The nonresidential construction value chain has felt the full effects of COVID-19. Although 2020 is set to be a challenging year, certain market segments such as ecommerce logistics facilities (e.g., distribution and sortation centers) and warehouses may be in a better position than others to weather the storm.

With this in mind, what should you know about the ecommerce fulfillment commercial construction outlook?

- Sustained ecommerce sales penetration and parcel volume growth are expected to drive long-term market growth; COVID-19’s impact on consumer behavior may drive a step-change increase in ecommerce penetration in the near term

- Warehouses and distribution and sortation centers that support ecommerce fulfillment are forecast to outpace growth in “traditional” warehouses (i.e., those that do not support ecommerce fulfillment activities)

- Expansion plans in fulfillment and logistics facilities have the potential to accelerate in the coming years due to long-term planned strategies (e.g., one-day/same-day shipping, last-mile expansion) and near-term COVID-19 needs (e.g., forward-positioning more inventory for surged demands)

What does the mean for you?

Contractors and service providers. The capex outlook for warehouses and distribution and sortation centers will create a greater need for cost-effective scaling of ecommerce infrastructure, network planning, ecommerce build-outs and retrofits, and increased automation. Further, demonstrating performance on key success factors — namely availability and execution speed — for serving new-build and repair-and-remodel (R&R) demands in the near term is important for contractors’ and service providers’ success.

Building products manufacturers. Shifts in consumer purchase behaviors and expectations of sustained ecommerce penetration will create fundamental changes in the ways manufacturers engage with customers, sell products and distribute/fulfill orders. The construction ecosystem must adapt to serve this demand through both consolidated national logistics players and localized distribution and sortation centers.

Investors. Asset owners and developers will need to develop strategies for positioning their portfolios to serve growing ecommerce fulfillment networks and a potential supply chain on-shoring trend.

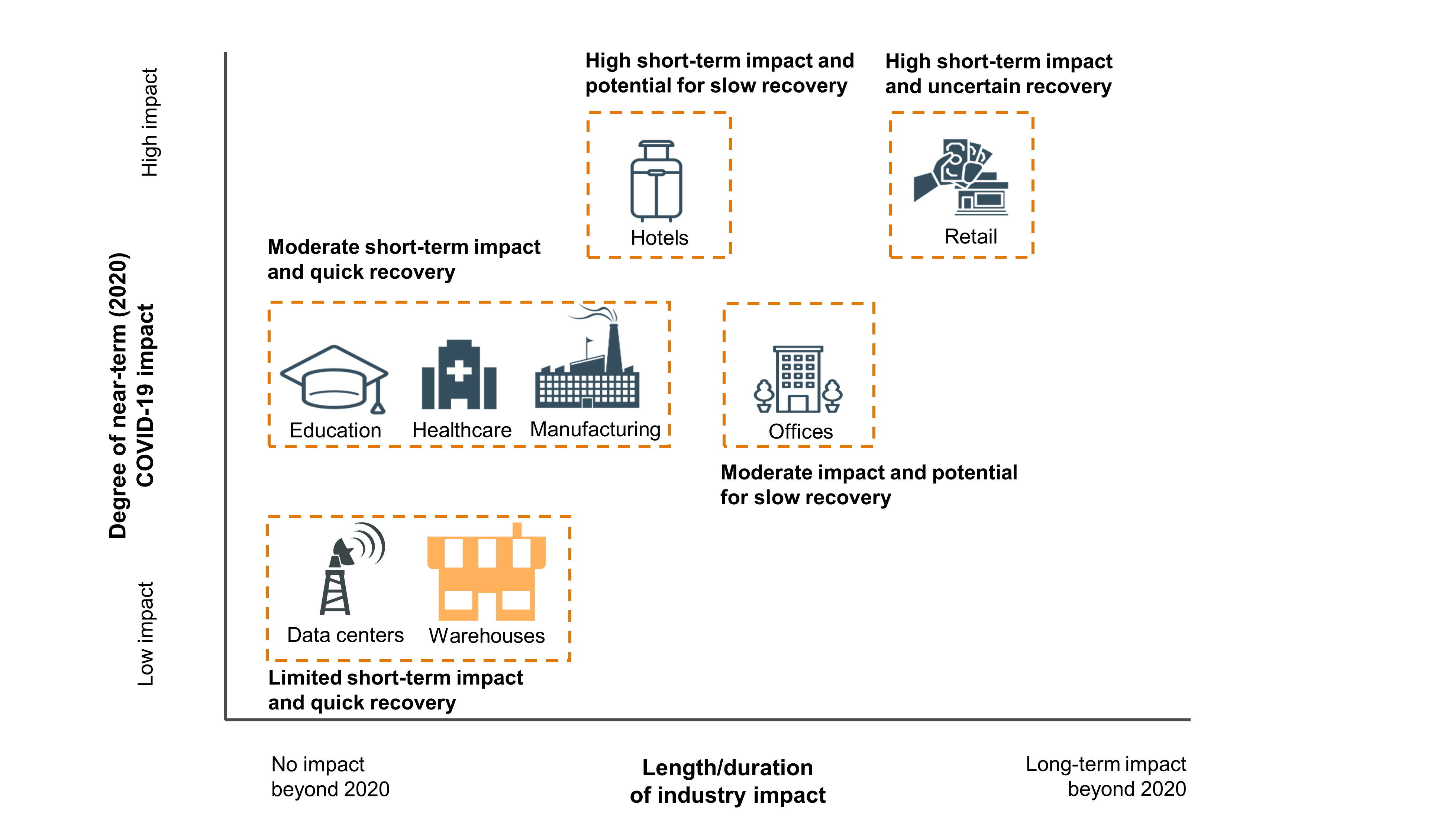

The eye of the storm

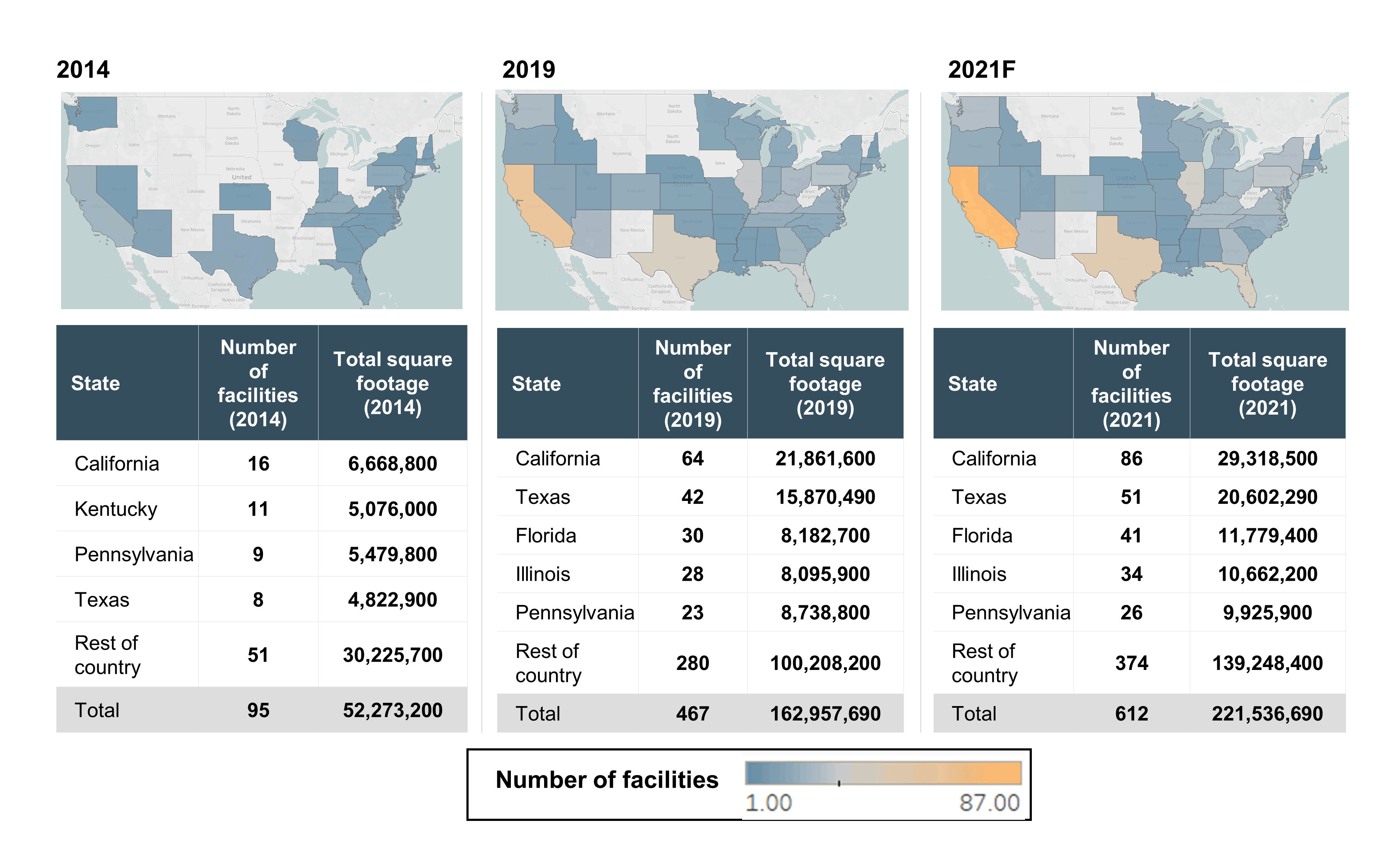

Distribution and sortation centers, particularly those involved in the support of ecommerce fulfillment, are in the rare situation of being fairly well insulated from the challenges of COVID-19. Attractive market fundamentals, including continued ecommerce sales penetration, growth in parcel shipping and ecommerce capex, play a role in insulating distribution and sortation centers and warehouses from COVID-19 effects. Additionally, warehouse construction may benefit as businesses look to build regional supply chain models in order to minimize potential supply disruptions from overseas, reduce dependence on foreign manufacturing for essential goods and expedite delivery times. So unlike some other segments, distribution and sortation centers and warehouses are not expected to see much of a near-term impact (see Figure 1). In fact, they may actually benefit from the potential near-term step-change in demand and longer-term continued growth in ecommerce penetration that is predicted to occur over the next three to five years.

Long-term ecommerce tailwinds and near-term increase in penetration

Long-term demand trends: Ecommerce sales penetration and parcel volume growth

The long-term outlook for ecommerce fulfillment commercial construction activities is buoyed by positive underlying market factors including ecommerce sales penetration and growth in parcel volume.

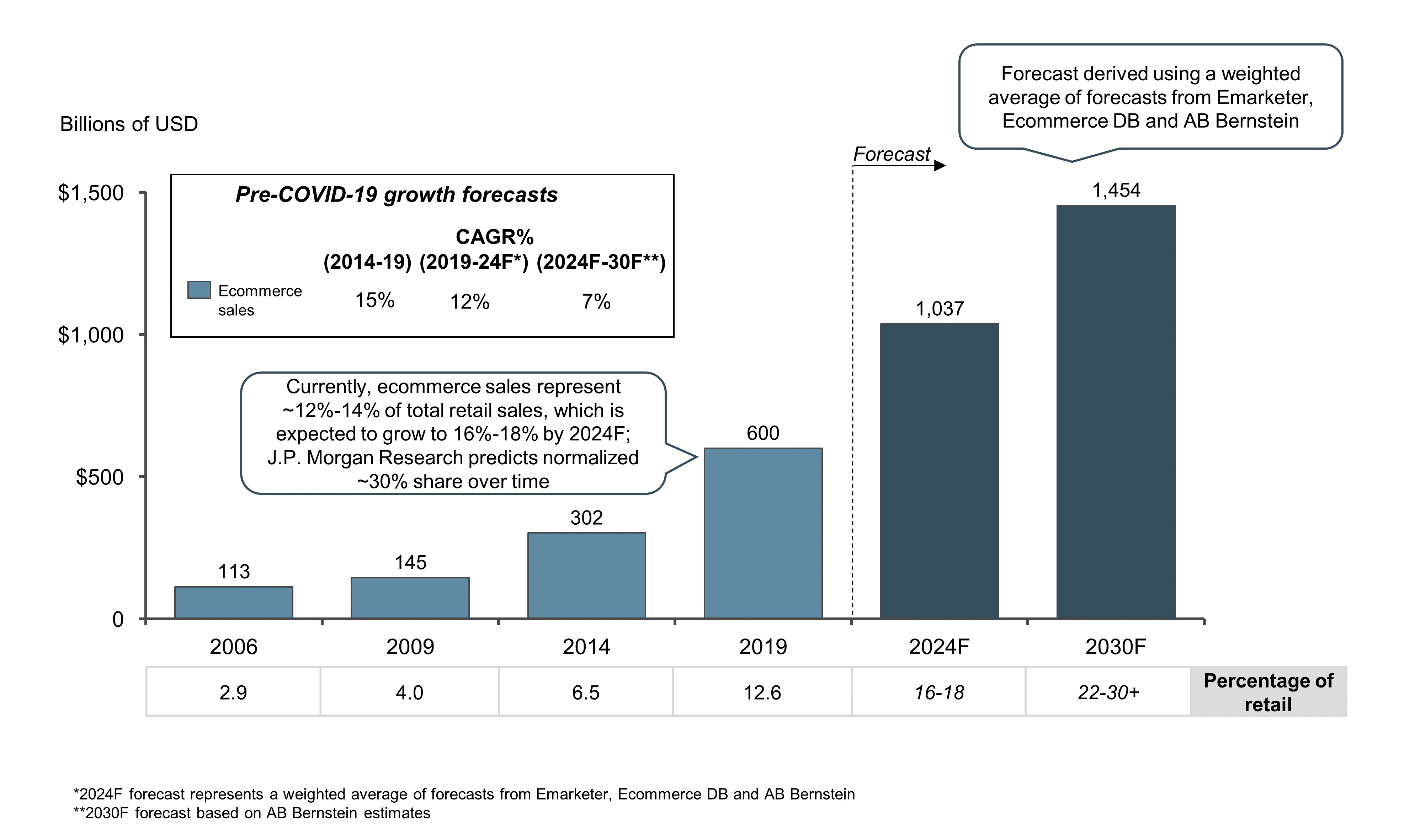

Based on pre-COVID-19 consensus estimates across retail and financial analysts, ecommerce is underpenetrated in the U.S. relative to international proxies, currently comprising ~12% of all retail sales compared with an estimated 25%-30% penetration in China and ~19% penetration in the U.K.1 Consensus estimates forecast continued penetration of U.S. ecommerce vs. brick-and-mortar retail through 2030, reaching more than twice current levels (see Figure 2). This trend suggests a runway for ecommerce growth, which will require significant investment in ecommerce fulfillment infrastructure to meet demand.2

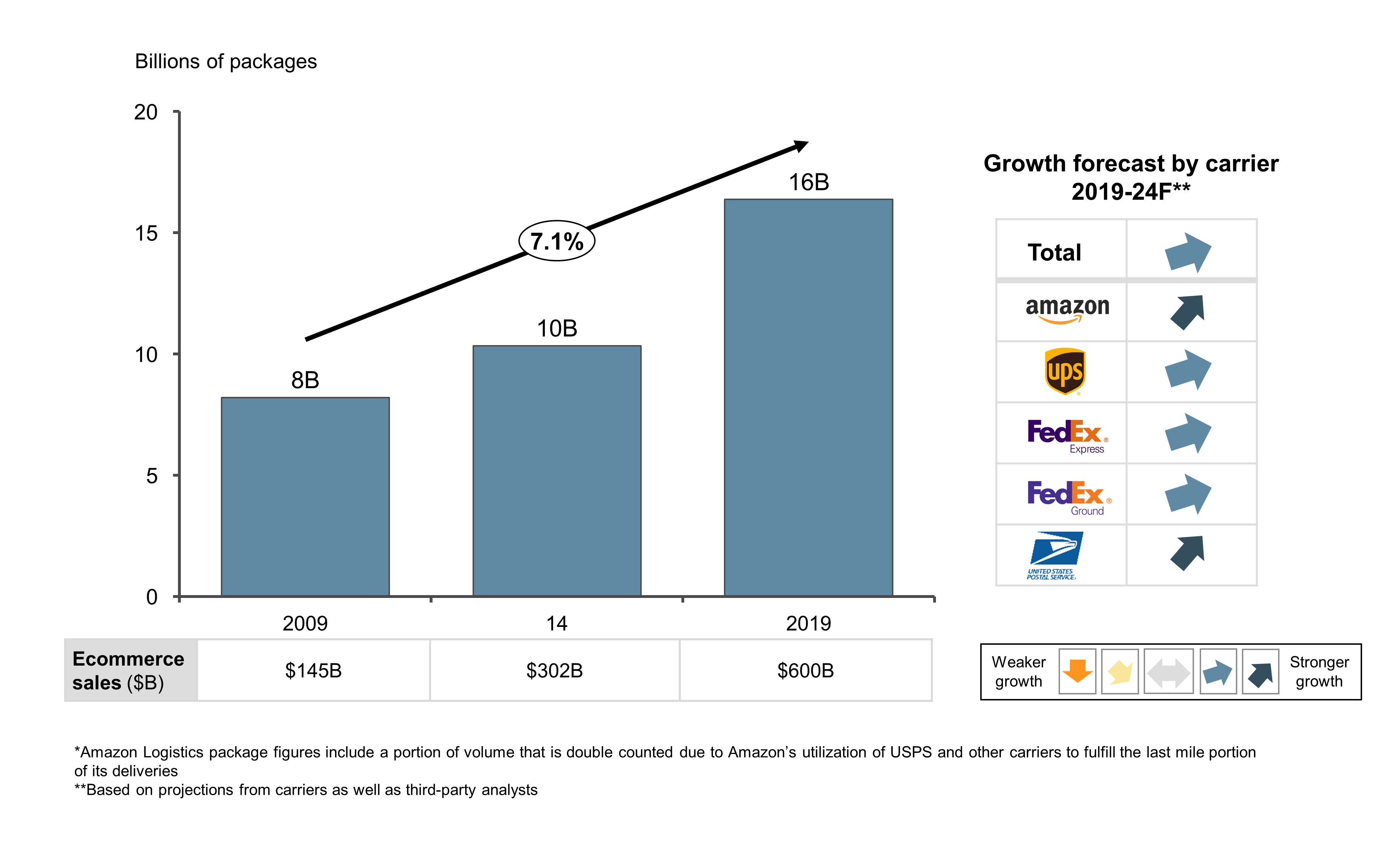

In addition, parcel volume has grown by ~7.1% p.a. from 2009 to 2019, driven by both ecommerce demand and packaging stock-keeping unit (SKU) proliferation. Based on pre-COVID-19 estimates, U.S. total package volume is forecast to enjoy strong growth over the next 5 years due to the expected continuation of historical trends (see Figure 3).3 Based on a recent survey of distribution centers and warehouses by Logistics Management, the average peak utilization for warehouses and distribution centers was 82.5% in 2019, with 20% reporting an average peak utilization of 95% or higher. Viewed in the context of high utilization rates, growing parcel volumes will necessitate increasing the capacity of ecommerce fulfillment networks (e.g., distribution and sortation centers), including the construction of new sites, the retooling of existing facilities and the implementation of warehouse automation to improve throughput.

Near-term demand impacts due to COVID-19 effects

The COVID-19 outbreak has created a near-term surge in ecommerce demand that is accelerating the long-run trends in ecommerce penetration in the U.S., with potentially long-lasting effects. The COVID-19 crisis and associated government response have created an environment where consumers are more likely to change traditional purchasing behaviors to the benefit of ecommerce. As brick-and-mortar retail locations have closed en masse and social distancing protocols have raised concerns about the safety of in-store shopping, particularly for vulnerable populations, there has been a significant surge in ecommerce demand.

The COVID-19 crisis has accelerated ecommerce adoption in the U.S., encouraging portions of the population that have never shopped online before to look to ecommerce as a new option. For example, there has been a 95% year-over-year growth in U.S. ecommerce orders as of June 1 based on CCInsights.org.4 Another indication of COVID-19’s impact on ecommerce demand can be seen in the recent surge in job postings for ecommerce and storage positions. ZipRecruiter has seen significant growth in ecommerce and storage job postings in March 2020, with particularly large increases in postings for warehouse handlers (699% increase), online merchants (354%) and warehouse attendants (324%).

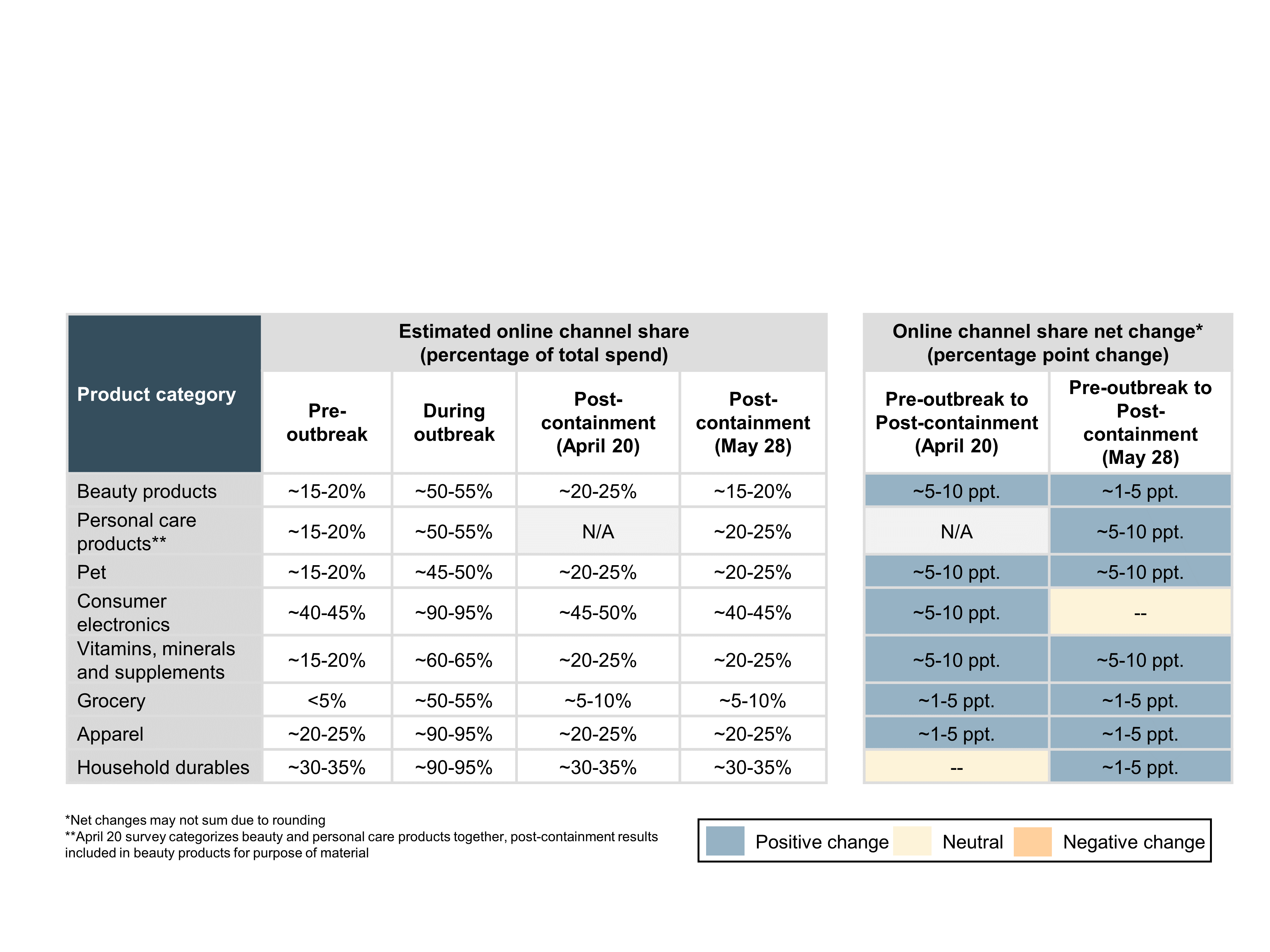

Although partly contingent on the duration of the COVID-19 crisis, a prolonged period of exposure to the ecommerce channel may lead to an accelerated rate of penetration in certain product categories that may persist over the long term. Recent L.E.K. Consulting consumer sentiment surveys indicate that many product categories are expected to retain a portion of their ecommerce share gains even after the outbreak is contained. Based on consumer feedback, higher purchase frequency product categories such as personal care, pet, and vitamins, minerals and supplements are expected to retain the most ecommerce share gains post-COVID-19, while categories such as consumer electronics and household durables are expected to revert back to mostly pre-COVID-19 levels (see Figure 4).

Takeaway: Shifts in consumer purchasing behaviors and expectations of sustained ecommerce penetration will create fundamental changes in the ways companies engage with customers, sell products and distribute/fulfill orders. The construction ecosystem must adapt to serve this demand through both consolidated national logistics players and localized distribution centers.

Warehouses and distribution and sortation centers that support ecommerce fulfillment are forecast to outpace the growth of traditional warehouses

Growth expectations for distribution and sortation centers and warehouses that support ecommerce facilities are higher compared with those that do not support ecommerce activities. Ecommerce fulfillment distribution and sortation centers and warehouses are forecast to take an outsized portion of market growth, with projected high single-digit growth over the next three to five years, driven primarily by underlying ecommerce demand.4 Given increases in ecommerce sales penetration and parcel volume growth, strong capex investment is expected to flow into the portion of the market that supports ecommerce fulfillment. Players such as Amazon, UPS, FedEx and the U.S. Postal Service have invested billions in their distribution networks from 2016 through 2019 (~14% CAGR), a trend that is expected to continue over the next three to five years.

In contrast, traditional warehouses (i.e., those that do not support ecommerce activities) are expected to experience flat to low single-digit growth over that same period. Traditional warehouses do not benefit from the attractive underlying demand trends of ecommerce and are typically less resilient to market downturns. In addition, commercial real estate analysts have recently observed higher vacancy rates among traditional warehouses and expect the segment to continue underperforming relative to ecommerce-oriented facilities.5

Takeaway: The capex outlook for warehouses and distribution and sortation centers supporting ecommerce fulfillment is particularly attractive and will create a greater need for cost-effective scaling of ecommerce infrastructure, network planning, ecommerce build-outs and retrofits, and increased automation in the future.

3. Capacity constraints and delivery time objectives accelerating build-out

The recent spike in ecommerce demand attributable to COVID-19 has the potential to accelerate build-outs, both planned and unplanned, in the near term (and possibly longer term). Major ecommerce retailers had planned aggressive expansions to their distribution networks pre-COVID-19 to enable faster delivery models and increased capacity. There is a delivery time “arms race” in the industry, as major players are competing to offer consumers faster delivery times, rapidly moving from two-day delivery models to same-day delivery models to two-hour delivery models in certain geographies. For example, an estimated 150 new facilities focused heavily on last-mile delivery capabilities are expected to come online for Amazon in 2020 and 2021 (see Figure 5).6

The ecommerce demand spike due to the COVID-19 crisis has strained the ability of ecommerce retailers to fulfill orders while maintaining the delivery times that consumers have become accustomed to. As a result, online retailers and third-party logistics providers may accelerate their ecommerce capex plans over the next few years (even through a recessionary period) to boost capacity and maintain delivery time objectives.

In addition to possibly accelerating planned ecommerce capex, major ecommerce retailers are exploring unplanned “emergency warehouse” space to serve COVID-19 outbreak demands with better forward positioning of essential products. Adding incremental ecommerce infrastructure to their networks (particularly for last-mile delivery) can enable ecommerce providers to position their inventories closer to densely populated areas and maintain short delivery times despite surging demand. In a recent interview, a JLL executive indicated that he expects ecommerce companies to drive much as 50% absorption of industrial leasing volume through the end of the year.

While investment in distribution and sortation centers and warehouses that support ecommerce fulfillment is expected to continue unabated (or even accelerate), traditional warehouse demand may also experience demand shifts due to COVID-19 effects. The COVID-19 crisis has highlighted downsides of the global supply chain model, which relies on sourcing goods from overseas. During the crisis, U.S. federal and state governments have had to contend with significant shortages of medical supplies due to a reliance on overseas manufacturing and a shortage of stockpiled goods domestically. In response to COVID-19 effects on supply chains, there is potential for increased localization of supply chains in the U.S. (i.e., on-shoring), which could drive the build-out of regional supply chains and strategic stockpiles to the benefit of traditional warehouses and distribution centers. CBRE Research estimates that a 5% increase in domestic business inventories would require an additional 400 million to 500 million square feet of warehouse space.

Takeaway: Demonstrating performance on key success factors — namely availability and execution speed — for serving new-build and R&R demands in the near term is important for contractors’ and service providers’ success. In addition, asset owners and developers will need to develop strategies for positioning their portfolios to serve a potential on-shoring trend.

How to make the most of this opportunity across the ecommerce and logistics infrastructure ecosystem

There are several key issues that investors, manufacturers and distributors should consider in these unprecedented times.

For investors:

- What are potential contracting and service provider rollup strategies to consider?

- What are key emerging market trends and implications for the ecommerce fulfillment commercial construction market (e.g., digital/industry 4.0., warehouse automation)?

For manufacturers:

- What digital customer engagement changes should be made to adapt to an evolving market?

- What strategies should be considered for adapting internal distribution and fulfillment capabilities for parcels vs. pallets?

- How has consumer behavior and key purchase criteria changed due to the COVID-19 crisis?

- What processes and strategies should be employed to enable greater agility in product design?

For distributors:

- What are the omnichannel distribution implications for ecommerce fulfillment trends?

- How should sales organizations adapt to optimize performance in a rapidly evolving market (e.g., go-to-market changes, incentive realignment)?

- How can networks be optimized to best meet demand for traditional and ecommerce fulfillment?

Conclusion

The COVID-19 crisis will undoubtedly have a significant impact on the building and construction market in the U.S. However, ecommerce fulfillment construction is expected to demonstrate resiliency and present opportunities for near- and long-term growth in these unprecedented times.

Editor’s note: Corey Highfield, Manager, and David Schulman, Consultant, contributed to this report.

Endnotes:

1U.S. Department of Commerce, Centre for Retail Research, Inside Retail Hong Kong, China Daily

2J.P. Morgan, AB Bernstein, Emarketer, Ecommerce DB

3Company annual reports, U.S.Postal Service annual report, Pitney Bowes, Morgan Stanley.

4L.E.K. market interviews and analysis

5Dodge Data and Analytics

6Amazon 10-K filings, company press releases, MWPVL.

01052021090158