While management of end-stage renal disease (ESRD) has been a longtime priority for both payers and policymakers in the U.S., a comprehensive renal health strategy that includes chronic kidney disease (CKD) has proven elusive. A lack of private-sector incentives and minimal focus in public policy have historically contributed to high costs and poor health outcomes for CKD patients. However, recent changes in federal policy and rapid adoption of value-based care (VBC) by public and private payers have contributed to a sea change in the management of renal disease. Led by third-party vendors, the field of kidney health management (KHM) is quickly growing and applying principles of managed care to improve outcomes and reduce cost in an area of the U.S. healthcare system that has traditionally been underserved.

The Evolution of Kidney Health Management and the Next Frontier

Key takeaways

Chronic kidney disease (CKD) is a large driver of U.S. healthcare costs. Despite the higher expense, the U.S. also experiences poorer outcomes for CKD patients.

This indicates a high level of both clinical and administrative need for CKD patient management. Even so, the U.S. healthcare system has traditionally been narrowly focused on end-stage renal disease while mostly ignoring early-to-mid-stage CKD.

Recently, however, increased governmental focus on kidney health and new incentives for better management of renal patients have touched off a rapidly emerging market for kidney health management (KHM).

Although KHM models are still in the early stages, they could reduce total cost of care in CKD by 20%-30% if fully optimized strategically and implemented successfully at the tactical level.

CKD, which refers to long-term reduction in renal function, is a large driver of U.S. healthcare costs and a significant source of unmet need in the healthcare system. Though KHM has been historically deprioritized relative to ESRD, a recent wave of innovation from public and private payers is coming together rapidly with an upsurge in federal policy initiatives to improve the quality of patient care and reduce total cost of care (TCOC).

Approximately 22% of annual Medicare fee-for-service (FFS) spending is for beneficiaries with CKD.

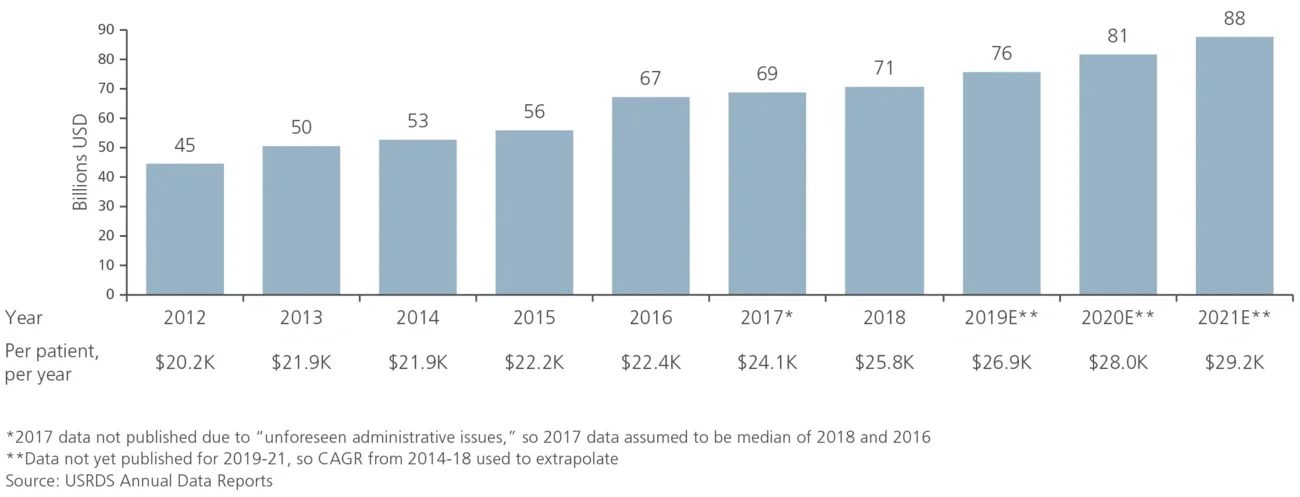

This high proportion of spend on CKD patients is due to the large underlying patient population and the high annual cost to treat CKD patients. An estimated 40 million American adults have CKD, or ~15% of the adult population — higher than the ~11% of the population with all forms of diabetes. CKD is also an expensive chronic condition to treat, with annual TCOC for CKD patients reaching ~$26,000 in 2018, compared to ~$12,000 for Medicare FFS beneficiaries without CKD (see Figure 1).

The high TCOC for CKD is caused by a multitude of factors:

- High prevalence of comorbidities in the CKD population (e.g., diabetes, hypertension, congestive heart failure)

- Challenges in care coordination across large, multidisciplinary care teams

- Complex pharmacotherapy regimens

- High rate of hospitalization

Figure1

Total Medicare FFS expenses and per-patient, per-year costs for CKD patients (2012-21E)

In addition to the shortcomings in traditional management of CKD, the transition from CKD to ESRD has historically been poorly managed. CKD patients frequently “crash” into dialysis; they present to the emergency room with acute kidney failure, requiring the unplanned and immediate initiation of dialysis. These patients often require high-cost inpatient hospitalizations before they can be stabilized, and infections are common from emergency catheterizations. Overall, crash dialysis starts are more expensive and traumatic experiences than planned dialysis, and these patients are much more likely to end up using in-center dialysis as opposed to dialysis at home.

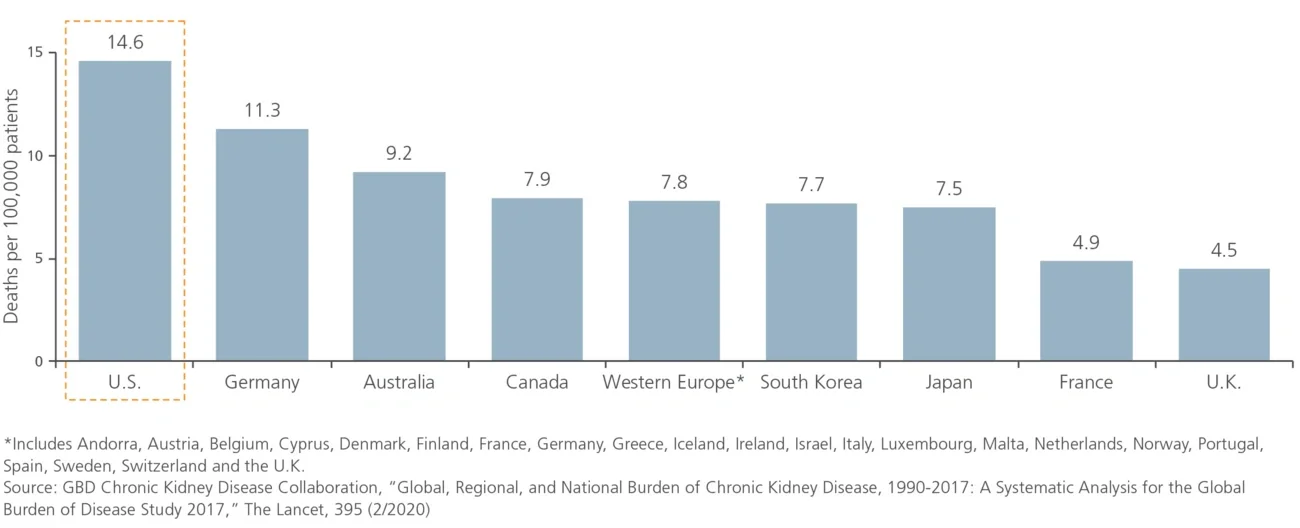

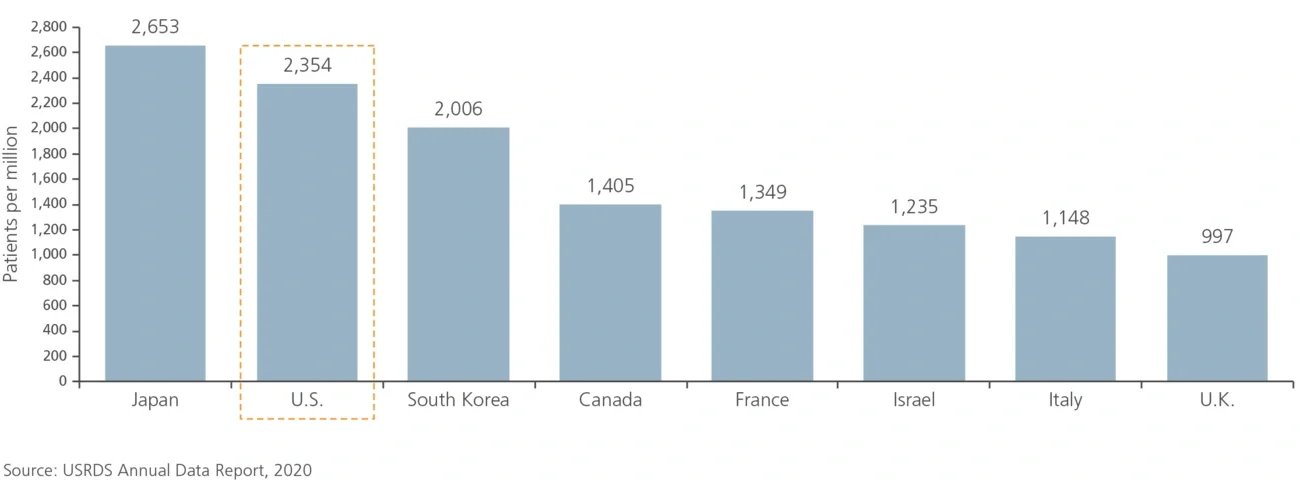

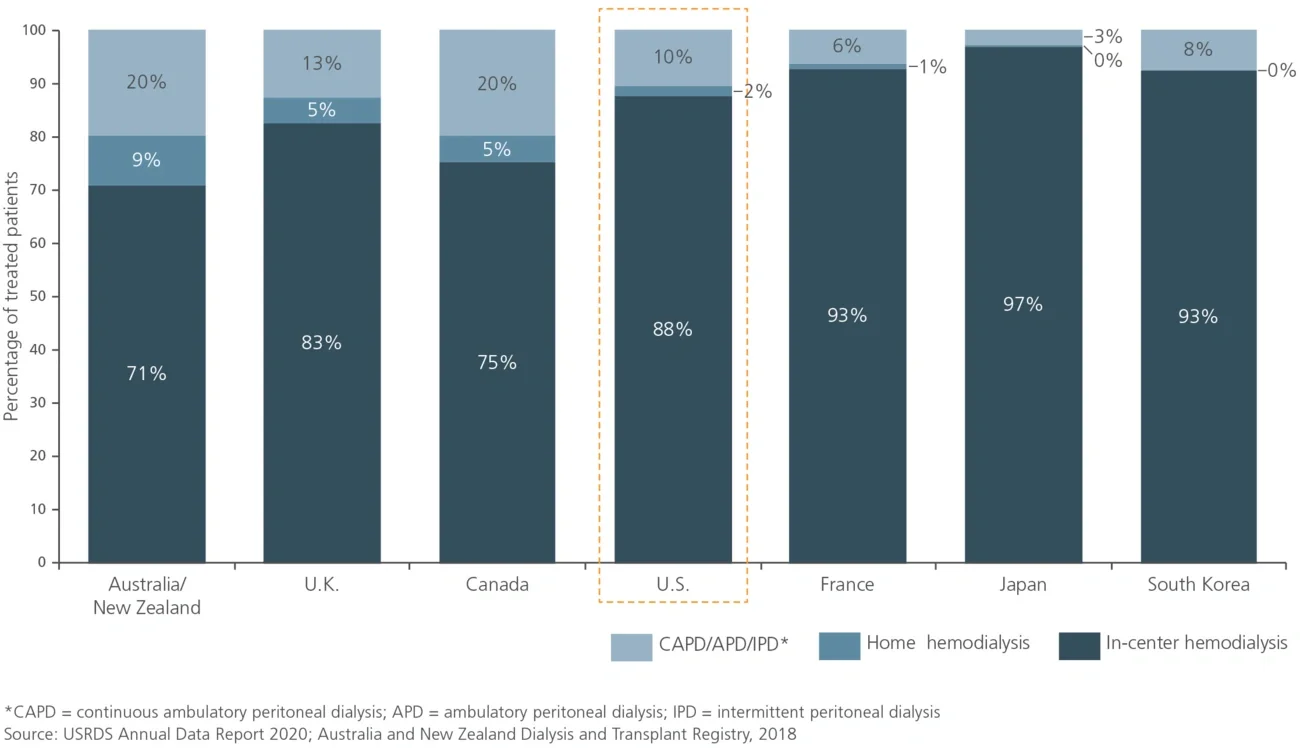

The U.S. also experiences poorer health outcomes for CKD patients than do other developed countries, despite the higher expense. The age-adjusted mortality rate for CKD patients in the U.S. is approximately double the rate in Western Europe and Japan and roughly 50% higher than in Australia (see Figure 2). ESRD is also a relative challenge for the U.S., with the prevalence of treated ESRD in the U.S. higher than in European counterparts and Canada by significant margins (see Figure 3). In addition, the U.S. does not leverage home dialysis (generally considered to be lower cost and easier on patients) as much as some other comparator nations, particularly Australia, New Zealand, Canada and the U.K. (see Figure 4). Taken together, high costs and poor health outcomes indicate a high level of clinical and administrative need for CKD patient management in the U.S.

Figure 2

Age-standardized CKD mortality rate by country (1990-2017)

Figure 3

Prevalence of treated ESRD by nation (2018)

Figure 4

Distribution of dialysis modalities for treated ESRD patients by nation (2018)

Despite the need, the U.S. healthcare system has traditionally been narrowly focused on ESRD while mostly ignoring early-to-midstage CKD. Due to a combination of factors, most stakeholders in the industry have either lacked the incentives to focus on CKD or felt little accountability for addressing kidney disease prior to initiation of dialysis.

Federal policy has focused historically on ESRD, starting with the 1972 expansion of Medicare, which created a specific carve-out for dialysis care. This policy specified that all patients with ESRD, regardless of age, are eligible for Medicare. Commercial payers have also devoted little energy to CKD, primarily because once patients progress to ESRD, they generally transition to Medicare following a 30-month coordination period. This reduces the incentives for commercial payers to implement programs that attempt to slow disease progression. The presence of a specified policy on ESRD, combined with the high visibility of ESRD compared to CKD, has created an institutional bias in healthcare policy that has only recently begun to shift.

The lack of focus on earlier-stage CKD management and intervention has been compounded by poor surveillance for CKD, leading to low diagnosis rates. The physical symptomology for most patients prior to the onset of ESRD is limited. This, combined with low primary care physician awareness of the warning signs that should trigger assessment of kidney failure, contributes to the poor identification of CKD patients. By the time patients are correctly diagnosed, their CKD is often advanced, which limits the opportunities to delay disease progression meaningfully through pharmacotherapy and lifestyle interventions.

Multiple forces at the level of public health policy, legislative action and private-sector innovation have converged to accelerate the pace of change in the CKD space today compared to the relative lack of attention that has defined the past several decades.

The Centers for Medicare & Medicaid Services (CMS) are pushing for better models of kidney care that include a focus on CKD, demonstrating the agency’s acknowledgment of deficiencies in the current system and its commitment to driving improvements at the policy level. Key programs were announced in 2019, with target implementation by 2022:

- The Kidney Care First (KCF) and Comprehensive Kidney Care Contracting (CKCC) models will increase incentives for CKD management activities that delay progression to ESRD and incentivize kidney transplants; these programs will also introduce VBC incentives for clinicians that may include opportunities for clinicians to take on financial risk for late-stage patients

- ESRD Treatment Choices (ETC) will adjust CMS payments to clinicians and ESRD facilities to promote dialysis at home, which is made more feasible by the holistic care incentives introduced in KCF and CKCC

Recent legislative action is also having an impact. The 21st Century Cures Act, passed in 2016, enables ESRD patients to switch from traditional Medicare coverage to Medicare Advantage (MA), thus pushing MA plans to seek VBC solutions to manage the anticipated influx of costly ESRD members.

Further, an executive order (Advancing American Kidney Health) was issued in 2019, which created incentives for providers to delay patient progression to ESRD as well as improve diagnosis and surveillance efforts for early-stage CKD. It also established ambitious goals around the promotion of dialysis at home and increasing access to kidney transplants, both of which are expected to help reduce lifetime ESRD costs.

The combination of new government programs, the increasing relevance of MA and the development of new VBC solutions represents a major change in the healthcare industry, which now has significant incentives to delay the progression to ESRD by better managing CKD patients. Collectively, these recent changes have formed a catalyst for action in the private sector, where several secular trends are also contributing to improvements in the management of CKD and ESRD patients.

- Commercial and MA payers are embracing VBC and shifting their strategies to include more financial risk sharing

- The emergence of better data analytics tools has significantly increased the ability to mine patient and claims data for clinically relevant information (e.g., clinical decision support, better risk stratification, missed diagnoses)

- The proliferation of better care management models is increasing the capability of payers and risk-bearing provider groups to influence outcomes through better patient engagement and improved care coordination among disparate clinical stakeholders

The confluence of increased governmental focus on kidney health and new incentives for better management of renal patients has created a new set of needs for payers and risk-bearing providers who are eager to implement VBC solutions. In response, the market for KHM is rapidly emerging.

Multiple vendors (e.g., Somatus, Strive Health, Cricket Health, Monogram Health, Healthmap Solutions) are providing KHM services to public and private payers today. The specific care models and analytical tools vary from company to company, but in general, these KHM vendors seek to partner with payers and other risk-bearing entities to improve renal health outcomes and lower TCOC. The primary levers of cost reduction include preventing the crash into dialysis, avoiding unnecessary hospitalizations and visits to the emergency room, delaying the onset of dialysis, and promoting in-home dialysis.

Recognizing the increasing criticality of managing the high costs of kidney disease, payers are either partnering with KHM vendors or attempting to develop in-house KHM solutions that replicate third-party offerings. Whether payers eventually opt for partnerships or in-house solutions (either organically developed or potentially by acquiring existing KHM vendors), the interest in KHM appears to be both robust and long term.

We are still in the early stages of adoption and evolution of KHM models. Market participants estimate that KHM models, if fully optimized strategically and implemented successfully at the tactical level, could reduce TCOC in CKD by 20%-30%. This would require the refinement of existing activities and the creation of new ones. Some example drivers of savings include new initiatives related to increasing the utilization of dialysis at home, innovations in pharmacotherapy, increasing the effectiveness of lifestyle interventions through the use of behavioral science, and leveraging a broad set of tools to drive transplant success.

- Home dialysis has the potential to reduce TCOC for patients who are healthy enough (peritoneal dialysis or limited hemodialysis is less expensive than in-center hemodialysis, but not all patients are eligible)

- Optimization of pharmacotherapy through the redesign of pharmacotherapy treatment plans and supports for patient adherence can reduce utilization of preventable inpatient care

- While lifestyle interventions are already a well-known part of KHM, adherence and efficacy are not yet optimized; leveraging learnings from behavioral science in an omnichannel engagement strategy could potentially impact patient behavior enough to meaningfully delay disease progression

- Optimization of transplant success via medication adherence solutions guided by behavioral science and digital patient monitoring can reduce post-transplant costs, including kidney transplant failure

The rapid evolution of the kidney care landscape over the past three years represents a transformation in the management of kidney disease and addresses a previously underserved series of challenges in the U.S. healthcare system while creating opportunities for both payers and vendors in the KHM space. Led by third-party vendors, the field of KHM is quickly growing and applying principles of managed care to improve outcomes and reduce cost in this traditionally deprioritized area of U.S. healthcare.

Editor’s Note: The Evolution of Kidney Health Management and the Next Frontier, originally published on 10/1/21, erred in its Figure 4 distribution of dialysis modalities by nation. This figure was revised and republished on 10/21/21.