This is the second in a series of articles that analyze why the packaging distribution industry is an attractive choice for M&A exploration.

As buyers approach potential acquisition moves in the packaging distribution industry, there are three key value creation levers to consider as factors in the decision: upstream value chain extension, equipment offering expansion and product mix diversification. Each can be enabled by M&A geographic footprint infill.

Upstream value chain extension

Potential buyers can focus their acquisition strategy on expanding their upstream value chain services to strengthen customer stickiness and realize margin uplift. This has been a theme especially in market segments where we see high-value packaging, such as beauty and high-end spirits.

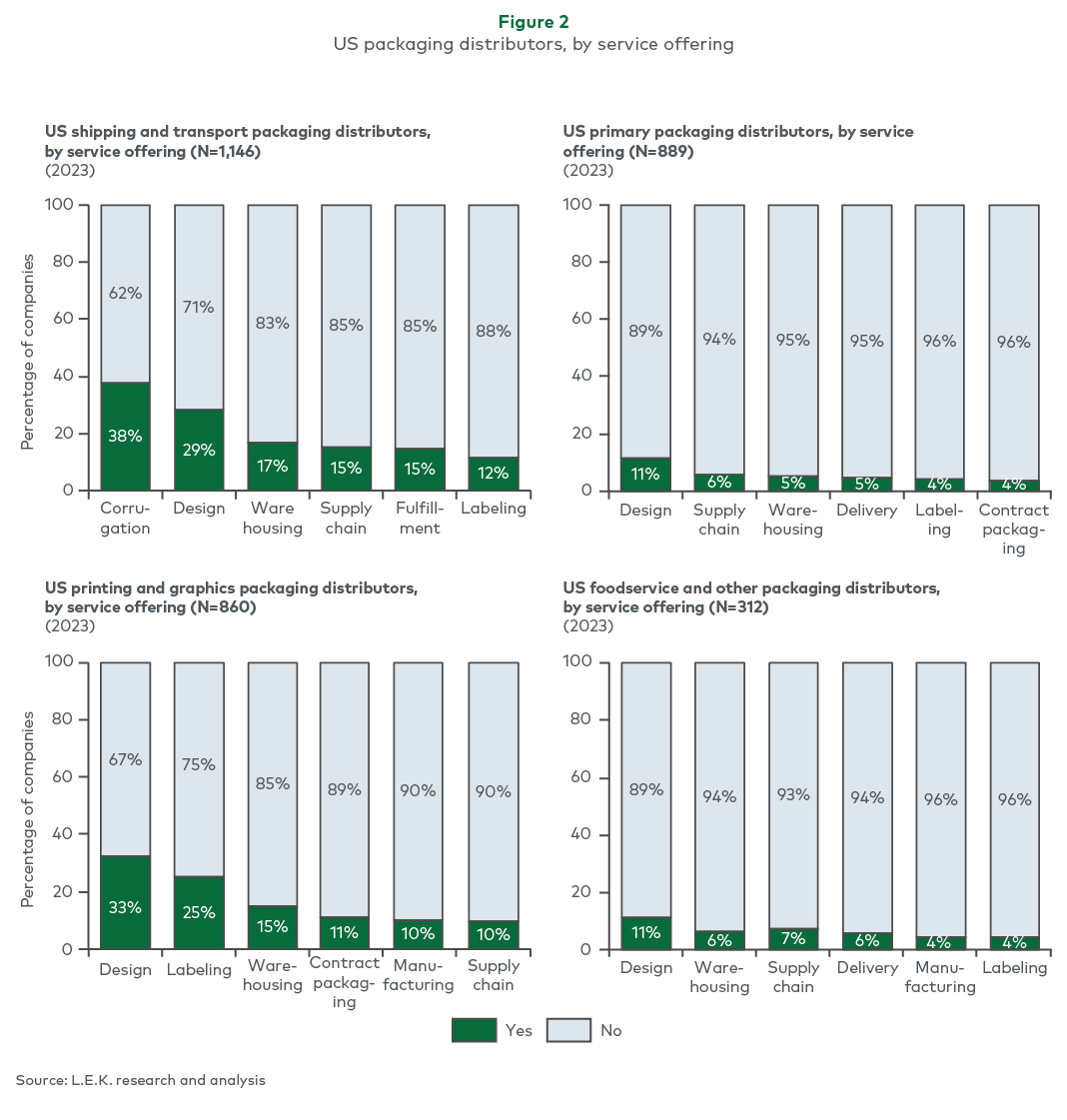

Examples of add-on, upstream capabilities include design, engineering, materials science and contract packaging capabilities. About 25% of the estimated 3,200 U.S. packaging distributors offer design services, and around 10% offer engineering and/or contract manufacturing services (each of which is usually accretive to typical distribution margins); this indicates an ongoing opportunity to acquire specific upstream capabilities.

Equipment offering expansion

Another area of potential value is equipment offerings, which can drive long-term consumable sales and support aftermarket parts and service offerings. Distributors that offer equipment are typically above $5 million in annual revenue. This indicates a need for higher levels of investment than what is required to distribute packaging products and indicates moderately more consolidation than other segments in packaging distribution.

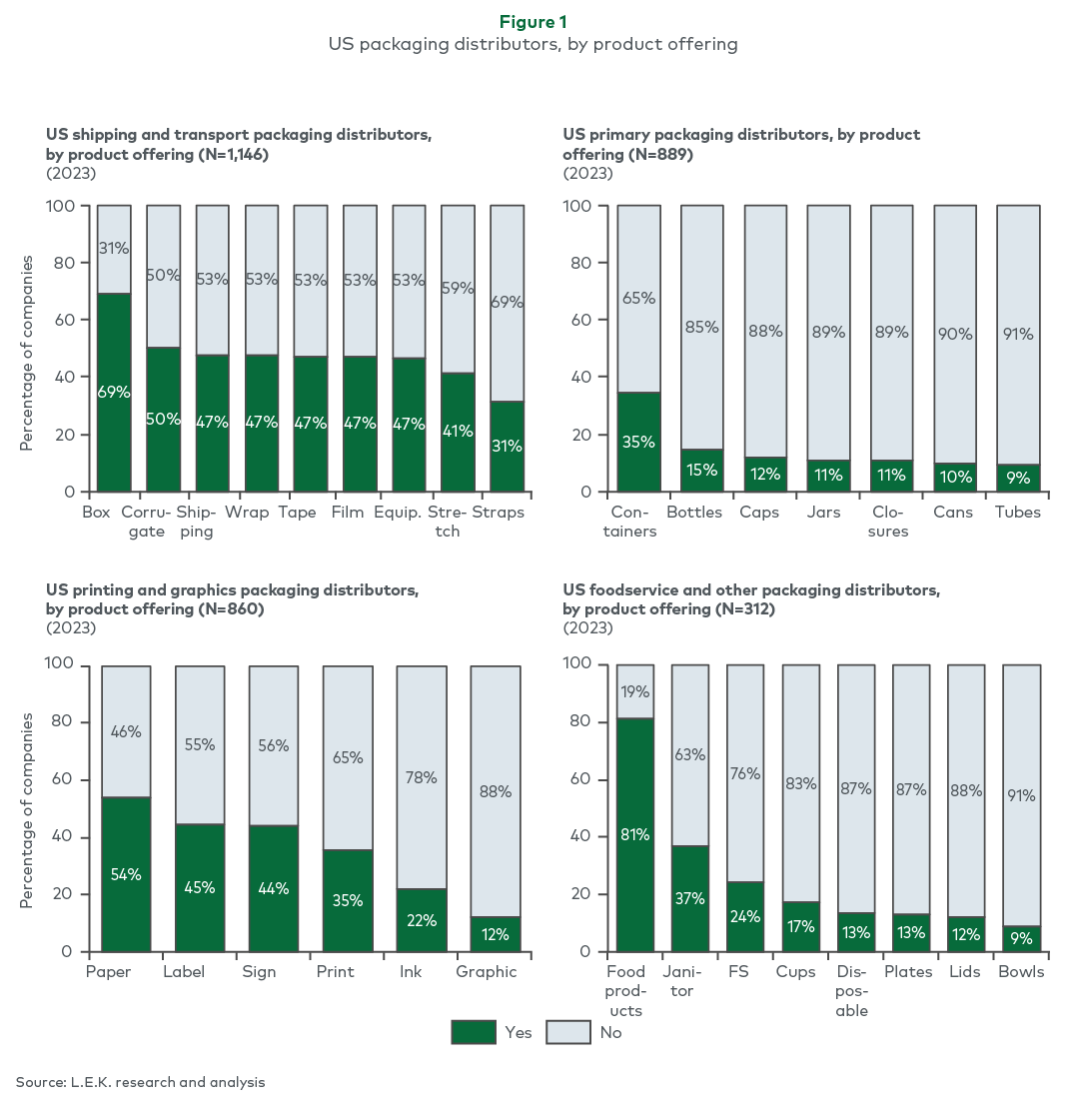

An estimated 47% of about 1,150 shipping and transport packaging distributors (one of four major archetypes in distribution, see Figure 1) offer equipment as a product, implying runway for equipment product and aftermarket service-offering expansion. By offering equipment, distributors have an opportunity to grow share of wallet with current customers; generate stable, recurring revenue via consumable sales; and expand their customer bases, providing future product cross-sell opportunities. Critical to success in serving the equipment aftermarket is having a network of maintenance engineers trained on original equipment manufacturer (OEM)-branded equipment, who can perform aftermarket services that may otherwise have been handled in-house by the OEM operator or the equipment OEM.

Further differentiation of potential acquisition targets can be made by identifying companies with equipment offerings that are generally well suited for aftermarket service expansion. About 47% of roughly 3,200 U.S. packaging distributors currently offer some form of services, indicating an opportunity to grow share of wallet with existing customers by acquiring or building service capabilities.

Product mix diversification

Packaging distributors could also add incremental products to capture a greater share of wallet within existing customer relationships. Potential buyers can accelerate revenue growth by identifying attractive, high-margin products and targeting the companies that offer these products. Product breadth across distributor archetypes varies, which may help narrow down viable options. Shipping and transport companies offer more of a consistent product mix, whereas primary packaging and foodservice and other distributors provide a more variable product set.

An illustrative example of this approach is janitorial and sanitary supplies, or JanSan, which has seen an increased focus stemming from the COVID-19 pandemic, along with the personal protective equipment (PPE) segment. Proving that offering noncore packaging products like this can be successful, 35%-40% of foodservice and other packaging distributors now carry JanSan and PPE products.

Adding to the product mix may also capture greater share of wallet outside core packaging markets while still benefiting from end-market and distribution synergies. This in turn increases customer stickiness, expands the types of customers and key stakeholders a company can work with, and accelerates growth.

M&A geographic footprint infill

As discussed in the first article of this series, the fragmented nature of the packaging distribution landscape is attractive and presents numerous opportunities to drive value. As consolidators look to add incremental capabilities and expand their offerings, local market-focused tuck-ins present a compelling M&A opportunity. This geographic footprint infill-focused strategy, which is largely enabled by market fragmentation, leverages scale benefits to drive both top- and bottom-line benefits.

From a top-line perspective, acquiring incremental products presents additional cross-sell opportunities to the sales force, and upstream value-add solutions can enhance a distributor’s value proposition and increase win rates. From a bottom-line perspective, M&A geographic footprint infill reduces logistics costs through network efficiencies and can present select opportunities to eliminate back-office redundancy, further driving margin improvement.

Up next in Article 3: A look at how bolstering digital offerings following a customer acquisition can secure quick wins and strengthen customer stickiness.

L.E.K. has developed a proprietary tool that helps quickly identify a long list of potential acquisition targets based on a thorough selection of metrics, including specific products and industries.

Please contact us at industrials@lek.com for more information.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting LLC

01192024100102