Key takeaways

-

There is clear consensus in the U.K. lending industry that the next macro-economic move will be down, not up.

-

Credit performance deteriorates in many lending types during downturns, leading to fears about loan recoveries, profitability and the viability of lending businesses.

-

How real are these risks, how do they vary between different types of lending, and what opportunities might present themselves to well-informed funders, investors and lenders?

-

There will be casualties amongst specialist lenders should another downturn strike in the U.K., but those in robust form and agile enough to take advantage of the situation will generate substantial commercial gain.

It is tough to call the timing, but there is clear consensus in the U.K. lending industry that the next macro-economic move will be down, not up.

In downturns, credit performance inevitably deteriorates in many lending types, leading to fears about loan recoveries, profitability and even the viability of lending businesses — especially in specialist lending and still more so in sub-prime specifically.

These fears can apply across all types of lenders, their debt funders, and current and prospective equity owners, sometimes fuelled by loose anecdotal evidence from the credit crunch and its aftermath.

But how real are these risks, how do they vary between different types of lending and what opportunities might present themselves to well-informed funders, investors and lenders? This Executive Insights explores the industry dynamics and in particular where to play and how to win in specialist lending in a future downturn.

In the U.K., the credit crunch affected lenders’ funding much more than credit performance

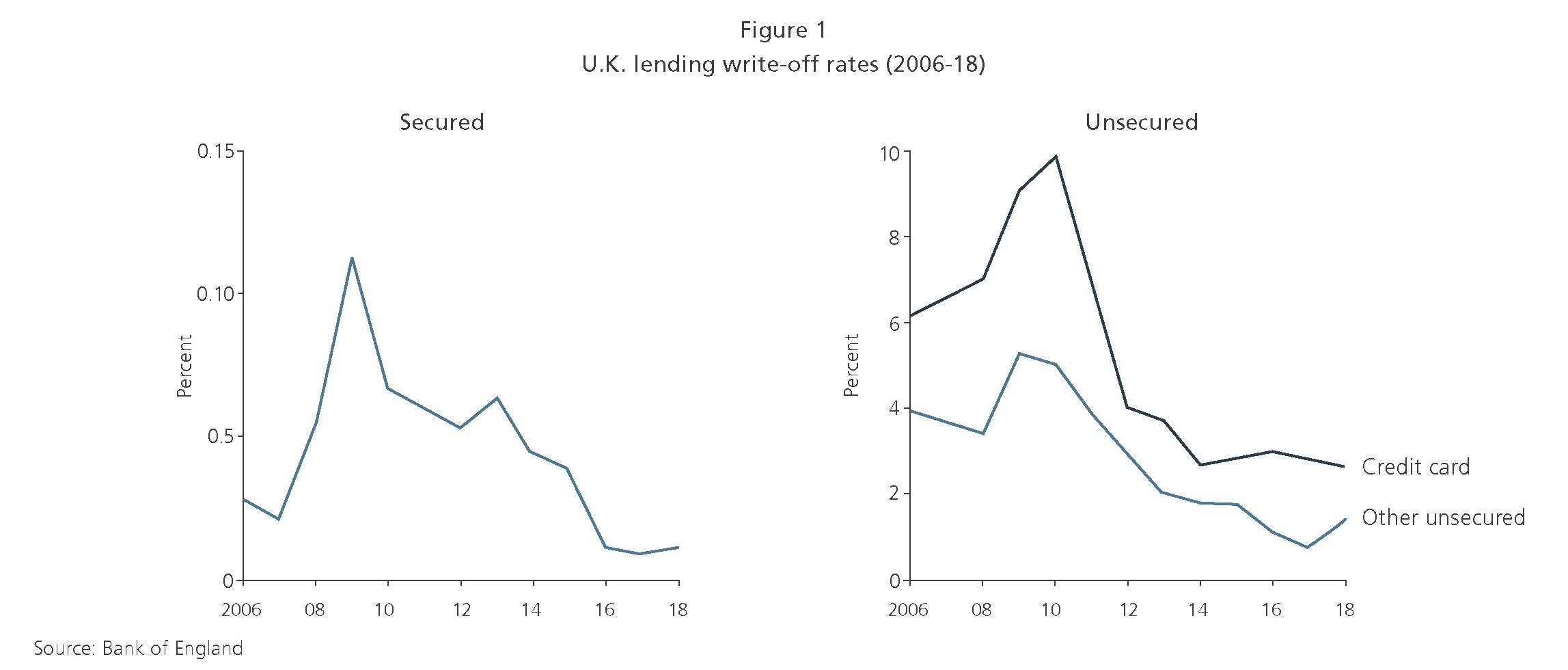

It is essential to recall that the primary cause of the retrenchment or closure of U.K. lenders in the credit crunch was withdrawal of funding, not credit losses, especially for sub-prime lending. Figure 1 shows U.K. banks’ and building societies’ write-off rates for secured lending and unsecured lending, respectively.

Although default rates and write-offs increased significantly, they did not do so transformationally — indeed, in the case of secured loans, write-off rates barely breached 0.1% even at the height of the post-crunch crisis. Further, write-off rates mostly recovered within two to three years and are now at levels significantly below pre-crisis levels.

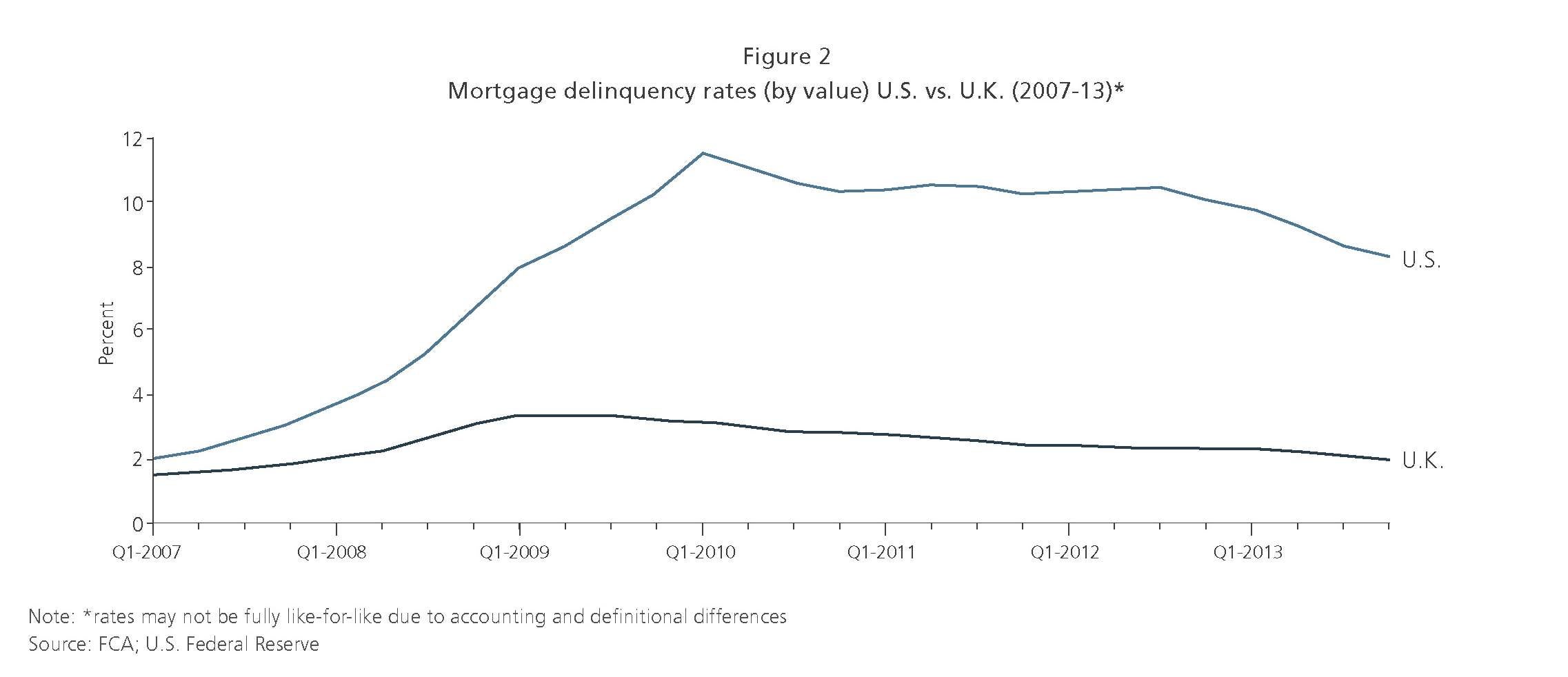

This performance was in stark contrast to the U.S. where loan delinquencies and actual credit losses were much worse, in large part because of the prevalence of sub-prime mortgages. For example, Figure 2 compares U.K. and U.S. mortgage delinquency rates for 2007-2013, i.e., from just before to a few years after the credit crunch.

Although the increases in U.K. mortgages were significant, those in the U.S. were around five times as high, and were still very high some five years after the onset of the crisis; U.S. anecdotes are not readily transferable to the U.K. Specialist lenders with enough ‘wool on their backs’ (i.e. those who had accurately assessed credit risk, had an in-depth understanding of their market, and had the right collections infrastructure and expertise in place) certainly experienced tougher conditions, but the risk was containable.

Despite this, many lenders, and especially sub-prime businesses, complained of their funding being withdrawn following the credit crunch simply because they were designated complex or sub-prime, rather than primarily due to credit performance or actual loan losses. It is evident that a lender’s funding position is as important as its credit performance.

Many specialist lenders survived through and prospered after the credit crunch

Some specialist lenders had very positive downturns. For example, consumer car finance company Moneybarn trebled the size of its book in the three years following 2009 with very low loss rates and conservative underwriting criteria. It was subsequently acquired in 2014 by Provident Financial for £120m, by which time it had become the U.K.’s largest vehicle finance group of its kind. This followed strong performance through and after the credit crunch in part due to a simple, disciplined underwriting model focusing on its strengths. Equally importantly, Moneybarn had also arranged solid term lending just prior to the onset of the crisis.

Similarly, in asset finance, Liberty Leasing and Kennet Equipment Leasing posted compound annual growth rates of 20% and 26% in the five years prior to 2011, respectively, followed by a further 30% and 18% over the subsequent five years.

Equally striking was the establishment and growth of a range of specialist banks, such as Aldermore, OneSavings Bank, Charter Court and Paragon, which emerged into the underwriting territory abandoned by the major banks following the crisis. These banks grew rapidly and profitably into sizeable institutions. Equally, more venerable institutions such as Close Brothers, with its through-the-cycle strategy which carefully balances growth vs. profitability, were also well placed and grew significantly and profitably as flightier, less disciplined firms retrenched and withdrew.

What’s different this time?

Whatever the outcome of Brexit, the nature of a forthcoming downturn is likely to be less muted than the credit crunch.

The banks are far more highly capitalised than before: for example, CET1 ratios of major banks are now nearly three times pre-crisis levels, at c.13-16%. Banks are therefore in a much stronger position to handle major economic turbulence, so emergency withdrawal, either from their own lending activities or from funding lending businesses, should be a far less serious threat to lenders. This greater resilience gives banks much more headroom to continue to support robust lenders, even in higher-risk product areas, rather than having to withdraw from entire categories.

Further, the post-recession tightening of underwriting regulation has improved lending standards, reducing credit risk for lenders. In consumer lending, the Financial Conduct Authority (FCA) has been far more proactive than its predecessors, with significant focus on product suitability and affordability, and treating customers fairly. Although the outcome of these interventions is yet to be proved out in a downturn, industry consensus is that current loan books are far more resilient than their pre-crisis equivalents.

L.E.K. Consulting believes that the most likely outcome of a downturn in the U.K. is some retrenchment of credit risk at institutions of all types, rather than radical withdrawal. However, there will be significant opportunities arising from these changes in credit risk, and some clear winners and losers.

All lenders are not born equal: How to pick the winners

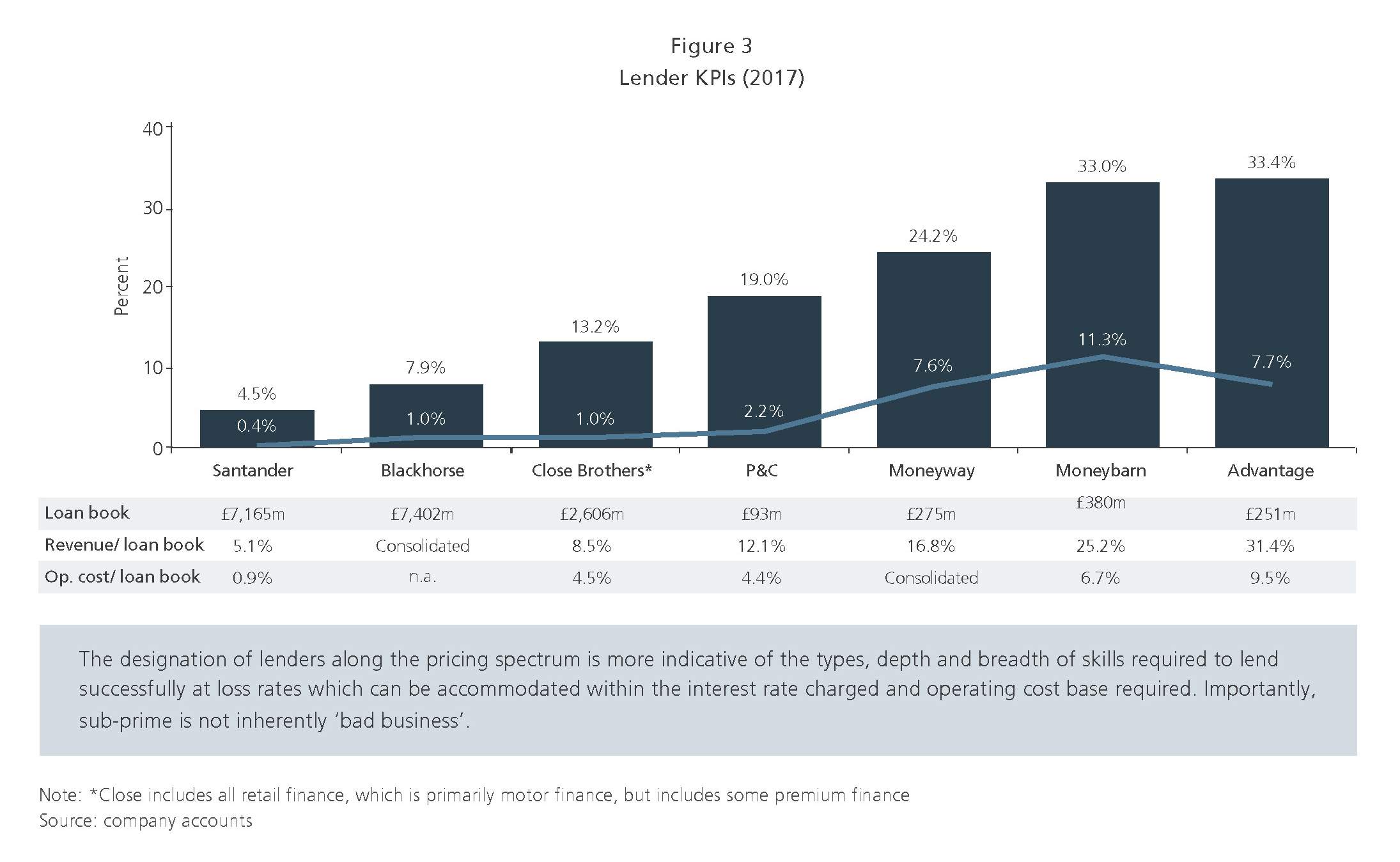

It is important to appreciate that the degree of downside risk to credit performance in each lending business varies considerably according to multiple criteria. Key technical and operational factors include loan security, interest margin (and consequently the headroom for losses), and the lender’s skill in collections of defaulted or distressed loans.

Downside risk is greatest where the combination of these factors is unbalanced, not simply where the risk of loan default is highest. For example, an experienced sub-prime lender with strong skills in underwriting and collections can contain increases in credit risk in a recession far more easily than can an ultra-efficient, low-risk but thinly resourced prime lender playing with a far lower spread on its loans.

Figure 3 below illustrates this balance in action for a range of U.K. motor finance lenders.

Also crucial is the lender’s position in the ‘pecking order’ of repayment to creditors if the customer becomes distressed — i.e., when a given customer runs into trouble and is unable to make all their loan repayments, which payments they choose to make first, and which they consider to be less important and therefore either delay or miss entirely. This may relate to formal security on the loan, but also links to:

- The quality of the lender’s relationships with its customers

- How vital the loan is to the customer (e.g., a customer may be unable to perform their job if their car is repossessed, and is very likely to prioritise mortgage payments over, for example, credit card debt)

- The customer’s desire to keep using the loan provider in the future — for example, using a particular type of debt may be essential to how they finance festive expenditure each year

Lenders who have expressly planned for a downturn are also likely to be better prepared. For example, Close Brothers recently published a 2019 annual report describing the bank’s substantial exercise in contingency planning for a recession, including creating detailed playbooks for its lending businesses.

In a downturn, continuity and robustness of funding arrangements are at least as important as these operational considerations. There are several key issues to think about in assessing the resilience of a lender’s funding position:

- Longer, committed funding facilities are more durable than both possibly cheaper, but looser and less committed/shorter-term block funding facilities, and securitisation and/or bond funding sourced from inexperienced or generalist investors who may take fright at lending in a downturn.

- Having access to multiple, experienced funding sources is a more stable position than having a smaller number of (or even single) arrangements, especially with less-experienced funders.

- Lenders with a track record of success through the previous cycle or — next best — those that have access to extensive performance data through the cycle (e.g. via broking activities such as at Charter Court) are at an advantage over peers who have only operated in or have knowledge of the benign post-downturn period (and therefore remain untested by more challenging market conditions).

- Those with serious contingency planning, and therefore more tightly contained potential losses, are also likely to be regarded more positively by funders.

Businesses that show both robust operating characteristics and strong fundability will likely thrive in any forthcoming recession, benefiting from the failures of others that do not.

Trickle-down lending economics

In addition to these core characteristics, changes in credit appetite from lower-risk, prime players may allow well-positioned lenders to pick up demand that these players no longer wish to serve. Where prime lenders retrench their appetites, previously borderline accepted customers will be rejected, leaving them addressable by the next tier; whereas these customers may feel risky to prime players, they will be higher credit quality than those typically available for mid-tier players to serve.

As such, overall average credit quality for mid-tier players may actually improve in a downturn rather than deteriorate, as they have access to better risks than would be available to them in more benign macro-economic conditions. Equally, sub-prime players will also likely benefit from contracting credit appetite in the mid-tier. This mechanism provided the underpinning for many of the successful examples referenced above.

However, not all lower-tier players will survive to benefit from this additional demand. Some will find that their underwriting models or collections processes were not as effective as they thought; others may have their funding withdrawn. But these market failures could provide still further opportunities for the stronger players that remain.

Brokers will also benefit from borrowers’ need to look beyond their previous suppliers: underlying demand for money typically remains robust during downturns, but needs more guidance to find the right provider amidst a more constrained supply environment. Those investors looking to participate in specialist lending but without balance sheet risk could therefore have an opportunity to do so via broking businesses.

A path worth travelling

There will be casualties amongst specialist lenders should another downturn strike in the U.K., but those in robust form and agile enough to take advantage of the situation will generate substantial commercial gain for themselves and their investors.

Lenders must review their business models now to ensure that they are in the best position possible to withstand a downturn, and meanwhile they must maintain underwriting discipline in the face of intense competition.

Funders and investors should conduct in-depth assessments of individual opportunities in order to understand which of the specialist lenders are likely to flourish in tougher conditions — and therefore which they should back. A high-level approach based on historical anecdotes could lead to both missed opportunities and costly errors.

01062020080145