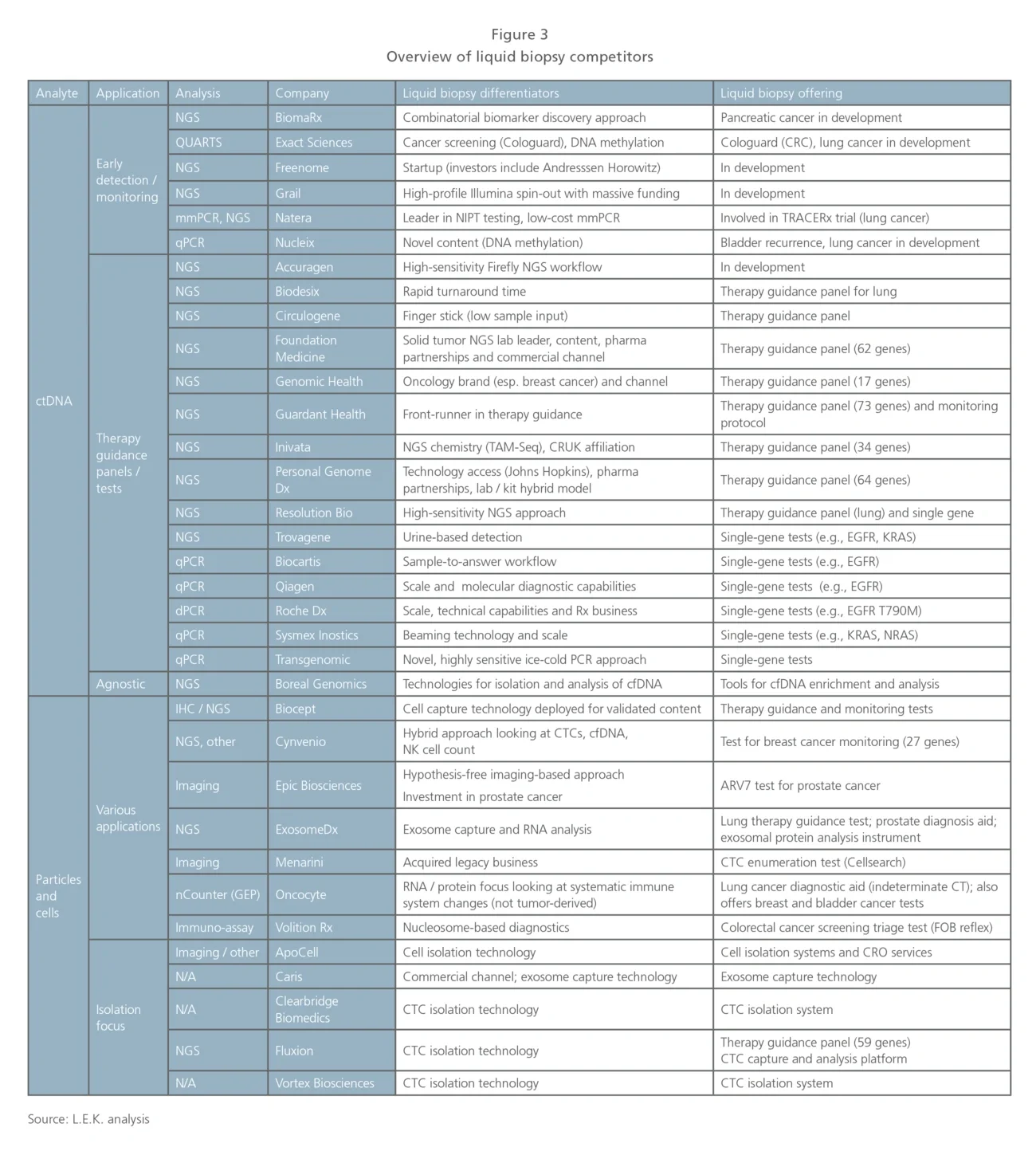

Differentiation in the nascent clinical liquid biopsy space today appears to be driven by a mix of technology (e.g., sequencing chemistry, cell capture technology and informatics) and investment in clinical trials/data to support utility. Commercial differentiation is minimal as few companies have reached the scale where this represents a meaningful differentiator. The intellectual property landscape is also dynamic and expected to support company differentiation in the future.

Looking across the competitive landscape, we define the following clusters:

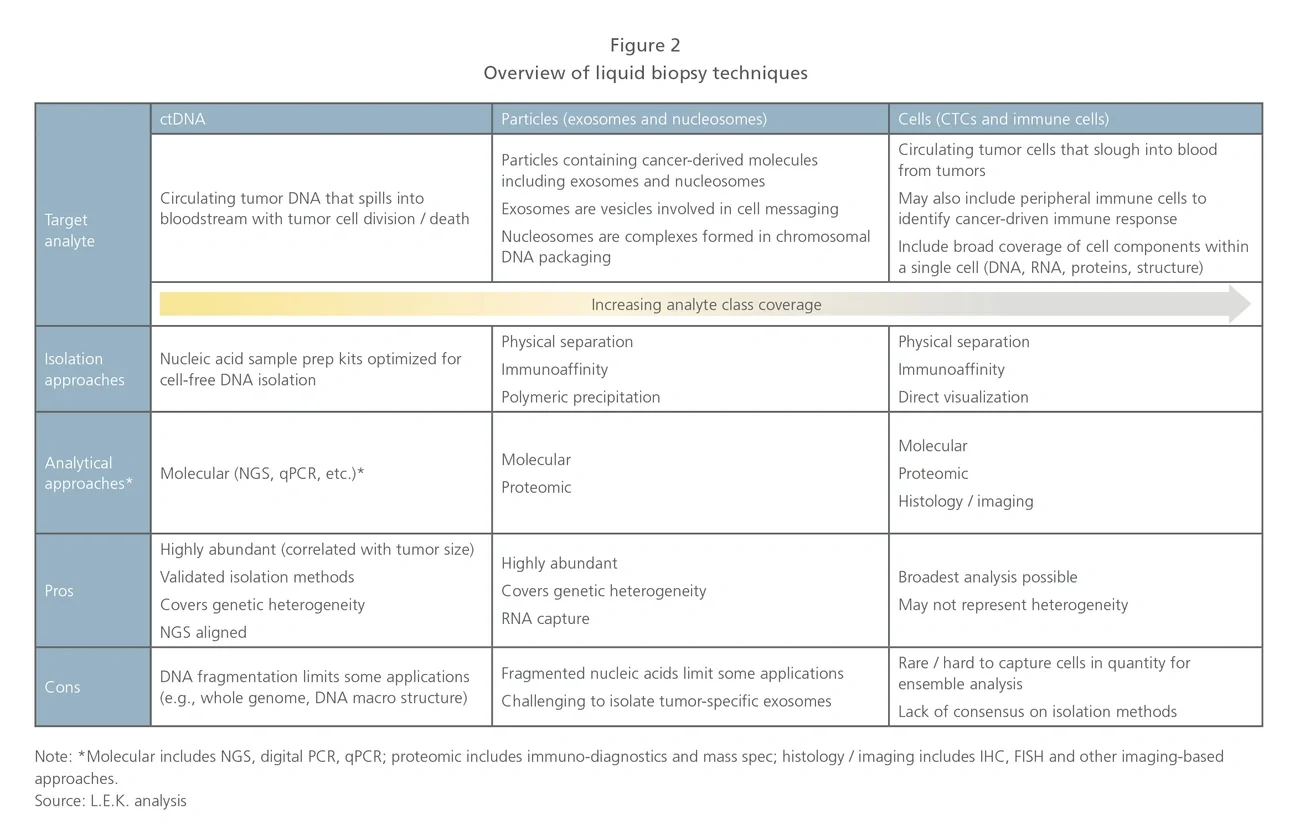

Early detection using ctDNA. Probably the most exciting segment (given its potential to impact health screening in the general population) includes various players seeking to develop offerings in early cancer detection and screening.

Competitors in this segment are expected to differentiate with clinical data to support test utility. Clinical studies for the general screening population are likely to be massive (~100K patients) in scale and require significant longitudinal analysis.

Grail is the poster child in the early detection space, having raised $1 billion in VC funding and recently embarked on a 120,000 patient study for early breast cancer detection. Many others are eyeing the early detection space, and some may ease their way into the general population applications through trials in at-risk patients, or as a reflex to other screening methods (e.g., low-dose CT, fecal occult blood).

Therapy guidance using ctDNA. This segment is the most crowded and is seeing actual clinical application today in metastatic patients. There is a core group of players deploying NGS-based liquid biopsy panels to support therapy guidance in biopsy-constrained situations. The clear front-runner here is Guardant Health, but many other competitors — several of which also play in the solid-tumor panel NGS space (e.g., Foundation Medicine, Personal Genome Dx) or have some differentiating technology enabling higher sensitivity or smaller sample input amounts — are also present.

Many traditional oncology diagnostics companies (e.g., Roche, Qiagen) have targeted single-gene tests based on PCR in the therapy guidance space, including regulated kits for companion diagnostic biomarkers such as EGFR. Players in this space are also likely to transition into monitoring applications for tested patients (looking at resistance or recurrence in treated metastatic patients).

Particles and cells (exosomes, nucleosomes, CTCs and immune cells). This is a heterogeneous segment developing varied clinical applications based on analysis of captured particles or cells. In some instances, competitors are enabling existing biomarkers to be measured from blood (e.g., Biocept, Exosome Dx) whereas others are developing novel content (e.g., Epic in prostate cancer and Cynvenio in breast cancer).

Epic is unique in that they do not enrich CTCs; rather, they image cells in a monolayer. Epic has focused efforts on prostate cancer and recently launched an ARV7 test to guide prostate cancer treatment. Cynvenio is interesting in that they are combining multiple techniques for their breast cancer recurrence monitoring test, which includes ctDNA and CTC DNA sequencing, as well as NK cell enumeration. Oncocyte is focused on blood-based immune cell function analysis. Another group of competitors in this space offers tools for CTC capture using various approaches, but is not focused on specific applications.

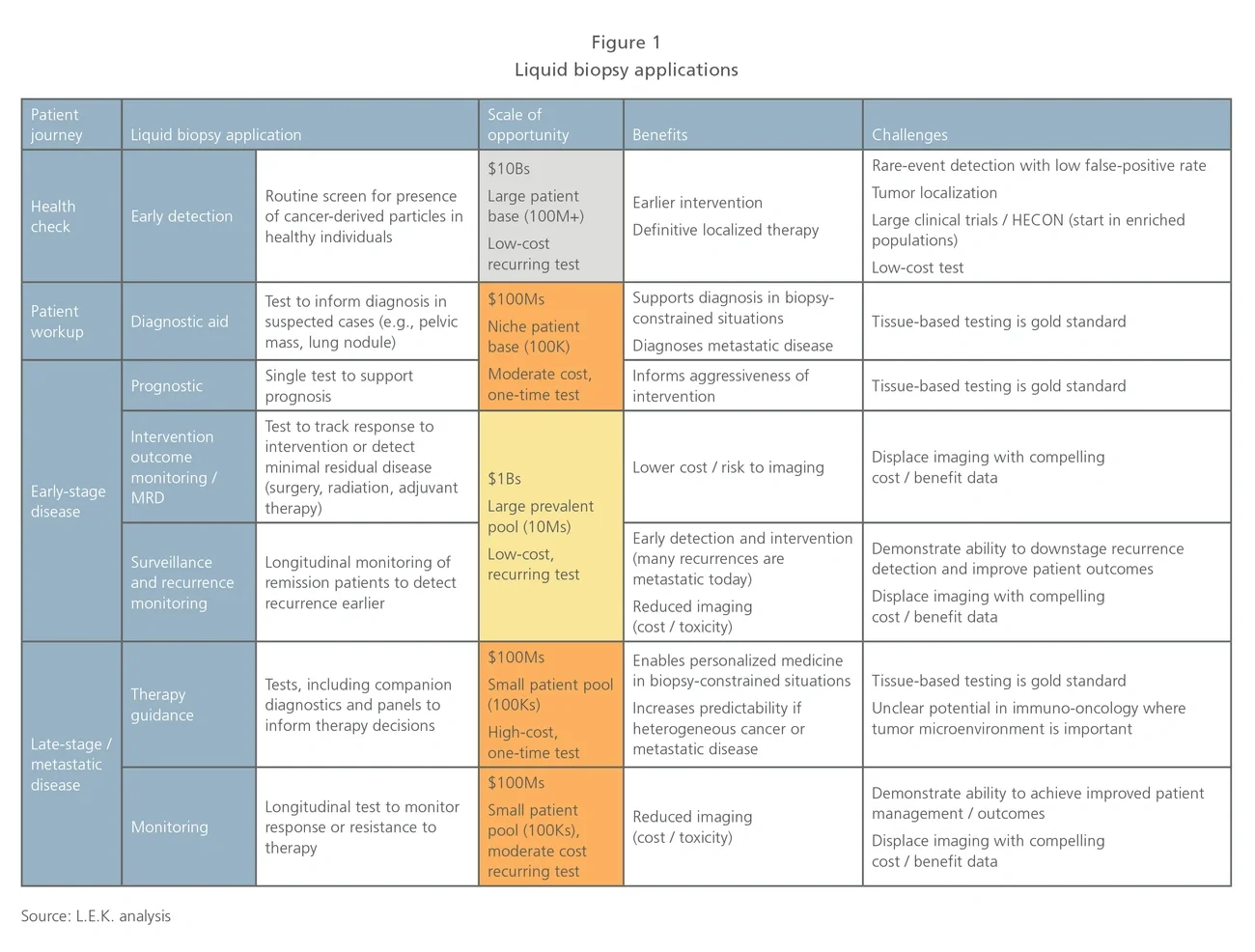

Significant opportunities lie ahead

The market opportunity associated with liquid biopsy represents one of the largest and most dynamic diagnostics/healthcare opportunities. While we are excited about the market potential and clinical utility, we urge pharma stakeholders, tools companies, diagnostic developers and other market stakeholders to carefully consider the impact liquid biopsy may have on the oncology landscape and what it will take to play and win.