Key takeaways

-

Consumers are making fewer store trips, so brands have to think and act in new ways to stay in front of consumers and drive brand consideration.

-

We have seen “lost sales” in many instances when distribution has moved from physical to digital.

-

As digital technologies rapidly develop and transform the way consumers interact with brands, many management teams struggle just to stop the associated sales leakage, let alone find ways to grow.

-

In this environment, four key strategies are essential for brands to consider as they seek to define a future-state business model capable of delivering growth.

Seventy-six percent of U.S. consumers have purchased a product they discovered through a brand’s social media post.1 Globally, 83% of people trust a referral from a family member or friend when deciding what to purchase (or where to purchase it) — making personal connectivity one of the most powerful ways to reach and influence consumers.2

While stores continue to be important, over 85% of consumers have used their phone to conduct research while in a store, and 43% use their phone in-store explicitly to check for deals and better pricing.3 In almost all consumer product categories, consumers are making fewer store trips, so brands have to think and act in new ways to stay in front of consumers and drive brand consideration. We have seen “lost sales” in many instances when distribution has moved from physical to digital. In fact, when a store closes (whether owned by the brand itself or by a third-party retailer), typically a very low percentage of the brand’s sales transfer to online, mobile or other digital channels.

As digital technologies rapidly develop and transform the way consumers interact with brands, many management teams struggle just to stop the associated sales leakage, let alone find ways to grow. To date, brands have tended to solve this issue by looking downstream ― to their channel and delivery strategies. However, in the new paradigm, we believe success lies in excelling both upstream and downstream. We encourage brands to spend just as much, if not more, effort on upstream strategies such as product development and awareness and conversion-driven marketing.

In this environment, four key strategies are essential for brands to consider as they seek to define a future-state business model capable of delivering growth (see Figure 1).

Adopt a “demand creation” approach

The reality of fewer physical points of distribution is that those remaining points, as well as your own channels or new channels, need to be more productive. This usually means that brands can’t overly rely on traditional retail partners to drive sales demand for them. Instead, if brands go on the offensive and succeed in creating material demand themselves, that demand can be pulled through their distribution network, regardless of its physical size. In other words, if consumers truly want your brand and products, they will find you. This allows brands to realize sales despite a shrinking distribution footprint, and in turn yields more control of the top line.

Demand creation is complex, but we like to zero in on three key areas:

- Brand awareness among and relevance to your target consumers. This combination leads to high “consideration” in the purchase moment. To be top of mind with target consumers and maximize traffic conversion, brands need to tap into a much broader suite of marketing vehicles.

- Preference over other brands. You want consumers to covet your brand. This is driven by superior differentiation on what matters most to the consumer. When a consumer is looking for a product in your category, ideally there will be no question in the consumer’s mind about which brand to choose. This can be achieved in various ways; most important, both brand and product need to be hitting on all cylinders.

- Brand presence. Your brand must be present in the daily lives of consumers in order for it to have a seat at the table when a purchase moment arrives ― or to stimulate such a moment. Platforms such as loyalty programs and personalized marketing can help you work your way in. As you move away from your top consumers, however, the task is much harder. You need to give consumers reasons to engage with you (meaningful experiences, frequent flow of new products, value-added content, meaningful stories that extend beyond product or commercial messaging but are relevant and worthy of engagement, etc.) outside of browsing or making a purchase.

A look into Nike’s demand creation

Nike takes a multidimensional approach to driving demand. Here are just a few examples of how they do this.

a) Community building

- The Nike Run Club not only provides motivation, music and tracking tools for fans, but also creates an online community for runners.

- The Nike Football Facebook fan page has 44 million likes, over 10 million more likes than Nike’s main Facebook fan page. The page has created a community for soccer players and fans.

- Similarly, the NikeWomen Instagram account and Facebook page have created a community for women. With posts of famous female athletes alongside nonfamous active women, the pages reinforce the company’s “if you have a body, you are an athlete” message.

b) Broad-based media advertising

- Through its use of broad-based media advertisement, Nike has made itself present in its consumers’ daily lives. The company, in addition to paid-television commercials, is a leader in the professional sports uniform space; you can’t watch an NFL or NBA game without seeing the brand’s products.

- As the brand appeals to a wide audience, Nike has been successful in its broad-brush approach while still maintaining a strong brand identity.

c) Highly interactive social media

- Last year, Nike Air Jordan collaborated with Snaps, an artificial intelligence (AI) platform on a Facebook Messenger bot that allows for two-way exchange between the brand and its audience.

- Another example of Nike’s innovative use of social media is Nike: Reactland, an immersive video game in which real-life Nike fans are the players, running past some of the world’s most famous landmarks.

Drive a much greater portion of sales via digital direct-to-consumer (DTC) channels

Doing this has many benefits, not the least of which are gap-filling for decreased store distribution and greater margin capture. The good news is, consumers are increasingly engaging with brands directly and are more willing to buy on brands’ sites or in their stores. In the past, brands focused on optimizing conversion on third-party retail websites, drafting off those sites’ much higher traffic. Driving sufficient traffic to the brand’s own site required much more investment with lower returns. While this is still true in many respects, today there is much more potential to capture meaningful sales on a brand’s own website. The explosive growth of major brands’ web traffic in recent years is evidence that consumers are finding value in direct engagement with brands as they browse and purchase. As many consumers have become more adept at online browsing, they are seamlessly and efficiently shopping brand sites on a regular basis.

Brands have historically made it very hard for consumers to buy on their sites. Brand sites have often employed pricing strategies that put them at a substantial premium to alternative channels, due to fear of degrading brand integrity and of inciting channel conflict with retail partners. Because consumers aren’t irrational, they treated these brand websites as channels of last resort and often chose to purchase elsewhere. Brands also were reluctant to market directly to consumers, which limited traffic. However, when brands behave as true retailers and take a more assertive, market-based approach, they can drive real traffic and sales volume. Achieving a double-digit total sales percentage from digital DTC was a noble aspiration in the past, but we’re now challenging brands to ask how within five years they can achieve at least 30% digital sales ― or upwards of 50% for more contemporary brands.

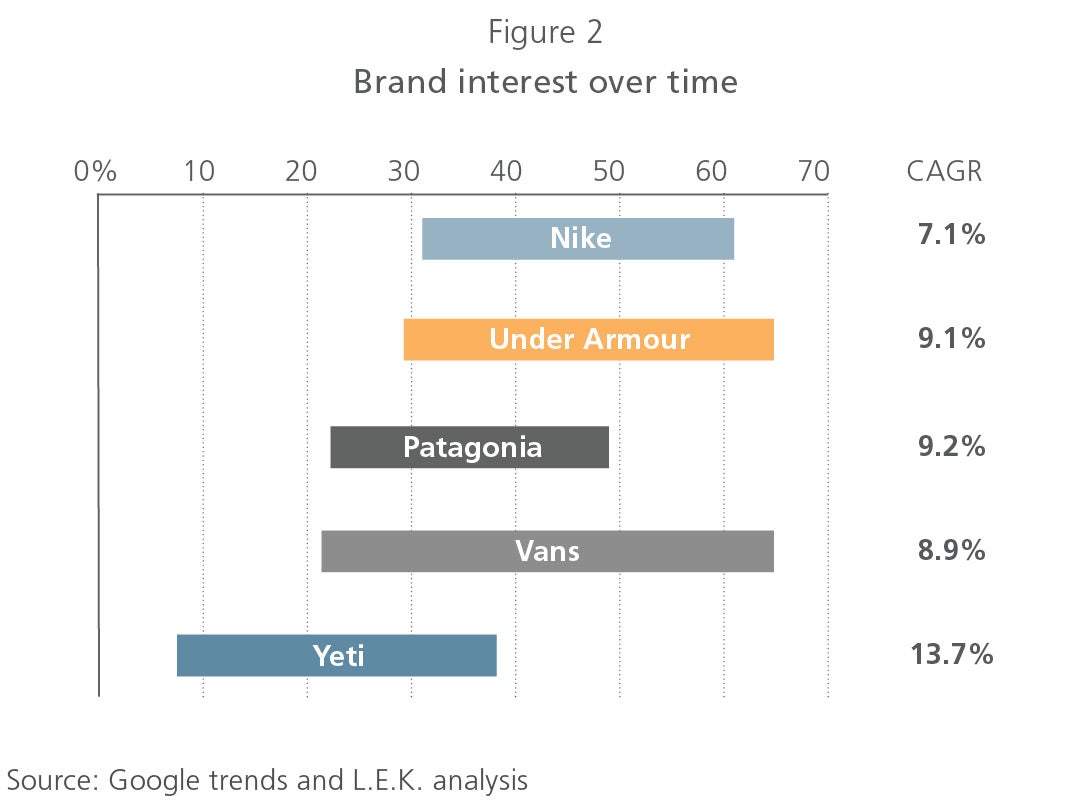

Many examples demonstrate that DTC can be a thriving channel when done right. Under Armour, for instance, captured 35% of FY 2018 global sales through its online and owned stores (see Figure 2). Other brands are also charging hard in growing DTC sales, with great success. For VF Corp. (the parent company of Vans, The North Face and other leading fashion brands), DTC accounts for roughly a third of sales, with goals to grow to over 50% of total company revenues by 2021. At Crocs, over 45% of sales in 2018 were DTC through its retail stores and ecommerce.

Dramatically improve your digital merchandising

Almost every (surviving) brand knows what it takes to merchandise its products effectively in-store. But when it comes to featuring brands and products effectively online, most brands have struggled to adapt to the challenges of the digital age: the constraints of computer and mobile screens, pages that limit the number of products consumers see, limitations on photos and video, countless brands vying for search rankings and page space share, paid ads, and so on. In the digital arena, merchandising excellence can make the difference between the consumer buying the product and the consumer not even knowing the product exists. Even if a brand’s full assortment is listed on a site, if the consumer can’t readily find a product or quickly recognize what differentiates it, that product might as well not be listed at all.

Digital merchandising excellence requires working strategically with digital channel partners to devise the right online strategies and content ― which often have little overlap with traditional in-store merchandising best practices. At a minimum, working with retail partners and sites to make sure your products are affiliated with the right categories, come up in the right searches, and are appropriately featured and promoted are all ways to drive consumers to your product. And once you get them looking at your product, getting them to buy requires that they be presented with the right information to get them to buy ― product features and benefits, compelling pictures and video, and other content that conveys the value proposition to create distinction from alternative products the consumer may consider.

The digital merchandising dilemma

In a store, the ways of getting your product in front of consumers are well understood — shelf placement, end cap displays, shop-in-shops, packaging, signage and other visual merchandising techniques. However, the digital world is arguably more complicated. Here are just a few of the reasons why:

- There’s not a common “front door.” Consumers can enter a website on various pages, depending on whether they directly type in the home page URL, or click through via a sponsored link or a Google search.

- Landing and category pages tend to be extremely broad, and there’s only so much room for a brand to occupy, if it’s even able to garner the space in the first place.

- The competing efforts of the retailer and brands fighting for real estate and ways to get noticed and drive click-throughs create tremendous “noise” to cut through.

- An “endless” aisle is a misnomer. First, screen space greatly limits the amount a consumer can see on a page. Further, many products easily get lost because they don’t appear high on search rankings or never get viewed because they sit “below the fold.”

- Product images and videos often fail to accurately or easily convey the products, their functionality, and even their true look and colors … or how they fit into a consumer’s home … or outfit.

- While product pages in theory present nearly a seemingly unlimited opportunity to showcase brand and product benefits, we too often find that many brands have very little to say and/or they do a poor job of saying or otherwise conveying it — resorting to dry lists of specifications or presenting only the minimum information.

Yeti’s approach to digital merchandising reveals best practices:

- First-class product images and videos that go to basics, to showcase product features as well as how the product is used in action (e.g., you can actually stand on the cooler in a boat and fly fish)

- Inspiring association of the brand with lifestyle across all it products (and on its site and all partner sites)

- Product details and content that show:

- Robust listing of product features (e.g., the “Vortex drain system” is “leakproof” and “designed for quick and easy draining”)

- Clear linkage of features to actual consumer benefits

- Deep social media presence showing lifestyle and benefits, meaning consumers are likely to shop for a “Yeti Cooler,” sidestepping the need to be on the front page (or “front door”) of ecommerce sites

- How its products and benefits fit into its target consumer’s lifestyle — easy to carry, rugged, serviceable equipment for an active lifestyle

- Insight into the practical functionality its products deliver (e.g., how many drinks each of its coolers holds, rather than just product specs)

- Robust listing of product features (e.g., the “Vortex drain system” is “leakproof” and “designed for quick and easy draining”)

Taken together, Yeti’s practices allow it to sidestep the front-door problem and maximize its chances of converting once customers reach its products.

Win with Amazon

Chances are that if Amazon isn’t already a meaningful sales channel for your brand’s category, it will be at some point in the future. About half of all product searches4 already begin on Amazon. Further, consumers are becoming more accepting of seeing premium brands on Amazon, and the ability of brands to achieve higher-quality brand positioning on the site will continue to improve. This means nearly every brand will want to be there, and in a way that maximizes the opportunity. While we see many brands participating on Amazon today and even claiming Amazon as their “No. 1 customer,” the fact is that their sales are still well below what is possible with a well-crafted, well-executed Amazon strategy.

Anker is a great example of a brand optimizing its Amazon relationship. Starting from zero in 2011, Anker became the leading Amazon seller and manufacturer of phone accessories and power delivery (including packs). They began with a simple set of core products (battery banks) and then carefully expanded to adjacencies where they could bank on the credibility of their products (e.g., cables and other accessories) before taking on further-afield products (wireless headphones). It embraced the exposure Amazon gives to partners that deliver quality products (measured by the number of 4- and 5-star reviews) on time. Anker also uses many digital marketing best practices, such as including rich content and brand attributes in the listing of even their cheapest iPhone cable. It has built a roughly $600 million business in seven years, almost exclusively by selling on Amazon. It is now leveraging this base and executing a broader DTC strategy.

Conclusion

For many brands, future sales are at risk because of less physical product placement and interaction with consumers, and a digital marketplace that is still not fully understood. Going on the offensive with these strategies should deliver more control of your destiny, mitigate risk and ideally drive growth (also see our Executive Insights: Total DTC: Building a Better Approach to Reach Your Consumers).

Endnotes

12017 Curalate survey

2Nielsen Global Trust in Advertising Report

3How mobile search is driving today’s in-store shopping experience

4More Product Searches Start on Amazon

09262019170942