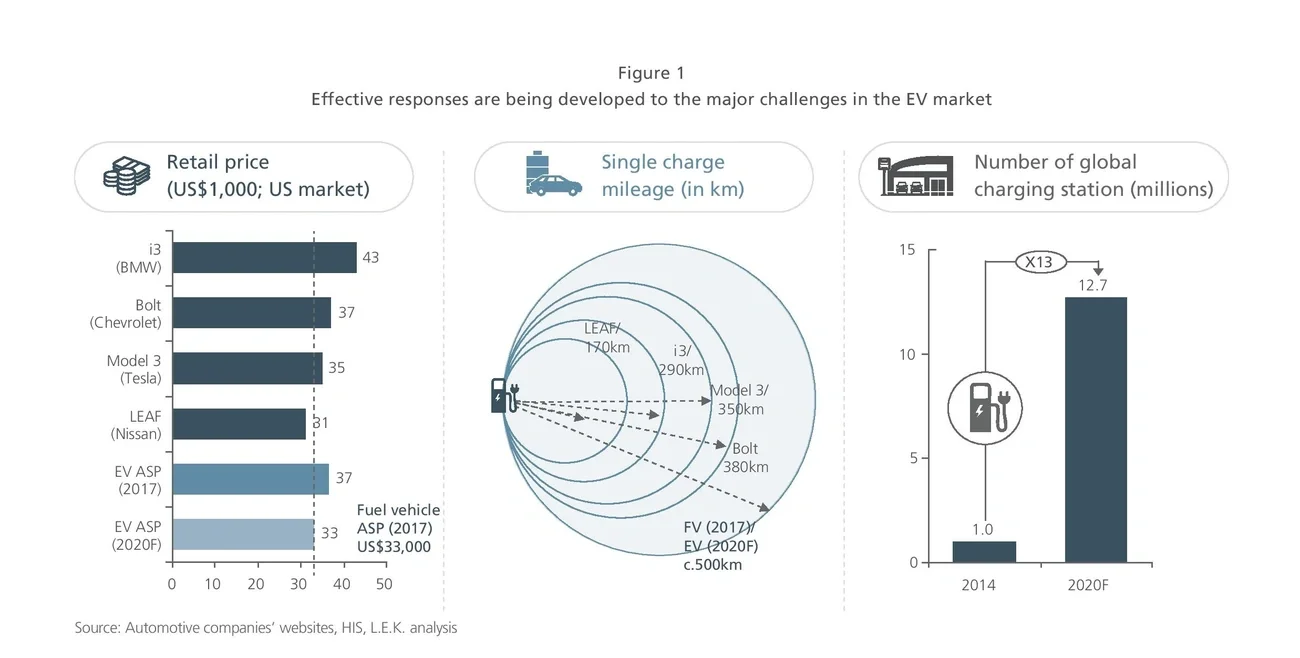

In the United States, the basic configuration of the latest Tesla Model 3 is priced at approximately $35,000, a price almost matching the median price of a traditional FV in the domestic market (about $34,000), and it has reported a battery life range of 350km. Traditional auto manufacturers are not far behind: LEAF (Nissan), Bolt (GM), i3 (BMW) and other models are also approaching traditional FVs in pricing and mileage. In China, startups like Nio and FMC (Future Mobility Corporation) are attempting to deliver durable, moderately priced EVs — and are positioned to serve an addressable market of upwards of a million users. Simultaneously, Chinese local authorities have also put forth an increasing number of policies supporting the construction of charging stations. This, in addition to high levels of domestic EV manufacturing activity, is making China one of the most developed and connected markets for EV technology. Commitment to building charging station infrastructure has also significantly reduced range and mileage anxieties among existing and prospective EV owners — lowering the barriers to EV ownership.

Governments are looking for balanced and holistic approaches to regulating EV development. On one hand, governments have strong interests in supporting the development of EVs. On the other hand, there is also some concern that excessive EV industry growth could present new sets of policy issues. For example, in the United States, status quo legal frameworks neither adequately address nor appropriately regulate driverless cars — the majority of which are electric. Specifically, issues of liability in the event of an accident involving a driverless car are not defined within the current regulatory structure. Congress is actively working to develop laws and regulations to ensure that by the time driverless cars are mass-marketed, appropriate regulations are in place.

From an adoption perspective, EV sales are expected to increase as soon as EV manufacturers expand capacity and add production lines. Although EVs will not entirely replace traditional FVs in the near term, there is an industry consensus that increased EV penetration is an inevitability. In the midterm to long term, EVs can expect to gain significant — and eventually majority — market share. The next decade will be one of momentous change for the automotive industry, and in order to respond strategically to market movements, it’s imperative for relevant stakeholders to have a deep knowledge of market trends.

This Executive Insights reviews three disruptive trends in the automotive industry precipitated by the rapid growth in the EV industry and offers preliminary suggestions on how best to respond and adapt to those trends.

Competitive emphasis on cost-effective hardware and value-added servicing

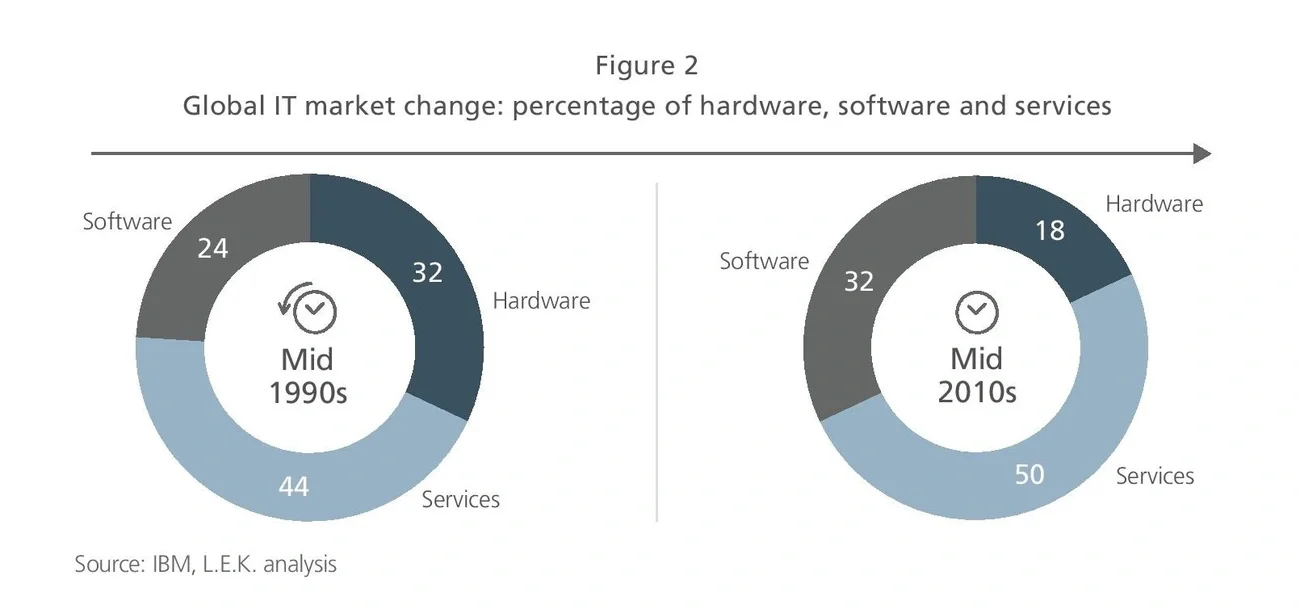

Evolution in the EV competitive landscape is expected to parallel evolution previously observed in the IT industry: Competitive foci will gradually shift away from the pursuit of breakthrough technologies and toward the development of cost-effective hardware and value-added services. The IT industry can be taken as a case study, with the past two decades in particular serving as an example of shifting modes of competitive positioning.

Since the 1990s, the core dimension along which IT enterprises have been competing has shifted away from hardware performance and toward provision of value-added and customized services. Take the PC, for example. Given the high levels of compatibility between PC parts (hard drives, memory, etc.) and narrow PC hardware margins, many PC manufacturers (Dell, Lenovo, etc.) have chosen to outsource to original equipment manufacturers (OEMs). Value-added services have become the primary margin driver in the consumer electronics industry. For example, since the 1990s, IT giant IBM has spun off lower-margin and less-competitive hardware holdings, moving further and further into services and software. Apple has long recognized that it’s able to exert comparatively more pricing power in the software business, and as a result it has been able to maintain a market-leading position in the digital world.

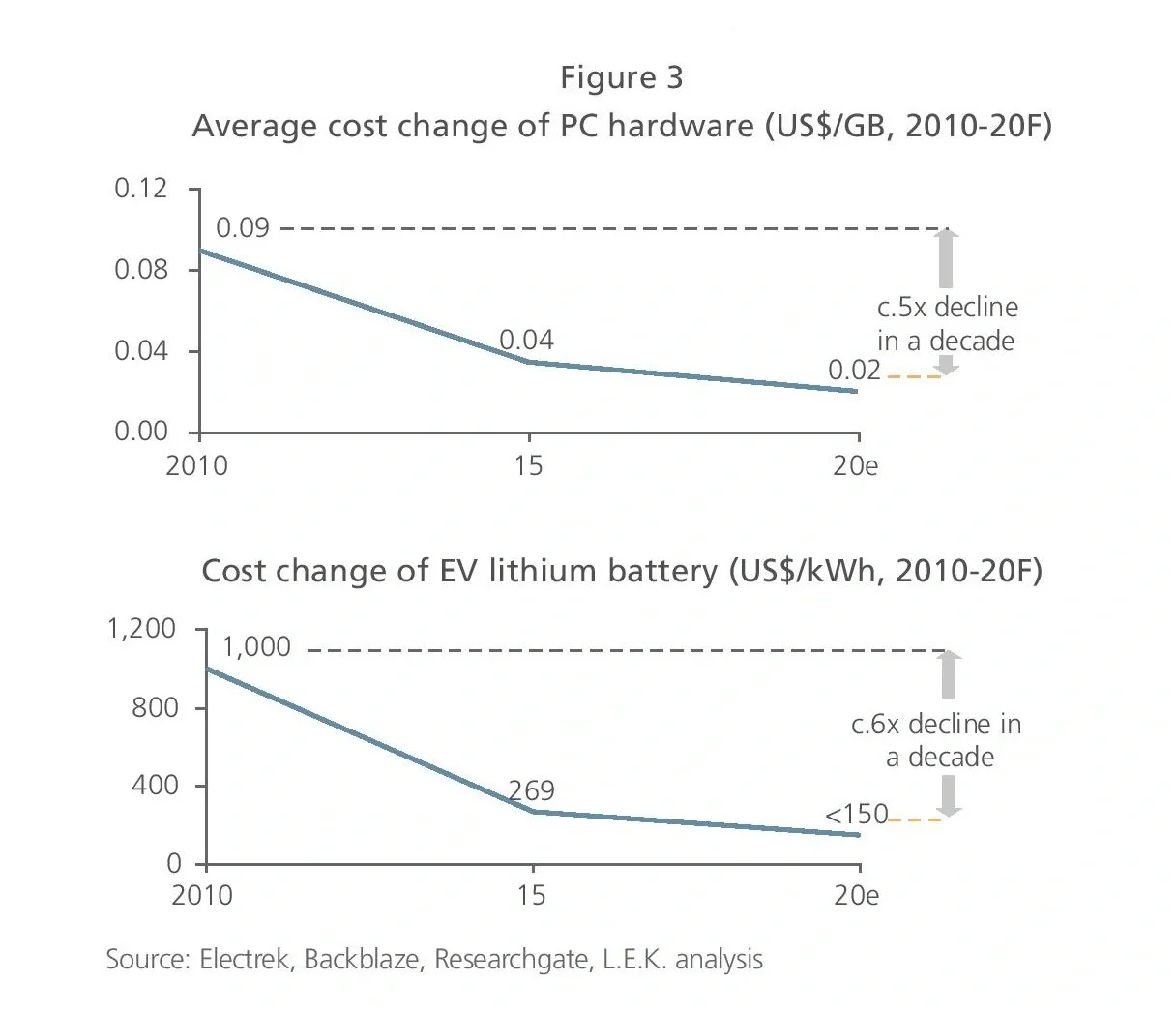

We believe that the IT industry (especially consumer electronics products such as PCs and mobile phones) serves as an important reference point for EVs and can be used to predict the competitive trajectory of and cost dynamics within the EV space (see Figure 2). For example, we expect to see similar cost decreases over time in EV main systems as we have seen historically in PC hard drives. The main system of electric cars (i.e., motors, electronic controls and batteries) is more standardized, modular and cost-effective than those of traditional FVs (engines, gearboxes, etc.), and EV main system costs are expected to decline markedly going forward. Even if the tech iterations and cost reductions in PC hardware under Moore’s Law are much faster than those in EV batteries, both are expected to follow similar directional manufacturing cost trends through the 2020 forecast period (see Figure 3).