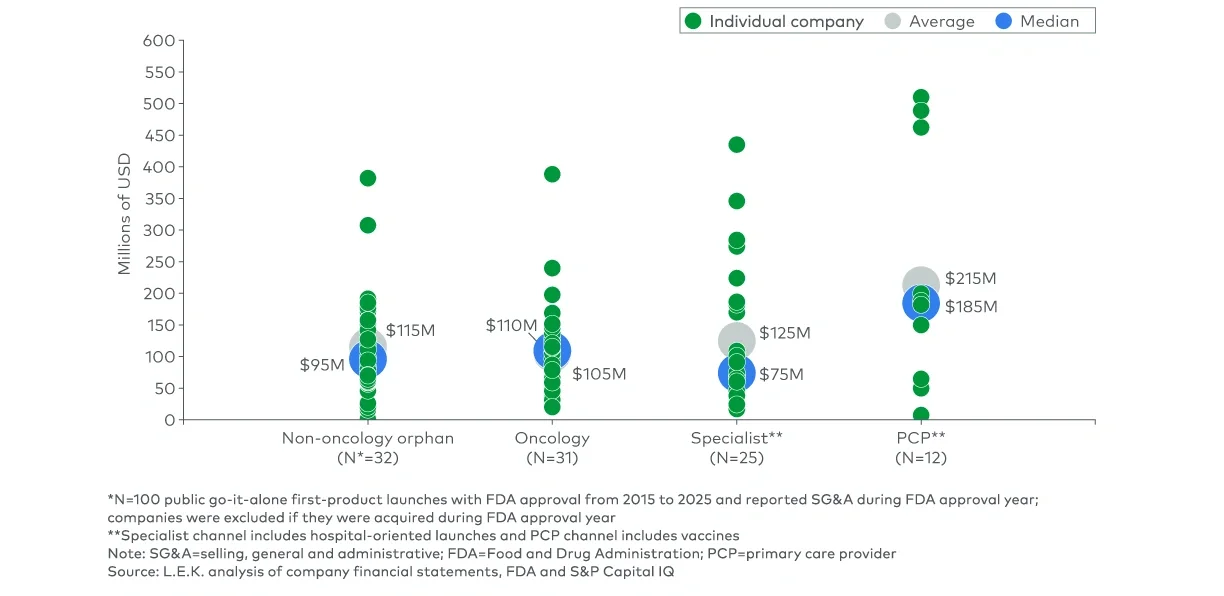

Revenue-lifting applications

There are several key AI applications supported by a growing ecosystem of specialist vendors that help biotechs commercialize more effectively and therefore increase revenue realized.

Commercial

- Patient and prescriber identification: In specialty markets, the highest-value healthcare professionals (HCPs) are typically those with the greatest concentration of clinically eligible patients, not the highest historical prescribers. AI combines claims, electronic health record, lab, biomarker and referral data to surface that signal and translate it into dynamic targeting and best-next-action prioritization. Because the capability sits on vendor platforms, it can be turned on close to launch and scaled with the field force.

- Patient access and adherence: Prior authorization (PA) friction and benefit verification delays often absorb a meaningful share of realized demand at launch, and early abandonment or adherence drop-off can erode revenue over the months that follow. AI is automating PA, benefit verification and hub operations on the access side and tailoring patient outreach by risk profile and behavior on the adherence side. Because these capabilities are vendor-mediated and the operating model is embedded in the platform, hub operations can scale with patient volume rather than be staffed ahead of it.

- Field-force copilots: Field-force copilots can make each rep more productive by improving call planning, tailoring content to individual HCPs and automating precall and postcall workflows. That can help the same field team reach more of the right prescribers without adding head count at the same rate. Over time, these tools may also shorten onboarding and time to productivity, giving companies more flexibility regarding when to hire and how quickly to scale. Because the field force is often one of the largest fixed-cost commitments in a launch, even modest gains in productivity and timing can matter.

Medical: Priming the market

Medical affairs does not generate revenue, and we are not suggesting otherwise. But it does prepare the conditions under which commercial operates, and AI is providing meaningful leverage in key use cases.

- Real-world evidence generation: Payers often require more evidence than is available at approval, and delays in generating that evidence can slow access and uptake. AI can help teams move faster by supporting cohort development, literature surveillance and clinical study report drafting. For a first-time launcher, that can reduce the need to build a large epidemiology or health economics and outcomes research team before launch while still helping the company prepare the evidence needed for payer conversations.

- MSL field engagement: AI can help medical teams train and support medical science liaisons (MSLs) with fewer internal resources. Before deployment, MSLs can use AI-based simulations to practice scientific exchanges and prepare for common HCP questions. In the field, AI tools can help them quickly find relevant literature and tailor follow-up. Shorter ramp times may allow companies to hire MSLs closer to launch while still giving a smaller medical team the support needed to engage a broader group of key opinion leaders.

Cost-avoidance applications

We do not want companies to assume AI will dramatically lower their overall cost base. However, there are still meaningful savings opportunities in functions where the underlying work is high volume and repeatable enough for automation to take on a significant share of it, such as:

- Commercial support functions: AI can now absorb a meaningful share of work across marketing content production, sales operations, data analytics and campaign execution. Historically, companies have scaled these functions by adding internal head count or relying more heavily on agencies as launch activity increases. AI can help companies keep those teams leaner and add support as the launch trajectory becomes clearer rather than committing the full cost base up front.

- Scientific communications and medical information: Scientific communications and medical information (MI) have historically required growing teams of medical writers, MI staff and external consultants as launch activity builds. AI can now take on more of the drafting, content assembly, literature review and response preparation behind publication plans, congress materials, slide libraries and MI inquiries. That allows first-time launchers to support more activity without adding full-time equivalents at the same pace.

- Enabling functions: Horizontal enterprise AI is increasingly supporting contract drafting, compliance Q&A, regulatory documentation, information technology triage and financial consolidation. For first-time launchers, where enabling functions are typically the most underresourced part of the organization, this lets teams operate effectively without the back-office infrastructure larger companies depend on.

Strategic implications for emerging biotechs

If AI improves launch economics, the implications extend well beyond operational efficiency. It could fundamentally change how emerging biotechs think about commercialization, partnerships and capital allocation.

First, a broader set of assets may support independent commercialization. By reducing infrastructure requirements, making capabilities more scalable and improving revenue capture, AI can expand the range of products that justify a stand-alone launch. In larger markets, AI-enabled targeting and field-force copilots may allow smaller teams to reach broader prescriber populations. In orphan and oncology markets, AI-driven patient identification and evidence generation may improve patient finding, access and uptake. As a result, assets that once required a partner may increasingly support independent commercialization.

Second, AI may strengthen a biotech’s position in partnership discussions. Even if a company ultimately chooses to partner, a credible AI-enabled launch alternative can improve negotiating leverage, preserve strategic flexibility and expand the range of deal structures available.

Third, improved launch efficiency can free capital for indication expansion, pipeline advancement and business development. For many emerging companies, that flexibility may reduce dependence on dilutive financing and accelerate the path to becoming a multiproduct organization.

What biotech executives should do now

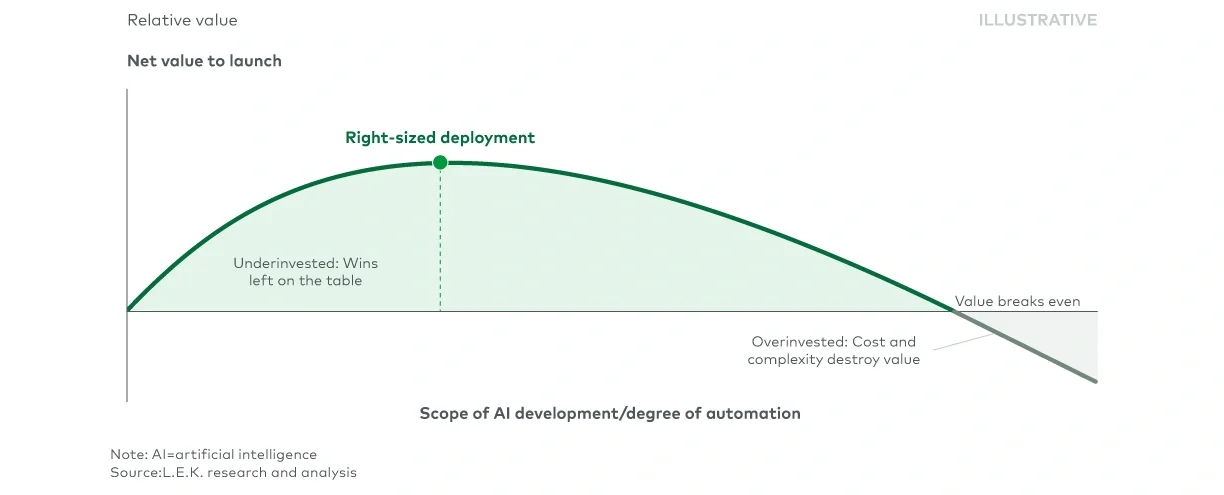

The key question is not whether to adopt AI but where it can most materially change the economics of a launch.

Executives should begin by identifying the commercial bottlenecks that matter most for their launch — patient finding, payer evidence generation, field-force productivity, content creation, patient services or other areas where AI could improve revenue, reduce cost or lower execution risk. AI should then be incorporated into launch planning early enough to influence organizational design, investment timing and partnership strategy rather than being layered onto an existing commercial model.

At the same time, leaders should remain disciplined. AI investments carry costs in technology, data, governance and oversight, and returns are unlikely to be linear. The greatest value will come from a small number of high-impact use cases rather than broad automation programs. Strong governance, clear accountability and appropriate human oversight should be built into every deployment from the outset.

The biotechs that benefit most from AI will not be those that deploy the most tools. They will be the ones that use AI to make better commercialization decisions — retaining rights where economics support it, partnering where external capabilities add value and building leaner, more scalable launch organizations.

The authors would like to thank Izzy Wilson for her contributions to this article.

AI was used in the drafting of this article.

Endnotes

¹L.E.K. analysis of company financial statements, FDA and S&P Capital IQ

²L.E.K. analysis of company financial statements, FDA and S&P Capital IQ

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC