Annual Packaging Study: What Happened to SKU Proliferation?

Part 3 of a four-part article series on the 2023 L.E.K. Packaging Brand Owner Study

Part 3 of a four-part article series on the 2023 L.E.K. Packaging Brand Owner Study

Many brand owners, who in a bid to increase margins and limit innovation costs had already begun reducing the number of stock-keeping units (SKUs) in their portfolios in 2019 shortly before COVID-19 hit, plan to continue with their SKU rationalization through at least 2024. However, some brand owners have continued to maintain a commitment to new product innovation and say they’ll continue to launch new branded product SKUs over the next year, citing product innovation and the introduction of sustainable packaging.

That’s according to L.E.K. Consulting’s sixth annual proprietary packaging study, which we conducted in the fourth quarter of 2023 and which makes clear how players in the packaging value chain can differentiate their offerings in order to best meet the needs of brand owners and, by extension, their investors.

Whereas historically, brand owners emphasized broadening the range of SKUs they offered in order to attract new customers or react to new consumer behavior and trends, most — including some of the largest and most recognizable consumer brands, such as Unilever, Coca-Cola and Tyson, among others — have shifted their SKU portfolio strategies in recent years to focus on their most profitable products in order to boost margins and cap innovation costs. Indeed, COVID-19 and the supply chain disruptions it created only accelerated those brands’ SKU rationalization strategies as they focused on long-run “core” SKUs to meet market demand.

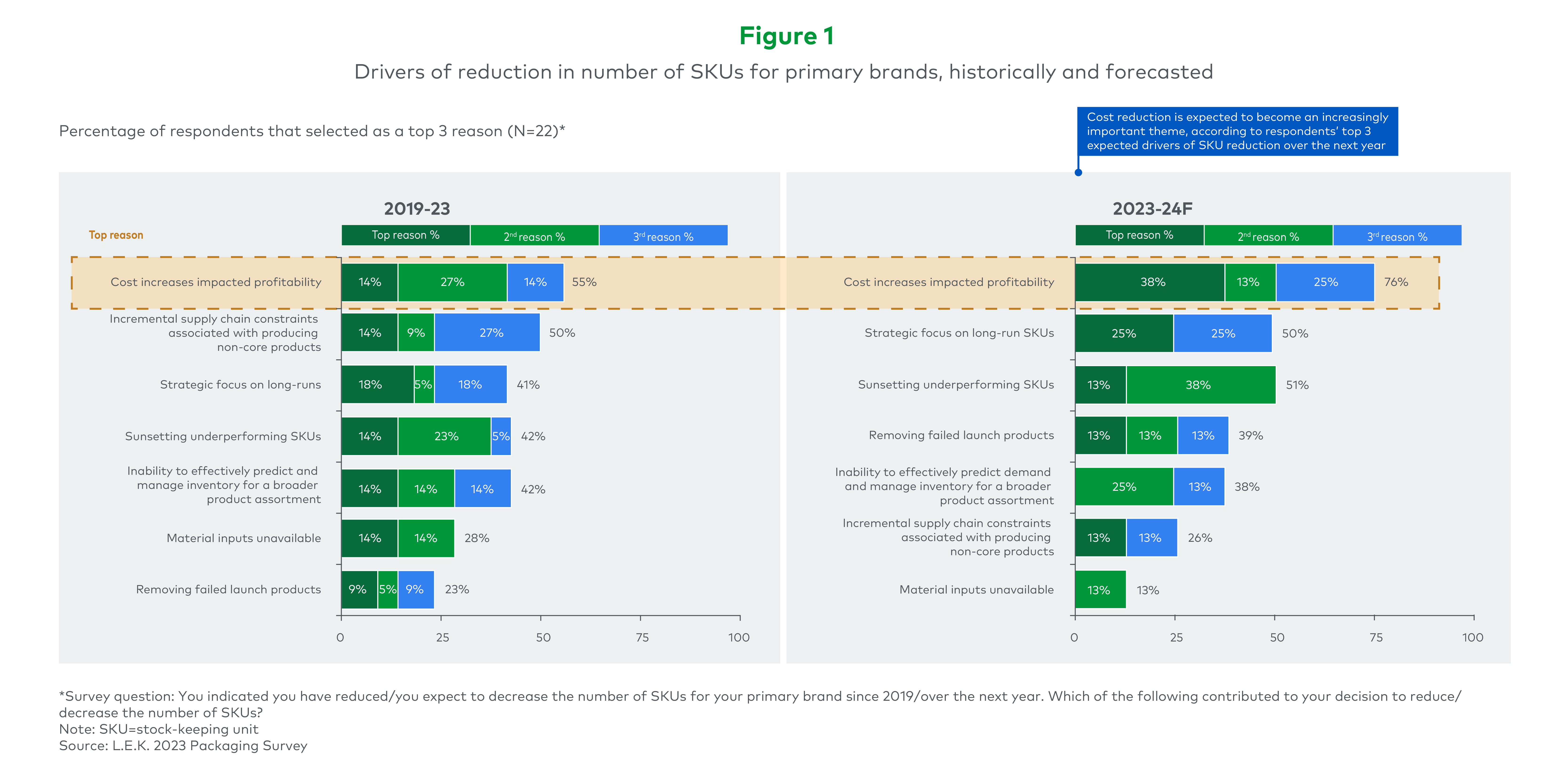

Going forward, cost mitigation associated with new SKUs and a strategic focus on core SKUs are expected to become increasingly important themes. In fact, heading into 2024, even more brand owners say minimizing the impact of cost increases on profitability is the top reason they will reduce their number of SKUs (see Figure 1).

To be sure, the SKU rationalization strategy is working, according to the respondent sample in our study. The decrease in SKUs has contributed an estimated 65-90 basis points (bps) to brands’ gross margins relative to 2019, and over the next year, continued SKU rationalization is expected to result in accelerated profitability improvement, adding another estimated 150-175 bps.

+65-90 bps

Decrease in SKU's: Estimated Brands' Gross Margin Increase

+150-175 bps

Estimated SKU Rationalization Profitability Improvement

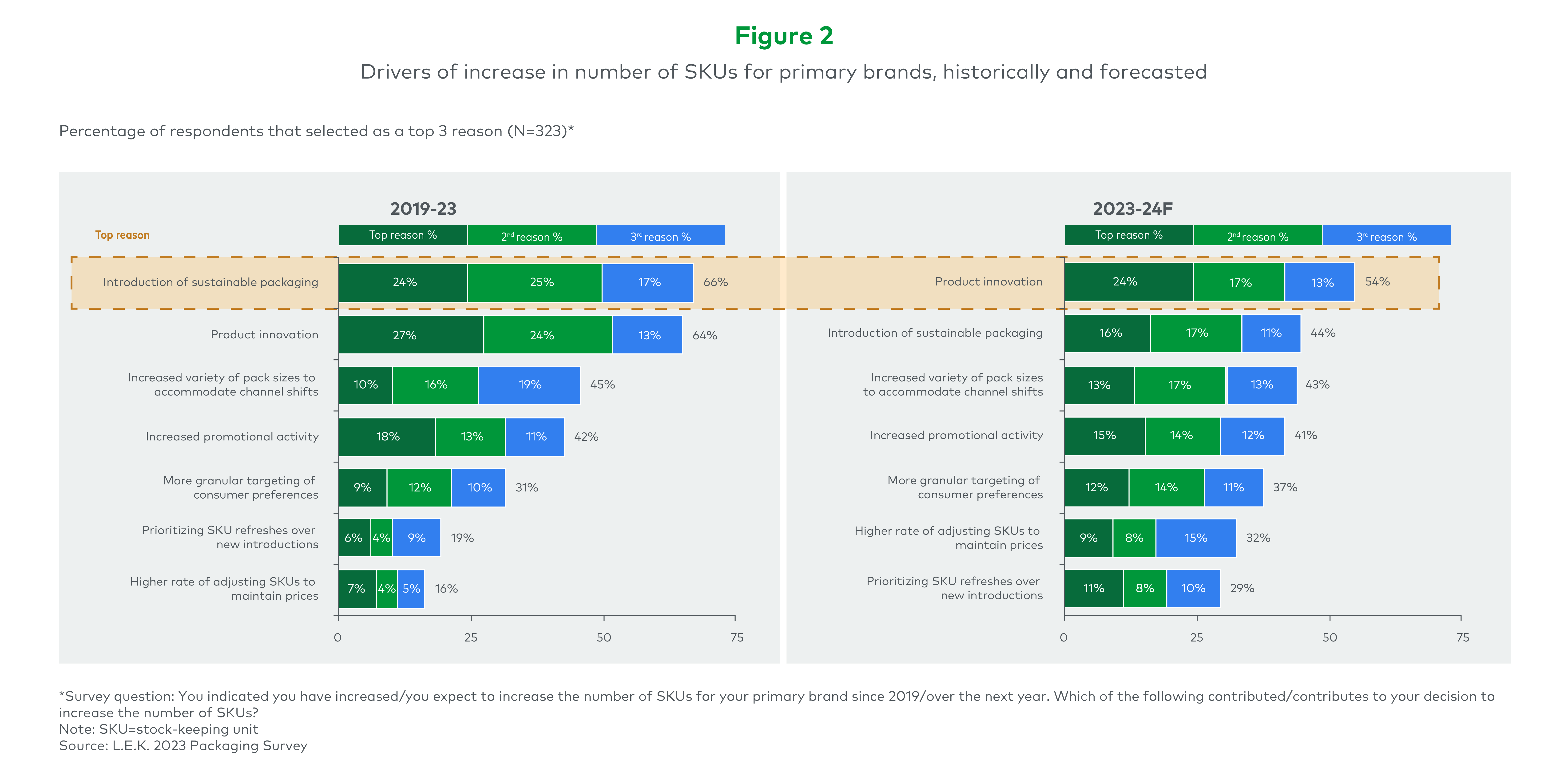

But not every brand is decreasing SKUs — some are adding more.

Brand owners that have increased SKU count offerings since 2019 cite the introduction of sustainable packaging, product innovation and an increase in the variety of pack sizes to accommodate channel shifts as the top three drivers. And while their relative rankings have shifted slightly for 2023-24 — product innovation now takes the top spot, while the introduction of sustainable packaging has moved to No. 2 — the top drivers cited by brand owners remain the same as they were for the past four years (see Figure 2).

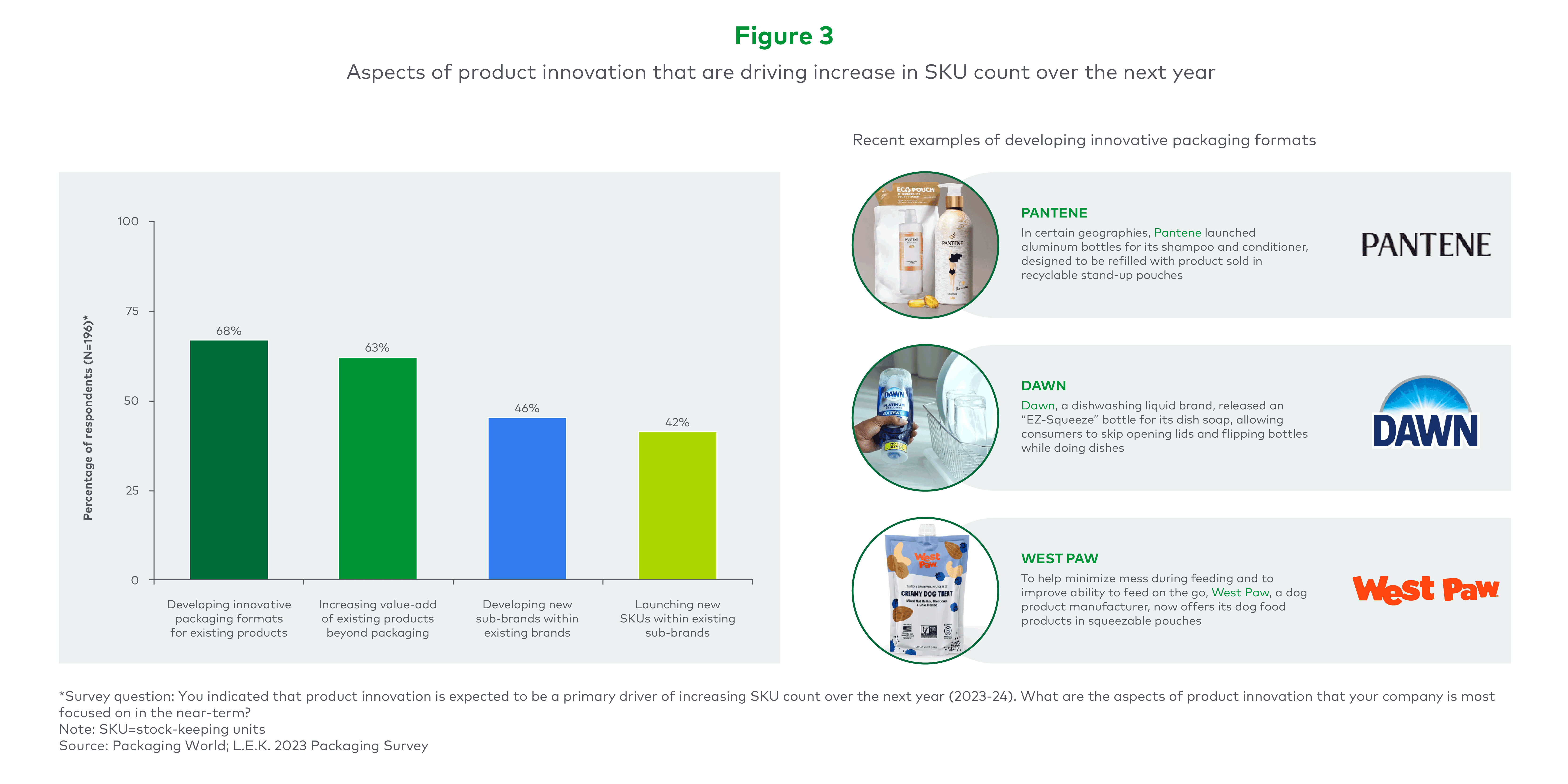

When it comes to the top driver of SKU introduction cited by brand owners for 2023-24 — product innovation — the majority of brand owners cite developing innovative packaging formats for existing products. Other reasons include increasing the value-add of existing products beyond packaging, developing new sub-brands within existing brands, and launching new SKUs within existing sub-brands (see Figure 3).

To learn more, please see our next summary of survey findings, which looks at the packaging sourcing strategies that brand owners are leveraging. Be sure to also read about the latest packaging trends and associated spend as well as the impact various megatrends are having on packaging.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC