also put forth an increasing number of policies supporting the construction of charging stations. This, in addition to high levels of domestic EV manufacturing activity, is making China one of the most developed and connected markets for EV technology. Commitment to building charging station infrastructure has also significantly reduced range and mileage anxieties among existing and prospective EV owners — lowering the barriers to EV ownership.

Governments are looking for balanced and holistic approaches to regulating EV development. On one hand, governments have strong interests in supporting the development of EVs. On the other hand, there is also some concern that excessive EV industry growth could present new sets of policy issues. For example, in the United States, status quo legal frameworks neither adequately address nor appropriately regulate driverless cars — the majority of which are electric. Specifically, issues of liability in the event of an accident involving a driverless car are not defined within the current regulatory structure. Congress is actively working to develop laws and regulations to ensure that by the time driverless cars are mass-marketed, appropriate regulations are in place.

From an adoption perspective, EV sales are expected to increase as soon as EV manufacturers expand capacity and add production lines. Although EVs will not entirely replace traditional FVs in the near term, there is an industry consensus that increased EV penetration is an inevitability. In the midterm to long term, EVs can expect to gain significant — and eventually majority — market share. The next decade will be one of momentous change for the automotive industry, and in order to respond strategically to market movements, it’s imperative for relevant stakeholders to have a deep knowledge of market trends.

This Executive Insights reviews three disruptive trends in the automotive industry precipitated by the rapid growth in the EV industry and offers preliminary suggestions on how best to respond and adapt to those trends.

Competitive emphasis on cost-effective hardware and value-added servicing

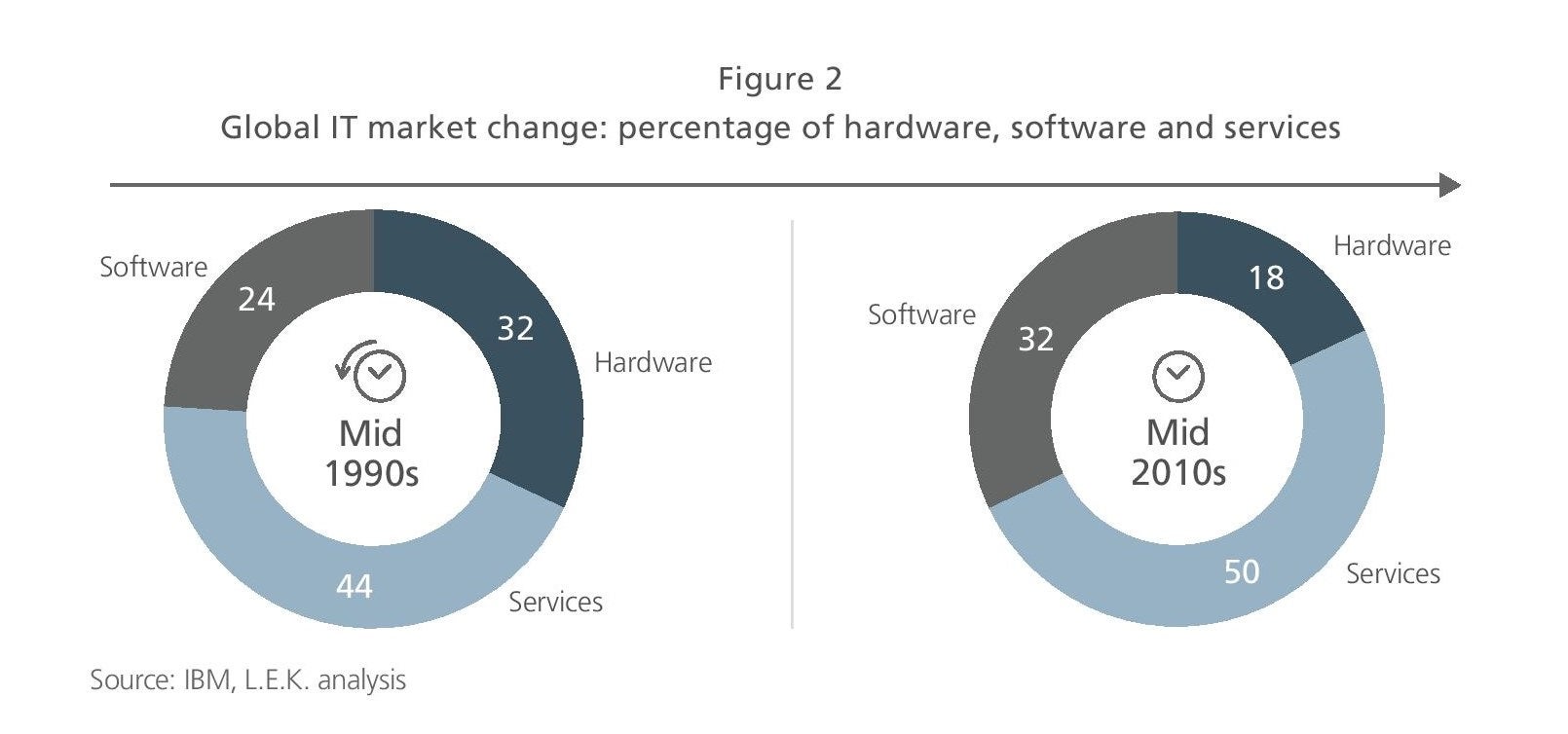

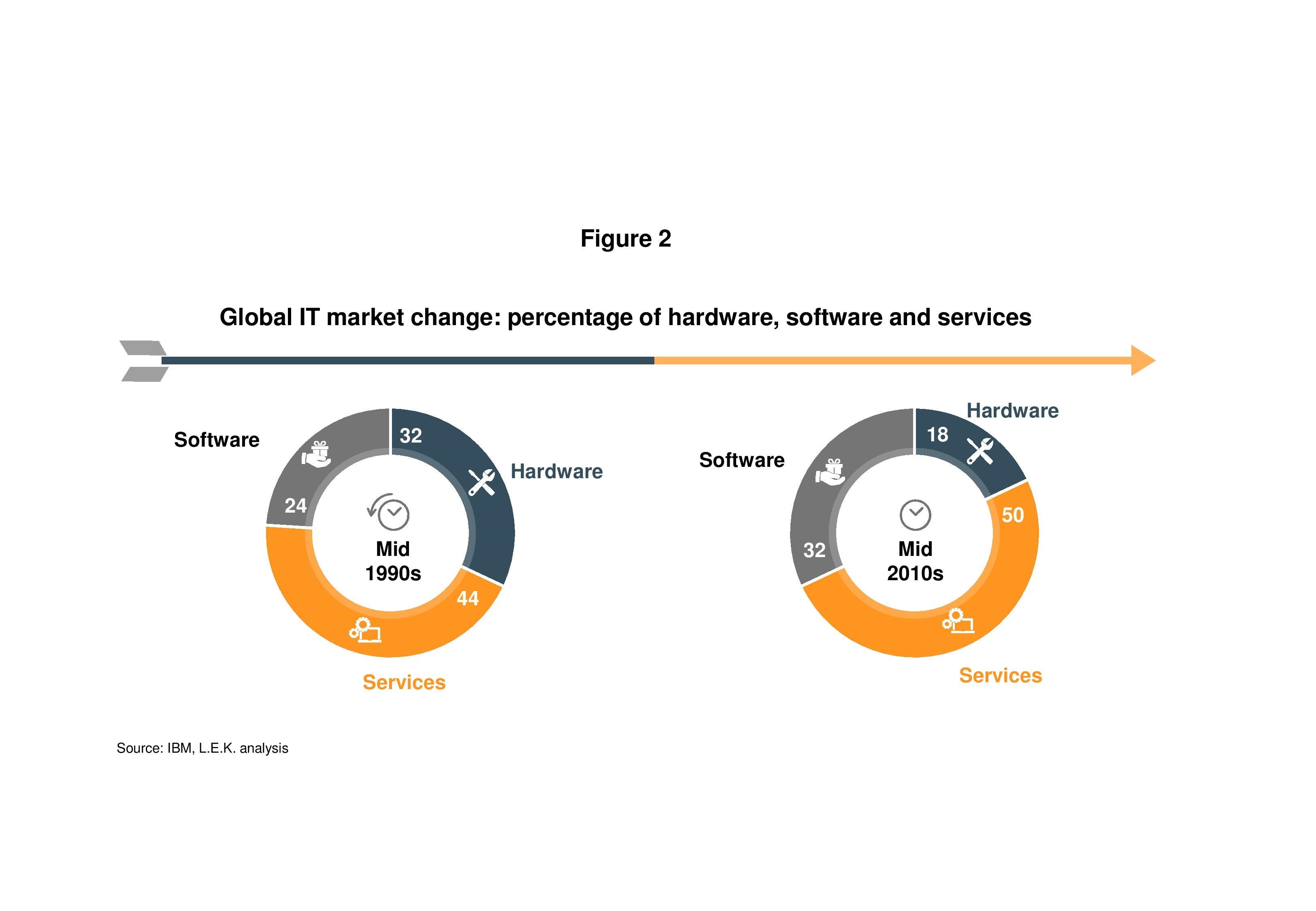

Evolution in the EV competitive landscape is expected to parallel evolution previously observed in the IT industry: Competitive foci will gradually shift away from the pursuit of breakthrough technologies and toward the development of cost-effective hardware and value-added services. The IT industry can be taken as a case study, with the past two decades in particular serving as an example of shifting modes of competitive positioning.

Since the 1990s, the core dimension along which IT enterprises have been competing has shifted away from hardware performance and toward provision of value-added and customized services. Take the PC, for example. Given the high levels of compatibility between PC parts (hard drives, memory, etc.) and narrow PC hardware margins, many PC manufacturers (Dell, Lenovo, etc.) have chosen to outsource to original equipment manufacturers (OEMs). Value-added services have become the primary margin driver in the consumer electronics industry. For example, since the 1990s, IT giant IBM has spun off lower-margin and less-competitive hardware holdings, moving further and further into services and software. Apple has long recognized that it’s able to exert comparatively more pricing power in the software business, and as a result it has been able to maintain a market-leading position in the digital world.

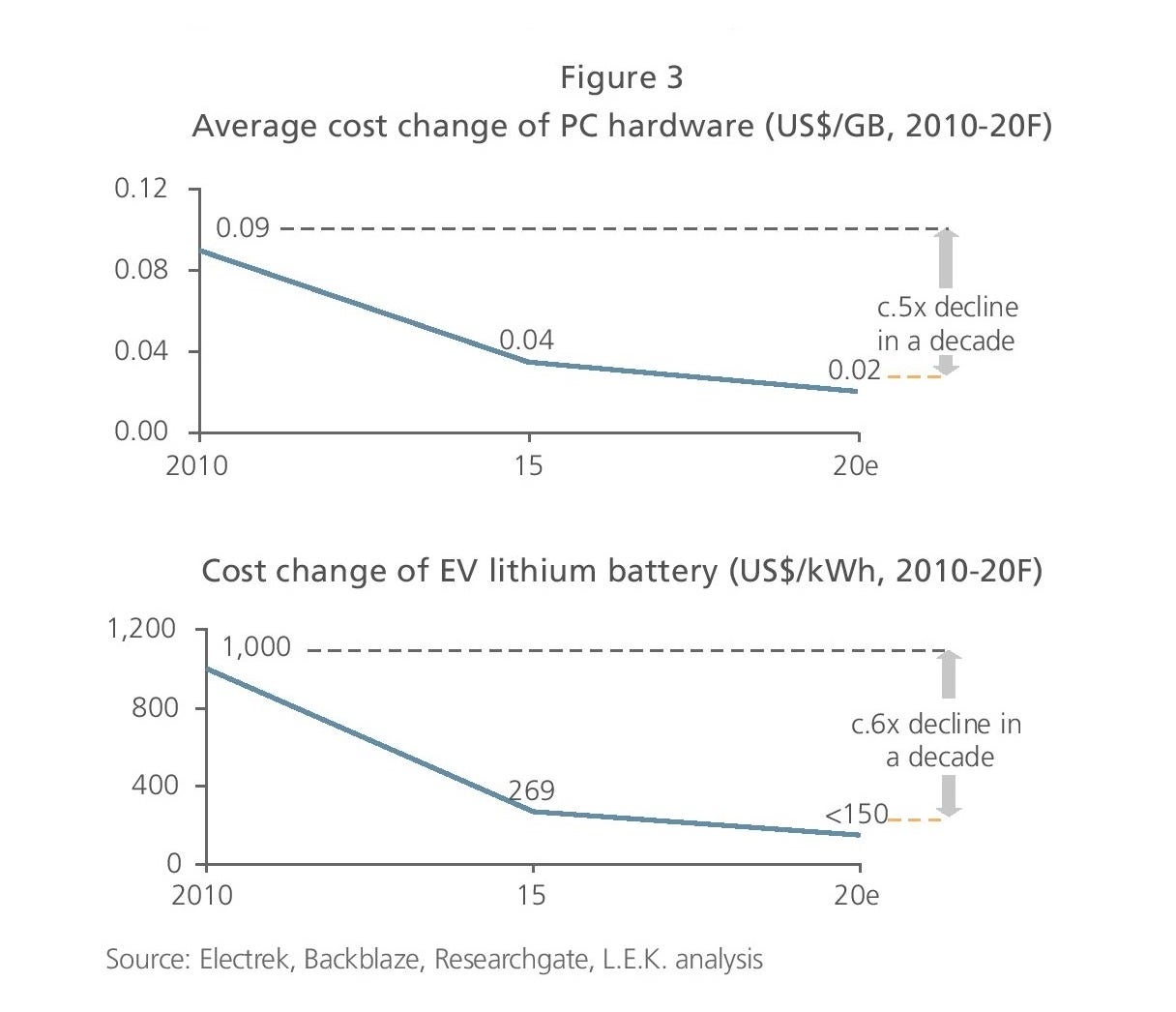

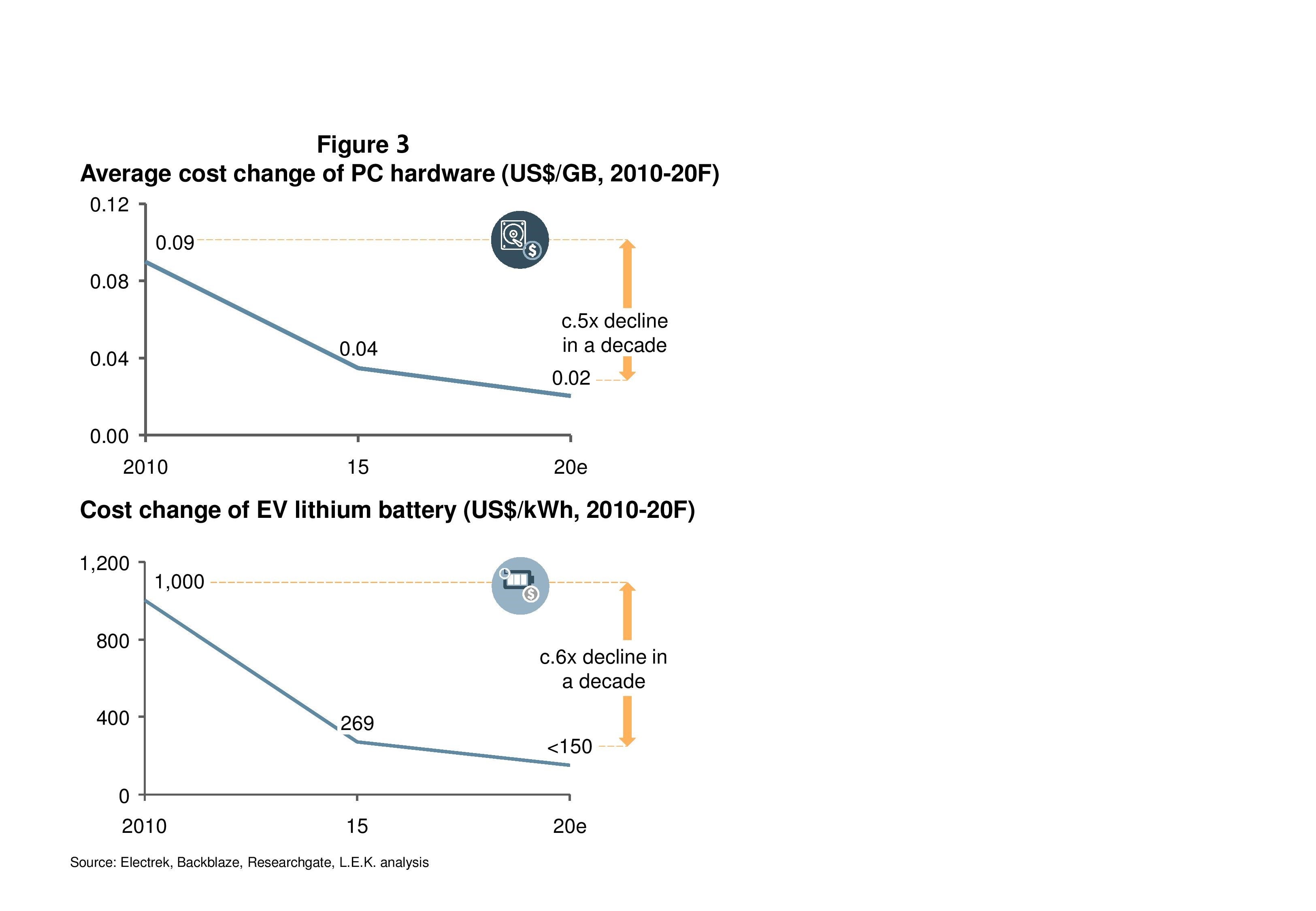

We believe that the IT industry (especially consumer electronics products such as PCs and mobile phones) serves as an important reference point for EVs and can be used to predict the competitive trajectory of and cost dynamics within the EV space (see Figure 2). For example, we expect to see similar cost decreases over time in EV main systems as we have seen historically in PC hard drives. The main system of electric cars (i.e., motors, electronic controls and batteries) is more standardized, modular and cost-effective than those of traditional FVs (engines, gearboxes, etc.), and EV main system costs are expected to decline markedly going forward. Even if the tech iterations and cost reductions in PC hardware under Moore’s Law are much faster than those in EV batteries, both are expected to follow similar directional manufacturing cost trends through the 2020 forecast period (see Figure 3).

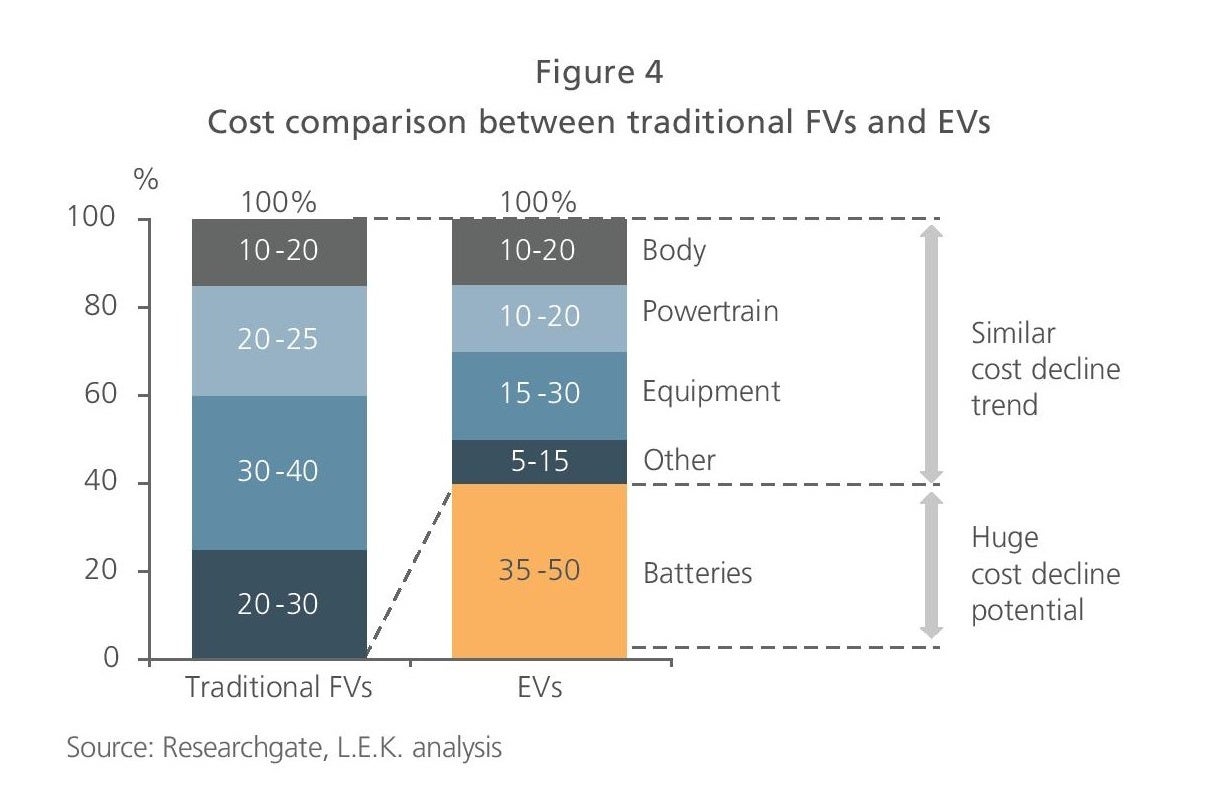

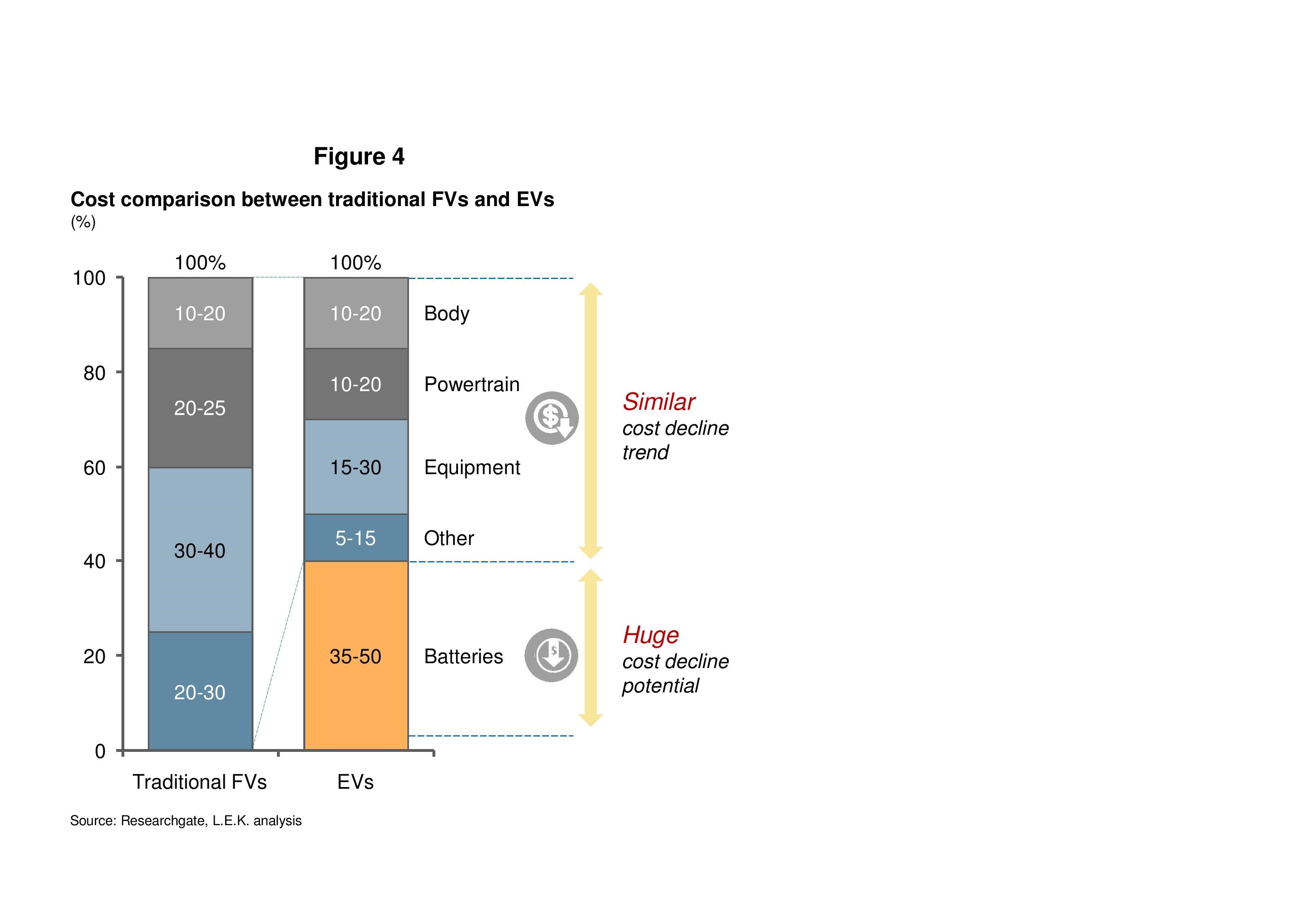

If we break down the manufacturing cost of cars (see Figure 4), we see that batteries now account for as much as one-third to one-half of the total cost. As battery costs decrease, we will see corresponding declines in overall EV pricing. In addition, because net fewer parts are required in EV assembly relative to traditional FV assembly, total EV assembly costs are significantly lower.

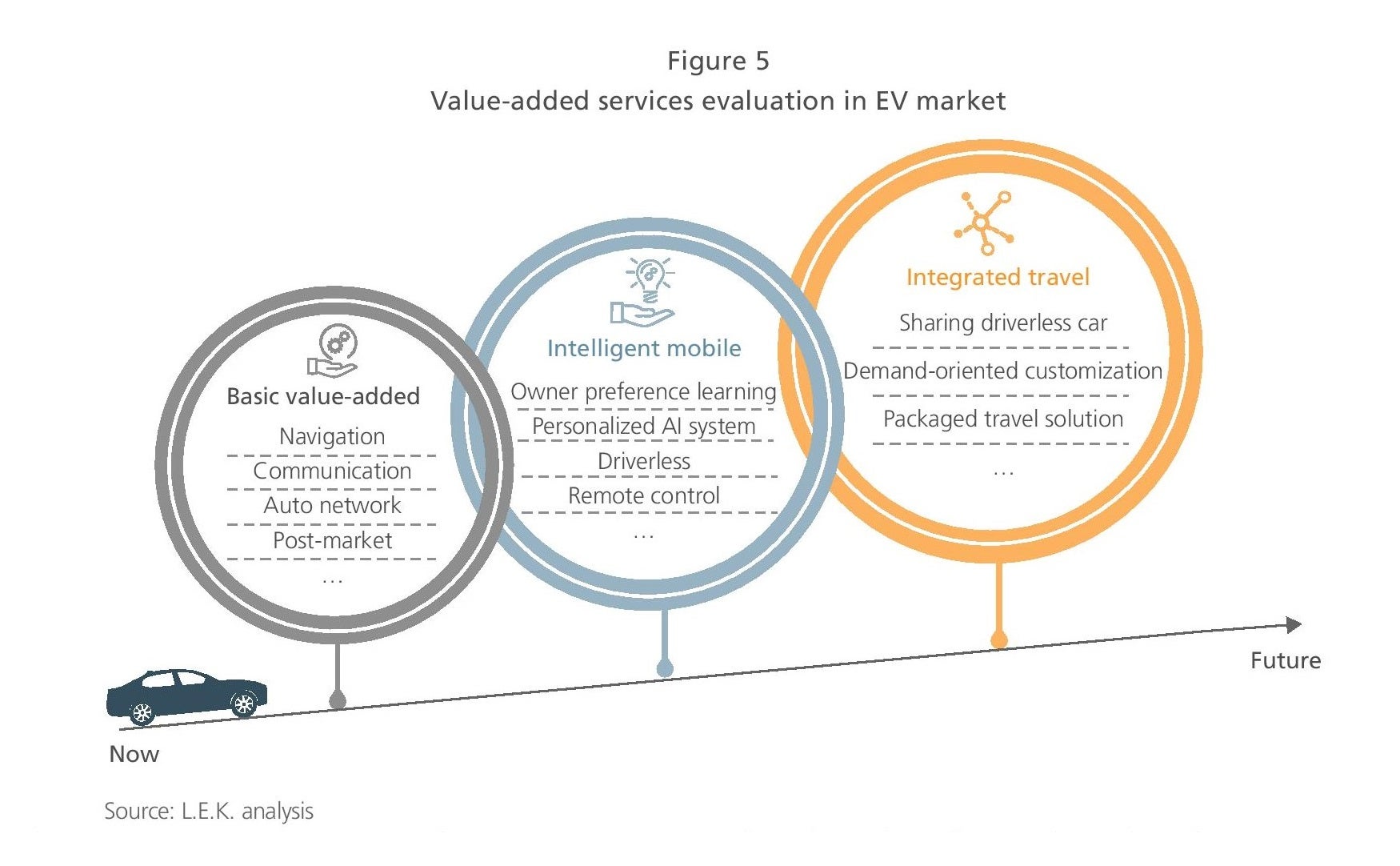

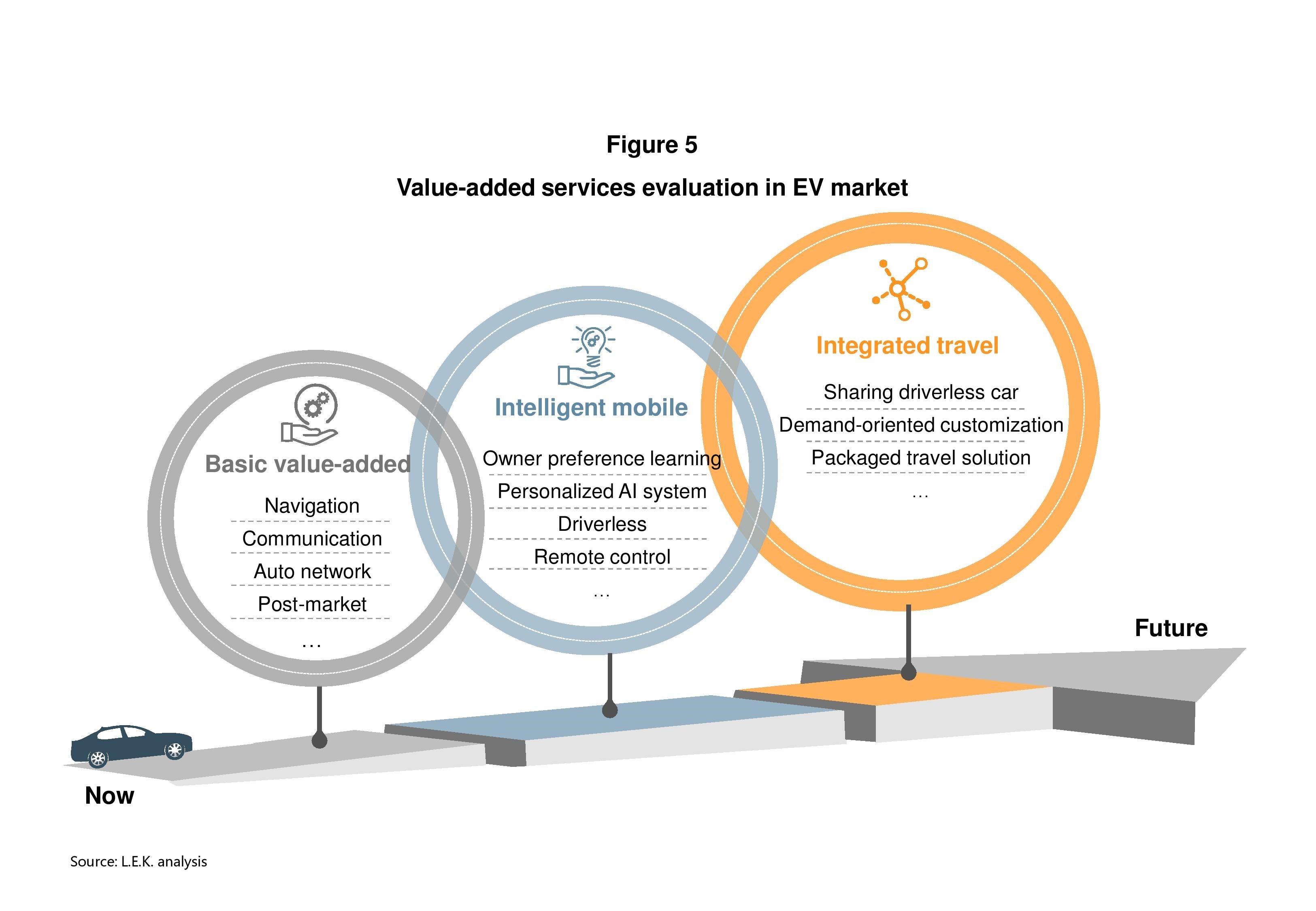

In an increasingly value-oriented future, technology-based competition is expected to be minimal and margins are likely to reside in value-added services. Below, we segment these services into three key groupings in accordance with their level of development (see Figure 5).

- Basic value-added services such as maps, navigation, automotive networks, aftermarket services and other extended services.

- Intelligent mobile services such as personalized smart systems, driverless systems and other artificial intelligence (AI) services.

- Integrated travel. Ultimately, EV manufacturers are working to become integrated travel solutions providers. This could include not only simple solution combinations (e.g., a driverless car plus car-sharing solution), but also could include customized solutions and systematic services (e.g., an intelligent integration of cars, high-speed rail and aircraft based on personal demand) for customers with distinct travel needs in varied travel scenarios (corporate sales, daily family trips, short travel, etc.).

Given the rapidity with which the EV industry has grown, many traditional FV manufacturers have not had time to formulate holistic responses to newer EV entrants and are likely, to varying extents, unprepared to adapt to the new demands and expectations inherent in the EV era. Changes in competitive dynamics, new entrants with novel business strategies and the emergence of new business models are all expected to put increasing pressure on traditional FV players.

Weakened demand growth in major automotive markets

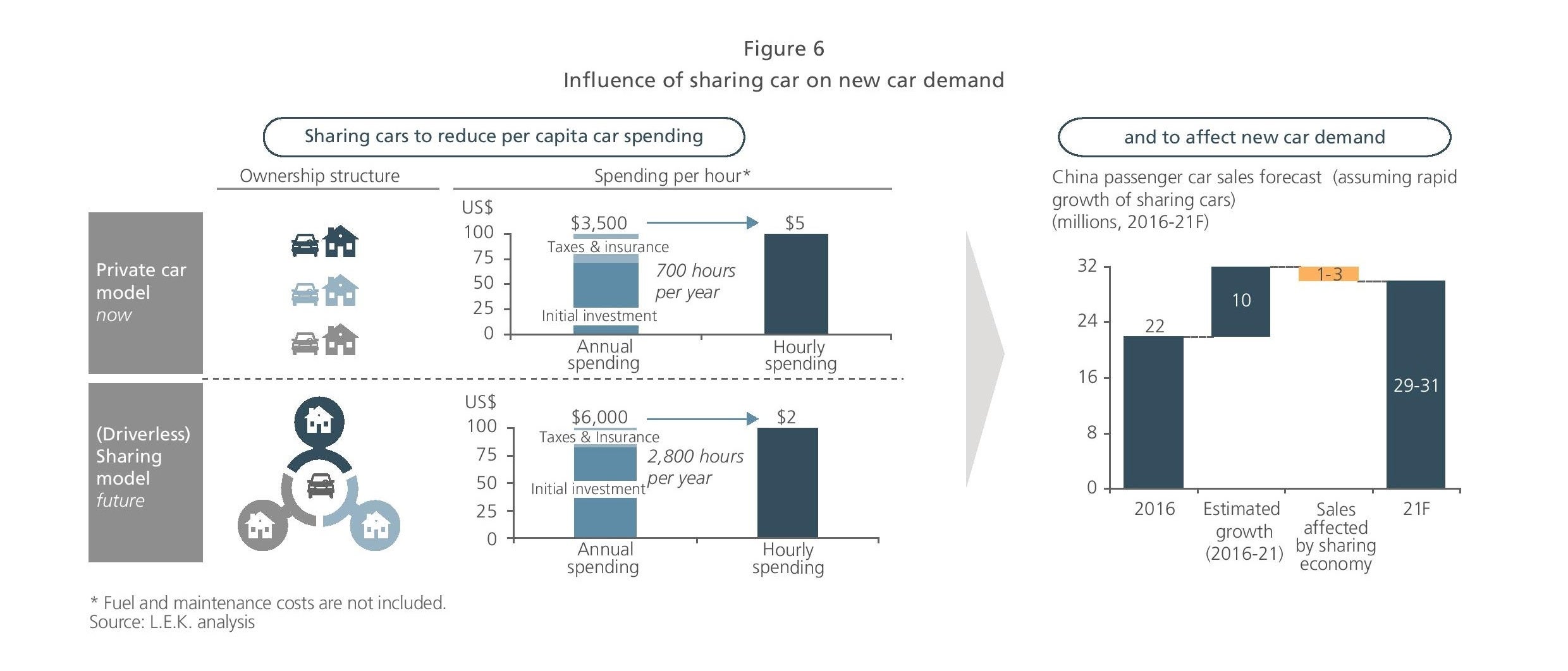

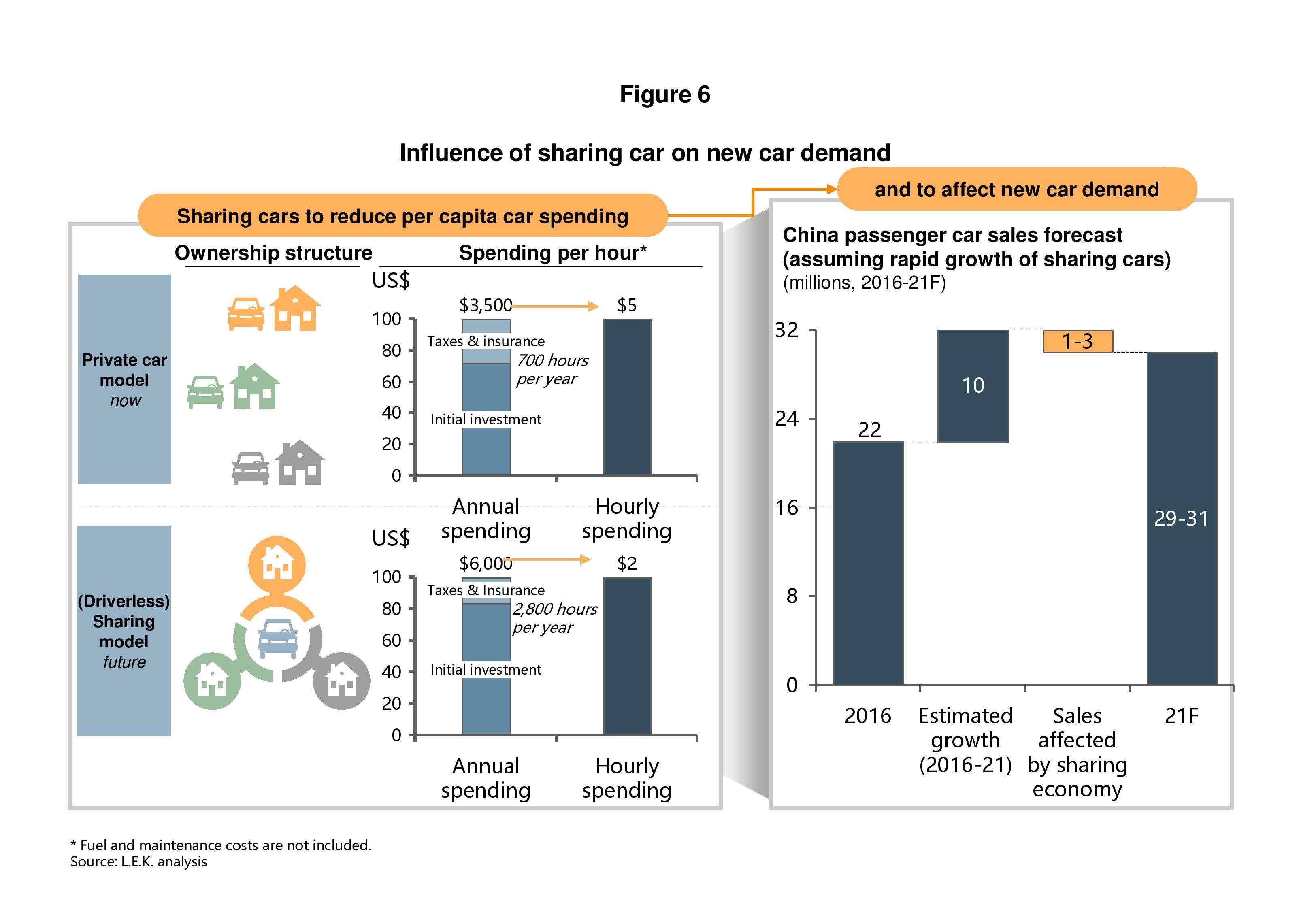

Future demand growth in major automotive markets is expected to be challenged by the development of ride share and driverless technology (see Figure 6). Ride share and related modes of travel have been broadly popularized in China; commercialization and penetration of driverless technologies will further catalyze the development of ride-sharing, fundamentally disrupting existing models of car ownership and utilization. Some consumers may shift away from car ownership and toward reliance on an on-demand, driverless fleet owned by a third party. A shared, driverless fleet could provide door-to-door servicing, significantly reducing an individual driver’s daily automotive-related spend. While ride share is unlikely to completely replace traditional models of private car ownership, driverless EV fleets are expected to exert a significant influence on individual propensity to purchase private cars — especially on new car sales in developed markets and major cities.

Traditional car companies will, invariably, be affected by these trends. But as long as they make adequate preparations, the impact of these trends will be disruptive rather than destructive. In fact, some more pioneering traditional FV manufacturers have already embraced the trend toward ride-sharing and have made investments in shared fleets. Globally, companies like Volvo, Volkswagen, GM and Ford have all set up or invested in a shared fleet. In China, Mercedes-Benz and BMW also announced shared-fleet trial operations beginning in 2016 and 2017, respectively. That said, development of a shared fleet is not the only solution car companies have available. More generally, we believe that going forward, the key to success for auto companies lies in adopting trend-aligned market positioning and developing business models that are able to meet the needs of high-value target populations.

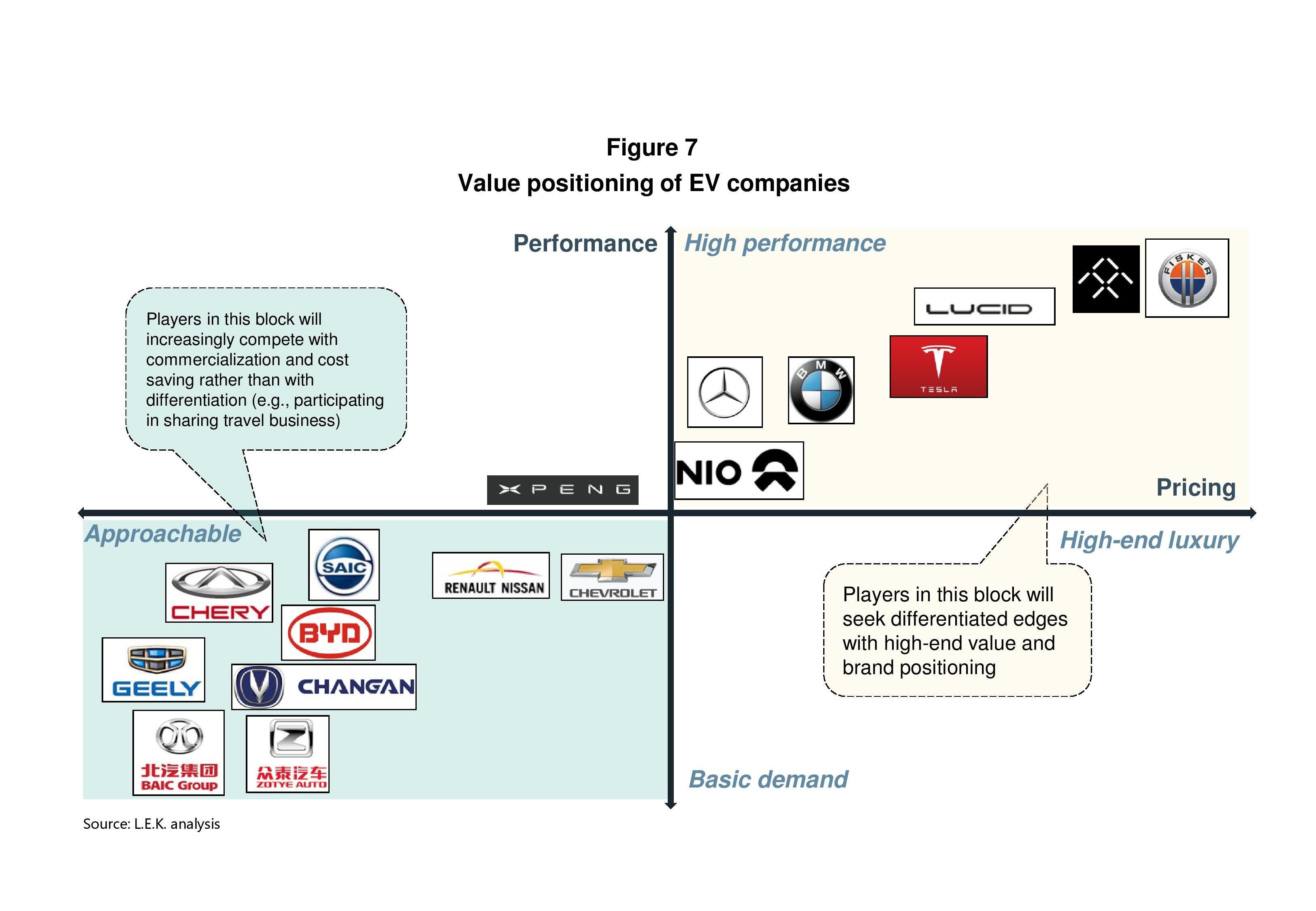

Bifurcated EV market growth strategies

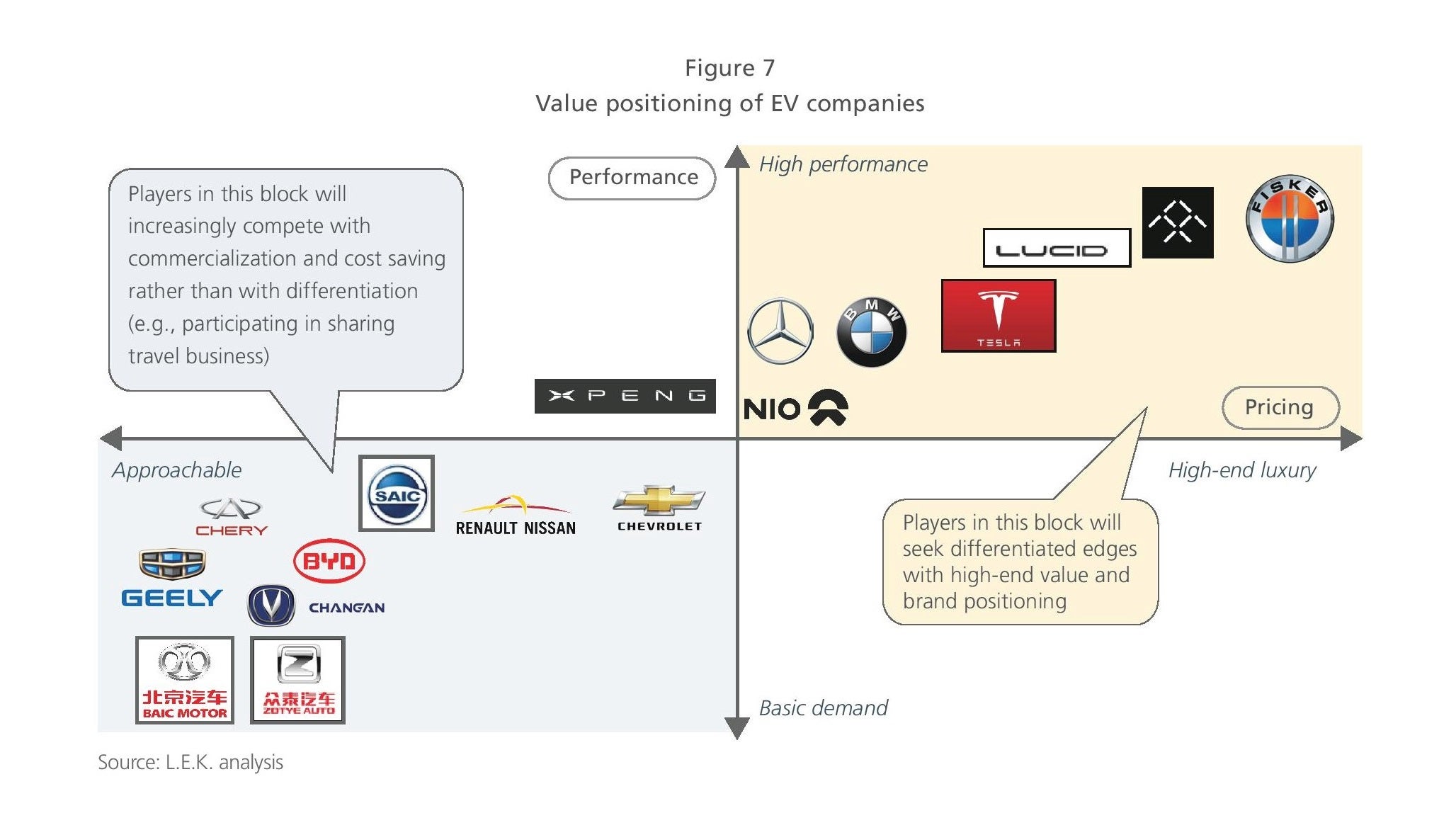

In the future, the market mandate for EV participants to pursue strategies with clear value propositions is expected to lead players to adopt one of two models of growth (see Figure 7). Here, EV participants include EV companies (including traditional and new players), auto parts manufacturers and service providers.

EV companies are likely to become increasingly bifurcated. Given intensifying competition in EV commercialization, one set of companies will increasingly adopt a large-scale and low-cost model. Their business models might include cooperation with ride-share corporations or shared-fleet operators (though EVs will need to take precautions to avoid becoming a low-value, accessory or ancillary business partner) or direct participation in the ride-share market. Some of them may even develop into the “Foxconn of EV,” a super EV OEM. For these enterprises, their core competitiveness lies in their cost and service model.

The other set of EV companies will attempt to win share through high-end differentiation. Some of them will emulate Tesla and offer customers strong design, positive user experience and excellent customer service. Others may position themselves as high-end, premium manufacturers in order to win share of wallet with high-value customers. In addition to having clearly defined and well-articulated value propositions, both traditional luxury automobile manufacturers entering the EV space (Mercedes-Benz, BMW, etc.) and emerging EV manufacturers (Nio, FMC, etc.) must recognize that their addressable market is relatively small and limited to a set of consumers with highly specialized preferences and demands.

Auto parts manufacturers, the second key group of EV market participants, also have to make a strategic choice. Once again, as in the IT and consumer electronics markets, we have seen two sets of business models emerge: low-cost, low-margin manufacturers and technology leaders with patent-enabled monopolies, such as Qualcomm. The next few years are crucial for auto parts manufacturers, many of which are experiencing margin-related pressure due to relatively low technological barriers to entry and the resulting high levels of capacity; in some parts markets, like battery manufacturing, there is even a risk of overcapacity. These margin pressures mean decisions around appropriate positioning are essential: Is it more strategic to pursue a strategy of offering lowcost products or to become an owner of a core technology patent?

The third group of participants is service providers. Customer-centric and differentiated service providers — especially those that can serve both value-oriented and high-performance EV companies — will experience rapid growth. For service providers, consumer electronics companies like Google and Apple can be taken as case studies in the importance of strong technology and platform-driven business models. Google was an early entrant in driverless-car market technology, with a program beginning in 2009, and Apple has effectively positioned itself, not only as a consumer electronics manufacturer but also as a software company with a network of compatible hardware, software and service offerings.

Going forward, thoughtful integration of big data capabilities, artificial intelligence and mapping reliability will be key to winning. In China, BAT (Baidu, Alibaba and Tencent, the top three domestic internet companies) are most likely to lead technology and platform integration initiatives. Baidu initiated a driverless automobile project in 2013, hoping to build the world’s largest, connected driverless tech platform — a platform linking other IT and automotive companies. Despite BAT’s market advantages, non-BAT companies still have opportunities to compete. Other service providers can build core tech competencies in a niche such as AI services. For example, JingChi Technology, a startup by ex-Baidu employees, has emerged as a leader in the development of driverless technology. Alternatively, breakthroughs can be enabled through business models, rather than technology; some examples include DiDi Chuxing, Atzuche and EVCARD. As long as service providers are able to identify and occupy distinct and necessary market niches, they can succeed in the EV market.

Sample Visuals

07282020180710