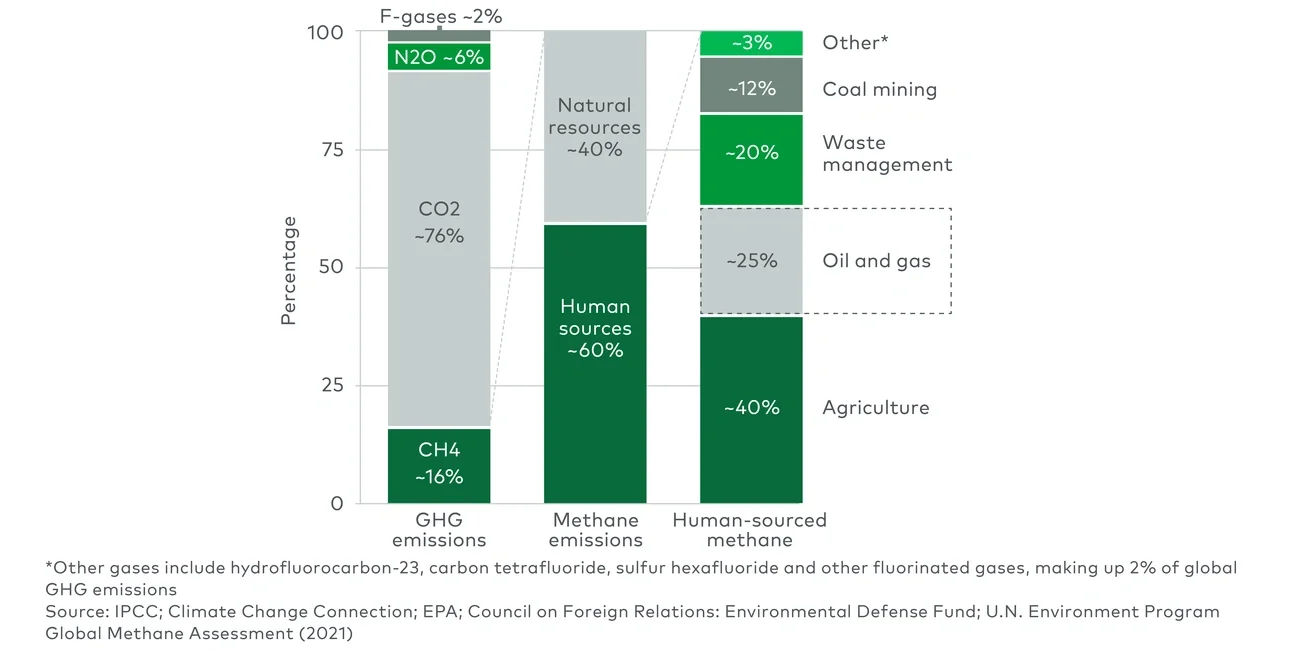

Methane emissions waste a valuable commodity. They’re also a key contributor to global warming, accounting for roughly 16% of greenhouse gases. These two factors have led to a consensus among industry leaders and environmentalists that it makes sense to curb leakages of methane gas.

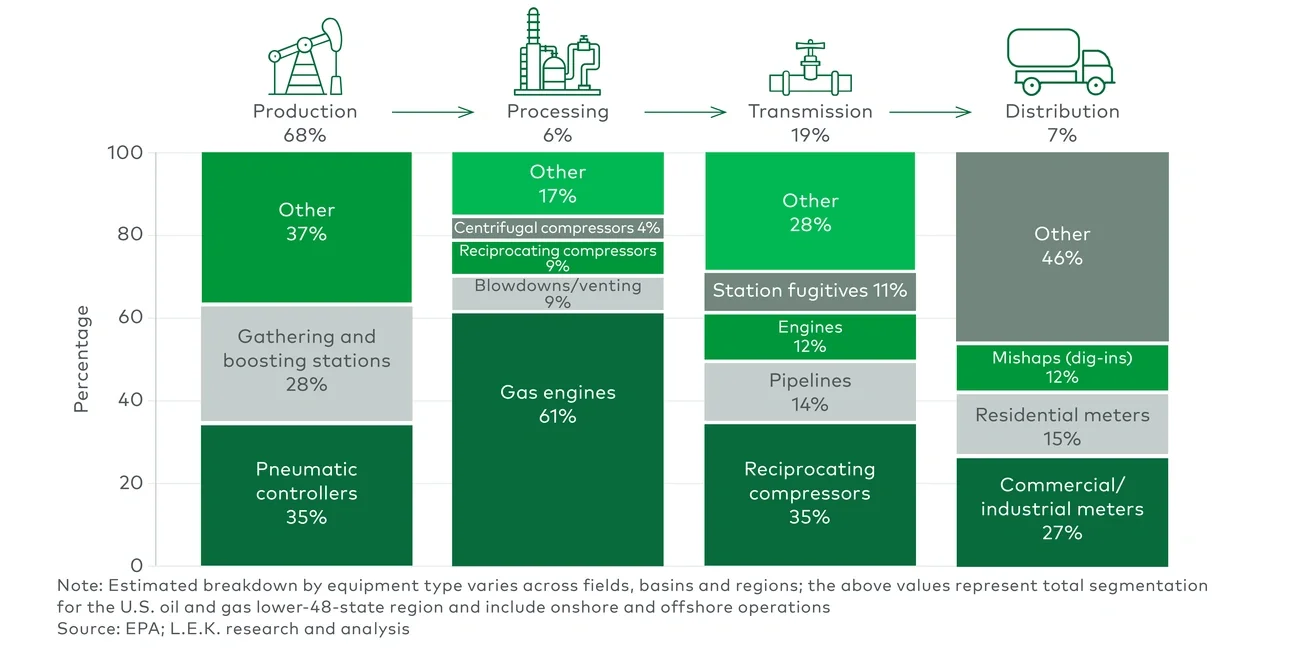

Sources of methane emissions are heavily concentrated in the oil and gas sector, which is navigating a broader transition to cleaner, lower-carbon energy. As more oil and gas companies commit to net-zero targets, controlling methane emissions may be the fastest way to make good on the pledge to improve their carbon footprint. This has prompted changes in upstream processes and investment in new technologies.

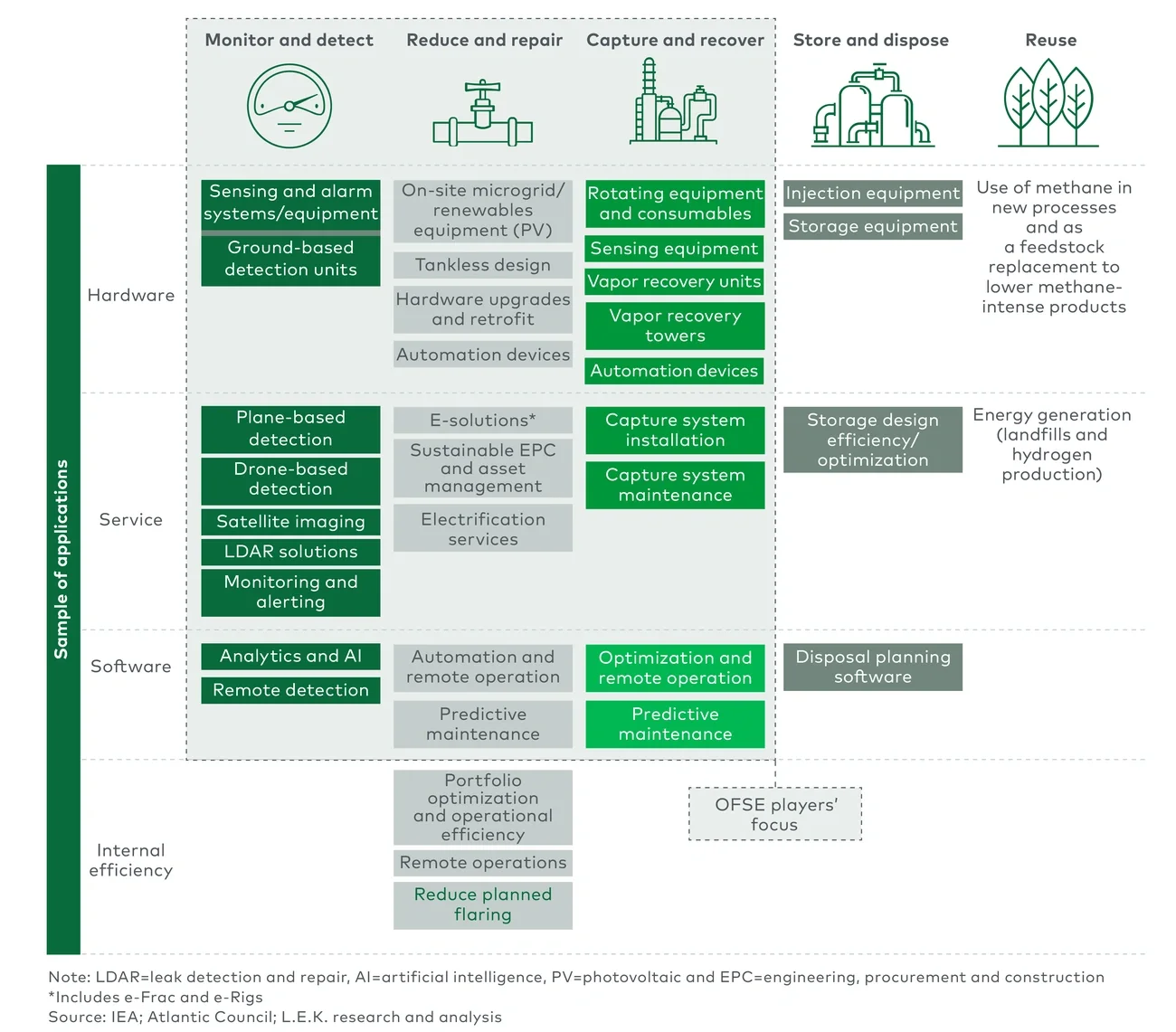

To size up the potential of the emerging methane management market, industry executives and investors need to ask these four questions:

- How big of a problem are methane emissions in oil and gas?

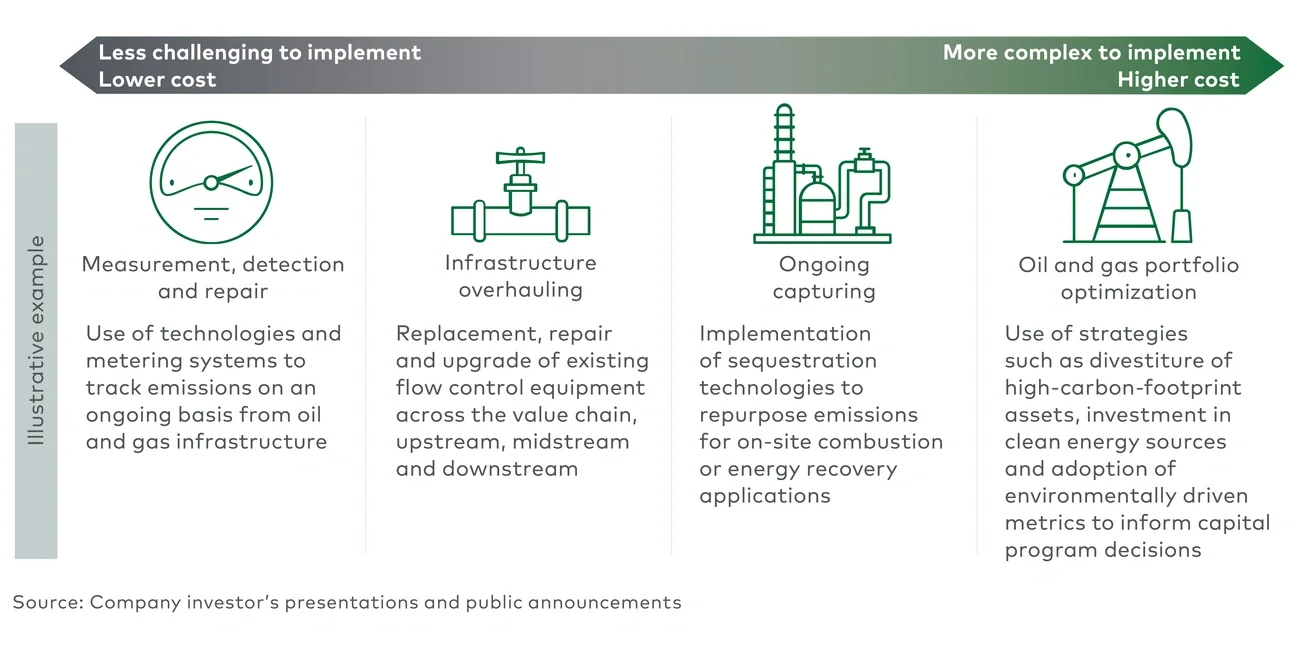

- How do companies address methane emissions today?

- What are the key challenges to reducing methane emissions?

- Where are opportunities to invest in the market?

Here’s what we know so far.

How big of a problem are methane emissions in oil and gas?

Most of the conversation around climate change and the environmental impact of emissions has been about carbon dioxide and carbon footprint. Carbon dioxide does account for most of the GHG from human activity. Unlike other reactive gases, it also stays in the atmosphere for hundreds of years.

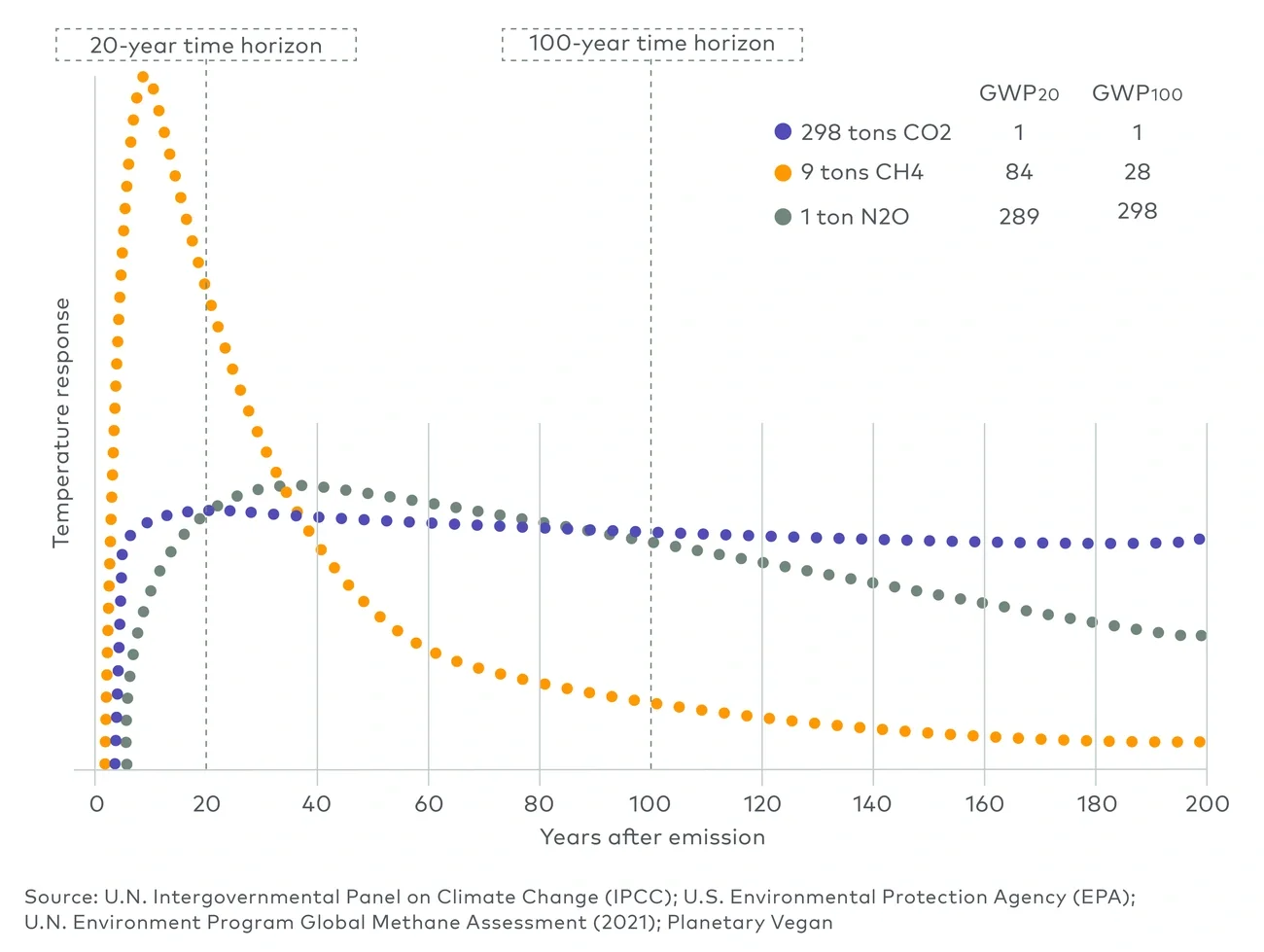

So why are methane emissions so relevant? One way to evaluate the relative effect of a GHG is by looking at its global warming potential (GWP), which measures how much energy one ton of the gas will absorb over time versus one ton of carbon dioxide (see Figure 1). The U.S. Environmental Protection Agency estimates that methane has a 100-year GWP of 28-36. In other words, it’s at least 28 times more potent than carbon dioxide over the course of a century. In the shorter term, measured over 20 years, methane’s GWP soars to 84 times that of carbon dioxide.