Summary

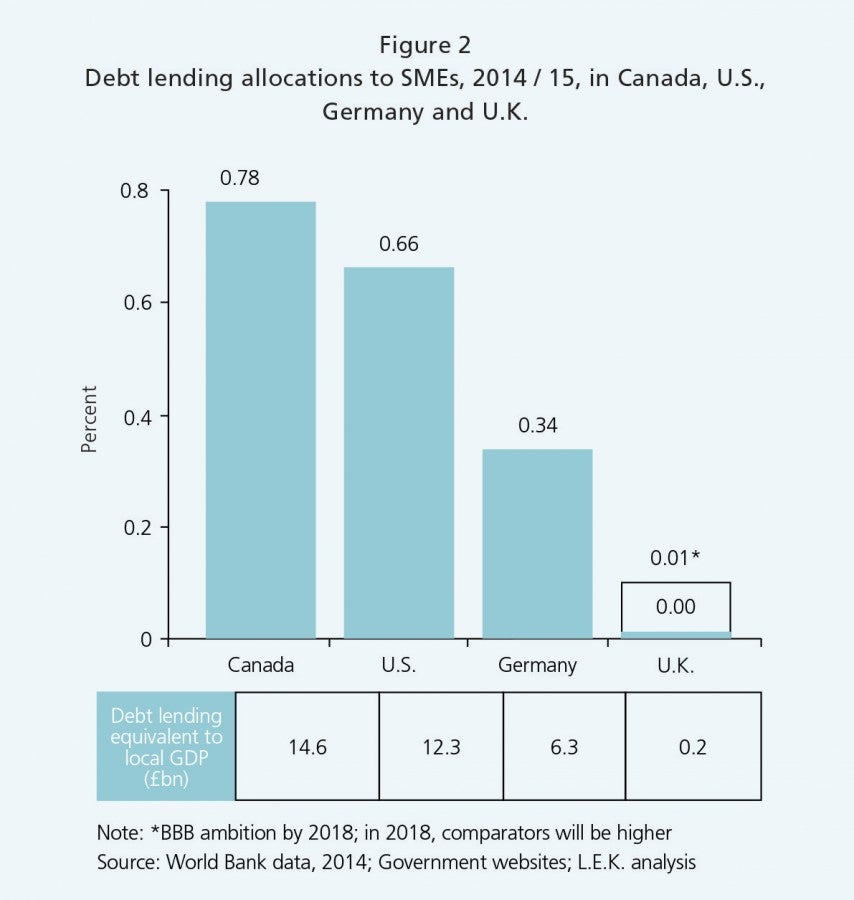

Small and medium-size enterprises (SMEs) are a critical part of the U.K. economy, representing 99.9% of private-sector companies and 60% of private sector jobs. However, there is a shortage of financing for these businesses, which is constraining their growth, restricting the U.K.’s ability to compete internationally, and may even be damaging the culture of U.K. entrepreneurialism. L.E.K. estimates the current lending gap at between £50 billion and £100 billion over the economic cycle.

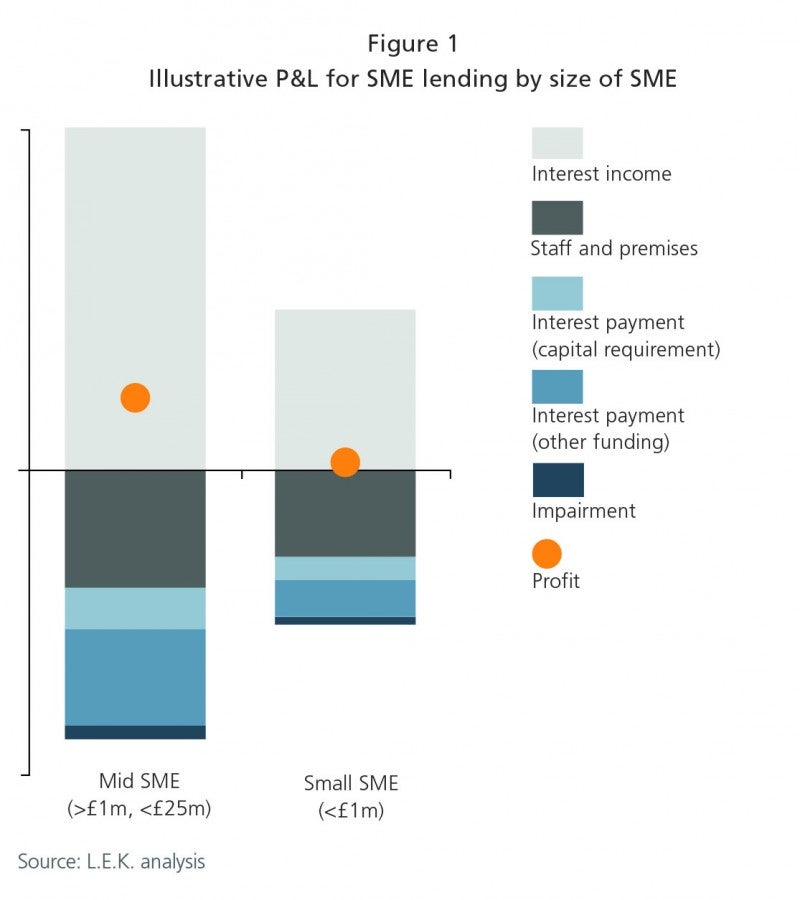

Banks’ reluctance to lend to SMEs comes down to simple economics: the potential cost outweighs the likely benefits. In other words, when considered in terms of profit and loss, the projected interest margins from lending look insufficient compared with bank operating costs, capital costs and hard-to-predict amounts of loan loss.

If SMEs are to continue to fuel the U.K. economy a different approach is needed. In this Executive Insights report, London Partners Peter Ward and Diogo Silva set out four potential solutions which, in combination, could help to reduce the lending shortfall:

- Reduce Operating Expenses

- Reduce Capital Costs

- Tackle Loan Losses

- Take a Much Wider Perspective — UK plc

The SME sector is fundamental to the growth and prosperity of the U.K. economy, and lenders have a crucial role to play in providing the finance that smaller businesses and entrepreneurs so desperately need. By adopting these four proposed solutions, banks could make an important contribution to funding growth in the U.K. SME sector.

Watch Peter Ward speak to this issue in the video below.

Sample Visuals

04302018140447